Bizfi Secures Additional $20 Million Financing

June 28, 2016Small business capital marketplace Bizfi has secured a $20 million investment from New York-based investment manager Metropolitan Equity Partners, supplementing the $65 million infusion in December last year.

Bizfi said this capital will be used to expand and optimize its funding programs and develop an effective marketing campaign to advertise those better.

“Our relationship has deepened over the past few months and when the opportunity to raise additional capital presented itself, MEP was the most logical partner,” said Stephen Sheinbaum, Bizfi founder.

Bizfi has so far crossed $1.7 billion in financing to more than 30,000 small businesses since 2005 with partners like OnDeck, Funding Circle and Kabbage.

Starting an ISO Shop? Here’s What You Need to do Differently

June 17, 2016 It’s not news that commercial finance brokers are hurting and some are even calling it quits. The industry that didn’t ask for more than a phone and a sharp sales acumen from anyone wanting to start an ISO shop is now stifled with competition. The low barriers to entry that welcomed new companies is causing a seismic shift in the way brokers do business. While some are ready to leave, most are still grappling with the changing times.

It’s not news that commercial finance brokers are hurting and some are even calling it quits. The industry that didn’t ask for more than a phone and a sharp sales acumen from anyone wanting to start an ISO shop is now stifled with competition. The low barriers to entry that welcomed new companies is causing a seismic shift in the way brokers do business. While some are ready to leave, most are still grappling with the changing times.

What’s different about the business now? Almost everything, some say. Gil Zapata who runs a four year old ISO shop, Lendinero, says clients were desperate for money when he started. However he doesn’t think of the competition as fierce but just messy. “There are brokers and ISOs entering and clogging up the system,” he said, “They are obviously fly-by-night and get pulled into it thinking the industry is a fast money maker but it’s really not.”

Competition did what competition does, drove prices and commissions down, costs up and hacked the product. For instance, daily payment ACH loans strongly tied to historical cash flow history didn’t exist. Neither did fancy verbiage for them. The onslaught of online lenders that entered the industry didn’t help either.

OnDeck started selling term loans, which had some similarities to other daily payment products, said Chad Otar, founder of New York-based MCA company Excel Capital Management. “ISOs, on their part have to be careful while pitching these products to clients, explain the contract clearly to avoid penalty.”

The competition has also led to loan stacking, much to brokers’ and lenders’ contempt. And the online lending ilk of Lending Club, Prosper and OnDeck cannot escape it either. Last week, (June 10th), Reuters ran an article calling stacking the latest threat to online lenders where “soft credit inquiries” and “patchy reporting” results in multiple lenders making loans to the same borrower, diminishing the ability to pay.

“Deals become impossible to structure and it becomes difficult for lenders to keep clients on the books when there are second and third names,” said Zapata. The proliferation of loan products that succeeded as a result of competition was a double edged sword. While there are more products to be sold, there are not enough borrowers to lend to.

From a funder’s perspective, that means acquiring and retaining a customer on price rather than an ongoing relationship. “The increased competition has led to commoditization of the MCA,” said Sol Lax, CEO of New York-based business funder Pearl Capital. “It was an exotic financial instrument 5 years ago and the ability to set up shop was restricted. That has changed.”

The ISOs are increasingly reliant on renewals, thanks to the high marketing costs. “A real differentiating factor is whether an ISO syndicates, their default rate, and their renewal rate. All of it is intertwined so that ISOs need to view their business more like investors and less like brokers,” Lax said.

So what would ISOs have done differently? Otar says he would have started an industry coalition similar to the Innovative Lending Platform Association. “I would have tried to pull a Godfather and formed a coalition with other companies and self regulate.”

For Zapata, doing things differently would have meant finding an early backer. “If I had to do this over, I’d have a good investor behind my back,” he said. “Find someone who knows the business and have a good game plan. If you don’t have deep pockets, your chances are minimal.”

