Why Funders Are Investing in Real Estate As Their Side Hustle of Choice

January 25, 2021

After five years in finance, Peter Ribeiro decided to strike out on his own and start US Business Funding in 2008, providing equipment leasing and financing for businesses. But when the housing market collapsed four months later, Ribeiro saw a second major business opportunity emerge. Earlier that year, he had purchased a $250,000 home in southern California that appraised for $355,000 at the time he bought it. Within seven months, the home’s value plummeted to $95,000. “I told myself I knew the area really well, so I might as well start buying some properties.”

After five years in finance, Peter Ribeiro decided to strike out on his own and start US Business Funding in 2008, providing equipment leasing and financing for businesses. But when the housing market collapsed four months later, Ribeiro saw a second major business opportunity emerge. Earlier that year, he had purchased a $250,000 home in southern California that appraised for $355,000 at the time he bought it. Within seven months, the home’s value plummeted to $95,000. “I told myself I knew the area really well, so I might as well start buying some properties.”

At that point, Ribeiro’s fledgling company still wasn’t generating much revenue. “I thought, ‘Man, I just can’t get a lot of loans done right now. I only have three or four employees.’ That’s how I got into the real estate industry.” Twelve years later and at the height of a global pandemic, Ribeiro is simultaneously running two thriving ventures —US Business Funding, and a portfolio of hundreds of rental properties he now owns.

At a time when fintech startups and other industry innovators are looking for investors, alternative lending execs like Ribeiro are instead choosing to put their money in real estate to beef up their investment portfolios. Although some execs shy away from talking publicly about their real estate dealings, citing the fact that they don’t want too much exposure, the consensus is that there’s a lot of money to be made in buying, selling and renting property – if you know what you’re doing.

“I think real estate is lucrative because when you look at the history of investments, there are two or three ways to really make money: You can put your money in the stock market, or you can put it in bonds. And the other one guaranteed to go up in value is real estate,” Ribeiro says.

“I think real estate is lucrative because when you look at the history of investments, there are two or three ways to really make money: You can put your money in the stock market, or you can put it in bonds. And the other one guaranteed to go up in value is real estate,” Ribeiro says.

To Ribeiro, real estate offers a few major advantages: It’s a tangible asset. You can leverage it as it appreciates in value. Deductions make it so you pay very little in taxes. And it offers significant cash flow. “It’s the best investment you can make,” he says.

What makes real estate an especially good fit for alternative lending and fintech execs is that they possess the skills, resources and financial literacy to succeed at it.

“Real estate is a long-term gain,” Ribeiro says. “The industry we’re in is a cash-flow cow. People who are doing well are printing money. But what can you do with that money? You can put it in the stock market, but you won’t control much. Then you pay capital gains on it.”

Attorney Paul Rianda, who represents both cash advance clients and real estate investors, says it makes sense that real estate investing appeals to alternative lenders – especially amidst the uncertainty of COVID-19.

Attorney Paul Rianda, who represents both cash advance clients and real estate investors, says it makes sense that real estate investing appeals to alternative lenders – especially amidst the uncertainty of COVID-19.

“If you’re a cash advance guy and COVID happened, then you’re not doing very well,” he says. “If you diversified your assets by doing real estate and cash advance, you’re able to weather these downturns a lot more easily than you would otherwise.”

Rianda has not yet counseled any of his own cash advance clients on real estate matters. But based on his insights from working with both areas, he says real estate would be a logical move for MCA executives, and he’s seen some of his clients in the bankcard industry buy up properties.

“One of my clients had a portfolio of merchants and sold it for a few million, then flipped over to real estate. So it’s a means (to an end),” Rianda says.

‘Snowball effect’

Ribeiro has relied on a simple strategy to steadily build his portfolio of residential properties: Buy. Fix. Leverage. Repeat.

“I feel like the portfolio is doubling every couple of years. It’s just a snowball effect,” he says.

After Ribeiro buys a home, he waits about six months before he has it appraised and fixes it up in the meantime.

“If you go to the bank within the first six months of purchasing it, they’re going to give you the actual market value of whatever you purchased the house for,” he says. “If you wait six months, they’ll reappraise the home and give its true market value, which could be another 40, 50 or 60 percent. And so now you’re going to have a lot more equity in the house, and you’re going to get a lot more money when you leverage that home to go buy the next one.”

Ribeiro says he sees lots of people making the mistake of buying a home, and then going to the bank a week or two later for a loan.

Constantly maintaining a positive cash flow is Ribeiro’s number one rule of real estate investing. “Your best friend is depreciation,” he says.

Constantly maintaining a positive cash flow is Ribeiro’s number one rule of real estate investing. “Your best friend is depreciation,” he says.

