Big Banks Less Transparent Than Online Lenders Federal Reserve Study Finds

March 4, 2016The results are in. Dissatisfied small business borrowers are more likely to encounter transparency problems with big banks, not online lenders.

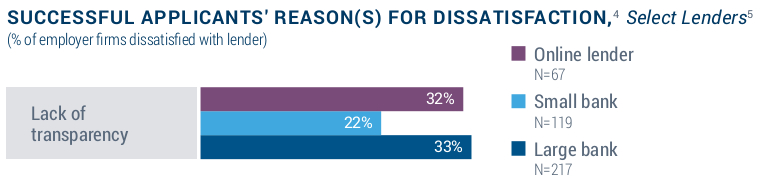

The margin of difference on this measure may have been razor thin, but the anti-online lender rhetoric isn’t matching up with borrower feedback. The 2015 Small Business Credit Survey, a comprehensive report released by the Federal Reserve, found that 33% of borrowers that were dissatisfied with a small business loan from a big bank, cited a lack of transparency as a reason. 32% of borrowers that were dissatisfied with an online lender cited a lack transparency. While both statistics show room for improvement, the results shatter the myth that online lenders are uniquely lacking in transparency.

The findings are also consistent with the results of a previous Federal Reserve study in which small business owners gave extremely high marks to online lenders for clarity (even after researchers tried to trick them). This latest report does not put online lenders in a favorable light, but it does show that a dissatisfied borrower is equally or more likely to be confused by a loan from Chase or Bank of America than they are from OnDeck or PayPal Working Capital.

The findings are also consistent with the results of a previous Federal Reserve study in which small business owners gave extremely high marks to online lenders for clarity (even after researchers tried to trick them). This latest report does not put online lenders in a favorable light, but it does show that a dissatisfied borrower is equally or more likely to be confused by a loan from Chase or Bank of America than they are from OnDeck or PayPal Working Capital.

Small banks were less likely than online lenders and big banks to experience dissatisfaction over transparency.

Online lenders were defined by the Fed as “alternative and marketplace lenders, including Lending Club, OnDeck, CAN Capital, and PayPal Working Capital.” Respondents could select multiple options for dissatisfaction, ensuring that a separate issue didn’t merely trump transparency.

Big banks also scored worse on difficulty of the application process. 51% of dissatisfied borrowers that got a loan from a big bank cited difficulty. Only 21% of dissatisfied borrowers that got a loan from an online lender cited difficulty.

A more difficult, lengthier, and more regulated process at big banks has apparently not led to more transparency with borrowers. The findings echo B. Doyle Mitchell Jr.’s testimony presented during a House Committee hearing last fall. Mitchell, who was speaking on behalf of the Independent Community Bankers of America, said that adding more pages to loan agreements do not make them any more clear to borrowers. “In fact it is even more cumbersome for them now,” he said.

The Federal Reserve’s own study has proven to be consistent with that assessment.

Lending Club Shifts Fee Arrangement With WebBank

February 26, 2016 It’s a “belt and suspenders” precaution according to Lending Club CEO Renaud Laplanche. The Madden v Midland case has forced the company to rethink their arrangement with WebBank, the chartered bank that allows them to make loans nationwide. Under the new terms, the fee LendingClub pays to WebBank for the loans it issues will be related to how the loans perform over time.

It’s a “belt and suspenders” precaution according to Lending Club CEO Renaud Laplanche. The Madden v Midland case has forced the company to rethink their arrangement with WebBank, the chartered bank that allows them to make loans nationwide. Under the new terms, the fee LendingClub pays to WebBank for the loans it issues will be related to how the loans perform over time.

Even if the U.S. Supreme Court were to rule unfavorably in Madden, Lending Club would still have been able to operate freely under their old arrangement. The change then may be a response to several cases, including ones that have accused online lenders of using chartered bank relationships to carry out alleged abuses. According to law firm Ballard Spahr, a “federal court refused to dismiss Pennsylvania racketeering claims against companies alleged to have partnered with a state bank to market Internet loans illustrates the risks inherent in these relationships and the importance of proper structuring.”

