Why We Shouldn’t Stop Calling it Peer-to-Peer Lending

June 1, 2015 There’s a troubling undercurrent brewing in the marketplace industry, the death of the word peers. We’re not supposed to say peer-to-peer lending anymore since few platforms actually allow for people to lend directly to their peers. In the case of Lending Club and Prosper, investors are actually lending money to the platforms themselves.

There’s a troubling undercurrent brewing in the marketplace industry, the death of the word peers. We’re not supposed to say peer-to-peer lending anymore since few platforms actually allow for people to lend directly to their peers. In the case of Lending Club and Prosper, investors are actually lending money to the platforms themselves.

Emphasizing the appropriate terminology probably makes it easier for people to understand. If it’s not peer-to-peer after all, then calling it that only serves to mislead potential borrowers and investors alike. And yet the term persists largely because the average person is still able to invest in an asset class it never was able to before, notes backed by the performance of individual consumer loans.

It could be argued that without money from peers to buy these notes, the loans themselves would never get issued, making it still peer-dependent or at least peer-relevant.

A game for Wall Street

Jorge Newberry wrote several months ago that the little guy as most of us imagine a peer to be, is dead. He was replaced by Wall Street, BlackRock, and Wealthy bankers. “These were killers,” He wrote. He added that while the industry “initially attracted ordinary citizens to invest in modestly sized consumer loans to people like them, over the last few years those peer investors often have been elbowed out and replaced by Wall Street’s finest.”

Retail investors have bemoaned the trend via online message boards, sometimes even accusing the platforms of giving the institutions first dibs on the highest quality loans and leaving the little guys to fight over nothing but the scraps that are more likely to underperform.

Even Dara Albright, the co-founder of the LendIt conference has acknowledged the takeover. In The Financial Advisor’s Guide to P2P Investing, Albright writes, “Unfortunately, what began as a true person-to-person marketplace – with the ordinary individuals lending to and borrowing from one another – has since become monopolized by institutional investors whose deep pockets and technological advantages have all but driven the individual lenders out.”

Further along in the paper, Albright makes the case that individuals need to take advantage of the yield these loans offer to narrow the wealth divide. She makes a compelling argument for investing but stops short of proposing a solution to regain market share. “There aren’t enough p2p loans to facilitate the strong investment appetite,” she concluded.

But just as the marketplace community has conceded the death of peers, the numbers don’t exactly reflect their sentiment.

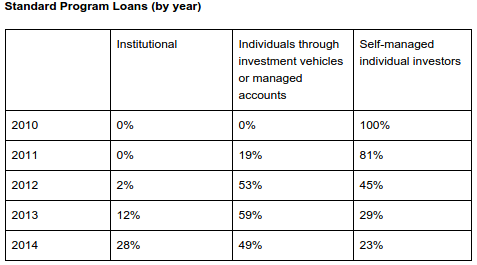

Only 28% of Lending Club’s loans went to institutional investors in 2014.

Only 28% of Lending Club’s loans went to institutional investors in 2014.While Newberry and Albright have made the case that retail investors are being locked out, there’s a dangerous flip side, they just might be getting locked in. If marketplace lending truly is becoming a game for Wall Street by Wall Street, then the few retail investors who are invested in it could eventually become collateral damage in a pissing match between wealthy bankers.

Investor faith

There are already concerns that the incentive for marketplaces are not aligned with those of their investors. PeerCube co-founder Anil Gupta wrote this on the LendAcademy forum about Prosper, “The quest to increase originations and revenue will trump any such risk management attempts, like what happened with banks issuing mortgages to unqualified borrowers in order to boost their own bottom lines.” He wrote that in response to an upset user whose borrower declared bankruptcy before making even a single payment towards their Prosper loan.

The user was questioning how Prosper would handle this since the timing of the loan prior to the bankruptcy filing had all the hallmarks of fraud.

Gupta added, “There is very little incentive for LC and Prosper to pursue such collections and recoveries claims. When LC was investing its own money in loans, they pursued collections and recoveries more vigorously (11.19% collection in 2007 vs 5.53% collection in 2011). It is no longer Prosper and LC money at risk.”

The user is not alone in his collections fears. Just a few days earlier I realized that 4.6% of all the notes I had purchased on Lending Club had already defaulted, a number that troubled me considering my average note is only 10 months old. With another 3-4 years still to go until maturity, the rate of defaults is already quite high.

The user is not alone in his collections fears. Just a few days earlier I realized that 4.6% of all the notes I had purchased on Lending Club had already defaulted, a number that troubled me considering my average note is only 10 months old. With another 3-4 years still to go until maturity, the rate of defaults is already quite high.

And while I’ve been told that my own personal stats are relatively normal, other retail investors occasionally run into quirks that force them to question the soundness of the reporting they receive.

For example, veteran users commonly rely on the FICO score updates Lending Club will publish for each issued loan. If a borrower’s score is dropping, you could sell the note for a discount to an interested buyer on a marketplace such as folio. Several people have admitted to using this strategy to mitigate losses. There’s just one problem, a user discovered a discrepancy in Lending Club’s FICO reporting. In at least one case, the borrower’s FICO score may have been overstated by more than a hundred points. For users beholden to the accuracy of these figures in order to properly execute their investment strategy, it’s a difficult pill to swallow.

Call it a kink or an oddity. Maybe it’s something that needs to be fixed or maybe something is being miscommunicated. Whatever is going on there, these are the kinds of risks that institutional capital is supposed to be able to tolerate in their quest for yield, but it’s gut wrenching for retail investors.

In the instance of the suspected bankruptcy fraud, several responses by fellow investors gave the impression that the platform simply isn’t going to care because they make money off of issuing loans, not collecting on them. That’s the exact type of Wall Street attitude that could come back to hurt retail investors.

Marketplace lending might not technically be designed as peer-to-peer but the little guy and their actual peers certainly have their funds at stake. Calling it a game for big banks, the wealthy, and Wall Street only encourages the players involved to take bigger risks, reduce transparency, and shrug off genuine criticism.

We can’t let that happen.

The Dumbest Guy in the Room

May 11, 2015 “This is the absolute dumbest thing I’ve ever seen,” she said while raising her voice. She was visibly agitated as if someone had just attempted to pass off a child’s crayon drawing as their doctoral dissertation. I began to laugh, not at her, but at the irony of the truth she was going on about.

“This is the absolute dumbest thing I’ve ever seen,” she said while raising her voice. She was visibly agitated as if someone had just attempted to pass off a child’s crayon drawing as their doctoral dissertation. I began to laugh, not at her, but at the irony of the truth she was going on about.

“So what would need to be different in order for this to be a more viable idea? Like what would I need to change and come back with?” I asked.

“Come back?! COME BACK?! Don’t come back,” she shouted while taking my business plan and literally crumpling it into a ball and throwing it on the ground. She then got up and left. She was shaking from the rage. I was the dumbest person she ever encountered and it took effort for her not to kill me.

This experience happened to me three years ago when a NYC-based Venture Capital group sent out invitations to a free seminar and workshop. I liked the refreshing thought of hearing what VCs had to say, especially those not familiar with the merchant cash advance industry. Besides, I had a few concepts I wanted to get feedback on, and thought this would be a great opportunity to do it.

The seminar was more of a fireside chat, held by a zen-like VC I’ll refer to as Rain. He was in his mid-30s, wore a long flowy purple velvet shirt and sat indian style and barefoot in the front of the room. It was a stark contrast to the attendees in the audience, all of whom were wearing suits. Rain walked the crowd through his experience as a VC, most of which seemed to be an annoyance to him. Startups were full of personal drama of which he often got roped into. There was always a partner who was an idiot, a delusion the founder(s) couldn’t see past, or an insatiable need for additional funds.

And during the Q&A at the end, an attendee asked him if he would ever consider using a VC to raise money if he were not a VC himself. “Put the phones down guys, this stays here,” he said. “I wouldn’t.”

However confusing that might come across as, it didn’t change the energy in the room. Just about everyone who attended had an idea for a startup and desperately wanted VC funding.

Afterwards, you were allowed to schedule a one-on-one with one of their startup experts to develop your ideas further. It sounded cool and it was free, so I signed up.

I drafted up a concise business plan based upon a model that was just starting to take root in the merchant cash advance industry. It had its own little twist and I’m sure flaws too, but I believed this one-on-one would be a helpful conversation where I could get honest feedback without giving anything away to potential competitors.

