Is Alternative Lending An Illusion? (LendIt 2015 Summary)

April 18, 2015More than 2,400 people packed into the LendIt conference last week in New York City and everywhere you turned, startups were boasting of their ability to lend billions of dollars to underserved consumers and businesses. Companies not even old enough to have attended last year’s LendIt conference had reportedly lent tens of millions or hundreds of millions of dollars already. Is it all an illusion?

Investors circled like hawks to try and grab an opportunity into this exploding market. Alternative lenders were practically being tackled by VCs, Private Equity firms, and specialty finance lenders:

Technological innovation is disrupting the status quo, attendees echoed. Surely banks can afford to develop new technology to compete, so why haven’t they? Lendio’s Brock Blake wasn’t afraid to challenge the Short Term Business Lending Panel on this. “Is there real innovation happening or is there regulatory arbitrage?” he asked.

The panelists mostly agreed that it was a combination of both. Stephen Sheinbaum, founder of Merchant Cash and Capital (MCC) and BizFi, said “regulation is not something that scares us in any way.” That’s not surprising considering MCC has survived more than ten years in business and fellow panelist CAN Capital has survived more than seventeen.

But for the newer players entirely reliant on third party brokers or dependent on a Reg D exemption to issue securities, their success may indeed be regulatory arbitrage. And time is on their side.

Karen Mills, the former head of the Small Business Administration asked several regulatory bodies who would stand up to oversee small business lending. “No one stood up,” she said.

It’s the brokers that worry some folks most, an issue that PayPal and Square Capital do not have to contend with at all. OnDeck CEO Noah Breslow stated, “there is always going to be a set of customers that want to shop and want to have help.”

Kabbage’s Kathryn Petralia explained that only 2% of their business comes from brokers and their fees are capped at 4%. CAN Capital’s Jason Rockman argued that it’s about working with brokers that share their values. MCC’s Sheinbaum said, “you have to be willing to not do business with some of the unscrupulous players out there.”

But while these industry captains minimized the role that brokers play, 2015 is already being dubbed the Year of the Broker.

The regulatory environment isn’t the only issue to be worried about, skeptics argued. There was cautious alarm about the market’s viability when interest rates rise or the economy takes a turn for the worse.

“I think there’s going to be a shakeout,” said Steve Allocca of PayPal. MCC’s Sheinbaum explained that when he sees other funders doing deals that don’t appear to make sense, to not feel pressured to do them as well. “Stick to your disciplines. Stick to your guns,” he preached.

Fundation CEO Sam Graziano argued that small business lending is already very risky. The lifetime default rate on 7(a) SBA Loans is 20%, he said. Graziano, who hates the term alternative lending prefers to refer to the industry as digitally enabled lending.

And digitally enabling is something that OnDeck has focused on. In Breslow’s presentation, he said that applying offline for a loan takes 33 hours of work on average. Banks are shuttering branches at a record rate, he added.

Banks are dead, said many in attendance. Kathryn Petralia of Kabbage disagreed. “The death of banks has been greatly exaggerated,” she argued on a panel.

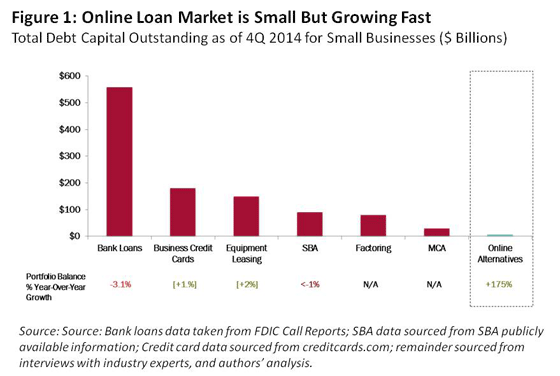

Indeed, Mills’ report shows that total outstanding debt on business loans by banks dwarfs the alternatives by more than 50 to 1.