In a brief, Ballard Spahr wrote:

In Commonwealth of Pennsylvania v. Think Finance, Inc., et al., the Pennsylvania AG, working with a well-known private plaintiffs’ firm, claimed that the companies and their individual principal had engaged in a “rent-a-bank” scheme in which a Delaware state bank “acted as the nominal lender while the non-bank entity was the de facto lender—marketing, funding and collecting the loan.”

By WebBank maintaining an interest in the outcome of the individual loans, Lending Club will reduce its potential standing as the de factor lender.

Notably, the breaking story focused on Lending Club. WebBank also has a relationship with others in the alternative finance community such as CAN Capital, Prosper, AvantCredit and PayPal. It’s uncertain if their arrangements will also be subject to change.

Former Bizfi Manager is Making a Splash in Delaware State Senate Contest

February 7, 2016 A former Bizfi manager is underwriting a new kind of 4-year deal. Thirty-two year old James Spadola, who lives in Wilmington, is bringing an impressive resumé to the Delaware state Senate contest for District 1.

A former Bizfi manager is underwriting a new kind of 4-year deal. Thirty-two year old James Spadola, who lives in Wilmington, is bringing an impressive resumé to the Delaware state Senate contest for District 1.

The world knows him as #HugACop after an outreach campaign he spearheaded for the Newark, Delaware police department went viral and inspired a new era of positive policing. Spadola has served as an officer there for more than 7 years.

He attended the University of Delaware, an experience that was interrupted when he was called up by the U.S. Army Reserve to take a tour of duty. Deployed in March 2003 for a year, he served as a prison guard and as his battalion commander’s gunner and driver in Iraq. He received the Combat Action Badge when his convoy was hit with an IED.

After returning home and graduating, Spadola moved to New York City and got a job at a hot new fintech startup named Merchant Cash and Capital (MCC). That was in February 2007, making him one of the company’s first ten employees. MCC Changed their name to Bizfi in September of 2015.

As an underwriter, Spadola was tasked with evaluating working capital applications submitted by small businesses. He was quickly promoted to Team Leader and later to Underwriting Manager, a senior departmental position.

Spadola told AltFinanceDaily of his time there, “I had a great experience at Bizfi and learned an enormous amount about the private sector and the troubles and challenges that small business owners deal with everyday.”

Bizfi General Manager Seth Broman, said of him, “having worked closely with James for several years, it was apparent to me and all those around him that James has a knack for helping those in need.”

After almost two years there, he moved to Delaware to join the Newark Police Department, where he’s been ever since. He still managed to find the time to get his MBA from Wilmington University in 2014.

Today, Spadola is underwriting a new kind of challenge, competing against incumbent state legislator Harris McDowell who has been in office since 1976. Running as a Republican in a blue state, Spadola thinks it’s time for new blood.

“I look forward to putting those business lessons, coupled with what I’ve learned through my other professional experiences, into practical application down at Legislative Hall,” he told AltFinanceDaily.

Visit his campaign Facebook page.

E-mail james@jamesspadola.com for further information.