Three minutes into the meeting, I was being scolded. “What do you mean it would break even for the first 2 years?!”

“Oh, well what I’m try –,” I attempted to respond. She talked over me. “You mean to tell me you would make no money in the first 2 years? Are you starting a charity?!”

“Well I was under the impress–,” I started, but she kept going. “This is the absolute dumbest thing I’ve ever seen.”

It was the hardest no I had ever gone through. I looked around the room to see if the other one-on-ones being conducted were going the same way. They weren’t. Everyone else looked to be cozying up to each other, crunching numbers, sharing laughs, and possibly on their way to even getting funded.

It was the hardest no I had ever gone through. I looked around the room to see if the other one-on-ones being conducted were going the same way. They weren’t. Everyone else looked to be cozying up to each other, crunching numbers, sharing laughs, and possibly on their way to even getting funded.

Not me though. I was the dumbest guy in the room, too dumb to even come back with something better. It was a humiliating moment considering I thought this was supposed to be an instructional meeting where the experts would essentially help you master a business plan.

As I walked out of the office towards the elevator, I noticed that even the cheery receptionist who had excitedly welcomed me in, ignored me with her head down as I walked out.

There goes the dumbest guy that ever existed, I imagined she was thinking.

My world spinning as the elevator descended, I tried to recount how it went wrong so quickly. I had showed her a pro-forma P&L that broke even for the first two years as I would reinvest 100% of the profits back into marketing to scale. I personally didn’t like it that way. I wanted to make money, but everyone around me was bleeding red and raising tens of millions along the way. I had started to believe that sacrificing any shred of profitability in exchange for growth is what got investors excited.

My expert didn’t share that view. A business that wasn’t profitable wasn’t a business. It was dumb, and not just regular dumb, but the dumbest thing that anyone ever thought of. EVER.

A couple of days later when I had shaken off the blow to my self esteem, I was thankful for the experience. She was a New Yorker to the core and so was I. I had no inner desire to start a business that didn’t make money (for the sake of disrupting or whatever), but I was being swept up in the craze of companies that were doing just that. She brought me back to reality, though she left a lasting imprint of a boot on my ass.

Three years later, companies with models similar to the one I had cooked up have raised hundreds of millions of dollars. They don’t break even. They lose money, lots of it. But they are looked upon and celebrated as some of the brightest guys in the room. Many of those guys are smarter than me and are probably executing their concepts way better than I ever could. But the lose-a-lot-of-money and grow model isn’t meant for everyone. It all depends on who you’re talking to.

In HBO’s Silicon Valley, a hit that many view as more of a reality show than a sitcom, they poke fun at a truth purveying the California startup scene. Forget profits, the show explains, just having revenues hurts your chances of raising money.

“If you have no revenue, you can say you are pre-revenue,” says the show’s billionaire Russ Hanneman. “You’re a potential pure play. It’s not about how much you earn; it’s about what you’re worth. And who’s worth the most? Companies that lose money! Pinterest, Snapchat, no revenue. Amazon has lost money for the last 20 years, and that Bezos motherfucker is the king!”

“If you have no revenue, you can say you are pre-revenue,” says the show’s billionaire Russ Hanneman. “You’re a potential pure play. It’s not about how much you earn; it’s about what you’re worth. And who’s worth the most? Companies that lose money! Pinterest, Snapchat, no revenue. Amazon has lost money for the last 20 years, and that Bezos motherfucker is the king!”

Two years ago, Bezos was worth $25 billion and was the 20th richest person in the world. Some experts might say a business model that loses money for 20 years would qualify as the new winner for dumbest thing that ever existed ever. It’s apparently just the opposite.

But once you find an investor that believes in the loss model, do you take the money and then go out and disrupt, hoping that somehow you’ll end up a billionaire?

Loan broker Ami Kassar is faced with that very dilemma. In his recent blog post, he wrote about the offer he has on the table from a VC, “While I could substantially grow my top line – the chances of making any profit are small and the chances of losing money are high.”

Fictional billionaire Russ Hanneman would surely approve, but over in realityville, Kassar is balking. “I can only speculate that they’re more interested in market share – than profits. Their investors want growth. They’re on the venture capital treadmill.”

Admittedly, I poked fun at Kassar, an entrepreneur I’ve often sparred with online. “Should I be worried that in their quest for growth they will build a train and run me over?” He asked in his blog.

Of course I linked to it in the following manner:

Kassar concludes that sustainable long term value is the only logical way forward. Is he wrong?

The current investment atmosphere where anybody with a model and a programmer is raising hundreds of millions of dollars to basically see how fast they can spend it all, is affecting those that have always believed in profits and longevity.

In another post by Kassar just a week earlier, he wrote, “Am I missing the boat and doing something wrong? That’s how I have felt lately as I’ve watched the emergence of the online small-business financing space. It seems every other week I wake up to another announcement about a company in the small-business financing space who has raised a lot of money from venture capitalists at a really high valuation.”

Just last week, consumer lending startup Affirm raised $275 million in a Series B round. Many people in the alternative lending community had never heard of Affirm but they are apparently so good that they can raise a quarter billion dollars.

Investors are scrambling. They don’t want to be left out. On multiple occasions, I have heard of investors skipping basic due diligence in a rush to capture a deal. Some of those deals blew up in a matter of weeks, others in months when they realized they didn’t even know who the owners were or what financial standing they were in.

Lending Club and OnDeck have received billion dollar valuations. That’s what everybody wants, though the market has temporarily cooled on OnDeck, a company that has lost money for almost eight straight years.

Even Shark Tank investor Kevin Harrington has gotten in on it, through his new business loan marketplace, Ventury Capital.

One thing looks certain three years after I met with that expert. The supposed dumbest thing that could ever be conceived of ever has made tons of people millionaires.

A year ago, Kevin Roose of New York Magazine wrote this of profitless startups, “They’re simply taking millions of dollars in venture capital with the hope of keeping prices low, pushing rivals out of the market, and eventually finding a way to turn a profit.” It can be predatory pricing, Roose argues. Basically large venture backed companies can sell below their cost using unlimited funds until the competition is out of business. Then with the entire market all to themselves, they can figure out a model towards profitability.

There seems to be a lot of this happening in the alternative lending space where the lenders backed by hundreds of millions of dollars are not only undercutting the competition at a loss, but they’re running lobbying campaigns that accuse their profitable brethren of being greedy and predatory. The media and general public eat this message up. There is no defense for a lender who has been accused of charging too much by one charging less even if the one charging less will need to declare bankruptcy if it does not raise a fresh round of new capital to sustain operations.

Only the rare observer can read between the lines as Forbes contributor Marc Prosser did. In his own research, he discovered that, “a company which loans money to small businesses at an interest rate of more than 50% was losing money.”

Though I won’t name names, there are a few players out there that believe the answer to their cycle of losses is to push regulatory agencies to attack profitable companies, or at least constrain them through penalties and new laws. Essentially, if it looks like they can’t win the war of attrition, then they might as well stick the government on them.

Speaking of the war of attrition, the race to bring costs to merchants down to zero doesn’t seem to be having the desired effect on the competition. In OnDeck’s Q4 earnings call for example, CEO Noah Breslow said the following:

Overall this market is still characterized by extreme fragmentation. The behavior that we see with our customers is that they might research other competitive options online but then when they actually apply to OnDeck and receive that offer, they kind of have this bird in hand dynamic, and there’s so much search cost associated with going out and looking at other places and so much uncertainty around that, they typically just take that offer that OnDeck has provided to them.

Translation: Once merchants have an offer from somewhere, they go with it. There is no price-competitive marketplace on the macro level.

OnDeck has been undercutting the entire merchant cash advance industry for years. None of their competitors have gone out of business, at least not because of a profit squeeze. Instead, everyone is growing, OnDeck included.

So why lose money?

In the case of OnDeck, they can argue that growth has allowed them to expand into Canada and Australia. They’ve forged partnerships with Prosper and Angie’s List. They’ve acquired more data because they’ve done more deals than most. And who is another billion dollar company likely to partner with in the lending space? Probably the one doing 10x the volume of everyone else, the one whose name is all over the place. They have the advantage to win the partnerships.

Five years from now, when the competition is trying to catch up in volume, all the lucrative partnerships might be snatched up already. Maybe it really is about who can spend the most the fastest. It’s a depressing thought.

