Alternative Lenders Spread Their Wings Internationally

June 20, 2017 As alternative lending gains global traction, a growing number of U.S-based alternative lenders are exploring international growth, with large companies like OnDeck, Kabbage and SoFi leading the way.

As alternative lending gains global traction, a growing number of U.S-based alternative lenders are exploring international growth, with large companies like OnDeck, Kabbage and SoFi leading the way.

Some alternative lenders have begun their expedition closer to home by extending their reach into Canada. Others are traveling farther beyond to parts of Europe and Australia, for example, while others are eying eventual growth in Asia.

Propelling the opportunity is the fact that a number of international banks are still unprepared to offer online lending on their own and thus are more amenable to partnerships with U.S.-based alternative lenders, according to Rashmi Singh, senior manager in the wealth management practice at EY.

It also helps that the options for local partners are somewhat limited. “There are not a lot of digital lenders [outside the U.S.] at the same level as some of the folks here,” Singh says.

To be sure, international expansion requires extensive time, money and regulatory know-how, and some U.S. alternative lenders may never reach the critical scale to be able to compete effectively. Nonetheless, as globalization proliferates, industry observers expect that additional forward-thinking companies will push beyond the limits of their current geographical borders.

“The question is not if, but when (and where) U.S. fintech companies will expand internationally,” contends Ryan Metcalf, chief of staff and director of international markets at Affirm, a San Francisco-based fintech that has partnered with Cross River Bank of Fort Lee, New Jersey, to allow shoppers pay for purchases over time with simple-interest loans.

Affirm—which works with more than 900 retailers and recently announced that it had processed its 1 millionth consumer installment loan—has focused on domestic growth so far, but the company is now considering a number of options for international expansion, Metcalf says.

SIZING UP THE MARKET

Certainly, there are numerous opportunities for homegrown lenders to expand internationally given the healthy growth alternative lending is experiencing in other parts of the world. Each market, of course, has its nuances and individual growth patterns.

Europe, for instance, has seen substantial growth over the past few years, with the U.K. leading the way in alternative finance. It has four times higher volumes in aggregate than the rest of Continental Europe, according to a 2016 report from KPMG and TWINO, one of the largest marketplace lending platforms in Europe. (P2P consumer lending is the largest component of alternative online lending in Europe, capturing 72 percent of the total in the first through third quarters of 2016, according to the report.)

After the U.K., France, Germany and the Netherlands are the top three countries for online alternative finance by market volume in Europe, according to a September 2016 report by the Cambridge Centre for Alternative Finance.

Asian markets, meanwhile, show significant promise for alternative finance players to make their mark due to the sizeable population of digitally savvy consumers who are still largely underbanked. China is by far the largest market for alternative lending in Asia. It’s also the world’s largest online alternative finance market by transaction volume, registering $101.7 billion in 2015, according to the March 2016 Cambridge Centre for Alternative Finance report. This constitutes almost 99 percent of the total volume in the Asia-Pacific region, the research shows. To date, most of the growth in China specifically has been from local firms, but that could change as the market there continues to develop.

Although there are many possible international markets to explore, U.S. lenders have to tread carefully before planting roots elsewhere, observers say. Some smaller U.S. lenders may find domestic expansion easier and more cost-effective because of the time, regulatory and financial commitment that goes along with exploring international markets. It’s a lot easier, for instance, to expand from New York to California, than it is to build out internationally.

Although there are many possible international markets to explore, U.S. lenders have to tread carefully before planting roots elsewhere, observers say. Some smaller U.S. lenders may find domestic expansion easier and more cost-effective because of the time, regulatory and financial commitment that goes along with exploring international markets. It’s a lot easier, for instance, to expand from New York to California, than it is to build out internationally.

“Why take on all the added costs and regulatory pressures, when you haven’t fully explored your home market, unless the business that you’re in deems it necessary,” says Mark Abrams, partner with Trade Finance Global, a London-based international corporate finance house, specializing in crossborder trade.

“It doesn’t make sense to start as a U.S. lender, do a few loans and then jump over to the U.K,” he contends.

What’s more, foreign banks looking for alternative lending partners typically prefer to work with larger, more established players. Even though new players’ technology may be ahead of the curve, the banks still want a longer track record. “It’s reputational for these banks,” says Singh of EY.

MANY CHALLENGES TO INTERNATIONAL EXPANSION

Several alternative lenders say they see significant growth opportunities by expanding internationally. At the same time, however, they are mindful of the substantial headwinds they face.