But former U.S. Treasury Secretary Larry Summers is convinced the tide is turning.”The conventional financial sector has, in important respects, let all of its main constituents down over the last generation, and technology-based businesses have the opportunity to transform finance over the next generation,” he said during the keynote speech.

With conference sessions looking and feeling like a cramped NYC subway during rush hour, the popularity of alternative lending is no illusion.

But healthy skepticism is at least creeping in while the industry marches forward. Changes in regulations, interest rates, and economic activity will separate those simply riding a wave from those that have created something real. Expect companies that exhibited at this year’s conference to be gone by 2016 or 2017, said several panelists.

The final count of LendIt attendees was 2,493 people. 150 people who tried to register at the last minute were turned away. More are expected to attend next year.

Objectively, alternative lending appears to be very real.

Rand Paul Accepts Bitcoin

April 7, 2015 Bitcoin’s got a real fan! Senator Rand Paul is now accepting bitcoin as one way to attract donations for his presidential campaign. And regardless of whether or not you agree with his views, I did at the very least make a donation on the basis that I am a believer in bitcoin.

Bitcoin’s got a real fan! Senator Rand Paul is now accepting bitcoin as one way to attract donations for his presidential campaign. And regardless of whether or not you agree with his views, I did at the very least make a donation on the basis that I am a believer in bitcoin.

Donating to Paul’s campaign by bitcoin is one of three payment options. The other two are credit card and paypal. He is able to accept bitcoin via BitPay, a company I just mentioned a few days ago.

How would I describe the experience of donating to Rand Paul for president using bitcoin?

Insanely simple!

By law, Paul will have to convert any bitcoins received into dollars before using them. Too bad…

Announcement: Dwolla partnership U.S. Treasury

February 19, 2015Company Announcement

Dwolla to help U.S. Treasury go paperless, prepare for a secure digital future

Each year the The U.S. Department of the Treasury’s Bureau of the Fiscal Service collects 400 million transactions worth $3.7 trillion. Ensuring that its collection programs stay relevant, safe, and cost-effective, they recently launched a new Digital Wallet program. The new initiative aims to modernize the way our country collects and distributes payments through the convenient offering of safe and innovative payment options. In June of 2013, the Digital Wallet initiative issued a request for proposal, asking national payment platforms to help the 225-year-old Treasury Department improve its flagship revenue collections product, Pay.Gov.

Each year the The U.S. Department of the Treasury’s Bureau of the Fiscal Service collects 400 million transactions worth $3.7 trillion. Ensuring that its collection programs stay relevant, safe, and cost-effective, they recently launched a new Digital Wallet program. The new initiative aims to modernize the way our country collects and distributes payments through the convenient offering of safe and innovative payment options. In June of 2013, the Digital Wallet initiative issued a request for proposal, asking national payment platforms to help the 225-year-old Treasury Department improve its flagship revenue collections product, Pay.Gov.

With existing partnerships with Microsoft Government and state administrations, Dwolla’s flexible architecture makes for an ideal partner in helping modernize public payments. Today, we’re excited to announce our selection as the U.S. Treasury’s first Digital Wallet partners, alongside PayPal (and ApplePay).

What is Pay.Gov? It’s smart government.

Nearly 200 federal agencies, ranging from the Department of Interior to the Department of Defense, use the U.S. Treasury’s Pay.gov platform to create and host custom online payment forms, collecting over 100 million transactions worth approximately $110 billion per year. These simple forms, which hide a sophisticated software and accounting system, allow federal agencies to collect and track non-income tax payments for things like climbing Denali or court fees. It’s a lot like Dwolla Forms, but made exclusively for the federal government.

By outsourcing their revenue collection needs to Pay.Gov, federal agencies not only provide taxpayers an improved experience but also streamline their own payment operations. In doing this, they reduce the operational costs, inefficiencies, and foregone payments. Simply put, Pay.Gov increases revenue for agencies and saves taxpayers money.