Some startup vets will you tell that the most important aspect is actually the team. The CEO of 140 Proof for example has written, “You succeed or fail not on the strength of your idea or your product, but on the strength of your team. Venture capitalists fund teams, not business plans.”

With that in mind, I tried to imagine how that meeting three years ago would’ve turned out had I showed up with OnDeck’s CEO Noah Breslow and Lending Club’s CEO Renaud Laplanche in tow. “We’re going to disrupt lending,” I imagine the three of us tell the fierce startup expert.

The expert knew nothing about me. As far as she knew, I was just some random guy off the street holding a stack of papers with an incredulous plot to dominate the lending industry. I had never worked for a bank. I was young. I had no partner. I didn’t graduate from Harvard or MIT. It probably looked pretty ridiculous. “Duhhh so whaddya think?” I imagined I appeared to her.

With her guard down, she had no reason to hold back from saying what she really felt, that the plan was the absolute dumbest thing she’s ever seen.

Might the dumbest guy in the room only be that because he believed what she said? Or did she have it right all along?

The Industry’s Bad Paper

February 8, 2015 Sometimes deals go bad. But what happens next?

Sometimes deals go bad. But what happens next?

I just finished reading, Bad Paper: Chasing Debt From Wall Street to the Underworld on a recommendation from a friend. In it, author Jake Halpern walks readers through the shadowy world of consumer debt collection. It was eye-opening to say the least.

Halpern’s research uncovered that consumer debts with seemingly no original paperwork is sold, resold, and resold again to companies that the debtor never heard of and would not recognize. A debt’s record amounted to some fields on a spreadsheet where the information is not always correct and might even have been collected already by someone else.

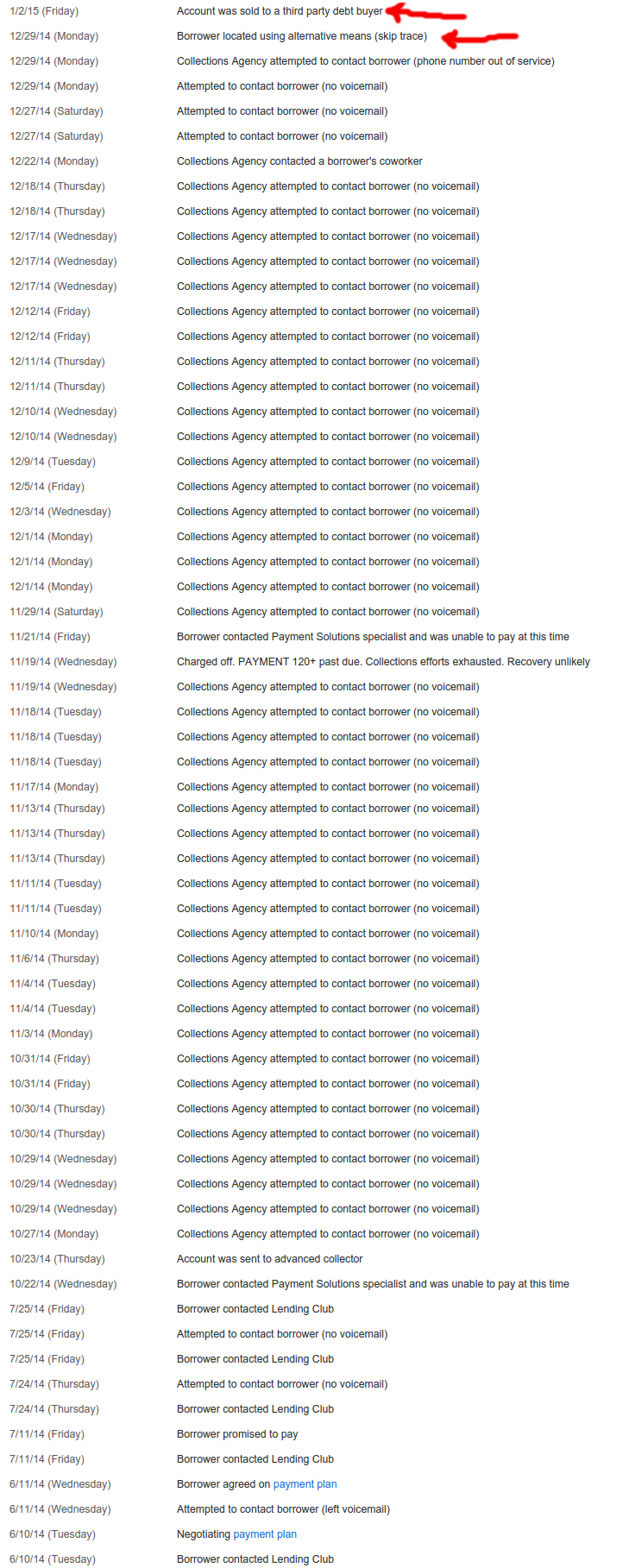

One has to wonder whose hands a Lending Club loan I participated in are in now. It was a $25,000 loan to a nurse. The notes below are from the real collections log provided by Lending Club. After making just 3 full payments on their 3-year loan, this 700 credit borrower went from negotiating a payment plan to off the grid. They called a co-worker, skip traced them, and finally gave up and sold her debt to a third party.

One has to wonder whose hands a Lending Club loan I participated in are in now. It was a $25,000 loan to a nurse. The notes below are from the real collections log provided by Lending Club. After making just 3 full payments on their 3-year loan, this 700 credit borrower went from negotiating a payment plan to off the grid. They called a co-worker, skip traced them, and finally gave up and sold her debt to a third party.

I’ve found that a lot of my defaulted loans thus far have gone bad in the first few months, a pattern that looked more like fraud than borrower hardship. It actually prompted me to call Lending Club and speak to a representative about it, who explained that they’re doing all they can to prevent fraud.

They were pretty relentless on this particular file, a nurse that was making $60,000 a year sounded like a winner. They had virtually no debt but the loan was supposedly used to consolidate outstanding debt into one monthly payment at the rate of 9.67%. The story didn’t exactly add up but since I don’t actually get to talk to the borrowers or look at their paperwork, I’m essentially just playing a numbers game.

That debt has been sold off and I as a note holder do not appear to be entitled to any money on the sale of it, not even pennies on the dollar. Bummer.

Because of platforms like Lending Club, I wasn’t the only one to lose out. 277 other retail investors who I don’t know and have never met participated in it with me. We’re all playing the numbers and we lost on this one.

With 1907 notes acquired on the platform so far, I’m not emotionally invested in any of them. How can I be? I have no idea who the borrowers are. I don’t even know their names! All I can do is diversify and make decisions based off of statistical analysis. If the borrower stops paying, go after them hard whoever they are!

Meanwhile in commercial transaction land

When it comes to merchant cash advance and business lending, the collection rules are different but so are the relationships. Even with strong advancements in automation, phone interviews remain an integral part of the underwriting process. A risk analyst typically calls the business owner, their landlord, and even several of their suppliers. Large dollar amount deals may even be presented to an entire risk committee for approval.

Suffice to say, pesky things like signed contracts do not usually prove elusive when a collector in this world gets their hands on it. Many commercial funding providers even record phone calls with the business owners where they get an additional verbal confirmation to the terms and conditions of the arrangement.

The collections process usually begins with the sales person or sales office that negotiated the terms with the business. Back when was I was an account rep, my commissions were paid in two pieces, upfront and a residual. That meant almost half my pay on a deal was tied to its performance. If a deal started to fall apart or defaulted, I had a personal stake in restoring the business to good standing.

The Fair Debt Collection Practices Act does not cover commercial transactions. And in the case of traditional merchant cash advances, there is likely no debt at all in a default, but rather a possible case of stolen receivables.

In the event where a deal I brokered was suspected of diverting receivables, I’d be the first one to know about it and the first person tasked with fixing it. That meant calls to the business, their home phones, their cell phones, and when necessary their landlord. If none worked, then their suppliers. The first goal was to determine if the business was still operating and in the vast majority of cases where defaults happened, they were.

Hardship was sometimes cited as a reason for breaching the agreement but not always. With a chunk of my paycheck on the line, I had to talk them back into good standing and unlike debt collectors, I didn’t have the ability to renegotiate the terms, lower a payment or cut them slack. It was back to the way it was or nothing.