Depreciation refers to one of the key tax benefits of real estate. Since owning a rental property is technically a type of business because it generates income, the property is considered a business asset. The IRS allows you to deduct the cost of acquiring that asset – the property – over the span of its useful life. For residential properties, the IRS sets a standard depreciation period of 27.5 years.

So if you buy a $100,000 property with a $20,000 land value, $80,000 of the asset is considered depreciable. Over the course of 27.5 years, you can take an annual deduction of just over $2,900 a year.

The trick, Ribeiro says, is to stick to lower-priced properties with an 80/20 home-to-land value. Most of his properties are single- and multifamily homes between southern California and Las Vegas.

Like Ribeiro, Rianda’s investor clients concentrate on one geographic area to find the best properties. “They look at the area for a long time, understand the area,” he says. “In my neighborhood, three blocks can make a 50 percent difference in the price of a house. You need to focus on a particular geographic area and do a lot of transactions in it.”

Small portfolio, big impact

Real estate investing has provided a way for Jared Weitz to earn more money while being able to focus on his primary job as CEO of New York-based United Capital Source Inc., the company he founded.

Real estate investing has provided a way for Jared Weitz to earn more money while being able to focus on his primary job as CEO of New York-based United Capital Source Inc., the company he founded.

“For me, it’s just a really good second income stream and a way to have a secure return of 4.5% to 6.5% a year,” he says.

Growing up, Weitz got a feel for real estate by watching his uncles invest in multifamily properties. At one point, Weitz’s uncle owned 15 different multifamily homes, and Weitz would help do the maintenance on them.

Eight years ago, Weitz invested in his first two-family home and has fixed and flipped eight properties since then. He currently owns two two-family homes and invests primarily in multifamily homes in Long Island, Brooklyn and Queens. Over the next five years, he plans to pick up at least two more four- or eight-family properties. Working with a small portfolio of residences in his home state has allowed Weitz to have full control over managing his properties and to turn a good profit.

“I think for me, it just offers more liquidity,” he says. “It’s an asset I can sell and liquidate at any time. That’s really important for me.”

Ideally, Weitz would like for his investment to build generational wealth that he can pass down to his son. With many people in the U.S. unable to qualify for mortgages, Weitz sees real estate investing as an opportunity to help the economy by giving renters a place to live and put down roots. “Depending on the neighborhood, you can put yourself in a situation where you have good renters for 20 to 30 years. They want to raise their families and have their kids grow up there,” he says.

Litigation among the pitfalls

Even though Ribeiro has had success with his business model, he cautions that there’s considerable risk involved with real estate.

“I love the industry. It’s a passion. It’s beyond my wildest dreams of the size of the portfolio and how well it performs,” he says. “But don’t think it’s all cupcakes and unicorns. There’s a lot to the madness. That’s why not everyone can replicate the model.”

“Professional litigators” and multiple lawsuits from renters are a major downfall that Ribeiro points to. He sees at least one substantial suit each year and tries to settle outside of court whenever possible.

“Professional litigators” and multiple lawsuits from renters are a major downfall that Ribeiro points to. He sees at least one substantial suit each year and tries to settle outside of court whenever possible.

As an attorney, Rianda says his real estate clients call on him not just for the purchase of the property, but for various issues that occur during the ownership period.

Here’s one scenario: A property owner has a tenant who isn’t paying rent, so the property owner sues the tenant. But while the lawsuit proceedings are under way, the tenant declares bankruptcy, which puts a stall on further litigation.

“There are people who understand the system and can make it difficult for you to get them out (of the property),” Rianda says, adding that it’s important to have legal counsel readily available. “You need someone who has really done this a lot and knows how the system works to get that person out of the rental property as quickly as possible.”

To minimize liability, Ribeiro has divided his properties into about 10 different business entities – each with a separate umbrella insurance policy.

Rianda sees his own real estate investor clients follow this strategy by grouping multiple homes under the name of an LLC. “If you personally own all these various assets, there’s the potential that if something catastrophic happened at one, it could bleed into all your other properties and potentially put them at risk,” he says.

Dual careers

Ribeiro’s real estate investments and finance company both serve as full-time occupations for him. Some years, he’ll focus more on one area than on the other, depending on market conditions. He spent more time on real estate between 2008 and 2013; then his business needs flip-flopped when real estate prices started going back up. This past year, he’s directed more attention to the finance company because of COVID, which necessitated some operational changes and a need to help clients who had been trying to get PPP loans. But he’s also started investing in commercial real estate, which has taken a hit because of companies forgoing office space to save overhead costs while employees work remotely.

Ribeiro expects to start seeing more mortgage defaults on lower-level homes in 2021 and 2022, after forbearance periods are over. And he’s been leveraging his assets to start buying more properties around the second quarter of the new year. “I think it will be a good time to start buying heavy again,” he says.

An attractive investment vehicle

With the pandemic weakening business portfolios, secondary investment options might sound like just what the doctor ordered.