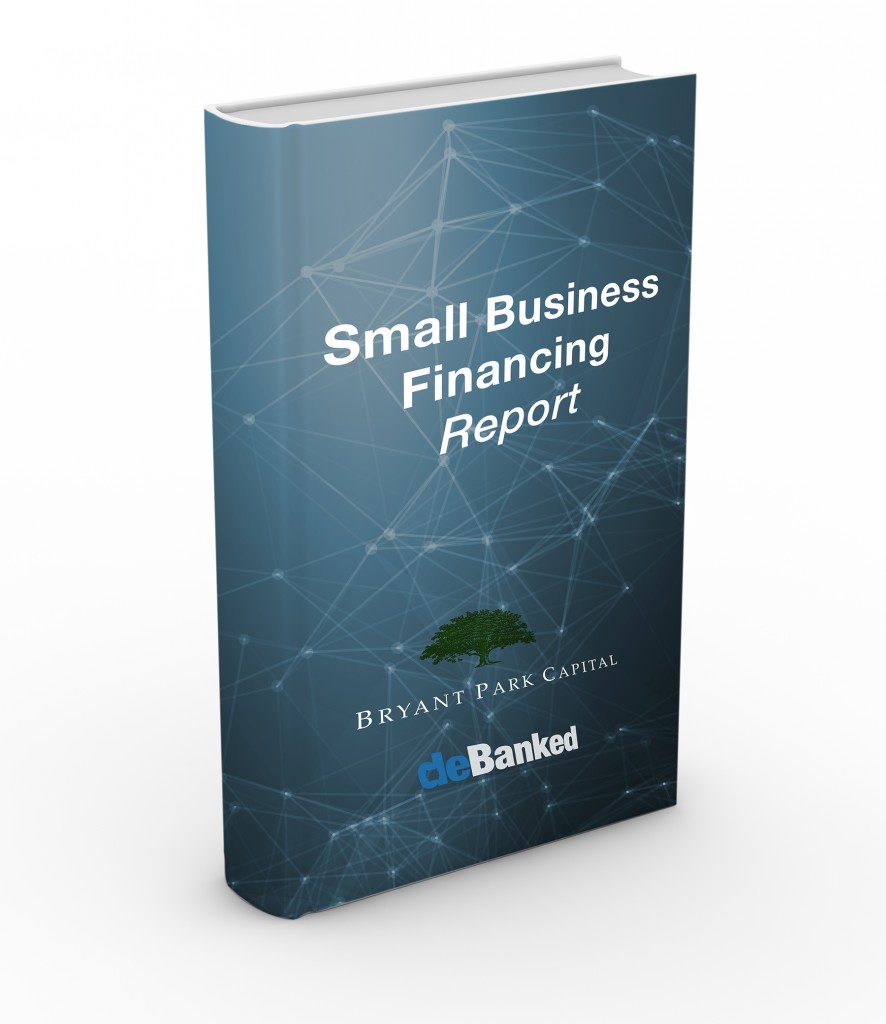

The First Ever Comprehensive Industry Report is Now Available

December 29, 2015 Months ago, investment bank Bryant Park Capital teamed up with us to conduct the first ever industry CEO survey of its kind. A sample of the initial findings were distributed at Money2020 in Las Vegas. Eligible participants that disclosed their identities to the surveyors have already received a complementary copy of the full anonymized report.

Months ago, investment bank Bryant Park Capital teamed up with us to conduct the first ever industry CEO survey of its kind. A sample of the initial findings were distributed at Money2020 in Las Vegas. Eligible participants that disclosed their identities to the surveyors have already received a complementary copy of the full anonymized report.

Today, those that either weren’t eligible to take the survey or missed the deadline to participate, can buy a copy of it.

With a sample size of small business funding companies that originate more than $2 billion annually, the final report reveals the industry’s Compound Annual Growth Rate, Average Annual Revenues, Average Annual EBITDA, Portfolio Loss Rates, Approval Rates, M&A Expectations, Valuation Expectations, Syndication Data, and much more.

This report is highly recommended for all funders and ISOs seeking to raise capital or for those that want to eventually sell their company. It’s also a must-have for any company that seeks to set short-term or long-term goals, that wants to compare themselves against the industry, or is creating a realistic business plan.

Investors in the industry also stand to benefit from this data.

If you are interested in buying the full report, e-mail sean@debanked.com.

The original report sample for public distribution

Mentioned in Forbes

Bryant Park Capital’s professionals have completed approximately 400 assignments representing an aggregate transaction value of over $80 billion.

Yellowstone Capital and Green Capital Join Family of Companies Under New Brand, Fundry

October 1, 2015AltFinanceDaily has confirmed that Yellowstone Capital has restructured through the formation of a new parent company, Fundry. Green Capital is also another subsidiary under the Fundry umbrella.

With Yellow and Green together, the business financing industry just got a little bit more colorful.

Yellowstone’s CEO Isaac Stern and President Jeff Reece have become Fundry’s CEO and President respectively.

“We have a solid foundation and a very successful business model,” Stern said. “But to maintain a position of leadership in this industry, we need to grow and we are evolving.”

Yellowstone Capital has been the subject of several news stories lately, most recently by being approved for up to $3.3 million in tax credits to move their business from New York to New Jersey.

In April, it was revealed that Stern had led a management buyout backed by a private family office that made Stern the only remaining co-founder to retain an equity stake. And in June, the industry learned that the company had originated more than $1.1 billion in deal flow since inception, ranking them high above many of their more well-known peers.