It escalates

Some returned to good standing and others played hardball. The deal’s original underwriter might then involve themselves and if they failed, then on it went to the internal funder’s portfolio management/collections team.

This is why the situation here on out is different: Imagine a doctor sells you the accounts receivable of all his patients for a discounted price. The doctor gets cash upfront and the buyer will hopefully collect the full value of the accounts receivable to earn a profit.

Now imagine the doctor accepts your cash upfront and then also collects the accounts receivable from the patients and shuts you out. In traditional merchant cash advances, collectors aren’t going after debt, but rather acquired property that is rightfully theirs. The business has shut them out of receivables they purchased.

If internal collection efforts fail, they can attempt to freeze various receivables the business might have. Merchant processing proceeds are usually the first stop. If the business accepts credit cards, the merchant processor can be instructed to freeze all or a percentage of the revenues without a court order. This is easier said than done but it does work and there are even a few third party collection firms that specialize in this.

And if that doesn’t work? Well, thousands of lawsuits have been filed against businesses for breaching these commercial transactions. The business owners themselves can potentially be culpable and liable depending on the agreement and the nature of the breach.

And if that doesn’t work? Well, thousands of lawsuits have been filed against businesses for breaching these commercial transactions. The business owners themselves can potentially be culpable and liable depending on the agreement and the nature of the breach.

Some business owners are shocked to learn that a deal they made over the phone with people they never met will actually track them down and sue them. Unlike consumer debts which might only be a few hundred dollars, commercial transactions are typically tens of thousands or hundreds of thousands of dollars. They will definitely pursue it.

On the largest default I ever presided over as an underwriter, the business owner said something to the effect of, “I stole your money. Let’s see how good you are at getting it back.” He said this just 24 hours after we had wired him the money. Ouch!

That happened more than six years ago but it was something I’ll never forget. A quick Google search today reveals that guy is still alive and kicking as he was recently interviewed about his success in amassing a restaurant empire in Florida.

Over the next couple years, I would hear variations of that “I stole your money” line from other businesses, typically on deals larger than $75,000. These were strategic defaults designed to strong-arm the funding company into a settlement or an attempt to simply walk off with the funds altogether. In other words, fraud.

All this does is raise the cost for the next business that conducts themselves honestly. It’s a damn shame.

Merchants prey on Wall Street

Critics can say what they want about the sophistication of businesses that enter into merchant cash advance transactions. Running a business requires a great deal of intelligence. And to some savvy businessmen, Wall Street’s money is on the menu as fresh meat.

Critics can say what they want about the sophistication of businesses that enter into merchant cash advance transactions. Running a business requires a great deal of intelligence. And to some savvy businessmen, Wall Street’s money is on the menu as fresh meat.

One experience I had was with the owner of a steakhouse in NYC that flew up from his residence in Brazil to try and close me (as the underwriter) on purchasing roughly $400,000 of his future credit card sales. What he didn’t know is that the night before I checked out the place anonymously by having dinner there with my wife. When the bill came, the server told me they no longer accepted credit cards. The next morning, the owner who spoke only in Portuguese arrived in tow with a translator and a lawyer. They traveled directly from JFK to our office, to which I informed them of the decline. They had stopped accepting credit cards a day too early for their scam on us to work and the restaurant closed two months later.

In another case, a souvenir shop in NYC asked if I would come by to pick up his application and statements in person since we were locally-based. After spending a half hour with the guy at his shop, I returned back to the office only to find out that he gave me doctored bank statements.

And then there’s the owner of a florist that made a career off of robbing merchant cash advance companies. The store, which is close to my hometown, had obtained more than 20 merchant cash advances by late 2008 and defaulted on all of them, netting the business close to $1 million. They hoped to make me victim number 21 but we figured it out in the 11th hour before the funds went out. The business is still there today though I’m unsure if it’s still the same owner.

In 2015, fake documentation is an epidemic. Underwriters in the industry cannot rely on faxed or emailed statements alone. They should be verified through APIs or through direct contact with banks. Many funding providers go a step further and actually request the usernames and passwords to business bank accounts just to be absolutely sure that what they’re seeing is what they’re getting.

But as tech-savvy millenials become the face of American small business, the ante is being upped on fraud. One underwriter told me they saw something even more worrisome, a fake bank website.

The scam is this: Knowing the underwriter is going to request the username and password of the business bank account to verify the statements, the applicant has designed a functional replica of a bank website on a web domain they own, one that looks like the bank name. The unsuspecting underwriter logs in to it and verifies the account data. There’s only one problem, it’s all fake.

While this appears to be an isolated event, it just goes to show that the war on bad paper is entering another phase.

Bad paper

While fraud is a substantial cause of the bad paper in the merchant cash advance and business lending industries, hardship does have its place. It is perhaps fortunate that in the commercial space, the paper isn’t sold off into some convoluted world of debt collection. More than likely the business will be dealing with the actual funding provider the entire way through the collections process, not a debt buyer ten levels down the chain. That’s good and bad for them.

It’s good because the owner will able to discuss matters related to the default with the party directly familiar with the original contract.

It’s bad because any chance that the contract and proof of the agreement will somehow get lost in the shuffle is pretty much nil.

Jake Halpern discovered that debtors can win lawsuits by simply challenging the debt buyer to produce evidence the debt is owed. That might work in the consumer world where debt changes hands ten times. On the commercial side, bad paper is an enduring companion. It may be business-to-business but somehow it’s more personal.

Contrast that with the Lending Club nurse who I know only as Member XXXXXXX. His/her debt is in the wind. I have no idea who they are, nor anything about the 277 other people that invested with me.

Halpern spent 256 pages tracing the path of a debt, the companies that bought it, sold it, stole it, and sued for it. It’s amazing how complex it is.

If he were to do a book on bad paper in merchant cash advance, it would go like this:

The business defaulted, the funding provider tried to collect and then sued. The End.

A Bitcoin Moment

February 1, 2015 I had a moment recently. It was late at night and I was ready to hit the hay.

I had a moment recently. It was late at night and I was ready to hit the hay.

“Oh wait, there’s something I need to get out of the way,” I told myself.

I had kept delaying the purchase of a new printer cord to replace the one I mangled. It was time to end that procrastination now! Even though it was 1 AM, I was sure that it would only take a few minutes to place an online order and I summoned the motivation to go for it.

Addicted to Amazon’s 1-Click ordering feature, I was bummed to discover they didn’t have the cord I needed. With no time to waste, I used Google to find a site that did carry it.

Found one.

Add to shopping cart.

Select payment method.

Ugh…

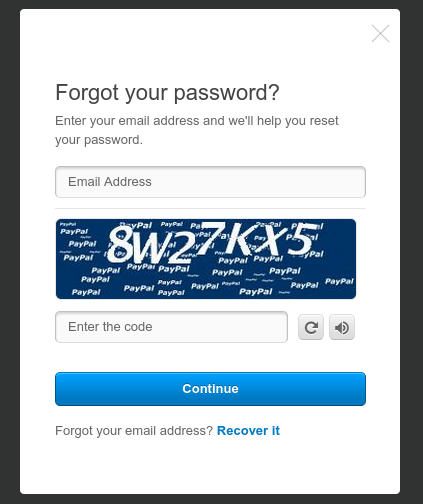

I didn’t have my credit card number memorized and I looked across the unlit room to see if my wallet lay nearby. It was somewhere in a pile on the coffee table, or maybe it was upstairs, or maybe I left it in my pants pocket. Unsure and too tired, I selected PayPal to speed things up, a service I hadn’t used in a while.

Incorrect password.

Incorrect password.

Ugh…

I entered my email address and completed a captcha.

No email…

Refresh email.

Still nothing.

Refresh email again.

Nothing.

Agitated, I started Googling for help about not receiving a PayPal password reset email and instead ended up on a message board where people griped about PayPal in general.

After perusing that forum like a zombie, I got up and walked around. My wallet wasn’t downstairs or at least I couldn’t find it.

Thirty six minutes had gone by since I first encountered the checkout screen. I stopped caring about the cord and I resolved to never print anything ever again.

Before shutting down the computer for the night, I checked my phone. The only news alert I had was about bitcoin. I laughed out loud and went back to the checkout screen. Bitcoin was a payment option. I selected it, copied and pasted the payment address and sent bitcoins stored on my computer to it.

Order placed.

—–

tl;dr

I needed to buy a cord online. Credit card was out of reach. PayPal password was forgotten. Bitcoin saved Gotham.