New Funder Doing 12-Month Deals With Weekly Payments (Guess Who)

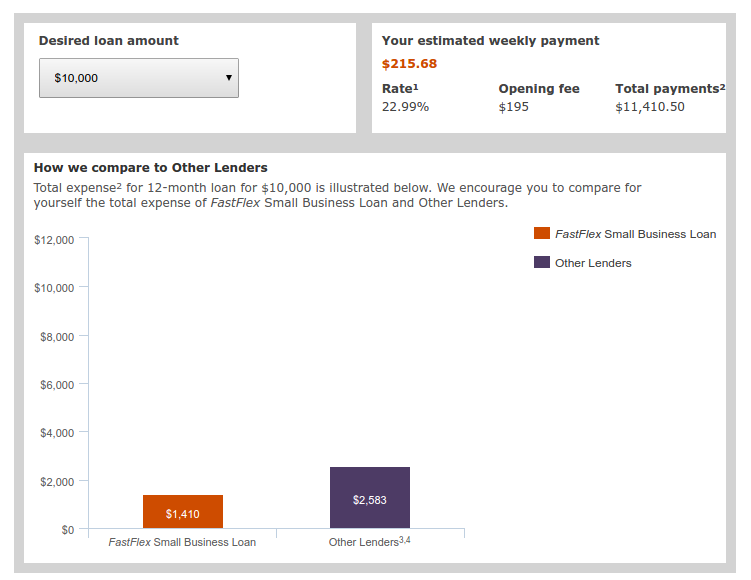

June 3, 2016 Merchants doing at least $4,100 a month in gross deposits are eligible for funding on a 12-month term with weekly ACH debit payments, a new funder revealed. Interest rates start as low as 13.99% but the max funding size is only $35,000. Underwriting decisions can be made instantly online with funds available the next day. “We consider your existing business checking history — not just your credit score,” they advertise.

Merchants doing at least $4,100 a month in gross deposits are eligible for funding on a 12-month term with weekly ACH debit payments, a new funder revealed. Interest rates start as low as 13.99% but the max funding size is only $35,000. Underwriting decisions can be made instantly online with funds available the next day. “We consider your existing business checking history — not just your credit score,” they advertise.

The name of the funder? Wells Fargo Bank.

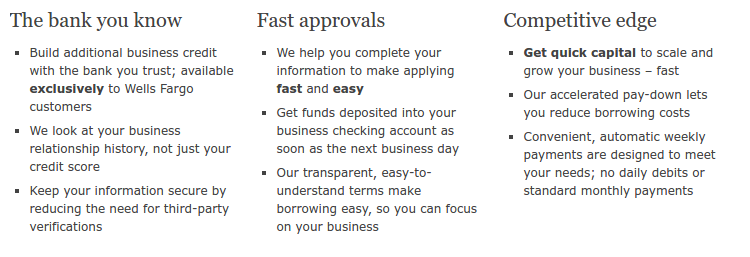

The caveat is that applicants must have banked with Wells Fargo for at least 1 year to be eligible. The upside is that little documentation is required to apply outside of the application. The loan is unsecured and the closing fee is only $195. Dubbed FastFlex, the product is clearly meant to compete against online business lenders because well, they mention CAN Capital, OnDeck, and Kabbage in the footnotes on their loan calculator page.

Using their loan calculator, Wells Fargo estimated a 10k loan on a 1.14 over twelve months with weekly ACH payments.

Wells Fargo’s marketing message sounds awfully familiar:

Next day funding, not just your credit score, weekly payments…

Wells Fargo is not alone in their attempts to attack online lenders. Discover Bank for example, is targeting Lending Club directly. By going after the same borrower profile and offering better terms, Discover hopes to cut into Lending Club’s newfound market share.

Unsurprisingly, it is the non-bank prime lenders that will feel the growing bank threat the most. Companies offering small business loans or merchant cash advances to small businesses with damaged credit or complex situations are unlikely to find their target customer pool become bankable any time soon.

In a first, Bizfi crosses $144 million in Q1 funding

May 17, 2016

Thanks to the partnership with Western Independent Bank, Bizfi had a record Q1 to date with $144 milion in loan originations.