The funding leaderboard which debuted in AltFinanceDaily’s May/June magazine issue and was broadcast to attendees at the 2nd Annual AltLend conference in New York City, was in many ways a turning point for the industry.

“I would think there are many more branded funders that would have made the list but didn’t,” said Arty Bujan, Managing Member of Cardinal Equity. “Most shocking is Paypal’s $500 million.”

Richard Battista, Vice president of Business Development at theLendster commented on the eye-opening figures of the industry’s largest players in general. “This is a reflection of the explosive growth that the industry is experiencing at the present time,” Battista said. There is a huge demand for funding from small businesses, who have consistently expressed interest in trying out new funding options.”

Perhaps the story of Yellowstone Capital’s rise can best be explained by Grant McCracken’s Five Stages of Disruption Denial. McCracken, who is a Canadian anthropologist and author, known for his books about culture and commerce, explained the theory behind these five stages in the Harvard Business Review in April, 2013. They are Confusion, Repudiation, Shaming, Acceptance, and Forgetting.

Yellowstone Capital confused their competitors when they were first founded in 2009 by substituting split-processing payments for ACH to high-risk merchants. Very few people within the industry understood why they were using the ACH network over relationships with credit card processors that everyone else relied on.

That of course led to the repudiation stage where people thought they were crazy and that their model wouldn’t work and segued into shaming where the concept of providing working capital to high-risk businesses was perceived to be something that no one should do.

Through it all, Stern and his team believed many of America’s small businesses were still being overlooked and underserved despite non-bank financing and online lending growing by leaps and bounds.

“At what point do we stop helping small business?” Stern said to AltFinanceDaily in response to an inquiry about whether or not some businesses are simply unfundable.

Today, we are in between the Acceptance and Forgetting stages. The ACH debit methodology has almost entirely replaced split-processing and dozens of funding providers claim to specialize in high-risk deals, the very same kind that the industry years ago didn’t understand and resisted.

Yellowstone Capital will serve as Fundry’s ISO relationship arm while Green Capital will serve merchants directly.

“2015 is our biggest year yet, but we really see it as a year of block and tackle work to set up for what needs to be done in 2016 and beyond,” said company president Jeff Reece.

“Yellowstone’s success will simply become the baseline for what Fundry is about to do.”

Alternative Funding: Over The Top Down Under

September 2, 2015 San Francisco had its gold rush, Oklahoma had its land rush and now Australia is experiencing a rush of alternative funding. After a slow start a few years ago, foreign and domestic companies have been flocking to the market down under in the last 18 months.

San Francisco had its gold rush, Oklahoma had its land rush and now Australia is experiencing a rush of alternative funding. After a slow start a few years ago, foreign and domestic companies have been flocking to the market down under in the last 18 months.

As many as 20 new alt-funders are doing business in Australia, but that number could swell to a hundred, said Beau Bertoli, joint CEO of Prospa, a Sydney-based alternative funder. “The market in Australia has been very ripe for alternative finance,” Bertoli, said. “We see an opportunity for the alternative finance segment to be more dominant in Australia than it is in America.”

Recent entrants to the embryotic Australian market include Spotcap, a Berlin-based company partly funded by Germany’s Rocket Internet; Australia’s Kikka Capital, which gets tech backing from U.S.-based Kabbage; America’s Ondeck, which is working with MYOB, a software company; Moula, which began offering funding this year but considers itself ahead of the curve because it formed two years ago; and PayPal, the giant American payments company.

The new entrants are joining ‘pioneers’ that have been around a few years, like Prospa, which has been working for three years with New York-based Strategic Funding Source, and Capify (formerly AUSvance until it was consolidated into the international brand Capify), which came to market in 2008 with merchant cash advances and started offering small-business loans in 2012.

Some don’t take the newcomers that seriously. “There are small players I’ve never heard of,” said John de Bree, managing director of Capify’s Sydney-based office, in a reference to local Australian funders. “The big ones like OnDeck and Kabbage don’t have the local experience.”

