The Fork in the Merchant Cash Advance Road

August 23, 2011Originally Posted on April 25, 2011 at 10:48 PM

The Merchant Cash Advance (MCA) industry is growing, albeit slower than some may have you believe. But it’s moving in two opposing directions, a condition that’s making it tougher to describe the financial product itself in general terms. MCAs are becoming more expensive and a lot cheaper at the same time. HUH? You read that right.

Originally aimed at business owners with poor credit, the risk of default or delinquency was overcome by withholding a percentage of sales revenue directly. As the credit crisis and Great Recession took hold, it attracted businesses of all credit backgrounds and today it’s widely accepted as a lending alternative, rather than a solution to poor credit.

As MCAs pushed forward to compete for customers normally accustomed to bank credit lines, the cost was stiffly resisted. These businesses had a tough time envisioning their financing terms to be anything outside of some percentage over the Prime Rate. Since a MCA is supposed to be structured as a sale, there is no APR equivalent, no timeframe, no amortization, nor any real familiarities of a loan. As the past couple years have passed, the product is more publicly understood, but for it to actually catch on, the costs had to come down. Many funding providers now refer to such high credit, low cost accounts as premium, platinum, preferred, gold, etc.

While the margins earned on high credit accounts shrank, funding providers were dealing with another challenge simultaneously, defaults. Whether the business owner intentionally interfered with their credit card processing or the store went out of business altogether, bad debt in the MCA world was mounting…FAST!

No matter which company ran the figures or how secret these portfolio statistics were, every funding provider came to the same realization. The lower the credit score of the business owner, the greater the chance of a problem. Why this came as any surprise, is a surprise in that of itself. The Fair Isaac Corporation (FICO) will have you know that any individual with a score below 499 has an 87 percent chance of being delinquent on a credit payment within the next 2 years. Delinquent, is defined as a payment of 90 days or more past due.

But wait… if a MCA is not a loan, nor does it depend on the business owner to make payments, then how can there be a risk of delinquency? Intentional manipulation of the revenue flow back to the funding provider can be relatively easy to do. A business owner could use spare POS equipment to accept card payments for which the funding provider is not aware of and therefore prevent the collection of funds. That’s a method known as splitting, and serious consequences can result when discovered. (Read more on what happens in the case of default or deliquency on a MCA in a previous article)

But outside the scope of malice, there’s the traditional reason, the inability to make payments. If the suppliers and wholesales aren’t being paid, then the business isn’t going to have inventory on hand to sell. If the rent isn’t being paid, then there’s not going to be any location to generate these sales. Essentially, the funding provider has a mutual interest in the business being able to satisfy ALL of their obligations, not just the MCA itself.

If there is an 87% chance that suppliers, landlords, or other essential creditors will not be paid on time in the next 2 years, then there’s an excellent probability that the business will be unable to operate at the same level. With no collateral as protection, the MCA industry has adapted to the challenge by raising the cost. Business owners with poor credit can expect funds to be expensive and the terms to be more restrictive. Lower funding amounts, higher withholding percentages, and the sacrifice of any negotiation is the price the MCA industry has set to make funding to the maximum risk group possible. These programs, which are now often referred to as starter advances, don’t work for everyone so the pros and cons should be weighed prior to executing a contract.

Both the premium advances and starter advances have experienced extraordinary growth to the point where they have become niches of their own. There are now starter advance companies and premium advance companies. Funding providers like Strategic Funding Source have taken the product a step further and reportedly did a MCA for an exhibit at the Tropicana Hotel in Las Vegas for $4 Million. Contrast that with deals that are struck for as little as $750. And we can’t fail to mention that some have taken it back to the basics, a loan. ForwardLine in Woodland Hills, CA lends money to businesses which are then repaid in accordance with a predetermined, fixed pace through the card sales. They have reintroduced concepts like APR back to the finance world.

If we continue at the current pace, MCAs will become less expensive, more costly, a lot bigger, and markedly smaller. We’ve come to the fork in the road for what the Merchant Cash Advance industry seeks to brand itself as. Loan alternative? First choice? Backup plan? Is it for smaller businesses or larger ones? Should it go the way of lending or continue to remain a structured purchase of future card sales? Is industry cohesion really necessary or will increased decentralization lead to greater acceptance of this financial product a whole? Will there come a time when America’s big banks swallow the industry up, buy out the existing portfolios, and add this product to their financing arsenals?