The New York-based fintech company funded 3,605 small businesses, a 49 percent increase from $96 million funded in Q1 last year, Bizfi said.

The partnership with Western Independent Bank in March this year opened up several markets in the midwest and west coast Alaska, Arizona, California, Colorado, Hawaii, Idaho, Montana, Nevada New Mexico, Oregon, Utah, Washington and Wyoming can benefit from this partnership. Referring to the partnership, Bizfi founder Stephen Sheinbaum said, “These types of relationships not only help to fuel Bizfi’s growth, they ensure the financial partner continues to maintain their customer relationships by providing their clients an alternative for the financing they need,”. “In 2016, we’re looking forward to further expanding our product set and partnering with more traditional financiers, enabling us to fund the growth of even more of America’s small businesses.”

Bizfi’s marketplace partners with lenders like OnDeck, Funding Circle and Kabbage and the company has so far funded 29,000 small businesses with $1.6 billion in capital since 2005.

Online Lending APR ‘SMART Box’ To Apply To Loans, Not Merchant Cash Advances

May 5, 2016

OnDeck, Kabbage and CAN Capital have launched an initiative to make online loan shopping easier. Dubbed the SMART (Straightforward Metrics Around Rate and Total Cost) Box, these lenders plan to present small businesses “with a chart of standardized pricing comparison tools and explanations, including various total dollar cost and annual percentage rate metrics that enable a comprehensive pricing comparison of loans of equivalent duration.”

The Box, clearly meant to increase transparency, was explained in an ironically confusing way, particularly where it said it would include annual percentage rate metrics. An Annual Percentage Rate (APR) is indeed a representation of several metrics and thus it wasn’t clear if the Box would just include some of these individual metrics and conveniently leave out the APR itself.

OnDeck CEO Noah Breslow for example told Forbes only six months ago that annual terms don’t make sense. “The APR overstates the actual cost of the loan to the borrower,” he said. He was not alone in thinking that way. Several studies have concluded too that merchants don’t always even know what APR represents. Lendio for example, found that two-thirds of small businesses selected the total dollar cost of a loan as the easiest to understand. Only 17.4% said the APR was the easiest.