But many players view the influx as a good sign. “I think it’s an endorsement of the market,” Bertoli said. “There’s more publicity and more credibility for what we’re doing here in terms of alternative finance.” It’s like the merchant who gets more business when a competing store opens across the street.

Besides, the market remains far from crowded. “I’m not concerned about the arrival of OnDeck and Kabbage because it really does validate our model,” maintained Aris Allegos, who serves as Moula CEO and cofounded the company with Andrew Watt.

The market’s relatively small size – at least compared to the U.S. – doesn’t seem to bother players accustomed to the heavily populated U.S., a development some observers didn’t expect. “I’m very surprised,” de Bree said of the American interest in Australia. “The American market’s 15 times the size of ours.”

Others see nothing but potential in Australia. “This is a market that will evolve over time, and we think the opportunity is enormous,” said Lachlan Heussler, managing director of Spotcap Australia.

Some view the Australian rush to alternative finance not so much as a solitary phenomenon but instead as part of a worldwide explosion of interest in the segment, driven by banks’ reluctance to provide loans since the financial crisis, de Bree said.

Viewed independently or in a larger context, the flurry of activity in Australia is new. “The boom is probably only getting started,” Bertoli maintained in a reference to the Australian market. “Right now, it’s about getting the foundation of the market established.”

To get the business underway in Australia, alternative funders are alerting small-business owners and the media to the fact that alternative funding is becoming available and teaching them how it works, de Bree said. “Half of our job is educating the market,” noted Heussler.

New players are building the track record they need to bring down the cost of funds, according to Allegos. “Our base rate is 2 percent or 3 percent higher than yours,” he said, adding that the cost of funds is more challenging than gearing up the tech side of the business.

Although the alternative-lending business started later in Australia than in the United States and lags behind America in in exposure, it’s maturing rapidly, said de Bree. Aussie funders are benefitting from the lessons their counterparts have learned in the U.S., he said.

But the exchange of information flows both ways. Kabbage, for example, chose to enter the Australian market with a local partner, Kikka. Kabbage learned from its earlier foray into the United Kingdom that it makes sense to work with colleagues who understand the local regulatory system and culture, said Pete Steger, head of business development for Atlanta-based Kabbage.

But the exchange of information flows both ways. Kabbage, for example, chose to enter the Australian market with a local partner, Kikka. Kabbage learned from its earlier foray into the United Kingdom that it makes sense to work with colleagues who understand the local regulatory system and culture, said Pete Steger, head of business development for Atlanta-based Kabbage.

Such differences mean that risk-assessment platforms that work in the United States or Europe require localization before they can perform effectively in Australia, sources said.

Sydney-based Prospa, for example, got its start three years ago and has been working ever since with New York-based Strategic Funding Source to localize the SFS American risk-assessment platform for Australia, said Bertoli, who shares the company CEO title with Greg Moshal.

Moula, which has headquarters in Melbourne, sees so many differences among markets that it decided to build its own local platform from scratch, according to Allegos.

One key difference between the two markets is that Australia does not have positive credit reporting. “We have nothing that even comes close to a FICO score,” said Allegos. The only credit reporting centers on negative events, he said.

Without credit scores from credit bureaus, funders base their assessments of credit worthiness largely on transaction history. “It’s cash-flow analytics,” said Allegos. “It’s no different from the analysis you’re doing in your part of the world, but it becomes more significant” in the absence of positive credit reporting, he said.

Australia lacks credit scores at least partly because the country’s four main banks control most of the financial sector and choose not to release credit information, sources said. The banks have warded off attacks from all over the world because the regulatory environment supports them and because their management understands how to communicate with and sell to Australian customers, sources said.

The big banks – Commonwealth Bank, Westpac, Australia and New Zealand Banking Group, and National Australia Bank – set their own rules and have kept money tight by requiring secured loans and long waiting periods, Bertoli said. It’s difficult for merchants who don’t fit into a “particular box” to procure funding, he maintained. “It’s almost like an oligarchy,” Allegos said of the banks’ grip on the financial system.

Eventually, the banks may form partnerships with alternative lenders, but that day won’t come soon, in Allegos’ estimation. It could be 12 months or more away, he said.