These are tough questions. Merchant Cash Advance is evolving, growing, and no longer moving in one direction. While we contemplate our next step, one thing is for certain, there’s no turning back.

– AltFinanceDaily

www.merchantprocessingresource.com

Our Favorite Merchant Cash Advance Commercials

August 23, 2011Posted on May 7, 2011 at 1:23 AM

TV has never been a popular venue for Merchant Cash Advance (MCA) providers to advertise. There is a highly specific target market, small business owners that accept credit cards as a form of payment that are looking for funding, that simply reduces the cost effectiveness of mass media. Why pay to reach 100 people when 97 of them may not even fit basic criteria such as owning a business? It doesn’t make sense.

TV has never been a popular venue for Merchant Cash Advance (MCA) providers to advertise. There is a highly specific target market, small business owners that accept credit cards as a form of payment that are looking for funding, that simply reduces the cost effectiveness of mass media. Why pay to reach 100 people when 97 of them may not even fit basic criteria such as owning a business? It doesn’t make sense.

That doesn’t mean that TV or online video commercials for MCA don’t exist, they do. Unfortunately most of them tend to be poorly self-produced webcam miniclips that are so boring, they are more likely to turn someone away from the product, than to help anyone. No offense. But there are some providers that actually took the time, effort, and money to create something worth watching. Here are some of our favorites:

Does anyone else have one they’d like to share? We’ll be happy to show it off!

– The Merchant Cash Advance Resource

Bank Loan Advertisements are nothing but a bait and switch

August 23, 2011

We stay in touch with many people in the financial industry, and not just Merchant Cash Advance. Back in late March we learned that lending was so tight, that credit cards were barely attainable. That was when the unemployment rate was 8.8% and as of May 2011, it’s back up to 9.1%. That was when the economy was expected to grow by 2.9% in 2011 but is now on pace for 2.7%. The point? If it was impossible to get a loan back in March, then how much worse could it get?

We stay in touch with many people in the financial industry, and not just Merchant Cash Advance. Back in late March we learned that lending was so tight, that credit cards were barely attainable. That was when the unemployment rate was 8.8% and as of May 2011, it’s back up to 9.1%. That was when the economy was expected to grow by 2.9% in 2011 but is now on pace for 2.7%. The point? If it was impossible to get a loan back in March, then how much worse could it get?

An insider shares it can get worse, much worse. Our friend Tim (name changed) is the manager of the small business lending unit of a major national bank. Any loan less than $1 Million dollars is considered to be for small business. Tim’s unit is on track to do more loans this year than last year and none of them are going to retail stores or restaurants. Did we hear that right?

“Retail stores and restaurants are too flakey to give money to.” That wasn’t just his opinion either because that’s actually part of the bank’s underwriting policy. They are completely prohibited from lending to those business types. So we had to ask…

What if they had 25 years in business? Declined.

What if the guarantors had 800 credit? Declined.

What if they had $5 Million in cash reserves in the bank? Declined.

What if…? Declined. Declined. Declined.

There is no criteria that would make them eligible, period. Tim admits that the interest charged on a loan is not profitable by itself anyway so to take any degree of default risk even if it’s small, is not worth it. Instead, they rely on their loan clients to open a business checking account with them, use their merchant processing, and sign up for other services on which they can charge fees and earn income. Their unit has an average turnover time of 3 months from the time the application is submitted to the time the loan is funded.

“We usually get a jump on setting them up with all our services right when they apply for the loan, so we can start earning on them right away,” Tim said. We wondered why they wouldn’t let restaurants and retail stores apply then. “Oh we let them apply for loans… we just don’t tell them they’re declined until after we’ve locked them into other fee generating services. They’re unlikely to pack up and change banks after that so it works out for us.”

There’s a term for this tactic and it’s called a ‘bait and switch.’ There really seem to be no loans for the businesses that need them, an assertion bolstered by the Small Business Administration’s 2011 1st Quarter report. Lending to small businesses has fallen by $15 Billion.

So where’s the money?

There are still alternative sources available, but we’ve yet to find anything that rivals the speed and flexibility of a Merchant Cash Advance (MCA). Too many small businesses hold out the hope that a bank will help them and pass up the opportunity to obtain alternative financing like a MCA. But how many missed opportunities will it take until it’s too late? How many businesses will sign up for checking accounts and expensive merchant processing, only to find out that no loan is coming and all they’ve acquired is an expensive long term contract for no value in exchange.