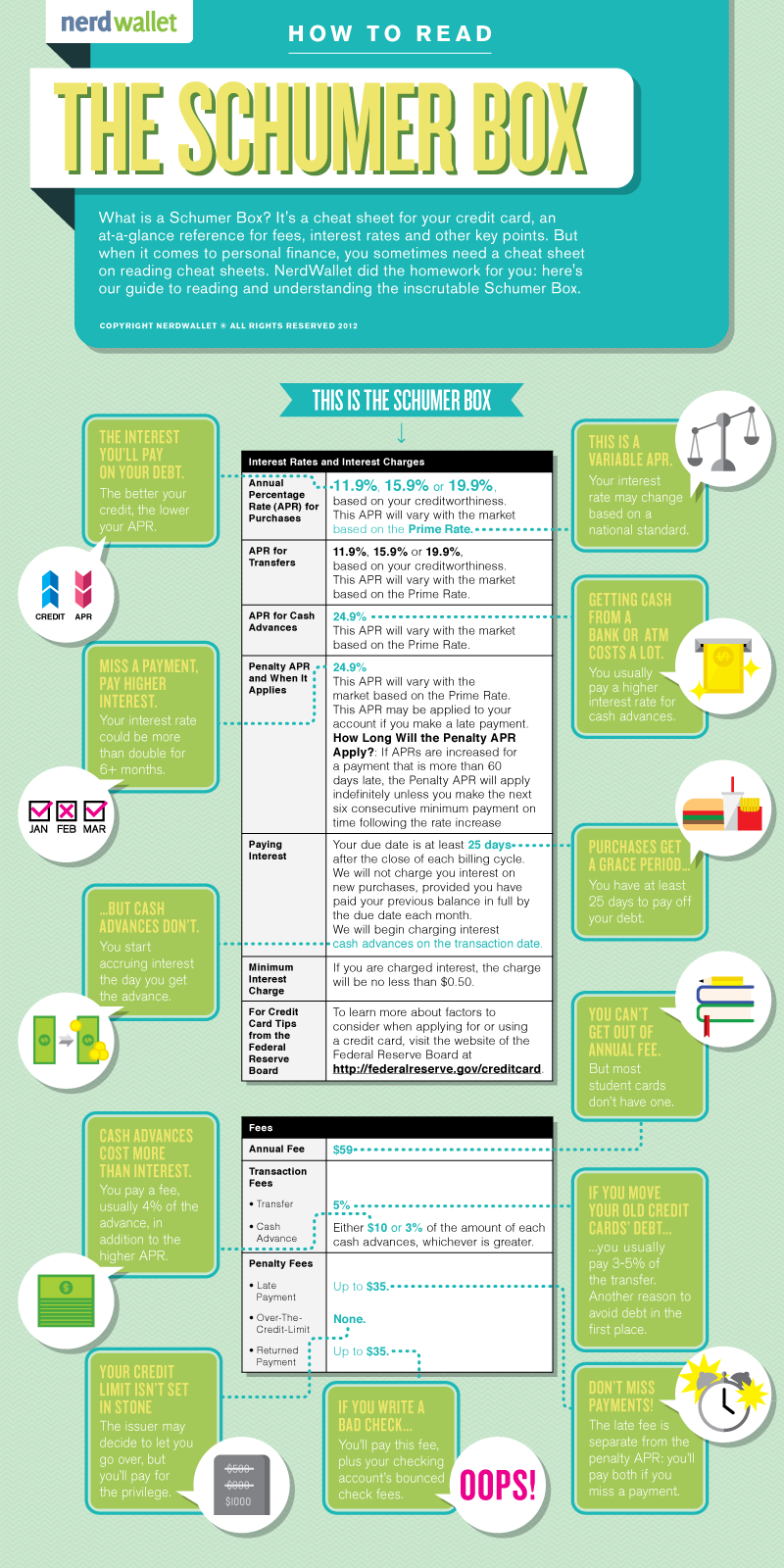

And there’s another thing, the fact that CAN doesn’t just do loans, they also do a significant amount of merchant cash advances. What role could an APR have there? While the Box’s final system won’t be decided until after the conclusion of a 90-day national engagement period that begins next month, one can only imagine that it might have a Schumer Boxer feel to it.

A Schumer Box explained:

Via: NerdWallet

The syntactic ambiguity in the announcement however was unintentional. A spokesperson for the group (Known as the Innovative Lending Platform Association) said that the SMART Box will indeed include Annual Percentage Rates.

But that’s where loans are concerned…

When AltFinanceDaily asked about merchant cash advances, Daniel Gorfine, vice president and associate general counsel of OnDeck; Parris Sanz, Chief Legal Officer of CAN Capital and Azba Habib, assistant general counsel of Kabbage, submitted the following joint response:

“As part of the SMART Box initiative, we are interested in engaging with providers of MCA products. Based on consistent assumptions about a small business’s future sales volumes and its ability to deliver the contracted amount of receivables within the period of time estimated during underwriting, the SMART Box could apply to MCA products.”

So long as SMART Box disclosure is voluntary, an MCA company could perhaps employ their own version of it. It just might come sans APR given the product’s history with state regulations. The Association is emphatic however that this concept could be used by MCA companies and others in the small business financing space. After all, the initiative is rooted in transparency for the small business owner, they say.

In September, the Association “will encourage those interested in promoting the responsible development of the small business lending industry to voluntarily adopt or support the model disclosure.”

Given the level of influence these companies have on the industry, the voluntary nature of the SMART Box has the potential to spark an industry-wide box revolution. MCA companies however would need to structure transparent disclosure around their contractual frameworks. But even that could be a good thing. One commercial financing broker for example, posted a redacted service fee agreement to the DailyFunder forum earlier this week that purported to show another broker trying to charge a merchant a 26% premium (26% of the funding amount) for their work. Despite this unusually high cost, the charge itself was hard to find, hidden among fine print on an otherwise benign looking page. Naturally, others in the industry did not respond kindly to it. Even other brokers referred to it as “outrageous,” “nonsense,” or “bs.”