Even as the financial system evolves, deep-seated differences will remain between Australia and the U.S. Most Americans and Australians speak English and share many views and values, but the cultures of the two countries differ greatly in ways that affect marketing, Bertoli said. “In your face” advertising that can work well with “loud, confident” Americans can offend the more “laid-back” Australian consumers and business owners, he said.

Australians have become tech-savvy and comfortable with online banking, but they guard their privacy and often hesitate to reveal their banking information to a funding company, Allegos said. The entrance of OnDeck and Kabbage should help familiarize potential customers with the practice of sharing data, he predicted.

Cost structures for businesses differ in Australia from the U.S., Bertoli noted. Australian companies pay higher rent and have to pay minimum wages set much higher than in the United States, he said. Published reports set the Australian minimum wage at $13.66 U.S. dollars. The higher costs down under can take a toll on cash flow. “Take an American scorecard and apply it to Australia?” Bertoli asked rhetorically. “You just can’t.”

Distribution’s not the same for commercial enterprises in the two countries, Bertoli maintained. Despite having about the same geographic area as America’s 48 contiguous states, Australia has a population of 23 million, compared with America’s 322 million.

Distribution’s not the same for commercial enterprises in the two countries, Bertoli maintained. Despite having about the same geographic area as America’s 48 contiguous states, Australia has a population of 23 million, compared with America’s 322 million.

No matter how many people are involved, changing their habits takes time. Australian merchants prefer fixed-term loans or lines of credits instead of merchant cash advances, Bertoli said. In many cases Australian merchants simply aren’t as familiar as Americans are with advances, Allegos said.

Besides, the four big banks in Australia tend to solicit merchants for credit and debit card transactions without the help of the independent sales organizations and sales agents. In the U.S., ISOs and agents play an important role in explaining and promoting advances to merchants, Bertoli said. Advances make sense for merchants because advances adjust to cash flow, and they help funders control risk, but just haven’t caught on in Australia, Bertoli said. Australians resist advances if too many fees are attached, said Allegos.

Pledging a portion of daily card receipts might seem too frequent, too, he said. Besides, advances are limited to merchants who accept debit and credit cards, while any business could conceivably choose to take out a loan, said de Bree.

Advances have to compete with inventory factoring, which has become a massive business in Australia, according to Heussler. The business can become intrusive because funders may have to examine balance sheets and talk to customers, he said.

Australia’s reluctance to turn to advances, leaves most alternative funders promoting loans and lines of credit. Prospa, for example, uses some brokers to that end but also relies on online connections, direct contact with customers, and referrals from companies that buy and sell with small and medium-sized businesses.

“Anyone that touches a small business is a potential partner,” said Heussler, including finance brokers, accountants, lawyers and even credit unions, which have the distribution but not the product.

Moula finds that most of its business comes from well-established companies and that loans average just over $27,000 in U.S. currency and they offer loans of up to more than $77,000 U.S. The company offers straight-line, six- to 12-month amortizing loans.

Using a model that differs from what’s common in the U.S., Moula charges 1 percent every two weeks, collects payments every two weeks and charges no additional fees, Allegos said. A $10,000 (Australian) loan for six months would accrue $714 (Australian) in interest, he noted.

Spotcap Australia offers a three-month unsecured line of credit and doesn’t charge customers for setting it up, Heussler said. If the business owner decided to draw down, it turns into a six-month amortizing business loan for up to $100,000 Australian. Rates vary according to risk, starting at half a percent per month but averaging 1.5% per month.

Spotcap Australia offers a three-month unsecured line of credit and doesn’t charge customers for setting it up, Heussler said. If the business owner decided to draw down, it turns into a six-month amortizing business loan for up to $100,000 Australian. Rates vary according to risk, starting at half a percent per month but averaging 1.5% per month.

If companies have all of the necessary information at hand, they can complete an application in 10 minutes, Allegos said. Moula has to research some applications offline if the company’s structure deviates too greatly from the usual examples – much the same as in the U.S., he maintained. The latter requires strong customer-service departments, he said.

Kikka uses a platform based on the Kabbage model, which gives 95 percent of customers a 100-percent automated experience, Steger said. “It goes to show the power of our automation, our algorithms and our platform,” he maintained.