When COVID first hit, some of Rianda’s clients started pursuing other investments like personal protective equipment (PPE). Most of his cash advance clients closed up shop for a few months.

When COVID first hit, some of Rianda’s clients started pursuing other investments like personal protective equipment (PPE). Most of his cash advance clients closed up shop for a few months.

“As time goes on, I’m starting to see my clients go back into their lending,” Rianda says.

Even as clients start to recoup their business, Rianda sees the wisdom in other investments and says cash advance executives are well suited for real estate. “It’s just a way that people who have been successful and spin off a lot of cash for their businesses see as a safe way to diversify their income,” Rianda says. “It’s something I find that people who are doing well in their business do, regardless of what business they’re in. So cash advance guys are just following the things people have done for years.”

Ribeiro cautions that people who get into real estate should look at it as a 10-year investment minimum, and not just a two- or three-month stint.

“It’s not a lottery ticket, and it’s not an overnight race,” Ribeiro says. “This is a long-term gain. But it’s a very lucrative gain from a cash-flow perspective and a tax perspective. I don’t think there’s a more attractive vehicle than real estate.”

Immigrating From Cuba With “Nothing in my pockets,” to a CEO Funding $12 Million a Month

December 15, 2020 “Work hard, don’t ask questions, and good things will happen to you,” Frank Ebanks described his keys to success in the MCA world. “Being Positive, working hard, and keeping my eyes open: If I hadn’t been looking for opportunities at 2 am in the morning on Craigslist, I would have never known about this industry, but it’s huge, it’s such a big industry.”

“Work hard, don’t ask questions, and good things will happen to you,” Frank Ebanks described his keys to success in the MCA world. “Being Positive, working hard, and keeping my eyes open: If I hadn’t been looking for opportunities at 2 am in the morning on Craigslist, I would have never known about this industry, but it’s huge, it’s such a big industry.”

Ebanks started what would become Spartan Capital shortly after seeing an ad calling for startup investors in an industry Ebanks had never heard of, called Merchant Cash Advance.

It was around 2016. Ebanks was up late in the NYU university library, putting himself through an MBA while working as a reactor operator at the Indian Point nuclear power plant in Westchester.

Despite the job security Ebanks enjoyed, he said he wasn’t happy with his career, wasn’t getting the satisfaction he wanted. He had already made it a long way— starting before the millennium as a Cuban immigrant, immigrating to the Dominican Republic in 1998 and then Florida in 2002 with empty pockets. Shortly after arriving, Ebanks enlisted.

“I spent some time in the army; I wanted to put in some time,” Ebanks said. “I said: ‘I’m a new immigrant, what’s the best thing that I could do to reward these opportunities?’ To serve in the army, give the country a couple years, and payback in advance for this opportunity that I knew I was going to have.”

Ebanks said he learned early on to take every opportunity seriously. He served for two years and then became an engineer and contractor for the army, working on the Patriot Missile defense system. He went through college at NJIT, graduating in 2009, and following in his father’s footsteps to become an electrical engineer.

After working with South Jerseys PSE&G, Ebanks took the opportunity to work full time shifts at the the nuclear power plant, and by 2016 he was pursuing an MBA and looking for ways to grow what he called “my empire.” Used to investing in small businesses already, discovering MCA fit right within his world.

“I’ve always been active, throughout my professional career I had businesses in real estate, I owned several businesses such as laundromats, a lot of retail cell phone stores and things like that,” Ebanks said. “So at one or two am in the morning, I’m working on how to build my empire. I was on Craigslist looking for opportunities, seeing what’s out there, and somebody wanted an investment, to partner up and start a company in a new industry.”

He took a meeting and learned a ton. Although he did not end up going into business with that person, he was hooked on the concept.

“I looked at that ad, and $10,000 later, we had a company,” Ebanks said.

He learned what he needed and ended up opening his own MCA business shortly after in New Jersey, finding he loved setting up syndicated MCA deals.

He learned what he needed and ended up opening his own MCA business shortly after in New Jersey, finding he loved setting up syndicated MCA deals.

“I did some research, opened an office in New Jersey, secured a manager to run the operation, and we started brokering deals and learning about syndication.”

He worked with SFS Capital, now called Kapitus. He fell in love with the immediate gratification feedback of making deals, seeing returns on account receivables, and watching renewals come in. The business grew, but things were not always a straight climb to success.

“There was a point where things were not going well and I had to start a new company, find new parters and investors with a funding direct-only focus, and moved into my basement- my wife was unhappy with that. I started hiring people, processors, underwriters, and ISO managers in my basement,” Ebanks said. “At one point, she said, ‘Okay, this is enough. Ten strangers are coming into my house every day, you’ve got to get an office,’ so we secured an office in New York. And that’s when things took off in 2017.”