How is Dwolla involved? How would this impact me?

Dwolla is now a live payment option for many US agencies (and this will grow over time)–allowing any taxpayer with a U.S. bank or credit union account to use Dwolla’s simple and secure online checkout experience to pay for a whole host of federal fees, products, and permits.

No cards. No checks. No pre-existing Dwolla account required. No sharing of sensitive payment information with the federal government.

What is Dwolla? A secure and modern way to make bank transfers.

When we began building the Dwolla payment network in 2008, we set out to create the ideal way to send money. What we quickly found is that the ideal way to move money has changed since the 1960s and 70s, and the only way to solve the problem was to start over.

Starting fresh with over 40 years of technological advancements, Dwolla was able to create an end-to-end payment network that modernized the legacy bank systems—making it easier to use, more accessible, and more secure. Today, we work with anyone or anything connected to the Internet, from solopreneurs to publicly traded companies, exchange infrastructures to software developers, state governments to financial institutions. We help our community rethink their payment operations, product offerings, and user experiences.

Create new standards in security and privacy: Dwolla has baked new technologies into its network, like authentication and tokenization, that eliminate sensitive financial information from a typical transaction.

Solve problems for all: Free turnkey products, like MassPay or Dwolla Forms, make it easy for anyone to send or receive funds without any existing technical know-how, while a healthy library of developer docs and APIs make it easy to plug Dwolla into nearly any platform, existing operation, or your own creation. Additional levels of support and customization are available and affordable.

Create a powerful, but flexible infrastructure: A simple, and dynamic platform, Dwolla was designed to handle the unique considerations of governments.

Create a platform for future innovation: Whether its mobile applications, real-time payments, or tokenization, Dwolla benefits are freely accessible via our API and developer documentation, allowing the network to scale and solve for the unique needs of an evolving payment landscape.

So what Dwolla can do for you? Grab a brochure from Dwolla.com/government or sign up for our upcoming webinar by emailing government@dwolla.com.

A Bitcoin Moment

February 1, 2015 I had a moment recently. It was late at night and I was ready to hit the hay.

I had a moment recently. It was late at night and I was ready to hit the hay.

“Oh wait, there’s something I need to get out of the way,” I told myself.

I had kept delaying the purchase of a new printer cord to replace the one I mangled. It was time to end that procrastination now! Even though it was 1 AM, I was sure that it would only take a few minutes to place an online order and I summoned the motivation to go for it.

Addicted to Amazon’s 1-Click ordering feature, I was bummed to discover they didn’t have the cord I needed. With no time to waste, I used Google to find a site that did carry it.

Found one.

Add to shopping cart.

Select payment method.

Ugh…

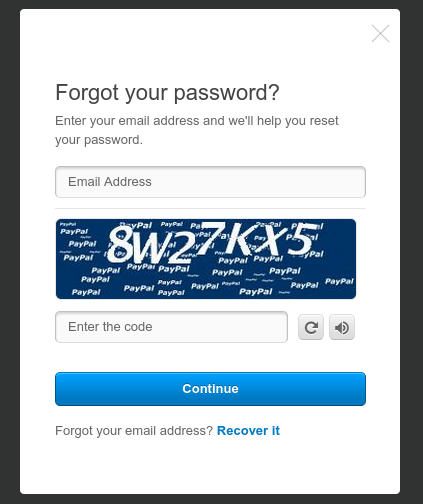

I didn’t have my credit card number memorized and I looked across the unlit room to see if my wallet lay nearby. It was somewhere in a pile on the coffee table, or maybe it was upstairs, or maybe I left it in my pants pocket. Unsure and too tired, I selected PayPal to speed things up, a service I hadn’t used in a while.

Incorrect password.

Incorrect password.

Ugh…

I entered my email address and completed a captcha.

No email…

Refresh email.

Still nothing.