Spotcap prefers to deal with businesses that have been operating for at least six months, Heusler said. The funder examines records for Australia’s value-added tax and other financials, and it likes to connect with the merchant’s bank account. Spotcap can usually gain access to the account information through cloud-based accounting systems and thus doesn’t require most companies to download a lot of financial documents, he noted.

Despite the differences between the two countries, banking regulations bear similarities in Australia and the United States, sources said. In both nations the government tries harder to protect consumers than businesses because they assume business owners are more financially savvy. For consumers, regulators scrutinize length of term and pricing, sources said, and on the commercial side the government is concerned about money laundering and privacy.

Regulation of commercial funding will probably intensify, however, to ward off predatory lending, Bertoli said. Government will consult with businesses before imposing rules, he said. A couple of alternative business funders aren’t transparent with their pricing and they charge several fees – that sort of behavior will encourage regulation, Allegos said.

“I know they’re watching us – and watching us very closely,” he added.

In general, however, the Australian government supports alternative finance, Bertoli said, because they want there to be options other than the four big banks and wants small business to have access to capital. Small businesses account for 46 percent of economic activity in Australia and employ 70 percent of the workforce, he noted, saying that “if small businesses are doing badly, the economy is doing badly.”

Hence the need, many in the industry would say, for more alternative funding options in Australia.

The Rest of the Alternative Lending Industry’s Funding Numbers

July 1, 2015 Let’s be serious, the industry’s much bigger than we may have let on when we published the industry leaderboard (some mods have been made) in the May/June issue.

Let’s be serious, the industry’s much bigger than we may have let on when we published the industry leaderboard (some mods have been made) in the May/June issue.

Right after AltFinanceDaily sent the final file off to the printers in May, PayPal announced that the widely circulated $200 million lifetime funding figures were slightly outdated.

How off were they?

Oh, just by about $300 million or so. By May 7th, PayPal’s Working Capital program for small businesses had already exceeded $500 million. The industry leaderboard has been revised to reflect the news. PayPal says they are funding loans at the rate of $2 million per day, which puts them on pace for more than $700 million a year. Um, wow?

One name that’s missing from that list is Amazon, whose secretive short term business loan program is reported to have already generated hundreds of millions of dollars in loans. Given the $300 million discrepancy that PayPal let ruminate for months, we’re in no position to speculate on Amazon. Anyone could try to assess what they’ve been up to however, since they file UCCs on their clients under the secured party name “AMAZON CAPITAL SERVICES, INC.”

Of course if you’re craving specific numbers, an anonymous source inside Yellowstone Capital revealed that Yellowstone produced $35.5 Million worth of deals in the month of June alone. Yellowstone has a strategically diverse business model that allows them to either fund small businesses in-house (essentially on their own balance sheet) or broker them out to other funders. Yellowstone was listed on AltFinanceDaily’s May/June industry leaderboard at $1.1 Billion in lifetime deals and $290 Million in 2014. June’s figures indicate that they are probably well on their way to surpassing last year’s numbers.

Curiously, platform/lender/broker/marketplace company Biz2Credit has been hanging on to the same stodgy old number for more than a year.

Funded over $1.2 billion. 200,000+ happy customers.http://t.co/3h64lI4cgG #smallbusiness #Funding

— Biz2Credit (@biz2credit) June 19, 2015

They were touting that same $1.2 Billion number exactly 1 year ago. Surely they have done more since then? Biz2Credit’s service covers a much wider scope however so a direct comparison with their peers may not be appropriate. A lot of their loans are arranged through traditional banks which are typically transacted in amounts larger than the average $25,000 deal alternative lenders do.

A source familiar with Biz2Credit’s breadth said he observed a deal where the company helped a businessman in Mexico obtain financing to purchase a new helicopter, a transaction which apparently necessitated a team to fly down there to sign paperwork. Definitely not a standard transaction!

When we published the industry leaderboard initially, it admittedly omitted some of the industry’s largest players. Many firms are fairly secretive about the numbers they release and we’re in no position to disclose numbers that aren’t supposed to be public. Below is data that we hadn’t published previously.

The industry’s unsung behemoths

The industry’s unsung behemoths

The $300 million lifetime funding figure publicized by NYC-based Fora Financial can’t be that stale. It’s the number currently stated on their website and a late February 2015 company announcement revealed they were only at $295 million at the time. We feel comfortable enough to now have Fora Financial on the leaderboard.