At that point, Ebanks had shifted his business model from securing deals to funding them all his own, using capital he raised. Ebanks said that being a broker partnered with Kapitus was great, but he wanted to grow and run his business entirely. The best way to do that was through ISO management, Ebanks said. Ebanks let the direct sales team phase out and he hired ISO managers, learning the ISO business as he went.

“So fast forward now: We have over five ISO managers, and we’re funding about $12 million a month,” Ebanks said. “It’s been a phenomenal journey and the most rewarding thing I’ve ever done in my life; I’m not shy to share how exciting every day is to me, and how other than my family and my kids and God, this is the most important thing my life.”

For brokers looking to get started in the industry, Ebanks has this advice to share: Don’t settle.

“Don’t settle, look for growth, and invest your money,” Ebanks said. “I always invested everything I could, 95%, every penny on the business. It matters especially at the beginning, the more you invest, don’t let it sit.”

That investment should go toward your business, your staff, and hiring. Ebanks said the more you invest, the bigger the bag, the more your firm would grow, and your employees will grow with you. Helping employees will mean they will eventually leave, but in Ebanks’ experience treating employees right creates partners.

“Some of them now are partners, and the employee-employer relationship is always more partnership,” Ebanks said. “Some of them own their own companies now, and we help each other out. If they have a big deal, they say: ‘Frank do you want to take $50,000 out of this deal?’ I say yea I trust you. I’ve known you for years.”

Now that he’s on track to grow with recurring customers, seeing some merchants come back to renew twenty times since 2016, Ebanks sees a possible bright future for Spartan Capital: becoming a chartered online bank.

“It is an alternative lending space but to offer the best products to people,” Ebanks said. “I think at the end of the day, and we need all the resources we can get, the next chapter is to apply and secure an online bank charter, it’s the future of the fintech industry.

“Why do people like doing business with us versus a bank? Some of them can do business with banks, but they choose to use us because they have direct access to us after 6 pm, they could call us Saturday, they can call us on a Sunday,” Ebanks said. “A great relationship that they can never get from a bank. I want to bring what we do in MCA to the banking industry to serve people that want banking products, but I want to give them that MCA experience.”

State That Wooed Yellowstone Capital to Its Shores Has Changed Its Mind

December 8, 2020 The Attorney General of the State of New Jersey filed a lawsuit against Yellowstone Capital, LLC and several affiliated parties on Tuesday.

The Attorney General of the State of New Jersey filed a lawsuit against Yellowstone Capital, LLC and several affiliated parties on Tuesday.

The 55-page complaint trots out a long list of allegations but appears to hone in on the company’s actions or alleged lack of action on the reconciliation provision of its merchant cash advance agreements. The AG alleges that the manner in which the defendants conducted themselves should subject the agreements to the state’s lending laws.

Notably, the State says these unlawful acts began in July 2015, months before the State lured Yellowstone to relocate its headquarters there from New York.

In September 2015, for example, the New Jersey Economic Development Authority approved Yellowstone for up to $3.3 million in Grow New Jersey tax credits. When Yellowstone officially moved to Jersey City in 2016, the city’s mayor even made a personal appearance at the office to welcome them.

Now that Covid-19 is ravaging the state’s economy, the political opinion has seemingly changed.

“We are taking action today to protect our State’s small businesses and small business owners from predatory practices in the market for merchant cash advances,” said Attorney General Gurbir Grewal. “Local businesses are struggling due to the COVID-19 pandemic, especially since many were unable to take advantage of the limited relief made available by the federal government through the Paycheck Protection Program. We will not tolerate – now or ever – efforts to take advantage of them through predatory lending and collection practices.”

In 2015, however, New Jersey officials assessed that Yellowstone would have a “net benefit to the State of $23.3 million over [a] 20 year period” and that it was economically important to attract their business operation. Yellowstone was at that time considering a move to White Plains, NY from the company’s original Manhattan offices, State officials argued, so they really had to offer the tax credits for them to come to New Jersey instead.

“Yellowstone is comprised of a team with years of industry experience,” says a 2015 project summary prepared by NJ Economic Development Authority officers Diane Ubinger and Mark Chierici. “As both a direct source of funding and as part of the country’s largest Independent Sales Organization network (‘ISO’) it has numerous in-house funders who concentrate on specific industries/businesses, while also having numerous funding partners within the MCA industry who fund its ‘outside-the-box’ transactions.”

But later in 2019, the deal changed when Yellowstone’s capital investment requirement was not met, the Authority’s communications director told AltFinanceDaily. As a result the company ended up not receiving the tax credits.

“The NJEDA is committed to ensuring that businesses approved for tax incentives are compliant with all program requirements and to making sure that companies that do not meet their commitments to the taxpayers of New Jersey do not benefit from NJEDA-administered programs.”