Refresh email again.

Nothing.

Agitated, I started Googling for help about not receiving a PayPal password reset email and instead ended up on a message board where people griped about PayPal in general.

After perusing that forum like a zombie, I got up and walked around. My wallet wasn’t downstairs or at least I couldn’t find it.

Thirty six minutes had gone by since I first encountered the checkout screen. I stopped caring about the cord and I resolved to never print anything ever again.

Before shutting down the computer for the night, I checked my phone. The only news alert I had was about bitcoin. I laughed out loud and went back to the checkout screen. Bitcoin was a payment option. I selected it, copied and pasted the payment address and sent bitcoins stored on my computer to it.

Order placed.

—–

tl;dr

I needed to buy a cord online. Credit card was out of reach. PayPal password was forgotten. Bitcoin saved Gotham.

Mayor Rahm Emanuel Declares War on Merchant Cash Advance

January 16, 2015 FOX 32 in Chicago is reporting that Mayor Rahm Emanuel is going on the offensive against merchant cash advance companies. Specifically it says,

FOX 32 in Chicago is reporting that Mayor Rahm Emanuel is going on the offensive against merchant cash advance companies. Specifically it says,

Mayor Rahm Emanuel will call on state and federal agencies to regulate business to business lenders. Emanuel said cash advance companies have accelerated their marketing efforts in recent months, resulting in small businesses taking loans they cannot afford.

The article states that business owners have turned to the City of Chicago for help in paying back loans with high rates of interest.

While the mention of APRs reaching into the ranges of triple digits is supposed to shock you, one business lender that charges such rates recently went public and had been backed by Google Ventures, Fortress Investment Group, Goldman Sachs, and Peter Thiel.

Less than 30 days ago we were celebrating these companies as the solution to a problem that has plagued small businesses for all time, access to capital.

While Emanuel is obviously famous for being the 23rd White House Chief of Staff and Obama’s right hand man for a period in his first term, he is not the first mayor to consider the role merchant cash advance companies and high interest business lenders have in cities across America.

All the way back in 2008, the U.S. Conference of Mayors (USCM) adopted a resolution titled, Protecting Main Street Small Business Owners from Predatory Lenders, from which some of the excerpts below are from:

WHEREAS, merchant cash advance companies have already lent approximately $2 billion at egregious rates and have been quoted in leading main stream media publications such as Forbes, Business Week, Dallas Morning News, and American Banker claiming that their new originations have increased 75% in the first half of 2008

WHEREAS, as with payday lenders and predatory lenders in the home mortgage community, Mayors need to take a leadership role to scrutinize predatory merchant cash advance companies, educate small business owners of the dangers posed by these firms, and increase awareness and promotion of alternative, more affordable funding sources to support this vital segment of our economy

BE IT FURTHER RESOLVED, that to protect the general health and viability of their small business communities, cities should investigate whether they can effectively regulate or ban merchant cash advances.

3 months after this resolution was passed, Lehman Brother’s collapsed and the economic crisis was in full swing.

According to a few industry leaders familiar with the 2008 mayoral resolution, UCSM privately retreated from their stance when all other types of commercial lending had dried up. Their seeming reversal, though not publicly stated invited merchant cash advance companies into their communities at the moment when Main Street was arguably at its weakest.

According to a few industry leaders familiar with the 2008 mayoral resolution, UCSM privately retreated from their stance when all other types of commercial lending had dried up. Their seeming reversal, though not publicly stated invited merchant cash advance companies into their communities at the moment when Main Street was arguably at its weakest.

Who do they think rolled up their sleeves and kept local economies alive when things were at their worst?

While non-bank funding can obviously be expensive, countless business owners have praised merchant cash advances in particular as a solution that came through when none other were available.

Emanuel will learn that companies such as Square and PayPal are part of the crowd that provides merchant cash advances. This is not a shadow industry. Non-bank business-to-business financing is already becoming less expensive nationwide.