Confessions of a Bitcoin Miner

December 18, 2014If you’re even vaguely familiar with Bitcoin, you’ve probably heard that you can mine them. It’s one of Bitcoin’s most unfortunate pieces of jargon because it sounds like a scam. We can’t mine U.S. Dollars so there’s no frame of reference for what enthusiasts are talking about. We can mine gold and silver of course, but how the heck can one mine a digital currency? It’s clear there’s more to Bitcoin than just being a form of money and that frightens people. It certainly frightened me.

The first time I imagined bitcoin mining, I pictured sentinels from The Matrix drilling down with unrelenting intensity towards the last human city of Zion. Perhaps the humans were hoarding a vast trove of valuable bitcoins and a war was being waged to achieve digital hegemony. Like Ray in Ghostbusters, I couldn’t help it. The thought just popped in there.

The first time I imagined bitcoin mining, I pictured sentinels from The Matrix drilling down with unrelenting intensity towards the last human city of Zion. Perhaps the humans were hoarding a vast trove of valuable bitcoins and a war was being waged to achieve digital hegemony. Like Ray in Ghostbusters, I couldn’t help it. The thought just popped in there.

The next thought was that I better stay away from Bitcoin. It was easier to take the blue pill where “the [Bitcoin] story ends, you wake up in your bed and believe whatever you want to believe.” That’s what many consumers have done in the past. And who could blame them? I liked my life without Bitcoin in it, so why mess it up?

But the maniac I am, I took the red pill and explored just how the deep the rabbit hole goes.

I mined some bitcoins and the machines didn’t kill me, at least so far. I’m mining them right now as I type this. If you’re getting excited that I’m about to tell you that I’m getting rich while you fools sit on the sidelines, you’re going to be disappointed. There is no actual mining. It’s just slang for facilitating bitcoin transactions over the Internet. Womp womp. If people weren’t sending bitcoins back and forth, then there would be nothing to facilitate and therefore nothing to mine.

To illustrate simply, I’ll start off by reminding you that Bitcoin has no central authority. There is no Visa, no banks, and no Federal Reserve to sign off on a transaction. Instead Bitcoin transactions are validated by computers connected to the Internet running free Bitcoin software.

To illustrate simply, I’ll start off by reminding you that Bitcoin has no central authority. There is no Visa, no banks, and no Federal Reserve to sign off on a transaction. Instead Bitcoin transactions are validated by computers connected to the Internet running free Bitcoin software.

If I have 5 bitcoins and I send 3 to you, computers all over the world running this software are processing algorithms to validate this and make them permanent in a global ledger. The computers make sure you really have those bitcoins to send and then transfers them. You can’t create a fake bitcoin or spend one you’ve already spent because the Bitcoin system will know about it.

On just a single day there are nearly one hundred thousand bitcoin transactions. That’s too much for just a few computers to handle, not to mention that the processing power required to validate them is intense. Validating transactions requires lots of processing power and utilizing processing power has a cost in electricity.

So it pays

The Bitcoin system has a built in reward system to incentivize people around the world to keep the system in order. If your computer achieves a specific milestone while facilitating transactions, you are rewarded with bitcoins. Again, don’t get excited. These milestones are extremely rare to reach and totally random (for the record it’s called solving a block). You could facilitate transactions for 200 years and never get any bitcoins back as a reward.

But while random, it’s a probability game. The faster your processing power, the better your odds of being the lucky computer to receive the reward. That’s a necessary but unfortunate component to Bitcoin because there’s a built-in arbitrage opportunity. Why be a passive facilitator when you could arm your computer with a faster processor and rig the odds in your favor? If your computer was significantly faster than the other ones on the network, you could potentially get rewarded bitcoins often enough and with enough consistency to cover both the cost of your upgraded computer and the electricity to keep it cranked up.

And with that understanding, an international arms race began for increased processing power. Up until early 2013 you could quite easily profit from being a facilitator. Those folks didn’t see themselves as facilitators anymore but as miners. It wasn’t a passive activity. It was a business, like hauling ore out of a silver mine.

Today, so many people have tricked out their processors that it’s nearly impossible to get an edge. In fact, mining often results in losses. I have experienced a net loss in actual U.S. dollars through mining even though I’ve acquired fractions of bitcoins. Net loss? whuh?!

Forget about using your desktop or laptop to mine bitcoins. That’s so 2011. Engineers went on to build special hardware chips much better than household computers that do nothing other than process calculations for bitcoin transactions. Then came small boxes of chips, then large ones…

And when everyone started buying large bitcoin processing boxes, they began to buy two or three of them…

Then a stack of them…

Then a room full…

Then a warehouse full…

And of course a lot of additional money had to be spent on cooling, ventilation, and protecting against fires.

This is where a little problem started. Once everybody was using a million dollars worth of specialized hardware for speed and was spending tens of thousands of dollars per month on electricity, the edge was constantly being neutralized. Worse, the frequency that bitcoins are awarded per day does not increase. There will only be 21 million bitcoins ever placed in circulation. They’re awarded through mining at a fixed frequency. You can try to be the recipient of each reward but the frequency of which they’re awarded doesn’t increase.

Bummer for those that have amassed nuclear arsenal sized mining operations.

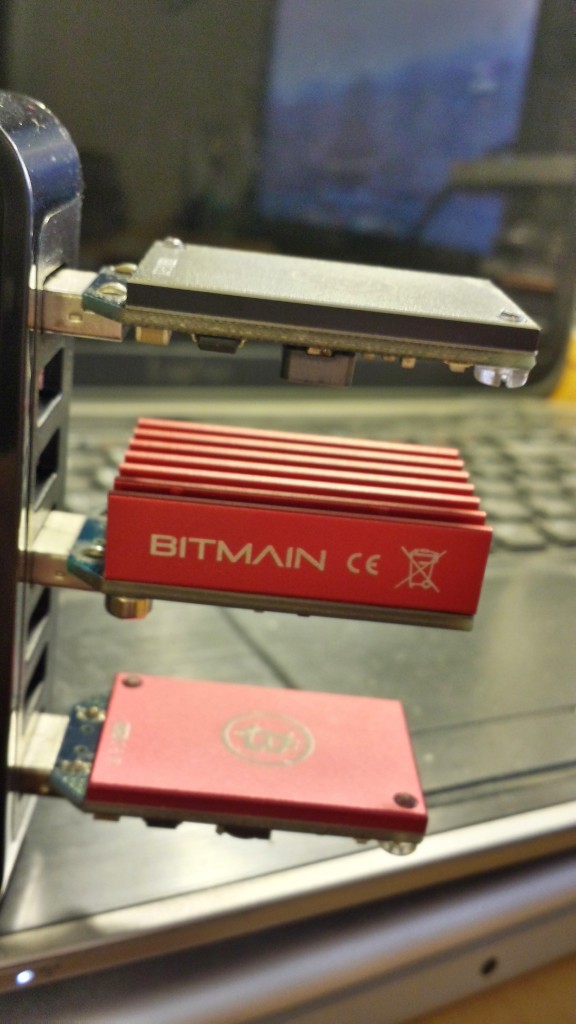

But also bummer for me. This is the extent of my mining equipment.

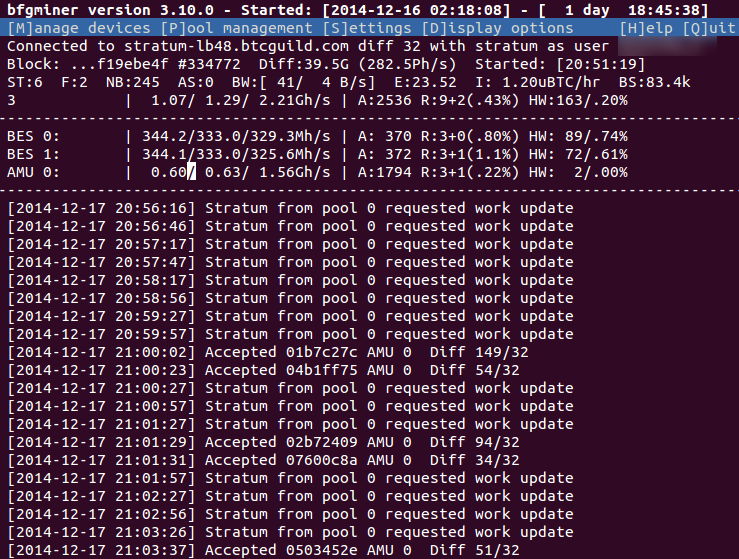

I have three small mining chips all connected via a USB strip. The outer pieces are ASICMiner Block Erupters and between them is a Bitmain Antminer U2. They run 24/7 connected to my home laptop. I can monitor their activity through this little window on my screen:

Combined they are crunching out an average of 2.2 Giga hashes (GH/s) per second, a speed so insignificant compared to the network’s competition that I will probably die without ever receiving a reward of bitcoins.