Additional allegations in today’s complaint were made regarding Yellowstone’s historical use of confessions of judgment, a recovery tool that was largely eradicated by the passing of a law in New York in 2019.

The AG’s case was filed in Hudson County in the Superior Court.

Yellowstone Capital offered no comment to this story.

Update: 12/9/20 This story has been updated to reflect the current status of the tax credits as provided by NJ EDA.

Where Fintech Ranks on the Inc 5000 List for 2020

August 12, 2020Here’s where fintech and online lending rank on the Inc 5000 list for 2020:

| Ranking | Company Name | Growth |

| 30 | Ocrolus | 7,919% |

| 46 | Yieldstreet | 6,103% |

| 351 | Direct Funding Now | 1,297% |

| 402 | GROUNDFLOOR | 1,141% |

| 486 | LoanPaymentPro | 946% |

| 534 | LendingPoint | 862% |

| 539 | OppLoans | 860% |

| 566 | dv01 | 830% |

| 647 | Fund That Flip | 724% |

| 1031 | Fundera | 449% |

| 1035 | Nav | 447% |

| 1053 | Fundrise | 442% |

| 1103 | Bitcoin Depot | 409% |

| 1229 | Smart Business Funding | 365% |

| 1282 | Global Lending Services | 349% |

| 1360 | CommonBond | 327% |

| 1392 | Forward Financing | 319% |

| 1398 | Fundation Group | 318% |

| 1502 | Fountainhead Commercial Capital | 293% |

| 1736 | Seek Capital | 246% |

| 1746 | PIRS Capital | 244% |

| 1776 | Braviant Holdings | 240% |

| 1933 | Choice Merchant Solutions | 218% |

| 2001 | Fundomate | 212% |

| 2257 | Lighter Capital | 185% |

| 2466 | Bankers Healthcare Group | 167% |

| 2501 | Fund&Grow | 165% |

| 2537 | Central Diligence Group | 162% |

| 2761 | Lendtek | 145% |

| 3062 | Shore Funding Solutions | 127% |

| 3400 | Biz2Credit | 110% |

| 3575 | National Funding | 103% |

| 4344 | Yalber & Got Capital | 76% |

| 4509 | Expansion Capital Group | 70% |

Checkout in the time of COVID

August 10, 2020 Point-of-sale (POS) lenders, also referred to as buy-now-pay-later (BNPL) firms, allow shoppers to break up their individual purchases into installments, often without interest. By adding BNPL as an option at checkout or further upstream in the purchase process, the consumer’s buying power is increased and they are often less likely to abandon their checkout cart. It is a win / win for all stakeholders.

Point-of-sale (POS) lenders, also referred to as buy-now-pay-later (BNPL) firms, allow shoppers to break up their individual purchases into installments, often without interest. By adding BNPL as an option at checkout or further upstream in the purchase process, the consumer’s buying power is increased and they are often less likely to abandon their checkout cart. It is a win / win for all stakeholders.

For these reasons, POS lending is one of the fastest growing segments in unsecured credit, with volume increasing at 40 percent year-over-year. COVID has further accelerated the demand for credit options at checkout.

According to McKinsey, annual growth is expected to jump to 150 percent thanks to an explosion in online shopping and government subsidy programs boosting retail sales. In Canada, firms such as Uplift, Paays, and PayBright are all seeing merchant demand skyrocket for their services, with the latter onboarding over 250 merchants per month.

K-Ching!

POS lenders are able to subsidize APRs by charging the merchant a fee of 4-6 percent of the purchase price. This is on average 2 percent more than the fees charged by credit cards companies. Despite the larger fee, BNPL is very attractive for retailers for a number of reasons. By providing point of sale financing retailers see:

- 30% increase in basket size

- 25% reduction in cart abandonment

- 20% increase in repeat traffic

With installment payments as an alternative, credit cards have seen a decrease in popularity among young shoppers, particularly on smaller ticket items under $500. There are a number of reasons why:

1. Clunky signup experience. Signing up for a credit card at checkout requires lots of paper, personal information, signatures and significant patience – antithetical to the one-tap checkout shoppers are accustomed to. Alternatively, BNPL approval is instant at checkout. 75% of merchants even advertise POS financing far before the register, at the beginning of the customer journey which can increase conversion by two to three times.

2. Challenge to qualify. 19 percent of consumers ages 22 to 30 lacked the credit history to be approved for credit cards in the first place. Many BNPL products do not perform credit checks, and those that do use alternative data sources to underwrite thin-file borrowers.

3. High APRs. With their parent’s household debt in their rear view mirror, many younger shoppers have an aversion to carrying revolving credit balances. Millennials on average carry two fewer cards than their parents. Psychologically, $1000 on your credit card looks scarier than four installments of $250 over time.

4. Customer confusion. Inactivity fees, late fees, over-the-limit fees, cash advance fees, are all poorly understood and masked within dense monthly statements. BNPL offers an elegant digital first experience and straightforward reporting.

