SoFi is Now a Fannie Mae Seller, Servicer

May 4, 2016

SoFi clocked in another milestone in mortgage lending by becoming an approved Fannie Mae seller and servicer.

SoFi Lending Corp, the company’s wholly owned subsidiary can, as a seller, sell mortgage loans to Fannie Mae and service loans on behalf of the Federal National Mortgage Association.

“While we launched our mortgage business focused on larger ‘jumbo’ loans, the certainty and efficiency offered by Fannie Mae will enable us to serve more members by expanding geographically and into smaller loan amounts,” said Michael Tannenbaum, VP of Mortgage at SoFi in a press release. “Sixty-five percent of SoFi’s purchase customers are first-time homeowners who have what we call a ‘millennial mindset.”

In March this year, the company was laying down the works to start a real estate trust to buy mortgages sold by the lender. According to Bloomberg, some of SoFi’s borrowers seek mortgages that are too big to be funded through Fannie Mae and Freddie Mac.

In the crowded online lending space, where customer acquisition is key, companies scramble to lock in borrowers early to keep lending to them through different life stages from student loans to auto loans to mortgages. SoFi uses the free cash flow method for mortgages, a deviation from the industry standard of debt-to-income ratio.

“There isn’t a banker out there that doesn’t look at me and shake his head and say, ‘You don’t know what you’re doing, but we’re doing it,” Cagney told Bloomberg. SoFi plans to sell $3 billion in mortgages this year.

Stairway to Heaven: Can Alternative Finance Keep Making Dreams Come True?

April 28, 2016

The alternative small-business finance industry has exploded into a $10 billion business and may not stop growing until it reaches $50 billion or even $100 billion in annual financing, depending upon who’s making the projection. Along the way, it’s provided a vehicle for ambitious, hard-working and talented entrepreneurs to lift themselves to affluence.

Consider the saga of William Ramos, whose persistence as a cold caller helped him overcome homelessness and earn the cash to buy a Ferrari. Then there’s the journey of Jared Weitz, once a 20 something plumber and now CEO of a company with more than $100 million a year in deal flow.

Their careers are only the beginning of the success stories. Jared Feldman and Dan Smith, for example, were in their 20s when they started an alt finance company at the height of the financial crisis. They went on to sell part of their firm to Palladium Equity Partners after placing more than $400 million in lifetime deals.

Their careers are only the beginning of the success stories. Jared Feldman and Dan Smith, for example, were in their 20s when they started an alt finance company at the height of the financial crisis. They went on to sell part of their firm to Palladium Equity Partners after placing more than $400 million in lifetime deals.

The industry’s top salespeople can even breathe new life into seemingly dead leads. Take the case of Juan Monegro, who was in his 20s when he left his job in Verizon customer service and began pounding the phones to promote merchant cash advances. Working at first with stale leads, Monegro was soon placing $47 million in advances annually.

The industry’s top salespeople can even breathe new life into seemingly dead leads. Take the case of Juan Monegro, who was in his 20s when he left his job in Verizon customer service and began pounding the phones to promote merchant cash advances. Working at first with stale leads, Monegro was soon placing $47 million in advances annually.

Alternative funding can provide a second chance, too. When Isaac Stern’s bakery went out of business, he took a job telemarketing merchant cash advances and went on to launch a firm that now places more than $1 billion in funding annually.

All of those industry players are leaving their marks on a business that got its start at the dawn of the new century. Long-time participants in the market credit Barbara Johnson with hatching the idea of the merchant cash advance in 1998 when she needed to raise capital for a daycare center. She and her husband, Gary Johnson, started the company that became CAN Capital. The firm also reportedly developed the first platform to split credit card receipts between merchants and funders.

BIRTH OF AN INDUSTRY

Competitors soon followed the trail those pioneers blazed, and the industry began growing prodigiously. “There was a ton of credit out there for people who wanted to get into the business,” recalled David Goldin, who’s CEO of Capify and serves as president of the Small Business Finance Association, one of the industry’s trade groups.

Competitors soon followed the trail those pioneers blazed, and the industry began growing prodigiously. “There was a ton of credit out there for people who wanted to get into the business,” recalled David Goldin, who’s CEO of Capify and serves as president of the Small Business Finance Association, one of the industry’s trade groups.