According to Fox, the Commissioner of the Chicago Department of Business Affairs and Consumer Protection said the goal is to offer small business owners loans at affordable rates with full disclosure.

Merchant cash advance companies would undoubtedly feel the same way. The dilemma is that advocates of affordable rates tend to really mean single digit rates. When single digit rates are not possible given the risk, they seem to argue that no financing should be given at all, leaving the business to fail or miss out on an opportunity. That’s the exact type of flawed thinking alternative financing companies address…

Ironically, a report from the Federal Reserve Bank of Cleveland last week concludes that small business job creation is lagging with a possible culprit being a lack of access to credit.

Coming out of the most recent recession, however, job creation by small businesses has lagged, and the new business formation rate continues to fall. While it is not clear that these trends are driven by weaker borrowing or limited access to loans, it is evident that businesses need adequate credit to succeed and grow. As such, policy makers should not lose sight of the trends related to small business credit, even with the recent positive reports showing improvements.

And of course in a supposed exposé on merchant cash advances that aired on Chicago Public Radio in November, clips of an interview I did with them were aired to fit the narrative of merchant cash advance as predatory. When asked by the interviewer what a small business owner should do if they didn’t understand a contract, I advised that they hire an attorney or an accountant, and if they couldn’t afford those then to find somebody they felt qualified to offer an opinion. “They should always get a 2nd set of eyes to review a contract if they don’t understand,” I said.

My advice did not air, nor did my explanation that there were two separate types of products that they were confusing as one, one being loans and the other being purchases of future receivables. I suppose it didn’t fit the characterization they were going for.

As quoted in Fox, Financial Advisor Kent Travis advised business owners to “read the documents, don’t sign anything on the spot, make sure you read it thoroughly and if you have trouble understanding it seek the advice of an advisor, CPA, an attorney or a financial planner.”

I couldn’t have said it better myself because I already did.

And in an interview I had with former Congressman Barney Frank, a chief architect of the Dodd-Frank Wall Street Reform and Consumer Protection Act, Frank voiced his opposition to regulations on business-to-business lending in early 2014.

There’s one thing the Fox story does mention that’s hard to argue with and that’s the need for greater transparency. I am all in favor of that.

—————–

For those that haven’t already signed up, this is a reminder that the Law Office of Pepper Hamilton LP is hosting a lunch at their office in New York on January 27th to specifically discuss the merchant cash advance industry’s future.

Interested in discussing legal issues, best practices, and the path forward for alternative business financing? Are you an ISO or funder interested in sharing your thoughts? Send me an email to let me you know if you’d like to attend. sean@debanked.com.

—-

Watch the Fox news report about merchant cash advances:

My Journey to Bitcoin

November 30, 2014 Count me amongst the libertarians, anarchists, and digital lunatics. I made an online purchase using bitcoin… and it was insanely easy.

Count me amongst the libertarians, anarchists, and digital lunatics. I made an online purchase using bitcoin… and it was insanely easy.

The first person I shared my experience with was a friend who works in automotive manufacturing, someone who operates outside the world of alternative finance. He thought I was crazy or rather he was more confused than anything. “Wait, bitcoin?” he asked. “I thought that was a scam that went out of business two years ago.”

Stunned by his remarks and disappointed with his lack of excitement for me, I told a few more friends about what I had accomplished. They had all heard the term, but none of them knew what it was. Oddly, most seemed to believe that bitcoin had already been revealed as a con and was something from years past, a scheme that came, got hacked and failed.

Not so long ago I was in their shoes. I received my first education in bitcoin this past fall, September 22, 2014 to be exact at the 3rd Annual Tomorrow’s Transactions NYC Unconference hosted in Google’s New York headquarters.

It’s a con?

Famous money laundering expert and author Jeffrey Robinson gave a blistering assessment of bitcoin the currency, which he described as a hoax perpetuated by “libertarian anarchists.” His contentious indictment was half warning, half sales pitch for his latest book, BitCon, which I bought the day it was released.