If you’re a restaurant or retail store, you can research our directory of verified funding providers HERE. Don’t wait for the bank to approve a loan they’re not allowed to approve and instead get what’s most important, the capital to grow.

– The Merchant Cash Advance Resource

The Merchant Cash Advance “Don’ts”

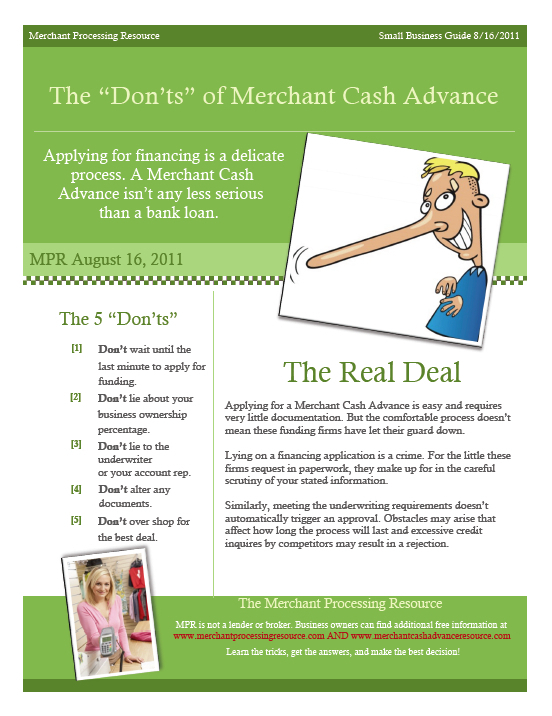

August 22, 2011In sales training, young men and women are taught to negotiate with positive language to close a deal. For example: “We can’t meet the deadline” is replaced with “We can achieve the objective, but we may need to extend the deadline.” Or “We don’t offer that service” is transformed into “We offer many services that can add value to your business but that particular one is a challenge.”We apply a bit of that psychology when developing resources for business owners. People are a lot more open to input when you cast out the negativity. So it’s a bit ironic then that we created a printable reference form, titled The Merchant Cash Advance “Don’ts”. Though it may be perceived as a little condescending, this little banker/business pep talk can protect you from making a major mistake that could cost your business money. So keep it handy even if you don’t plan on applying in the near future.

1. Don’t wait until the last minute to apply for funding.If a firm is advertising funding in 3-5 days, don’t put yourself in a position where you MUST have the funds in 5 days or less. The underwriting process may take longer than you anticipate. The advertised timeframes generally describe a perfect situation. For example: If all documents are received by day 1, all references checked out by day 2, you could potentially receive funds by day 3 assuming the technical setup is already completed. There are situations where business owners have spent 10 days waiting to obtain a copy of their lease from their landlord, which piggybacks onto the 3-5 days. Additionally, supplemental paperwork may be asked for, a trade reference might be unreachable, or your method of card acceptance might require more time to integrate. Anything can happen so don’t wait until the last minute!

2. Don’t lie about your business ownership percentage.This might be seem like silly advice but underwriters report that it’s a growing trend. People with low credit scores tend to assume that they will be declined for their score alone. Therefore they may feel inclined to state that a partner, friend, or family member with excellent credit is the owner of their business and not them. This is bad for several reasons:

- Credit score isn’t the sole determining factor for a Merchant Cash Advance. So why lie?

- Misrepresentation of ownership will be discovered and the application declined.

- Misrepresentation to obtain financing constitutes fraud and is a crime.

3. Don’t lie to the underwriter or your account rep.The liar loans of the mortgage boom ultimately led to the financial crisis and lending shortage. That means the days of declaring whatever you want to obtain the deal you want, are gone. If you state that you generate $100,000 in sales per month, be prepared to show documentation that backs up that claim. Your sales agent or account rep is probably compensated if you close on financing. That doesn’t mean they will help you get there at all cost. They are bound by a certain code of ethics and all applicable laws. If they become aware of any misrepresentation or intended misrepresentation, don’t expect them to be an accomplice to your dishonorable act. If you put them at risk, they will inform the underwriter and terminate your application.