Many of the early entrants came from the world of finance or from the credit card processing business, said Stephen Sheinbaum, founder of Bizfi. Virtually all of the early business came from splitting card receipts, a practice that now accounts for just 10 percent of volume, he noted.

At first, brokers, funders and their channel partners spent a lot of time explaining advances to merchants who had never heard of them, Goldin said. Competition wasn’t that tough because of the uncrowded “greenfield” nature of the business, industry veterans agreed.

Some of the initial funding came from the funders’ own pockets or from the savings accounts of their elderly uncles. “I’ve met more than a few who had $2 million to $5 million worth of loans from friends and family in order to fund the advances to the merchants,” observed Joel Magerman, CEO of Bryant Park Capital, which places capital in the industry. “It was a small, entrepreneurial effort,” Andrea Petro, executive vice president and division manager of lender finance for Wells Fargo Capital Finance, said of the early days. “A number of these companies started with maybe $100,000 that they would experiment with. They would make 10 loans of $10,000 and collect them in 90 days.”

That business model was working, but merchant cash advances suffered from a bad reputation in the early days, Goldin said. Some players were charging hefty fees and pushing merchants into financial jeopardy by providing more funding than they could pay back comfortably. The public even took a dim view of reputable funders because most consumers didn’t understand that the risk of offering advances justified charging more for them than other types of financing, according to Goldin.

Then the dam broke. The economy crashed as the Great Recession pushed much of the world to the brink of financial disaster. “Everybody lost their credit line and default rates spiked,” noted Isaac Stern, CEO of Fundry, Yellowstone Capital and Green Capital. “There was almost nobody left in the business.”

RAVAGED BY RECESSION

Perhaps 80 percent of the nation’s alternative funding companies went out of business in the downturn, said Magerman. Those firms probably represented about 50 percent of the alternative funding industry’s dollar volume, he added. “There was a culling of the herd,” he said of the companies that failed.

Life became tough for the survivors, too. Among companies that stayed afloat, credit losses typically tripled, according to Petro. That’s severe but much better than companies that failed because their credit losses quintupled, she said.

Who kept the doors open? The firms that survived tended to share some characteristics, said Robert Cook, a partner at Hudson Cook LLP, a law office that specializes in alternative funding. “Some of the companies were self-funding at that time,” he said of those days. “Some had lines of credit that were established prior to the recession, and because their business stayed healthy they were able to retain those lines of credit.”

The survivors also understood risk and had strong, automated reporting systems to track daily repayment, Petro said. For the most part, those companies emerged stronger, wiser and more prosperous when the crisis wound down, she noted. “The legacy of the Great Recession was that survivors became even more knowledgeable through what I would call that ‘high-stress testing period of losses,’” she said.

ROAD TO RECOVERY

The survivors of the recession were ready to capitalize on the convergence of several factors favorable to the industry in about 2009. Taking advantages of those changes in the industry helped form a perfect storm of industry growth as the recession was ending.

The survivors of the recession were ready to capitalize on the convergence of several factors favorable to the industry in about 2009. Taking advantages of those changes in the industry helped form a perfect storm of industry growth as the recession was ending.

They included making good use of the quick churn that characterizes the merchant cash advance business, Petro noted. The industry’s better operators had been able to amass voluminous data on the industry because of its short cycles. While a provider of auto loans might have to wait five years to study company results, she said, alternative funders could compile intelligence from four advances within the space of a year.

That data found a home in the industry around the time the recession was ending because funders were beginning to purchase or develop the algorithms that are continuing to increase the automation of the underwriting process, said Jared Weitz, CEO of United Capital Source LLC. As early as 2006, OnDeck became one of the first to rely on digital underwriting, and the practice became mainstream by 2009 or so, he said.

Just as the technology was becoming widespread, capital began returning to the market. Wealthy investors were pulling their funds out of real estate and needed somewhere to invest it, accounting for part of the influx of capital, Weitz said.

At the same time, Wall Street began to take notice of the industry as a place to position capital for growth, and companies that had been focused on consumer lending came to see alternative finance as a good investment, Cook said.

For a long while, banks had shied away from the market because the individual deals seem small to them. A merchant cash advance offers funders a hundredth of the size and profits of a bank’s typical small-business loan but requires a tenth of the underwriting effort, said David O’Connell, a senior analyst on Aite Group’s Wholesale Banking team.