In 2014, Delaware-based Swift Capital revealed that they had funded more than $500 million. It’s unclear how much that’s increased since then.

Credibly (formerly RetailCapital), has publicized that they’ve funded more than $140 million in their lifetime. Founded in Michigan, the company has opened offices in New York, Arizona, and Massachusetts. They’ve been added to the lifetime leaderboard.

New York City-based AmeriMerchant has a claim on their website that they have funded more than $500 million since inception. How much more exactly? We’re not sure.

Coral Springs, FL-based Business Financial Services keeps their figures mostly under wraps but a good guess would place their lifetime figures at somewhere between $700 million and $1.2 billion.

Miami, FL-based 1st Merchant Funding had reportedly funded close to $100 million in the Spring of 2014. It’s uncertain as to where they might be now.

Woodland Hills, CA-based ForwardLine surpassed $250 million in funding as far back as 2013.

Orange, CA-based Quick Bridge Funding disclosed more than $200 million in funding in late 2014.

Troy, MI-based Capital For Merchants has funded $220 million since inception. But there’s more to the story. Capital For Merchants is owned by North American Bancard, a merchant processing firm that acquired another merchant cash advance company, Miami, FL-based Rapid Capital Funding in late 2014. And coincidentally, Rapid Capital Funding had just acquired American Finance Solutions months earlier, which is an Anaheim, CA-based merchant cash advance company that had funded more than $250 million since inception. All told, North American Bancard owns at least three merchant cash advance companies: Capital For Merchants ($220 million), American Finance Solutions ($250 million+), and Rapid Capital Funding (undisclosed). There are rumors that they’re in talks to acquire at least one more company in the space, which, if true, would make North American Bancard one of the industry’s most powerful players.

Don’t bother counting up the above totals

These figures all barely scratch the surface as AltFinanceDaily’s database indicates there are literally hundreds of genuine direct funders in the industry.

Thanks to the company representatives that took the time to confirm their funding numbers with us directly. Anyone interested in sharing their figures can email sean@debanked.com. If there is a gross inaccuracy somewhere as well, please report it to us.

This page might be updated in the future so check back!

The Official Business Financing Leaderboard

June 20, 2015A handful of funders that were large enough to make this list preferred to keep their numbers private and thus were omitted.

| Funder | 2014 |

| SBA-guaranteed 7(a) loans < $150,000 | $1,860,000,000 |

| OnDeck* | $1,200,000,000 |

| CAN Capital | $1,000,000,000 |

| AMEX Merchant Financing | $1,000,000,000 |

| Funding Circle (including UK) | $600,000,000 |

| Kabbage | $400,000,000 |

| Yellowstone Capital | $290,000,000 |

| Strategic Funding Source | $280,000,000 |

| Merchant Cash and Capital | $277,000,000 |

| Square Capital | $100,000,000 |

| IOU Central | $100,000,000 |

*According to a recent Earnings Report, OnDeck had already funded $416 million in Q1 of 2015

| Funder | Lifetime |

| CAN Capital | $5,000,000,000 |

| OnDeck | $2,000,000,000 |

| Yellowstone Capital | $1,100,000,000 |

| Funding Circle (including UK) | $1,000,000,000 |

| Merchant Cash and Capital | $1,000,000,000 |

| Business Financial Services | $1,000,000,000 |

| RapidAdvance | $700,000,000 |

| Kabbage | $500,000,000 |

| PayPal Working Capital* | $500,000,000 |

| The Business Backer | $300,000,000 |

| Fora Financial | $300,000,000 |

| Capital For Merchants | $220,000,000 |

| IOU Central | $163,000,000 |

| Credibly | $140,000,000 |

| Expansion Capital Group | $50,000,000 |

*Many reputable sources had published PayPal’s Working Capital lifetime loan figures to be approximately $200 million in early 2015, but just a couple months later PayPal blogged that the number was more than twice that amount at $500 million since inception. The print version of AltFinanceDaily’s May/June magazine issue stated the smaller amount since it had already gone to print before PayPal’s announcement was made.