The Supporting Cast

Today POS lenders are competing in a land grab for merchant partnership. But for FIs and fintechs who have yet to plant their flags, there are still ways of participating in the BNPL boom.

- Banks. Banks have largely participated indirectly in the BNPL sector, by providing portfolio financing to fintechs or by offering installment options for larger ticket items within their existing credit card programs. Wayne Pommen, CEO of PayBright, sees more bank and fintech collaboration in the next few years: “I predict more buying and partnering, Banks are too far behind to build this themselves.” Marcus Pay, the recently launched retail banking arm of Goldman Sachs is the only group to directly compete in the POS financing ring, with JetBlue as their launch partner.

- Platforms. E-commerce enablers that power millions of independent merchants are piling in to embed POS financing within their platforms. Marketplaces Ebay and Etsy have partnered with Afterpay and Klarna, while the digital infrastructure whale Shopify has an agreement with Affirm.

- Cards. Traditional credit card companies who have the most to lose from BNPL are getting ahead of the trend in several ways. Visa took a controlling stake in Klarna in 2007. More recently they launched Visa Installments, a developer tool for issuers in the Visa network to pilot branded installment products. Though Visa Installments stretches the definition of BNPL, David Fry, CEO of travel financing startup Paays does not mind the ambiguity. “I am not religious about the distinction between cards and installments. What we care about is what the customer is looking for, and what they have to pay to get access to that product”.

POS Lending has the potential to transform consumer lending as it’s evolution is inextricably tied to the growth of e-commerce. It is all about understanding the needs of the shopper and their digital journey. POS lenders are making it increasingly easy for merchants to streamline the buyer path to purchase.

MCA in Conversation: Where do we go from here?

July 27, 2020 DeBanked Magazine recently posted the “Underwriter’s Song” to highlight an entire industry’s yearning for simpler times, claiming it was the MCA soundtrack for 2020. But I disagree and nominate a different song. You see, growing up in the south with a close-knit family gave way to a childhood filled with generations worth of entertainment. Many of my summers and holiday vacations were spent with the Turner Classic Movie channel playing in the background, and songs from the Oldies Country station on the radio. I tell you this to explain how I am reminded of a song I’ve heard countless times before, and is more applicable today than ever before. That song is “If We Make It Through to December” by the venerable Merle Haggard, a tune whose message resonates with not only the merchant cash advance industry, but our entire country.

DeBanked Magazine recently posted the “Underwriter’s Song” to highlight an entire industry’s yearning for simpler times, claiming it was the MCA soundtrack for 2020. But I disagree and nominate a different song. You see, growing up in the south with a close-knit family gave way to a childhood filled with generations worth of entertainment. Many of my summers and holiday vacations were spent with the Turner Classic Movie channel playing in the background, and songs from the Oldies Country station on the radio. I tell you this to explain how I am reminded of a song I’ve heard countless times before, and is more applicable today than ever before. That song is “If We Make It Through to December” by the venerable Merle Haggard, a tune whose message resonates with not only the merchant cash advance industry, but our entire country.

The Expectations and Reality

Way back in March and April, the consensus appeared to be an expected return to “normal” by June, while areas hit hardest by COVID-19 would return by July. Yet here we are, teeter-tottering on the fence of moving forward. Now, our country is faced with the possibility of a second wave of shutdowns, rising crime, riots, a fourth stimulus, and funders whose workforce remains remote or have yet to resume funding. The proverbial “goal post” has moved yet again, and with it the expectations of many of us in the industry. Over the past few weeks, I had the opportunity to speak with a number of our referral partners to gauge their thoughts on the current state of our industry. A common theme in our discussions was the desire for validation. Not just as a business owner, but as an employer. They wanted to be reassured that they were taking the best steps forward and not alone in their decision making. To help those seeking the same validation, here is what the majority had to say:

- Yes, all had to terminate or furlough staff on various levels.

- Yes, all adjusted marketing budgets.

- Yes, all are struggling with managing remote employees.

- Yes, all are finding it harder to place files.

- Yes, all are seeing interruptions in relationships with funders and merchants alike.

- Yes, all are competing against the Government’s low-cost products.

- Yes, all are having files killed in late stages of funding or having offers adjusted.

- Yes, all are struggling to predict what comes next.

- Yes, all are managing unrealistic expectations from clients.

- Yes, all are having merchants walk away from fair and just offers.

- Yes, all are struggling to remain motivated.

- And yes, all of you are doing the best you can!

The New Normal

The Word Cloud below describes the state of the MCA industry using our partners’ own words. I find that the overall thoughts are best visualized by taking a step back to see which stand out the most. Our conversation was focused on the industry as a whole, then a discussion specific to Elevate Funding and how we’ve pivoted during these unprecedented times. As you can see, some of the keywords that stand out the most are; merchants, PPP, offers, funders, and marketing.