The prospect of providing funds became even less attractive for banks. The recession had spawned the Dodd-Frank Financial Regulatory Reform Bill and Basel III, which had the unintended effect of keeping banks out of the market by barring them from endeavors where they’re inexperienced, Magerman said. With most banks more distant from the business than ever, brokers and funders can keep the industry to themselves, sources acknowledged.

At about the same time, the SBFA succeeded in burnishing the industry’s image by explaining the economic realities to the press, in Goldin’s view.The idea that higher risk requires bigger fees was beginning to sink in to the public’s psyche, he maintained.

Meanwhile, loans started to join merchant cash advances in the product mix. Many players began to offer loans after they received California finance lenders licenses, Cook recalled. They had obtained the licenses to ward off class-action lawsuits, he said and were switching from sharing card receipts to scheduled direct debits of merchants’ bank accounts.

As those advantages – including algorithms, ready cash, a better image and the option of offering loans – became apparent, responsible funders used them to help change the face of the industry. They began to make deals with more credit-worthy merchants by offering lower fees, more time to repay and improved customer service. “The recession wound up differentiating us in the best possible way,” Bizfi’s Sheinbaum said of the changes.

His company found more-upscale customers by concentrating on industries that weren’t hit too hard by the recession. “With real estate crashing, people were not refurbishing their homes or putting in new flooring,” he noted.

Today, the booming alternative finance industry is engendering success stories and attracting the nation’s attention. The increased awareness is prompting more companies to wade into the fray, and could bring some change.

WHAT LIES AHEAD

One variety of change that might lie ahead could come with the purchase of a major funding company by a big bank in the next couple of years, Bryant Park Capital’s Magerman predicted. A bank could sidestep regulation, he suggested, by maintaining that the credit card business and small business loans made through bank branches had provided the banks with the experience necessary to succeed.

Smaller players are paying attention to the industry, too, with varying degrees of success. Predictably, some of the new players are operating too aggressively and could find themselves headed for a fall. “Anybody can fund deals – the talent lies in collecting the money back at a profitable level,” said Capify’s Goldin. “There’s going to be a shakeout. I can feel it.”

Smaller players are paying attention to the industry, too, with varying degrees of success. Predictably, some of the new players are operating too aggressively and could find themselves headed for a fall. “Anybody can fund deals – the talent lies in collecting the money back at a profitable level,” said Capify’s Goldin. “There’s going to be a shakeout. I can feel it.”

Some of today’s alternative lenders don’t have the skill and technology to ward off bad deals and could thus find themselves in trouble if recession strikes, warned Aite Group’s O’Connell. “Let’s be careful of falling into the trap of ‘This time is different,’” he said. “I see a lot of sub-prime debt there.”

Don’t expect miracles, cautioned Petro. “I believe there will be another recession, and I believe that there will be a winnowing of (alternative finance) businesses,” she said. “There will be far fewer after the next recession than exist today.”

A recession would spell trouble, Magerman agreed, even though demand for loans and advances would increase in an atmosphere of financial hardship. Asked about industry optimists who view the business as nearly recession-proof, he didn’t hold back. “Don’t believe them,” he warned. “Just because somebody needs capital doesn’t mean they should get capital.”

Further complicating matters, increased regulatory scrutiny could be lurking just beyond the horizon, Petro predicted. She provided histories of what regulation has done to other industries as an indication of the differing outcomes of regulation – one good, one debatable and one bad.

Good: The timeshare business benefitted from regulation because the rules boosted the public’s trust.

Debatable: The cost of complying with regulations changed the rent-to-own business from an entrepreneurial endeavor to an environment where only big corporations could prosper.

Bad: Regulation appears likely to alter the payday lending business drastically and could even bring it to an end, she said.

Still, regulation’s good side seems likely to prevail in the alternative finance business, eliminating the players who charge high fees or collect bloated commissions, according to Weitz. “I think it could only benefit the industry,” he said. “It’ll knock out the bad guys.”

Letter From the Editor – March/April 2016

March 1, 2016 In early 2016, a recession seemed inevitable, until it didn’t. Rumors of rising defaults across a variety of marketplace lenders have been defended as falling within model estimates. The stock market’s sudden plunge recovered. And Madden v Midland’s long-term impact is being chalked up as overblown. All is well again, well mostly anyway. Institutional investors have gotten a little spooked and the once insatiable appetite seems to have become just a little bit satiable.