Robinson argued that bitcoin adoption, while minuscule, was still greatly exaggerated.

There are fewer card-carrying members of #BitcoinCanada than #Starbucks in #Calgary. BitCon: http://t.co/lQecBgwRdp

— Jeffrey Robinson (@WritingFactory) November 2, 2014

He explores several challenges in his book, one of which can be summed up as:

Why would someone exchange dollars into bitcoin only to have to convert their bitcoin back into dollars?

It’s a great question, but it’s something I’ve done every time I’ve traveled abroad. Dollars to euros and then euros back to dollars. Dollars to pounds, dollars to canadian dollars, etc. But why do an exchange at all when the counterparty prices their goods or services in dollars?

Spend $ to buy #bitcoin to pay for #Blackfriday stuff priced in $. Where's the logic? #BitCon— Jeffrey Robinson (@WritingFactory) November 29, 2014 http://t.co/U26d35G0u9

Benefits

Assuming bitcoin’s value against the dollar wasn’t volatile, I can think of three immediate reasons:

1. I don’t have to enter in my credit card number on a website and risk it being hacked or stolen.

2. I can make a payment online if I don’t have a credit card or debit card.

3. I can spare the merchant the payment processing fees.

Let’s forget about point one for now because it’s easy to overlook the pervasiveness of point two. According to the FDIC’s latest National Survey of Unbanked and Underbanked, 25 million people in the country do not have access to a bank or banking products at all. Poverty is a main driver of that but curiously 34.2% of respondents in that group cited that they don’t like dealing with banks or don’t trust them as a reason. 30.8% said that account fees were too high or too unpredictable.

And that’s just the unbanked. 1 out every 5 households in the country is underbanked. They have a bank account but have also obtained financial services and products from non-bank alternative financial services providers in the prior 12 months.

To those of us that rely on banks for everything this may seem extreme, perhaps even downright unbelievable. Coincidentally, Robinson wasn’t the only notable figure at the New York Unconference. He was joined by Lisa Servon who later spoke about her hands-on experience with the unbanked and underbanked. A professor of urban policy at the New School in New York, Servon got a job as a check casher/payday lender in a storefront on a busy corner in downtown Berkeley, California to learn about these households on the front lines.

Consumers can be intimidated by banks she said at the Unconference, especially minorities. Even people who can afford to use banks opt not to. A sample of her experience was published a month ago in the New York Times.

Moving on to point three, accepting bitcoin can either be free or vastly less expensive than accepting a credit card payment. Payment processing fees are significant in commerce. I know this because I accept credit card payments through both Square and PayPal in another business I run and it costs me nearly 3% per transaction. I’ve also sold merchant processing for years and have priced hundreds if not thousands of accounts.

You know that thing American Express invented called Small Business Saturday where consumers are encouraged to spend money at small businesses? Paying with your AMEX card is encouraged of course and AMEX charges about 3.5% to the merchants on every sale.

By going dollars->bitcoin->dollars, you can do even more to help small business by saving them the fee. Granted, most consumers probably wouldn’t jump through any hoops to save a business money especially if it meant trying to figure out how to convert your dollars into something they perceive as “a scam that went out of business two years ago.”

I’ve read all the warnings about bitcoin already and have even been lectured by Robinson personally:

@financeguy74 A fool and his money… the numbers don’t lie. Enjoy Vegas.

— Jeffrey Robinson (@WritingFactory) November 4, 2014

and yet what intrigued me most about bitcoin aside from the transaction costs, was the fact that it was not run by a government.

What if?

Five years ago I had a sinking feeling. The safety and security of the U.S. economy was put to the test. Stock prices fell, lending dried up and millions of Americans actually began to ask themselves, what if? As in what if the dollar collapses? What if your bank account suddenly became worthless? What if you had to suffer for the mistakes others in your country made?