Unless…

Join forces

There’s a trick to mining to ensure you don’t die rewardless. You can combine your processing power with other miners and leverage your chances. Then if the group’s effort yields a reward, it’ll be distributed on a prorated basis. Someone got this idea a long time ago and in today’s ultra competitive environment, it’s practically a must.

They’re called mining pools. Pools aren’t just a couple of friends, they’re nearly small cities of miners working together collaboratively. The pool I mine in (BTC Guild) has 14,000 to 16,000 users mining together at any one moment and a single user could have an entire warehouse full of mining equipment. In the last hour, the fastest user provided 1,047,666.38 GH/s worth of power to our pool. That’s 476,211x more than what I contributed and he is just 1 of 15,000 users in our pool. woah!

What’s even more wild is that BTC Guild only makes up 5% of the world’s Bitcoin mining power. And yet because I am part of that pool I am paid a prorated amount for every reward the team earns. Surprisingly, that number is not zero. Running 24/7, I am earning an average of 60,000 satoshis a month.

The exchange rate of Bitcoin is extremely volatile but at this moment 60,000 satoshis is equivalent to 19 cents. Yes, 19 cents per month!

And don’t forget that the mining chips cost money to buy and running them 24/7 runs up more than 19 cents worth of electricity used. This means Bitcoin mining isn’t about getting rich. I’m losing money mining. It’s a hobby or benefit conferred upon the digital currency system to keep it running smoothly and accurately. Well at least for me…

Remember that miner that’s out-processing me on a scale of 476,211 to 1? He’s earning about $90,000 per month. I don’t know what his expenses are to run an operation like that but I’m sure it’s not cheap. His biggest enemy is that the value of Bitcoin to the dollar has fallen pretty heavily this year. $90,000 a month in revenue could become $45,000 a month just through exchange rate risk. Those are pretty high stakes to gamble with. But it could also become $180,000!

And whether the big players like that mine or don’t is irrelevant. Whether he makes money or not doesn’t matter. Arbitrage opportunities in the facilitation of transactions is for ultra geeks with big bucks. Mining as a hobby is for regular geeks. It’ll cost some money to do but you get to contribute to a system you believe in.

As for you, the potential average currency user, mining is not really of any consequence. The facilitation of digital transactions already happens with dollars, euros, and pounds. In My Journey to Bitcoin, I explained that buying a cup of coffee with a credit card requires 8 people to get paid for the transaction. Sure the process is completely different for Bitcoin but so what? Bitcoin is unique.

The problem is the mining terminology. It should be called facilitation but that doesn’t sound sexy especially if you are trying to convince an investor to give you $1 million to take advantage of potential arbitrage opportunities on the network.

And that’s about it. The real story behind mining isn’t so scary and you won’t necessarily be at any disadvantage if you still have no idea what the hell mining is. Bitcoin is full of technical nonsense best left to geeks, but you as an actual currency user do not have to worry about a lot of it.

If you’re at all like me though, obsessively curious about how things work and excited to try them out, I’m happy to clue you into the mechanics of mining and even get into the finer details behind it.

An ASIC Block Erupter costs about $10 on Amazon or eBay. I run Ubuntu Linux as my native desktop OS at home (geeky I know) but you should be able to do it with Mac or Windows. The mining software I use is BFG Miner 3.10 and I use BTC Guild as my pool. Admittedly, I am waiting for a delivery of two more Antminer U2s (5x faster than the Erupters but just as cheap) and a delivery of two Antminer U3s (210x faster than the Erupters). I will in all likelihood not achieve a profit even with the additional equipment. And that’s okay, it’s enjoyable just messing with the gizmos.

The best way to learn about Bitcoin is to try it yourself. Hey maybe you’ll hate it, but at least it’ll be based off experience. You can buy fractions of a Bitcoin, even just a few dollars worth from Coinbase. From there you can shop online, convert them back to cash, or send them all to me. 😉

I’m not afraid to say that I mine bitcoins, even if it’s infinitesimally small amounts. What else did you expect from a guy running the AltFinanceDaily website?

I put my bitcoins where my mouth is. If you’re into alternative finance too, it’s finally time you gave in and tried it.

My Satoshi Monday

December 3, 2014Call me brave, batshit crazy, or AltFinanceDaily in the modern era. Earlier this week I wound up at the Bitcoin Center in NYC, a place I didn’t really believe existed. They supposedly host events downtown by Wall Street every Monday and Thursday nights with free alcohol and food.

I don’t believe it, I thought. I called the place ahead of time, twice, half expecting the second attempt to reveal the number was actually out of service. Nevermind the fact that the first time I called, an enthusiastic gentleman was eager to have me stop by.

These bitcoin events start at 7pm. I got there 10 minutes early just to scope the situation out, that way I could escape before anyone knew I was there. Can’t take any chances with these bitcoin people.

But it looked safe. Well, safe enough. The Bitcoin Center is a giant open room on the first floor of 40 Broad Street. The lighting is dark and the floors are pure cement. It could easily double as a handball court or a trading floor, which it kind of is.

And so I kicked off a Satoshi Monday with a crowd that looked like they were doing unix programming in the 1980s. I was glad I dressed casual. We may have been physically near Wall Street but mentally it was light years away. I half expected Richard Stallman, the legendary icon of the free software movement to pop in and start handing out bitcoins, digitally of course, through some kind of cool free software.

And so I kicked off a Satoshi Monday with a crowd that looked like they were doing unix programming in the 1980s. I was glad I dressed casual. We may have been physically near Wall Street but mentally it was light years away. I half expected Richard Stallman, the legendary icon of the free software movement to pop in and start handing out bitcoins, digitally of course, through some kind of cool free software.

I’ve seen mainstream bitcoin enthusiasts at payments conferences around the country, you know, banker types, but the Bitcoin Center keeps it real. Within 15 minutes of my arrival, I had already had conversations that involved taking down the Federal Reserve, the Koch Brothers, and overthrowing the government. I learned that bankers were poisoning nature and that nature was gearing up for revenge. A war was brewing and you didn’t want to be on the wrong side. “You don’t want to f*ck with nature!” someone screamed.

I had no idea what any of it had to do with bitcoin but the crowd wasn’t all like that. Thank God.

Others gave me the inside scoop on Gems, a company that wants to be the “Bitcoin of social networks”. One fellow bought XGEMS early and if I was smart I should try to pick some up too. Maybe another time…

Cryptocurrencies and cryptoassets of all kinds were uttered. Of course each one seemed to be in presale, was only being offered for a low rate today, or was only open to a select few and for a limited amount of time. If you didn’t get in now, it was too late. The more seemingly elusive they were, the more people wanted to buy them, regardless of whatever they were.

Just as I was beginning to question My Journey to Bitcoin, shit got real. “You selling?” a guy asked me. I assumed he meant drugs. But when he saw how paralyzed I had become, he started to laugh. “I’m talking about bitcoin dude,” you have any to sell?

He wouldn’t be the first to ask me that night. In fact there’s a sizable group of folks that attend just to trade bitcoin. There was even an opening bell and an honorary guest bell-ringer guy to kick off trading.

The Bitcoin Center isn’t an exchange though. Any deals made and arranged are between you and another party. Online exchange prices affect the price on the floor but deals made on the floor don’t affect online exchange prices. On Satoshi Mondays, bitcoin goes for cash money.

The Bitcoin Center isn’t an exchange though. Any deals made and arranged are between you and another party. Online exchange prices affect the price on the floor but deals made on the floor don’t affect online exchange prices. On Satoshi Mondays, bitcoin goes for cash money.

I thought it was dumb at first so I asked the next guy that was looking to trade, “Why would I buy bitcoin from random people like you in person when I could just do it online?” I should’ve seen it coming. “Must be easy for people like you who have a bank account,” he responded.