4. Don’t alter any documents.Changing the expiration date on a lease, editing out the embarrassing withdrawals from the bank statements, or any other more or less blatant alteration will result in a rejection. Merchant Cash Advance underwriters are extremely adept in detecting alterations and fraud. Altering documents in an attempt to secure financing is a crime. You are well advised not to try this, no matter how harmless you may perceive the alteration to be.

5. Don’t over shop for a deal.You are entitled to obtain quotes from multiple sources, but don’t press your luck. Too many credit inquiries can spook an underwriter. For one, it tends to drive down the margins that will be earned because competition, thus making the deal less profitable for them and less attractive to put on the books. On the other hand, they may suspect that the other firms declined you and therefore they are being picked as a last resort. When underwriters start to feel this way, your approval may be retracted and it can be a tough battle to convince them to change it back.

We promise next time to provide a guide full of “Do’s”! But for now, we’re making it a point that Merchant Cash Advance is a serious business. The process may be fast and easy, but don’t get too comfortable and make claims you can’t back up. That will lead nowhere good…

– The Merchant Cash Advance Resource

http://www.merchantcashadvanceresource.com

Deja vu? Merchant Cash Advance in Wall Street Journal

August 10, 2011 Have you ever had a deja vu moment where you feel like something has happened already even though it hasn’t? And then all of the sudden it happens? Yeah, we just got a little of that. Or maybe we’re just psychic.

Have you ever had a deja vu moment where you feel like something has happened already even though it hasn’t? And then all of the sudden it happens? Yeah, we just got a little of that. Or maybe we’re just psychic.

It was just a couple months ago that we published a scathing editorial on the failure of the Merchant Cash Advance (MCA) industry to reach mainstream acceptance. (See: The Colossal Marketing Failure of the Merchant Cash Advance Product – June 28th, 2011). Most of our readers acknowledged the shortcomings but were at a loss for suggestions to overcome them. ISO&Agent Magazine quickly added their two cents by claiming that MCA was waiting for its big moment (See: Cash Advances: Negotiating a Maturing Market – July 26th, 2011) but completely missed the mark when they identified cost as the obstacle holding it back. It’s not cost, it’s communication.

How often is MCA cited in mainstream news publications? Wall Street Journal? New York Times?

-direct quote from our piece on June 28th

Today we can say that Merchant Cash Advance got its mention in the Wall Street Journal. :::Applause::: Though it’s only in their blog section, most people today get their news online anyway. The article features AdvanceMe, the largest and oldest player of the bunch. So how does the glorification of one company carry over to the industry as a whole? There were a bunch of good messages in there that describe the product itself: The article title implies it’s becoming more popular: “Cash-Advance Demand Rising” A description of how it works: “Merchant cash advances, which first appeared about a decade ago, provide capital in exchange for a share of future debit or credit-card sales. As such, they tend to be used by retailers, restaurants and other small businesses where a large number of customers pay with cards.”The common uses for it: “Business owners use the cash to buy new equipment, restock inventory or pay off debt” Yes, Yes, and Yes. Good for AdvanceMe and good for the MCA industry but this is only the beginning.

Every business owner should be aware of MCA, not just the ones that read the Journal today. It is Un-American (Yeah, that’s right) to withhold information from business owners that may enable them to capitalize on opportunities. With no bank loans available, most projects in this country are on hold. It’s simply not fair. We badly want to take the credit for today’s Journal mention, especially since we delivered our two previous articles on this topic to their editors in July. But the real hero here is AdvanceMe. Their press release the day before clearly caught the attention of the mainstream media. Great job guys. And we’d be remiss if we didn’t point out they forecasted an increase in funding by $1 billion in the next 2 years. That’s about equal to the industry’s entire volume combined. Is Merchant Cash Advance about to hit its growth spurt? AdvanceMe seems to think so. If they’re about to have their ‘moment‘, they’ll likely pull everyone else along with them.

– AltFinanceDaily

../../

Merchant Cash Advance Applicant Fraud on the Rise

July 24, 2011

Fraudulent Applications are becoming more commonplace in the Merchant Cash Advance industry. Scott Griest, the CEO of American Finance Solutions had this to say about it:

- Hard fraud is when outright crooks are submitting applications for businesses that do not exist, have stolen a business’ identity or a desperate actual owner has altered his financial documents to qualify for more favourable terms.