In 2009, a colleague and I pledged to stick together should an eventual economic apocalypse happen. Our plan was simple:

1. Exchange all our money for a gigantic gold brick and two shotguns

2. Sit on gold brick and guard it with those shotguns

Survival would remain possible by chiseling off pieces of the gold brick and exchanging them for food and water. We’d each take turns sleeping and hopefully survive until things returned to normal, if ever.

A fantasy to be sure, and it was great for laughs to break up the day, but what if?

My apocalyptic paranoia is one of many stereotypes of the bitcoin faithful, but I have no interest in exchanging 100% of my dollars to bitcoins. And no, I don’t think the dollar is going to collapse tomorrow. I am intrigued however by a currency that eludes governmental control. We can all keep a gold brick in our back pockets, even if it’s small, and even if it’s digital. If for no other reason, it’s a small hedge for peace of mind.

It’s quite ironic that while critics talk up the dollar’s superiority and the strength of the U.S. government, only 14% of Americans approve of how Congress is handling its job. Not to mention that the nation is at this very moment $18 trillion in debt, a number very unlikely to be made whole. Remove the term bitcoin from the conversation and it’s quite likely the average person would at least be amenable to the possibility of a non-governmental currency.

Perhaps as Americans we are somewhat blind to risks, that we feel nothing catastrophic could possibly to happen to us. To many it is literally unthinkable. A completely independent currency has its merits both now and in far bleaker times.

Of course should the apocalypse occur and all you have is bitcoin, rest assured you will be able to buy a shotgun since you can pay for them with bitcoin:

The get rich quick crowd

Here lies another criticism of bitcoin, that everyone is holding it and no one is spending it. Far from idle, there are currently more than 80,000 bitcoin transactions per day. Without prohibitive transaction fees though, volume is a poor measure of adoption since I could easily send bitcoins back and forth between accounts I own and classify them as transactions.

There are indeed those holding and not spending. Rampant speculation is both a cause of volatility and an argument for its long term unsustainability. Speculators are hoping the digital currency will appreciate and make them filthy rich. If that day never comes, a big sell off will cause its value to drop.

And therein lies the argument… when or if the speculators leave, will that spell the end of bitcoin?

If bitcoin had no practical uses outside of being another digital currency like World of Warcraft gold, then bitcoin would likely be a con, a predictable one that probably would’ve combusted already.

There may actually be a massive market correction in the future. At the current moment, Coinbase reports that 1 btc = $376.23. On November 14th, I paid $397 for 1 btc. It lost about 5% of its value in two weeks, a tough percentage to stomach for the faint of heart, and most certainly the average consumer. It’s also equal to the plunge the S&P 500 took between October 8th and October 16th so such short term volatility exists in other mainstream assets.

I’m not necessarily speculating though. I spent almost half my bitcoins shopping on Overstock on Black Friday, an experience I will detail in another post. A 5% swing might be acceptable for an investment but it’s quite ugly for a currency and this fuels the misinformation that bitcoin is a scam, con, or has already gone out of business two years ago.

1 btc could drop to $100 or $10 after a furious market shakeout and it wouldn’t change how I felt about it. It could also rise back up to $1,000 or higher. That volatility is enticing, almost sexy, but it’s the lack of transaction fees and governance by mathematics rather than actual governments that have me hooked

White knight

Still, bitcoin is waiting for a few white knights, merchants willing to price their goods and services in bitcoin. For years, I have priced advertisements on this website in dollars, but to show my support, I will soon be pricing them in bitcoin going forward. Dollars will still be accepted of course, but those Paypal fees hurt. Paypal costs me 3% in a split second. Is a 5% loss in bitcoin value over two weeks really that wild by comparison?