In early 2016, a recession seemed inevitable, until it didn’t. Rumors of rising defaults across a variety of marketplace lenders have been defended as falling within model estimates. The stock market’s sudden plunge recovered. And Madden v Midland’s long-term impact is being chalked up as overblown. All is well again, well mostly anyway. Institutional investors have gotten a little spooked and the once insatiable appetite seems to have become just a little bit satiable.

But we’re back, and so is the beast that has come to be known as “marketplace lending.” The FDIC says that term can encompass unsecured consumer loans, debt consolidation loans, auto loans, purchase financing, real estate loans, merchant cash advance, medical patient financing, and small business loans. It can “include any practice of pairing borrowers and lenders through the use of an online platform without a traditional bank intermediary,” they wrote in their Winter 2015 Supervisory Insights report.

In this issue, we examined one piece of marketplace lending that has created many success stories, the merchant cash advance industry. For years, it’s turned hungry 20 somethings into front-page worthy stars. Will that trend continue or has the moment passed? The quality of leads will play a role in who makes it big and who doesn’t, said some of the folks we interviewed. Ironically, while the industry is often considered to be online, the Internet is reportedly becoming a less reliable place to acquire customers because of competition and cost. Having problems with leads? You’re not alone, we’ve learned.

But not everyone is struggling. In March, we published a list of the top 8 alternative small business funders of 2015. The numbers were either reported to us directly or we determined them using publicly available information. In this issue, we’ve got the year-over-year statistics for 18 companies. Some of them might surprise you.

I don’t want to finish off my introduction to this issue with the R-word, but since there were signs of weakness earlier this year, we did ask the wider marketplace lending industry what to expect from the next recession. Everything is at risk, they said, from borrower defaults to institutional backing to regulatory action. Marketplace lending, however big and strong it is now, is not believed to be impervious to market forces. Will the beast prevail? Or is it destined to fail?

–Sean Murray

The Reason Behind Lendio’s 1175% Growth

February 25, 2016 Lendio, the small business loans marketplace closed 2015 with $128 million in financing for 5100 businesses. That number swiftly becomes impressive compared to the 400 businesses funded with $12.4 million the previous year.

Lendio, the small business loans marketplace closed 2015 with $128 million in financing for 5100 businesses. That number swiftly becomes impressive compared to the 400 businesses funded with $12.4 million the previous year.

Lendio CEO Brock Blake attributes this 1175 percent growth to the partnerships the company forged, the most noteworthy one with Staples where Lendio finances the small businesses that Staples often interacts with. “We had a great year with our partnership,” he said. “Staples has been a fantastic partner — they have the merchants and we have the finance.”

The Salt Lake City-based company prides itself on its partnership strategy. In 2014, the company struck a deal with UPS to offer their marketplace for free to The UPS Store business customers.

Blake is also excited about expanding the marketing channels and growing the firm’s online marketing strategy.

Lendio’s average loan size is $25,000 and their clients have typically been in business for 26 months in industries like construction, retail, restaurants and real estate.

CFPB (and others) Not Amused By Quicken’s Push-Button Mortgage Ad

February 9, 2016Is Quicken in the right place at the wrong time?

Imagine a world where you could get a mortgage at the push of a button. And then imagine like literally pushing that button while you’re sitting in a dark auditorium watching a magic show. As the magician saws a woman in half, you agree to a $400,000 loan payable over 30 years. That pivotal moment, according to Quicken’s vision for American prosperity, will lead to a “tidal wave of ownership” that will flood the country with new home owners.

Consider the implications of that commercial on its own merits (or watch it below of course) and then imagine watching it after you’ve just seen The Big Short in theaters. Given that the movie is a true story about the build-up of the housing and credit bubble in the 2000s that led to a near catastrophic global collapse, a mortgage “tidal wave” might not be the best way to describe your new mobile app.

After Quicken’s push-button mortgage commercial aired during the Super Bowl, the Consumer Financial Protection Bureau responded on twitter:

When it comes to #mortgages, take your time, ask questions and #knowbeforeyouowe. https://t.co/UUaGyWDbzk

— consumerfinance.gov (@CFPB) February 8, 2016

While the mortgage process shown on TV looked overly ambitious, a Quicken customer service rep who I chatted with while posing as a borrower, said that it really can be all done online, even if the mortgage was for like $600,000. When I inquired about what documents I’d need to provide through that process, I was told all I needed to do was state the address of the home.