Much of the conversations focused around merchants and their new funding expectations. Each partner I spoke with agreed the demand for money is there, but the willingness to move forward on offers was very low. This reluctance is driven in part by low cost expectations based on PPP and SBA product rates, as well as uncertainty over increased debt in an unstable market. We’re also seeing a change in merchant demographics, where the mid-sized small businesses who previously did not qualify for SBA loans, now have access to these products. As a result, the remaining merchants whose best option is an MCA are now located on the opposite extreme ends of the spectrum; either those who did not qualify for PPP or SBA EIDL, and the large-scale businesses whose lines were revoked by their bank. Our response as a company has been to adjust our offers to better suit merchant’s expectations, and to shift from underwriting a business owner’s activity to underwriting the consumers’ activity. Monitoring government restrictions down to a county level countrywide and understanding consumer trends has enabled us to further mitigate risk during a time of uncertainty, and not only fund deals, but fund deals that will perform.

Meanwhile, our industry is seeing credit profiles and business profiles that have never applied in our space before, as a decreasing number of providers are available to service current merchants. During our conversations, some expressed a concern over lack of A-paper funders. Many of whom have either paused funding or entirely moved over to servicing PPP products. Another concern was the mental toll of having deals fall apart at the eleventh hour due to fast changing qualifications, variations in merchant revenue, or funders deciding to pause funding at inopportune times. These factors combined with the increasingly common “bait-and-switch” technique of funders providing a large offer, only to change to a much lower offer in the final stages of funding, has left many broker shops and ISOs feeling very discouraged.

The Path Upward and Onward

The conversations were not entirely negative, as new marketing opportunities have opened up with the goliaths of the industry such as Kabbage, OnDeck, Lendio, and Square shifting their marketing dollars towards PPP and SBA products. Many folks are finding their advertising dollars across marketing platforms are stretching further, particularly with search engine optimization. While this opens up an increased likelihood of fraud and in applicants who fall below qualifications, it has enabled many shops to operate on an even playing field with inbound marketing. Many small funders, including Elevate Funding, have already created new products to cater to lower revenue merchants and those directly affected by COVID-19. We’ve already received tremendous response on this change from partners and merchants alike. As merchants slowly shift back towards alternative financing solutions once the government runs out of money for its loan products, we remain optimistic there will be increased opportunities in terms of both volume and quality.

While the Word Cloud highlighted a number of topics, it also highlighted important topics that were not discussed; Expectations, Renewals, Commission, Aggression, and Repositioning.

Expectations in particular, is of note as it is different from opinions. Everyone has an opinion, but there is a tremendous sense of uncertainty going forward and it’s very difficult to create expectations or goals when forecasting is not possible. Many companies are doing away with forecasting models altogether, and switching to a dashboard for production goals and expectations based on real time data.

The drastic change we’re seeing now should demonstrate the importance of renewals and customer retention. Neither of which were brought up during all of my partner discussions. Over time, the industry has moved away from a “residual mindset” to seeking instant gratification of new fundings in the quest for market share supremacy. As funders, we have to ask ourselves; Are we inadvertently throwing out the baby with the bathwater with new deal bonus structures and monthly promotional campaigns to drive new deal growth? Or perhaps, renewals were scarce in discussions because when funders said when funding stopped, they meant all funding? While I can’t speak to each funder’s operations, Elevate has continued to fund throughout the pandemic with established merchants and renewals being a saving grace to drive our momentum forward. In my opinion, client retention has never been more important during an ever-changing landscape.

I was shocked to see commission taking a backseat to approvals and banks during our discussion. But the focus has seemingly move towards approvals and conversions, which will in turn lead to commissions returning. Which brings me to Aggression and Repositioning. The state of our industry is a timid one, and it’s neither the fault of the funders or the merchants. Many experts will tell you that our space was overdue for a market correction of sorts, because many were far too aggressive for far too long. This aggression gave way to bad habits such as lowered underwriting standards and lack of consideration for merchant ability to repay. More and more funders are shifting back to “normal” guidelines, providing fair and just offers. This is an encouraging sign that we are finding our way back to sustainable positive growth. But it will take time for the industry to fully reposition itself. Something that is being delayed by products from the PPP, SBA, and the hope for a third round of stimulus.

But hope is on the horizon. While the pessimists will look at that word as a form of denial, I challenge all of you to take a glass half-full approach. Hope is the confident expectation of good. The change and adjustments we’re experiencing now are what life is all about, and will ultimately lend way to better things. If you’re in need of a little dose of hope, or want a sounding board to know you’re not alone through this, feel free to drop me a line at heather@elevatefunding.com.

Stay safe, be well, and do not lose hope.