- Soft fraud is when a legitimate business has submitted actual documentation, but is still not being truthful about his or her business.

- All funding companies should become members of NAMAA.

- In AFS’s first month of membership they detected more than $20,000 in submitted fraud deals.

Bad debt has dropped by 50% over the past 12 months due to fraud detection.

– The Merchant Cash Advance Resource

Merchant Hash Advance

July 16, 2011

Short on capital? Your business may benefit from a Merchant ‘Hash’ Advance. Restaurants, retail stores, and auto repair shops can easily obtain funding, but medical marijuana dispensaries need love too.

A few cannabis related deals have floated around the Merchant Cash Advance (MCA) industry before, but rarely do they close. At best they elicit a few chuckles from underwriters, who will likely make a few juvenile jokes before turning down a viable, serious, and legal business. The store owners walk away frustrated but neither side is to blame.

In states like New York, where many MCA powerhouses reside, marijuana of any kind is illegal. That makes the sale of it for medicinal purposes in states where it’s legal a foreign concept. We spoke to an underwriter of one Long Island, NY based MCA firm who shared this: “I’ve eaten dinner at a restaurant and I’ve bought flowers from a florist. I understand what makes both businesses tick. I’ve never been to, nor met anyone who has been to a medical marijuana dispensary. I don’t really know what the transaction is like, what risks they face, what their profit margins should be. It’s a big unknown. Is it easy for a dispensary to lose their license and suddenly go out of business? Are there laws that prohibit outside financing? Do we need to keep tabs on where they obtained their inventory from? We typically call a restaurant’s vendors prior to funding to ensure they’re in good standing. I would feel a little weird calling up a weed farm for a reference.”

And he’s not the only one that feels that way. Banks do too. Funding aside, evidence shows cannabis related businesses stuggle to fulfill basic needs such as opening a bank account or accepting credit cards. According to a report by creditcards.com, it’s not uncommon for their checking accounts to be closed without warning, sending the business scrambling for help elsewhere.

But the situation isn’t all grim. We interviewed Nick Emerson, the Managing Director of 420 Card Processing in Campbell, CA (420 CP), a firm that’s changing it all. 420 CP not only provides card acceptance services to medical marijuana dispensaries but can also connect them with access to capital.

Using the concept of MCA, 420 CP and their funding partner will provide actual loans based on credit/debit card processing volume It’s a joint partnership. (Sorry couldn’t resist!). And there’s great news. The typical easy criteria that made traditional MCAs so popular still applies. So long as the license to sell medical marijuana can be proven, dispensary owners have the same odds of being approved as a restaurant would.

So the oportunity is there and the target market is bigger than most people think. According to Nick, “Medical marijuana is legal in sixteen states and DC to the best of our knowledge. Those states are: AK, AR, CA, CO, DC, DE, HI, ME, MI, MT, NV, NJ (still pending), NM, OR, RI, VT and WA. Some of these states are in the throes of evaluating how to implement the ballot measures that were passed and they do not all enjoy the same structures.” But once the ground rules are in place, it’s business as usual. “We have faced no problems as our company is dedicated to providing credit card processing services solely to the medical marijuana industry. As you can imagine, our clients love us.”

Add that to the ever growing list that the Mechant Cash Advance concept is being applied to.

- Damaged Credit? Funded!

- Short Time in Business? Funded!

- Restaurants? Funded!

- Retail Stores? Funded!

- Auto Shops? Funded!

- Las Vegas Casinos? Funded!

- E-Bay Stores? Funded!

- Medical Marijuana Dispensaries? Funded!

Short on capital? If you accept electronic payments, someone somewhere is willing to provide cash against those future sales. No matter what you do…

– The Merchant Hash Advance Resource

###

About 420 Card Processing

420 Card Processing was founded by card processing professionals, with decades of combined experience, who are committed to equal access and opportunity for those involved in all aspects of providing medical marijuana to patients in states that have legalized its use. 420 Card Processing provides services to retailers, wholesalers, suppliers of gardening equipment, and physicians. 420 Card Processing is a member of Americans for Safe Access, California NORML and the National Cannabis Industry Association.

For more information on obtaining a merchant account or funding from 420 Card Processing, contact Nick Emerson:

Sales@420cardprocessing.com

(800) 579-1675900 E. Hamilton Ave.

Suite 100

Campbell, CA 95008