A no-doc process?

According to the Wall Street Journal, “borrowers can authorize Quicken to access their bank and other financial information directly, eliminating the need for sending pay stubs, bank statements and tax returns back and forth.” So there’s still documents, they’re just electronic and retrieved via APIs.

Having scanned the process, there is clearly more than just one button to push (I counted 9 steps), but it may actually be possible to get a mortgage while watching a magic show. Apparently a lot of people on twitter don’t think that’s a good thing:

Thanks Rocket Mortgage for thinking the '08 housing crisis needed a sequel

— Wyatt Rasmussen (@Wyatt_Rasmussen) February 8, 2016

Let's start another financial collapse. #RocketMortgage https://t.co/7CkBTGJRPD

— Turney Duff (@turneyduff) February 8, 2016

My kid was playing with my phone and bought 7 houses. I can return those right? #RocketMortgage #SB50

— Tim Murphy (@TimMurphy104) February 8, 2016

Rocket Mortgage: explaining the 2008 financial crisis in one commercial

— Rahul Vedantam (@RahulVedantam) February 8, 2016

This commercial is making an excellent case for a massive real estate bubble. It worked awesome in 2007. #RocketMortgage

— Ben Shapiro (@benshapiro) February 8, 2016

Meanwhile, Rana Foroohar, Assistant Managing Editor and Columnist for Time and Global Economic Analyst for CNN, argued that the backlash is unfounded. “No, the Rocket Mortgage Ad Is Not the Sign of Another Financial Apocalypse,” was the headline of her Time story published on Monday. Her evidence? Nobody can afford a mortgage anyway so there’s nothing to worry about, she basically says.

Private equity firm Blackstone has become the largest buyer of single family homes in the country over the last few years. […] Most ordinary Americans need mortgages to buy real estate; at current housing prices and incomes, it would take a typical family more than twenty years to save even a 10% down payment for a home plus closing costs. But they can’t get the loans, because in our post-crisis world, banks are still keeping credit tighter than usual. Besides, many individuals simply don’t have the secure employment, nest egg, and increasingly high credit scores needed to obtain a mortgage these days.

– Rana Foroohar

http://time.com/4212259/rocket-mortgage-super-bowl-ad/

See? There can’t be a bubble brewing because nobody can possibly qualify.

So when Quicken makes wildly provocative sales pitches like this:

Push Button. Get Mortgage. https://t.co/UzOXYFF25C#RocketMortgage 🚀🚀🚀

— Quicken Loans (@QuickenLoans) February 8, 2016

What they’re really apparently trying to say is that the process for those that qualify is supposedly more transparent and therefore better for borrowers:

.@CFPB We agree. No better way than #RocketMortgage for full transparency into mortgage options & info needed to make the right decision.

— Quicken Loans (@QuickenLoans) February 8, 2016

Of course, it probably doesn’t help when their legal help page is titled “legal mumbo jumbo.”

Quicken CEO Bill Emerson tried to clarify the message of the commercial to the WSJ. “What we’re saying is that a strong housing market filled with responsible homeowners is important to the economy,” he said.

Don’t worry about the mumbo jumbo folks, just push button, get mortgage.

—

What do you think? Is Quicken walking down a slippery slope?