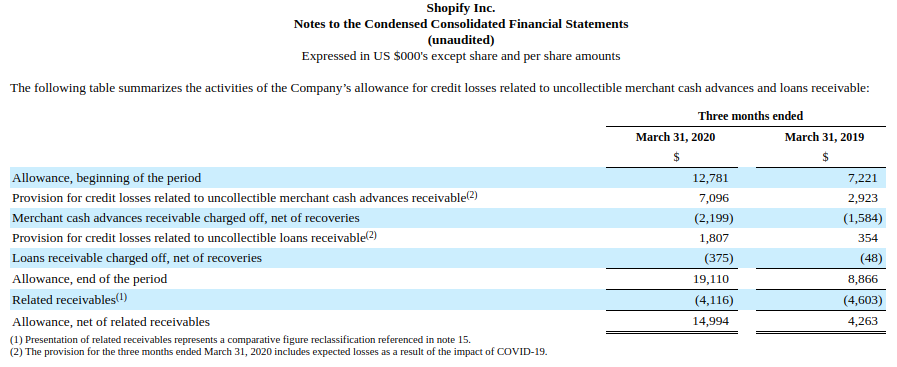

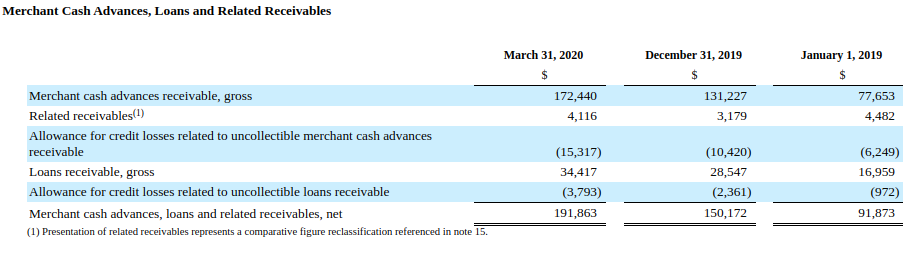

Shopify Shows Strength in Q1 Results, Issues $162.4M in MCAs and Loans

May 6, 2020eCommerce platform Shopify, 2nd only to Amazon in retail eCommerce sales, issued $162.4M in merchant cash advances and business loans in Q1, up from $115.9M in the previous quarter. The statistic pushed them past the $1 billion threshold of funds cumulatively issued since inception.

The company’s provision and allowance for loan losses ticked up from significantly from the same period the prior year but Shopify at that time was originating 50% less volume.

The company reported a GAAP net loss of $31.4M on $470M in revenue. Shopify also has approximately $2.36B in cash and cash equivalents on its balance sheet.

The company reported an increase of monthly recurring revenue, thanks to an increase in the number of merchants joining the platform, strong app growth, and Shopify Plus fee revenue growth.

Shares of Shopify (NYSE: Shop) jumped by more than 5% after the announcement.

Funding Metrics Announces New $100 Million Revolving Credit Facility

March 4, 2020

Bensalem, PA, March 4, 2020 – Funding Metrics, LLC (the “Company”) announced today the closing of a new $100 million revolving credit facility with a multi-billion dollar institutional credit fund. The Company will use the funds to expand and accelerate the growth of its small business funding platform. Brean Capital served as exclusive financial advisor to the Company on the transaction.

“We are very pleased to announce this new $100 million facility, which will allow us to significantly expand our ability to provide funding to the growing small business community across the United States,” said Co-Founder, Chairman and Chief Executive Officer, David Frascella. “This new facility represents an exciting milestone in our continued growth. Funding Metrics has tripled its origination volume since 2017, totaling over $500 million since company inception. I am very proud of the robust funding platform our team has created, the strong relationships we have developed with our independent sales organization partners, and especially the trust placed in us by our merchants. Funding Metrics has created a best of breed technology based platform allowing most funding offers to be sent in under three hours.”

Additional capital provided by the facility will allow Funding Metrics to capitalize on growth opportunities in 2020 and beyond as well as on the extensive infrastructure of people and technology it has built over the last few years. Mr. Frascella added, “We look forward to additional submissions from the ISO network and funding the next wave of small business leaders nationwide.”

About Funding Metrics

Funding Metrics is a leading data and analytics driven online provider of funding for small businesses throughout the United States. The Company uses proprietary risk models combined with real-time cash flow data to evaluate business performance and provides growth capital for entrepreneurs in a fast and efficient way through its two online brands, Lendini and QuickFix Capital. Since 2014, the Funding Metrics has provided over $500 million in funding to more than 9,500 small businesses in all 50 states. The Company is headquartered in Bensalem, PA, with additional offices in Jersey City, NJ and San Jose, Costa Rica.

For more information, please visit: www.fundingmetrics.com

For more information / questions / interview requests / media inquiries, please contact:

David Frascella

Email: info@fundingmetrics.com | Phone: 855-212-6610