I let that one sink in. Just the day before I had blogged that 25 million Americans are unbanked, meaning they don’t have bank accounts or even access to banking products. This fellow was one of them. He lived off cash but wasn’t letting that stop him from shopping online. He gave you cash, you gave him bitcoins. He stayed unbanked but not cut off from the Internet connected world.

I wanted to ask him why he chose that route over a prepaid debit card, but cards are not a cure-all. Other attendees told me that they buy products overseas and that they were either being charged a huge percentage on top to cover the card processing fees or that merchants had stopped accepting cards altogether. Sure they could make an international wire transfer but even that was a headache for merchants looking to conduct an automated business online.

Bitcoin was said to be simpler for all involved, something I believe because I purchased a new monitor using bitcoins on Overstock.com just last week. It was actually faster and easier than using a credit card. Seriously. I also saved Overstock on the processing fees. See what a good citizen a bitcoin buyer can be?

Bitcoin was said to be simpler for all involved, something I believe because I purchased a new monitor using bitcoins on Overstock.com just last week. It was actually faster and easier than using a credit card. Seriously. I also saved Overstock on the processing fees. See what a good citizen a bitcoin buyer can be?

An in-person bitcoin exchange also prevents the parties from having to pay an online exchange fee, not to mention that you can gain an edge through negotiating. The liquidity of cash on the spot can create some serious arbitrage opportunities.

People threw down thousands of dollars to buy bitcoins which were then transferred via a mobile app. I probably had enough to do some trading but I didn’t need the cash.

When the free pizza arrived, the crowd turned into a mob. The underbanked it seemed were also underfed and a life of living bitcoin to bitcoin meant this might be the only meal they had for some time. I pushed their weaker counterparts, the unbanked, out of the way to get a hot slice and they pushed me right back.

“Bank account lover!” they shouted. It was a harsh indictment, but they knew. As AltFinanceDaily as I was, they knew that ultimately I was banked.

Damn.

Some people left right after they ate. Those that remained began to tell me about their digital mining operations, a necessary component of the Blockchain technology that cryptocurrencies like bitcoin are built off of. Bitcoins don’t just magically appear. Computers on the Internet perform wildly difficult mathematical calculations in order to facilitate the creation and transfer of bitcoins. This design is partially why nobody can beat the Bitcoin system.

One guy told me that he had his basement completely redone so that he could turn it into a mining center. Most mining is done with specialized computer hardware that can perform nothing other than mining. You can actually buy such machines at the Bitcoin Center. If your mining is productive for the system, the system will reward you with bitcoins. The processing power required to solve the complex mathematics makes the odds of being rewarded very low. As time goes on, the system’s equations get more and more difficult to crack.

One guy told me that he had his basement completely redone so that he could turn it into a mining center. Most mining is done with specialized computer hardware that can perform nothing other than mining. You can actually buy such machines at the Bitcoin Center. If your mining is productive for the system, the system will reward you with bitcoins. The processing power required to solve the complex mathematics makes the odds of being rewarded very low. As time goes on, the system’s equations get more and more difficult to crack.

Some miners are backed by billion dollar investment funds and have a serious advantage in the mathematics arms race. But for those that just casually dabbled in mining, they seemed to be getting a little something from doing it, even if it was small.

Some miners are backed by billion dollar investment funds and have a serious advantage in the mathematics arms race. But for those that just casually dabbled in mining, they seemed to be getting a little something from doing it, even if it was small.

Admittedly one guy talked me into buying mining equipment, something miniscule and inexpensive, a novelty almost. It of course packs so little power that its contribution to the Bitcoin system will be insignificant and will likely yield nothing. I didn’t buy it from him though, I bought it on Amazon. Not taking any chances with the bitcoin weirdos.

I used a prepaid debit card to buy an Amazon gift card which I then used to buy a bitcoin mining machine, or something. I swear I’m not crazy. The moment I clicked buy though, something happened to me. My beard got a little more scraggly, the designer label on my pants faded away, all my past presidential votes magically got switched to Ron Paul, and I finally understood that nature was coming to kill us all.

Well, that’s almost what happened.

The Bitcoin Center might bring out the the industry’s worst stereotypes but between the lines, there’s something there. The unbanked, the merchants/consumers dealing with the costly nightmares of credit card processing, and the freeing feeling of operating outside the traditional banking system. I get it.

And they got me because I was one of the last people to leave that night. Before I knew it, Satoshi Monday almost became Satoshi Tuesday. “Party’s over buddy,” said one of the important Bitcoin Center people. I was ready to go. I really was. I had absorbed a lot. But I had just one more question for him.

“You selling?”

—–

Want to just try it out? Buy just $1 worth of bitcoin on Coinbase. You have nothing to lose by learning.

My Journey to Bitcoin

November 30, 2014 Count me amongst the libertarians, anarchists, and digital lunatics. I made an online purchase using bitcoin… and it was insanely easy.

Count me amongst the libertarians, anarchists, and digital lunatics. I made an online purchase using bitcoin… and it was insanely easy.

The first person I shared my experience with was a friend who works in automotive manufacturing, someone who operates outside the world of alternative finance. He thought I was crazy or rather he was more confused than anything. “Wait, bitcoin?” he asked. “I thought that was a scam that went out of business two years ago.”

Stunned by his remarks and disappointed with his lack of excitement for me, I told a few more friends about what I had accomplished. They had all heard the term, but none of them knew what it was. Oddly, most seemed to believe that bitcoin had already been revealed as a con and was something from years past, a scheme that came, got hacked and failed.

Not so long ago I was in their shoes. I received my first education in bitcoin this past fall, September 22, 2014 to be exact at the 3rd Annual Tomorrow’s Transactions NYC Unconference hosted in Google’s New York headquarters.

It’s a con?

Famous money laundering expert and author Jeffrey Robinson gave a blistering assessment of bitcoin the currency, which he described as a hoax perpetuated by “libertarian anarchists.” His contentious indictment was half warning, half sales pitch for his latest book, BitCon, which I bought the day it was released.

Robinson argued that bitcoin adoption, while minuscule, was still greatly exaggerated.

There are fewer card-carrying members of #BitcoinCanada than #Starbucks in #Calgary. BitCon: http://t.co/lQecBgwRdp

— Jeffrey Robinson (@WritingFactory) November 2, 2014

He explores several challenges in his book, one of which can be summed up as:

Why would someone exchange dollars into bitcoin only to have to convert their bitcoin back into dollars?

It’s a great question, but it’s something I’ve done every time I’ve traveled abroad. Dollars to euros and then euros back to dollars. Dollars to pounds, dollars to canadian dollars, etc. But why do an exchange at all when the counterparty prices their goods or services in dollars?

Spend $ to buy #bitcoin to pay for #Blackfriday stuff priced in $. Where's the logic? #BitCon— Jeffrey Robinson (@WritingFactory) November 29, 2014 http://t.co/U26d35G0u9

Benefits

Assuming bitcoin’s value against the dollar wasn’t volatile, I can think of three immediate reasons:

1. I don’t have to enter in my credit card number on a website and risk it being hacked or stolen.

2. I can make a payment online if I don’t have a credit card or debit card.

3. I can spare the merchant the payment processing fees.

Let’s forget about point one for now because it’s easy to overlook the pervasiveness of point two. According to the FDIC’s latest National Survey of Unbanked and Underbanked, 25 million people in the country do not have access to a bank or banking products at all. Poverty is a main driver of that but curiously 34.2% of respondents in that group cited that they don’t like dealing with banks or don’t trust them as a reason. 30.8% said that account fees were too high or too unpredictable.

And that’s just the unbanked. 1 out every 5 households in the country is underbanked. They have a bank account but have also obtained financial services and products from non-bank alternative financial services providers in the prior 12 months.

To those of us that rely on banks for everything this may seem extreme, perhaps even downright unbelievable. Coincidentally, Robinson wasn’t the only notable figure at the New York Unconference. He was joined by Lisa Servon who later spoke about her hands-on experience with the unbanked and underbanked. A professor of urban policy at the New School in New York, Servon got a job as a check casher/payday lender in a storefront on a busy corner in downtown Berkeley, California to learn about these households on the front lines.

Consumers can be intimidated by banks she said at the Unconference, especially minorities. Even people who can afford to use banks opt not to. A sample of her experience was published a month ago in the New York Times.