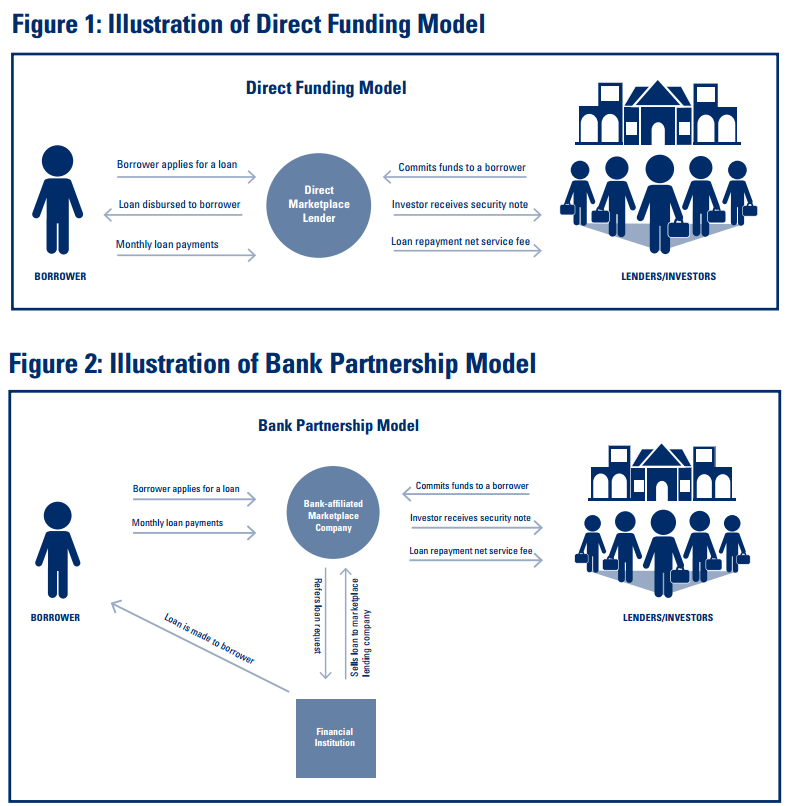

How the FDIC Defines Marketplace Lending

February 5, 2016Marketplace lending is one of this year’s hottest buzzwords but its meaning is not very intuitive. According to a recent Federal Deposit Insurance Corporation (FDIC) report, “marketplace lending is broadly defined to include any practice of pairing borrowers and lenders through the use of an online platform without a traditional bank intermediary.” This might sound similar to peer-to-peer lending and that’s because it’s the same thing, the FDIC explains. “Although the model, originally started as a ‘peer-to-peer’ concept for individuals to lend to one another, the market has evolved as more institutional investors have become interested in funding the activity. As such, the term ‘peer-to-peer lending’ has become less descriptive of the business model and current references to the activity generally use the term ‘marketplace lending.'”

Voilà, marketplace lending is what you get when peers are replaced by private equity firms, pension funds, and hedge funds. Additionally, there is a general assumption that the intermediary platform is also underwriting and grading the loans.

The FDIC separates marketplace lenders into two categories, the “direct funding model” and “bank partnership model,” both of which are illustrated below:

In both circumstances, investors are actually buying securities, rather than participating in the loans themselves.

The FDIC says that marketplace lending can encompass unsecured consumer loans, debt consolidation loans, auto loans, purchase financing, education financing, real estate loans, merchant cash advance, medical patient financing, and small business loans.

For even more information, read the official report.

Opus Bank Enters into Strategic Marketing and Referral Agreement with Leading Online Lender to Increase Lending to Small Businesses

January 21, 2016IRVINE, Calif.–(BUSINESS WIRE)–Opus Bank (“Opus”) (NASDAQ: OPB) announced today that it has entered into a marketing and referral agreement with OnDeck® (NYSE: ONDK), the leader in online lending for small business, that will leverage Opus’ 58 retail banking office distribution located in major metro markets up and down the West Coast and OnDeck’s sophisticated credit and funding platform. Entering into this arrangement allows Opus to offer a complete solution to those small businesses that are looking for financing up to $500,000, including a range of term loans and lines of credit powered by a streamlined application process and fast access to the funds.

Stephen H. Gordon, Founding Chairman, Chief Executive Officer, and President of Opus Bank, stated, “I am excited to have entered into this marketing and referral agreement with OnDeck. Opus offers an extensive suite of lending products through its Commercial Bank and, while we receive a significant amount of inquiry for small business loans through our Retail Bank, OnDeck has proven to be much more proficient in underwriting and funding these smaller loans. This partnership enables Opus to further leverage and scale its strong market presence by offering small balance financing solutions that it was otherwise not able to efficiently accommodate and, in doing so, generate additional revenues while not using Opus’ balance sheet or capital.”

Gordon concluded, “Since Opus’ inception, it has had an acute focus on providing tailored financial products, services, and solutions to those small and mid-sized commercial businesses, entrepreneurs, real estate investors, and professionals with a vision to expand and grow. Opus is now better positioned to provide faster access to capital to those businesses where the availability of small balance financing has an outsized impact on their ability to expand, create new jobs, and succeed. At Opus Bank, we understand that by providing capital financing to successful entrepreneurs and their businesses, we are enabling those businesses to flourish and, in turn, build healthy, vital, and vibrant communities from the ground up.”