Still, bitcoin is waiting for a few white knights, merchants willing to price their goods and services in bitcoin. For years, I have priced advertisements on this website in dollars, but to show my support, I will soon be pricing them in bitcoin going forward. Dollars will still be accepted of course, but those Paypal fees hurt. Paypal costs me 3% in a split second. Is a 5% loss in bitcoin value over two weeks really that wild by comparison?

I think not.

Bitcoin is more than a currency. It’s not the euro, the yen, or the peso. It’s a detachment from governments and banking. It’s self-control. Without the private key, your bitcoins can’t be seized.

We live in a world today where everybody has their hand in your money. Just look at what happens when you pay for a cup of coffee using your credit card. The following parties all get paid a percentage:

- The small business owner

- The small business owner’s merchant account representative

- The merchant account representative’s company (the ISO)

- The payment processor (the processor settling the transaction)

- The acquiring bank (the payment processor’s bank that is authorized to use the payment networks)

- The payment networks (Visa, mastercard, etc.)

- The customer’s card issuing bank (The bank that issued the card to the customer gets a percentage of every sale made with that card)

- The state (where there is sales tax)

If you thought bitcoin was insane, what do you call a system where eight parties need to get paid to facilitate the sale of a cup of coffee? And my example was simple. There are typically more parties involved that that.

I don’t want to give the impression that you can evade taxes with bitcoin. I have every intention to stay on the up and up with governments. But remove the tax man and the merchant from the equation, and one has to wonder what the heck is going on with the other six parties, all of whom will ultimately decide if your transaction is acceptable to them. They decide, not you. They can freeze your funds if they don’t like the transaction and they do. It happens to merchants all the time.

Your money is not really yours. You have rights to it, but only to an extent. It can be garnished, frozen or confiscated. That’s the price of liquidity and relative stability. If you can afford to color outside the lines, where you can remove the six bankers and their control, why not experiment? There’s something pure about it, liberating. And when you add in the fact that it’s governed by math, it’s more than that, it’s beautiful.

deBank

If you are under the impression that bitcoin is intimidating, a scam or out of business, well then I encourage you to step out of governments for a minute, to deBank, and take a walk on the digital side. I’m not going to convert all my dollars to bitcoin and you shouldn’t either. Try it out with some extra cash.

If you are under the impression that bitcoin is intimidating, a scam or out of business, well then I encourage you to step out of governments for a minute, to deBank, and take a walk on the digital side. I’m not going to convert all my dollars to bitcoin and you shouldn’t either. Try it out with some extra cash.

Sure, you’ll be in company with libertarians, anarchists, and lunatics. And yes, there’s the paranoid, the speculators, and those transacting in illicit goods and services. The beginning of the Internet and computers was much the same way with the unix and linux faithful.

Perhaps bitcoin needs a Steve Jobs, a Bill Gates, to package up something simple and suitable for the average household. Every American would appreciate squirreling away a little something that is out of reach of government and banks.

The vast majority of Americans already don’t trust congress, and 92 million Americans are already underbanked or unbanked. In 2014 buying a cup of coffee involves paying eight people and the government has spent $18 trillion that it doesn’t have. You have to start to wonder who the real lunatics are. Consumers are waiting for something… even if it’s just a little peace of mind, a hedge, a gold brick in their back pocket, the feeling of independence, freedom, control. Something…

I AltFinanceDaily and loved it. Now it’s your turn.

Industry Takes ALS Ice Bucket Challenge

August 24, 2014Have you been nominated to take the ALS ice bucket challenge yet?

Kabbage below:

Their video made the local Atlanta news.

OnDeck in Times Square NYC:

Noah Breslow, their CEO also did it:

Funding Circle:

PayPal

Coincidentally, in the industry’s 2012 fantasy football competition for charity, league winner Sure Payment Solutions chose to donate all funds raises ($7,100) to the ALS Association.

Whether you get nominated or not, you can donate at http://www.alsa.org/.

Feel free to tweet @financeguy74 if you or your company accepted the challenge. 🙂