Moving on to point three, accepting bitcoin can either be free or vastly less expensive than accepting a credit card payment. Payment processing fees are significant in commerce. I know this because I accept credit card payments through both Square and PayPal in another business I run and it costs me nearly 3% per transaction. I’ve also sold merchant processing for years and have priced hundreds if not thousands of accounts.

You know that thing American Express invented called Small Business Saturday where consumers are encouraged to spend money at small businesses? Paying with your AMEX card is encouraged of course and AMEX charges about 3.5% to the merchants on every sale.

By going dollars->bitcoin->dollars, you can do even more to help small business by saving them the fee. Granted, most consumers probably wouldn’t jump through any hoops to save a business money especially if it meant trying to figure out how to convert your dollars into something they perceive as “a scam that went out of business two years ago.”

I’ve read all the warnings about bitcoin already and have even been lectured by Robinson personally:

@financeguy74 A fool and his money… the numbers don’t lie. Enjoy Vegas.

— Jeffrey Robinson (@WritingFactory) November 4, 2014

and yet what intrigued me most about bitcoin aside from the transaction costs, was the fact that it was not run by a government.

What if?

Five years ago I had a sinking feeling. The safety and security of the U.S. economy was put to the test. Stock prices fell, lending dried up and millions of Americans actually began to ask themselves, what if? As in what if the dollar collapses? What if your bank account suddenly became worthless? What if you had to suffer for the mistakes others in your country made?

In 2009, a colleague and I pledged to stick together should an eventual economic apocalypse happen. Our plan was simple:

1. Exchange all our money for a gigantic gold brick and two shotguns

2. Sit on gold brick and guard it with those shotguns

Survival would remain possible by chiseling off pieces of the gold brick and exchanging them for food and water. We’d each take turns sleeping and hopefully survive until things returned to normal, if ever.

A fantasy to be sure, and it was great for laughs to break up the day, but what if?

My apocalyptic paranoia is one of many stereotypes of the bitcoin faithful, but I have no interest in exchanging 100% of my dollars to bitcoins. And no, I don’t think the dollar is going to collapse tomorrow. I am intrigued however by a currency that eludes governmental control. We can all keep a gold brick in our back pockets, even if it’s small, and even if it’s digital. If for no other reason, it’s a small hedge for peace of mind.

It’s quite ironic that while critics talk up the dollar’s superiority and the strength of the U.S. government, only 14% of Americans approve of how Congress is handling its job. Not to mention that the nation is at this very moment $18 trillion in debt, a number very unlikely to be made whole. Remove the term bitcoin from the conversation and it’s quite likely the average person would at least be amenable to the possibility of a non-governmental currency.

Perhaps as Americans we are somewhat blind to risks, that we feel nothing catastrophic could possibly to happen to us. To many it is literally unthinkable. A completely independent currency has its merits both now and in far bleaker times.

Of course should the apocalypse occur and all you have is bitcoin, rest assured you will be able to buy a shotgun since you can pay for them with bitcoin:

The get rich quick crowd

Here lies another criticism of bitcoin, that everyone is holding it and no one is spending it. Far from idle, there are currently more than 80,000 bitcoin transactions per day. Without prohibitive transaction fees though, volume is a poor measure of adoption since I could easily send bitcoins back and forth between accounts I own and classify them as transactions.

There are indeed those holding and not spending. Rampant speculation is both a cause of volatility and an argument for its long term unsustainability. Speculators are hoping the digital currency will appreciate and make them filthy rich. If that day never comes, a big sell off will cause its value to drop.

And therein lies the argument… when or if the speculators leave, will that spell the end of bitcoin?

If bitcoin had no practical uses outside of being another digital currency like World of Warcraft gold, then bitcoin would likely be a con, a predictable one that probably would’ve combusted already.

There may actually be a massive market correction in the future. At the current moment, Coinbase reports that 1 btc = $376.23. On November 14th, I paid $397 for 1 btc. It lost about 5% of its value in two weeks, a tough percentage to stomach for the faint of heart, and most certainly the average consumer. It’s also equal to the plunge the S&P 500 took between October 8th and October 16th so such short term volatility exists in other mainstream assets.

I’m not necessarily speculating though. I spent almost half my bitcoins shopping on Overstock on Black Friday, an experience I will detail in another post. A 5% swing might be acceptable for an investment but it’s quite ugly for a currency and this fuels the misinformation that bitcoin is a scam, con, or has already gone out of business two years ago.

1 btc could drop to $100 or $10 after a furious market shakeout and it wouldn’t change how I felt about it. It could also rise back up to $1,000 or higher. That volatility is enticing, almost sexy, but it’s the lack of transaction fees and governance by mathematics rather than actual governments that have me hooked

White knight

Still, bitcoin is waiting for a few white knights, merchants willing to price their goods and services in bitcoin. For years, I have priced advertisements on this website in dollars, but to show my support, I will soon be pricing them in bitcoin going forward. Dollars will still be accepted of course, but those Paypal fees hurt. Paypal costs me 3% in a split second. Is a 5% loss in bitcoin value over two weeks really that wild by comparison?

Still, bitcoin is waiting for a few white knights, merchants willing to price their goods and services in bitcoin. For years, I have priced advertisements on this website in dollars, but to show my support, I will soon be pricing them in bitcoin going forward. Dollars will still be accepted of course, but those Paypal fees hurt. Paypal costs me 3% in a split second. Is a 5% loss in bitcoin value over two weeks really that wild by comparison?

I think not.

Bitcoin is more than a currency. It’s not the euro, the yen, or the peso. It’s a detachment from governments and banking. It’s self-control. Without the private key, your bitcoins can’t be seized.

We live in a world today where everybody has their hand in your money. Just look at what happens when you pay for a cup of coffee using your credit card. The following parties all get paid a percentage:

- The small business owner

- The small business owner’s merchant account representative

- The merchant account representative’s company (the ISO)

- The payment processor (the processor settling the transaction)

- The acquiring bank (the payment processor’s bank that is authorized to use the payment networks)

- The payment networks (Visa, mastercard, etc.)

- The customer’s card issuing bank (The bank that issued the card to the customer gets a percentage of every sale made with that card)

- The state (where there is sales tax)

If you thought bitcoin was insane, what do you call a system where eight parties need to get paid to facilitate the sale of a cup of coffee? And my example was simple. There are typically more parties involved that that.

I don’t want to give the impression that you can evade taxes with bitcoin. I have every intention to stay on the up and up with governments. But remove the tax man and the merchant from the equation, and one has to wonder what the heck is going on with the other six parties, all of whom will ultimately decide if your transaction is acceptable to them. They decide, not you. They can freeze your funds if they don’t like the transaction and they do. It happens to merchants all the time.

Your money is not really yours. You have rights to it, but only to an extent. It can be garnished, frozen or confiscated. That’s the price of liquidity and relative stability. If you can afford to color outside the lines, where you can remove the six bankers and their control, why not experiment? There’s something pure about it, liberating. And when you add in the fact that it’s governed by math, it’s more than that, it’s beautiful.

deBank

If you are under the impression that bitcoin is intimidating, a scam or out of business, well then I encourage you to step out of governments for a minute, to deBank, and take a walk on the digital side. I’m not going to convert all my dollars to bitcoin and you shouldn’t either. Try it out with some extra cash.

If you are under the impression that bitcoin is intimidating, a scam or out of business, well then I encourage you to step out of governments for a minute, to deBank, and take a walk on the digital side. I’m not going to convert all my dollars to bitcoin and you shouldn’t either. Try it out with some extra cash.

Sure, you’ll be in company with libertarians, anarchists, and lunatics. And yes, there’s the paranoid, the speculators, and those transacting in illicit goods and services. The beginning of the Internet and computers was much the same way with the unix and linux faithful.

Perhaps bitcoin needs a Steve Jobs, a Bill Gates, to package up something simple and suitable for the average household. Every American would appreciate squirreling away a little something that is out of reach of government and banks.

The vast majority of Americans already don’t trust congress, and 92 million Americans are already underbanked or unbanked. In 2014 buying a cup of coffee involves paying eight people and the government has spent $18 trillion that it doesn’t have. You have to start to wonder who the real lunatics are. Consumers are waiting for something… even if it’s just a little peace of mind, a hedge, a gold brick in their back pocket, the feeling of independence, freedom, control. Something…

I AltFinanceDaily and loved it. Now it’s your turn.