About Opus Bank

Opus Bank is an FDIC insured California-chartered commercial bank with over $6.2 billion of total assets, $5.0 billion of total loans, and $4.9 billion in total deposits as of September 30, 2015. Opus Bank provides high-value, relationship-based banking products, services, and solutions to its clients through its Retail Bank, Commercial Bank, Merchant Bank, and Correspondent Bank. Opus Bank offers a suite of treasury and cash management and depository solutions and a wide range of loan products, including commercial business, healthcare, technology, multifamily residential, commercial real estate, and structured finance, and is an SBA preferred lender. Opus Bank offers commercial escrow services and facilitates 1031 Exchange transactions through its Escrow and Exchange divisions. Opus Bank provides clients with financial and advisory services related to raising equity capital, targeted acquisition and divestiture strategies, general mergers and acquisitions, debt and equity financing, balance sheet restructuring, valuation, strategy, and performance improvement through its Merchant Banking division and its broker-dealer subsidiary, Opus Financial Partners. Opus Bank operates 58 client experience centers, including 33 in California, 22 in the Seattle/Puget Sound region in Washington, two in the Phoenix metropolitan area of Arizona, and one in Portland, Oregon. For additional information about Opus Bank, please visit our website: www.opusbank.com. Opus Bank is an Equal Housing Lender.

Forward-Looking Statements

This release may include forward-looking statements related to Opus’ plans, beliefs and goals, which involve certain risks, and uncertainties that could cause actual results to differ materially from those in the forward-looking statements. The forward-looking information presented in this press release is not a guarantee of future events, and actual events may differ materially from those made in or suggested by the forward-looking information contained in this press release. Forward-looking statements generally can be identified by the use of forward-looking terminology such as “intend” or “expect” or variations thereon or similar terminology. All such statements speak only as of the date made, and Opus undertakes no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise.

Loan Brokers: Fight Back and Defend Your Brand

January 16, 2016 LIFE DOESN’T PLAY FAIR AND NEITHER DOES YOUR COMPETITORS

LIFE DOESN’T PLAY FAIR AND NEITHER DOES YOUR COMPETITORS

Let’s face it, a big part of our job is customer service. As a direct funder or lender, or as a large or small brokerage, a big part of our job is to service our existing customers, partners, vendors and suppliers with the utmost integrity, efficiency and ethics. But even the best of customer service intentions can become scarred when those who compete against you, choose to compete unfairly through vile fabrications, defamations and falsehoods.

MORE MONEY, MORE PROBLEMS

Not many people (including myself) are too fond of hip hop music as most of the time the lyrics are questionable, but in 1997, everybody agreed with The Notorious B.I.G. when he touched on the concept of making more money and having to subsequently deal with new problems.

The bigger and more exposed you get, the higher the probability that you’ll have a run-in with dissatisfied merchants, partners, vendors and suppliers. This is common knowledge, as many of the largest ISO/MSPs and MCA firms are all over the ripoff reports in one form or fashion, with current and prior customers blasting the companies over sometimes legit issues, and other times issues of a petty nature that could have been resolved in means of a lesser depiction. But continuing on, the bigger you get, the bigger your “haters” will get as well. The rise of the internet has multiplied the presence of haters and trolls to a population standing taller than ever before. These haters love to use online discussion boards, social media, blogs, and review sites to spread their lies, hatred and vile.

JUST BECAUSE YOU SMELL SMOKE, THAT DOESN’T MEAN THERE’S A FIRE BURNING

I’m not sure who the author of this quote is, but it says the following: People will question all the good things they hear about you, but believe the bad without a second thought. Haters know this quote to be true and are quick to spread their venom knowing that if it’s coming from multiple sources, then far too many people will take them at their word using the flawed logic of “where there’s smoke, there must be fire.”

Well, I say just because you smell smoke, that doesn’t mean there’s a fire burning. Instead, you could more than likely have a group of haters who have perfected the art of blowing smoke, which is to make unfounded or exaggerated claims. As a result, you need to protect your brand against haters. There are those of you who believe that if you just ignore them then they will go away. Well, I disagree with that notion and so does Motorhead’s Lemmy Kilmister. “I don’t understand people who believe that if you ignore something, it’ll go away,” he was once quoted as saying “That’s completely wrong because if it’s ignored, then it gathers strength. Europe ignored Hitler for twenty years, as a result he slaughtered a quarter of the world!”