Their reactions make clear that there is a desire for transparency even among the group most often blamed for the lack thereof. Some of the industry’s forward thinkers have told AltFinanceDaily that a system like a SMART Box is the future of the industry whether one agrees with it or not. And if not for the sake of small businesses and regulators, then for the sake of being able to compete fairly against companies that may be relying on truly hidden fees.

SMART Box. All aboard the transparency train?

Online Small Business Lending Task Force Initiated by the ETA

April 30, 2016 The Electronic Transactions Association (ETA) is now advocating on behalf of online small business lenders.

The Electronic Transactions Association (ETA) is now advocating on behalf of online small business lenders.

Though you might not have suspected it last week at Transact16, the ETA very much plans to involve themselves in the affairs of marketplace lending. That might not have been obvious from a Bloomberg article that reported that OnDeck, Kabbage and PayPal were forming a splinter organization as an “extension” of the ETA known as the Online Small Business Lending Task Force. Referred to as a new initiative in the announcement, the group’s mission is described as striving to “prevent hasty or overly restrictive regulations.”

But the group’s named lobbyist, Scott Talbott, is also the ETA’s lobbyist. And the three lenders named, were already members of the ETA. When Talbott was asked by AltFinanceDaily to clarify the relationship between the “task force” and the ETA, he said that the two weren’t separate. The “ETA organized its members to lobby on the issue. It’s what we do every day,” he wrote.

The “task force” merely highlights members in the trade group that share a common interest.

Formed in 1990 and comprising of over 550 companies across 7 countries, the ETA has served the payments industry well. OnDeck, Kabbage and PayPal therefore find themselves in good company and led by advocates with well-established government relationships.

Along with the ETA, the online small business lending industry has found support from the Marketplace Lending Association, the Small Business Finance Association, the Commercial Finance Coalition and the Coalition for Responsible Business Finance.

Shark Tank’s Kevin O’Leary Has a Man-to-Man Talk About Alternative Lending

April 26, 2016Yes, it’s an IOU Financial commercial, but given Kevin O’Leary’s business celebrity persona, roles on Shark Tank and Dragons’ Den, authored books, and regular contributions on CNBC, he’s certainly qualified to sympathize with small business owners on the difficulties of obtaining a loan.

Kevin O’Leary is not the only shark to support alternative lenders. His co-hosts have served as spokespeople for IOU’s competitors:

- Barbara Corcoran – OnDeck

- Lori Greiner – Kabbage

- Kevin Harrington – Ventury Capital (actually as a co-founder of this company)

And don’t forget of course the merchant cash advance guys who actually were contestants on Shark Tank themselves:

California DBO Releases Report on Alternative Lenders

April 15, 2016 The results of a survey that the California Department of Oversight issued late last year to 14 alternative lenders are in. Affirm, Avant, Bond Street, CAN Capital, Fundbox, Funding Circle, Kabbage, LendingClub, OnDeck, PayPal, Prosper, SoFi and Square all responded. CircleBack Lending declined to take it.

The results of a survey that the California Department of Oversight issued late last year to 14 alternative lenders are in. Affirm, Avant, Bond Street, CAN Capital, Fundbox, Funding Circle, Kabbage, LendingClub, OnDeck, PayPal, Prosper, SoFi and Square all responded. CircleBack Lending declined to take it.

The DBO requested data on term loans, lines of credit, merchant cash advances, factoring transactions and other products.

Other than determining that billions of dollars are being deployed from these companies, they found that median consumer loan APRs ranged between 5.37% APR and 35.94% APR. For businesses, the median APR ranged from 18.56% APR to 51.40% APR.

The number of delinquent (30 days or more past due) consumer financing dollars as a share of total dollars outstanding ranged from .99% to 20.30%

The number of delinquent business financing dollars as a share of total dollars outstanding ranged from .55% to 6.79%.