LOOK AT DONALD J. TRUMP

If he wins the candidacy or not, Donald Trump will go down as perhaps the most fiery presidential candidate of all time. When Trump believes something, he says it, without filter and without care of political expediency. When Trump is “attacked” by the media or one of his fellow GOP opponents, he fires back. On the O’Reilly Factor after the final GOP debate of 2015, Trump clarified that if the media or one of his GOP opponents makes a valid criticism about him, he’s perfectly fine with that, but what he has a problem with is when they flat out lie about something he’s said, done or believes in.

While I’m an Independent and not sure who I will support for the 2016 Presidential election, I find myself in agreement with Trump on a number of things, including how Trumps responds to “haters.” My stance is that if you have a valid criticism about something I’ve said, done or believe in, then I’m all ears! But when you flat out lie about me, now you are going to tick me off.

GET MAD, GET MAD!

One of the reasons for Trump’s surge in the polls is the fact that a lot of people are angry at leaders in Washington and aren’t going to “take it” anymore. Trump’s fiery persona attracts people to the real estate tycoon, causing him to have a massive lead in the Republican race. Like Trump, you should get mad as well if you have worked to build your brand, resumé and marketplace standing, and then all of a sudden here comes some anonymous troll spitting out all types of defamations across the internet:

- Don’t work with XYZ Company, they are a scam!

- XYZ Company stole my money!

- XYZ Company’s President is a criminal!

- XYZ Company backdoors deals!

The definition of libel is to write something about an individual or a company that is defamatory, which is a statement that is false but written in a way to convince the public that it’s true. The internet has increased the presence of libel so much, that insurance companies market their personal umbrella policies as a form of insurance in case you are sued for libel. Some people don’t realize that typing something on the internet can get you in trouble if you are lying about the person or the company in question. Now, I’m not advising you to run out and sue everybody who lies about you online, as that would be very costly, however, I am advising you to get mad by fighting back and doing some of the following to protect your brand.

FLOOD THE MARKET WITH TESTIMONIALS

Begin to flood the market with positivity. When a prospective client searches for your company in Google and finds the negative reviews, they can also see the various videos, blogs and review sites where your customers, partners and vendors are praising you. You can always say: Look at the many customer testimonials that we have and look at the size of our customer portfolio, clearly more people are satisfied with us than dissatisfied.

THE BETTER BUSINESS BUREAU

The BBB will provide you an “A+” or “A” rating as long as you respond to any complaints filed in a timely manner. You can use your “A” rating status in marketing and in response to prospective clients inquiring about negative reviews. You can always say: We have an A+ rating with the BBB, we must be doing something right.

PUBLIC RELATIONS

A lot of direct funders and large brokerages have large sources of operating capital to play with, so why not hire a PR Team? Have a PR Team speak with the media often to generate as much positive press as possible to help balance out the negative press. In addition, have the company CEO and other high ranking officials do various forms of PR when available.

TAKE THE FIGHT TO THE TROLLS

Go to the discussion board, social media post, blog post, vlog post, or website, and directly respond to the person creating the negative press. Debate your points, prove them to be wrong, show them to be a liar, and encourage your employees, vendors and partners to join in on the fight. Silence can be taken in one of two ways, either people will think you are “too big” for this petty non-sense, or they will think that you are silent because you are guilty. I say take the fight to the trolls, debate your points and then move on after you’ve put the verifiable truth on the table.

THE FINAL WORD

Some people will already know something is a lie, but choose to believe it anyway because they want it to be true regardless. Sean Parker’s character from the Social Network said that, “even if you’ve managed to live your life like the Dalai Lama, they’ll still make things up because they don’t want you, they want your idea.” The honest truth is that most of your haters are just jealous of you because, you have something that they want but don’t have. So, don’t allow them to throw you off your game.

As a quote I read the other day from some unknown source said, “you should never hate people who are jealous of you, but instead respect their jealousy as they are the people who think that you’re better than them.” Having haters is a sign that you’re doing something right. Your prospective customers and partners with good judgment should be able to read between the lines to see the truth, and for those that can’t, well, maybe they are too gullible (and stupid) to be doing business with anyway.