Regulation is among the biggest, if not the biggest, challenge. A lot of firms in the U.S. have invested a lot of time and money to get up to speed on U.S. regulations. When they look to Europe or to Canada or Mexico or elsewhere, there are different regulations. “If you’re speaking to folks in three continents, now you are looking at regulations times three,” says Singh of EY.

Certainly there’s a time commitment involved; it can take six to eight months for a U.S. lender to get their U.S.–based platforms compliant with regulations in another country, she says.

What’s more, regulatory barriers can vary greatly country to country, notes Metcalf of Affirm. Take Canada for example where very low barriers to entry exist with some provincial exceptions. In the U.K., on the other hand, it can take eight months or more to receive a lending license, he says.

That’s why it’s so important for online lenders to make strategic decisions about where they want to invest their time and resources—even if they have sound technology that’s easily adaptable outside the U.S. “The minute you throw in cross-border regulations, it gets very complicated,” Singh says.

Understanding the local culture of the market you’re trying to tap is also crucial, according to Rob Young, senior vice president of international at OnDeck, where he oversees all aspects of the company’s non-U.S. expansion efforts.

Within the past several years, OnDeck has begun offering small business loans to customers in Canada and Australia. Frequently Canada is a first step for U.S. companies that want to expand internationally because of the shared language and similarities between the economies, Young explains.

After the Canadian operation was successfully underway, the opportunity arose for the online lender to expand to Australia—which shares several similarities with the Canadian market. OnDeck doesn’t break out how much of its overall loan portfolio comes from these two markets, but it has announced publicly that it’s delivered more than CAD$50 million in financing to Canadian small businesses since 2014.

“So far we’re very satisfied with the performance,” Young says, referring to its expansion into both Canada and Australia.

Young notes that while a U.S.-based alternative lender can leverage certain things like technology from a central location within its home country, having dedicated teams on the ground in local markets is also critical. Marketing and pricing all have to be competitive with the needs of the local market, he says.

In Canada and Australia, for example, OnDeck has found that the “personal element” is really important. Young says customers there expect to interact with sales representatives who have ties to the community, understand the local market and can relate to the issues small businesses there are facing.

“I don’t think you can establish that rapport if you are trying to serve them with a sales team overseas,” he says.

U.S.-based alternative lenders also need to be careful to create products that fit the culture and needs of a particular market. For instance, alternative players that focus on luxury asset-based lending would want to look at countries with high concentrations of wealth. “It doesn’t make sense to grow to a country where there’s very little wealth because you’re not going to have much success,” says Abrams, of Trade Finance Global.

Even knowing the market well doesn’t guarantee results, which Lending Technologies, a white label technology provider for the MCA space, has discovered first hand.

Markus Schneider, the company’s chief executive, is originally from Switzerland and he knows the market there well, so he set out to fill a void he saw for an MCA-like product. However, Lending Technologies, which has offices in New York and Zurich, has hit some roadblocks along the way.

“It’s a very different mind-set there. People are more risk-adverse,” Schneider says.

The company already has a Swiss distribution partner in place, but has had trouble finding a lender willing to underwrite the funds. Schneider would also be willing to work with a U.S. lender that wants to partner with Lending Technologies to provide MCA services to merchants in his home country.

“We’re going to do this. It’s just a matter of time,” he says. “There’s a tremendously underserved segment of the market there.”

FINDING THE RIGHT FIT

To be successful internationally, U.S. companies also have to be willing to shift gears as needed when things aren’t working out as expected.

Take Kabbage, for example. The small business lender expanded into the U.K. in 2013, two years after its U.S. debut. But the company found that having its own small business lending business in the U.K. was too challenging for regulatory and capital reasons. It no longer offers new loans from this platform.

Instead, the funding company decided that a better global strategy was to license its technology to financial institutions in international markets a less capital-intensive, yet economically sound way of doing business.

Kabbage—which recently announced the establishment of its European headquarters in Ireland—has licensing arrangements with Santander in the U.K., Kikka Capital in Australia, Scotiabank in Canada and Mexico and ING in Spain. The company plans to launch operations in several additional countries this year where banks use Kabbage’s technology to offer online loans to their clients, says Pete Steger, head of business development at Kabbage.

“We are partnering with local experts. That’s our strategy,” Steger says.

Funding Circle has also made changes to its international strategy. Earlier this year, the company—which got its start in the U.K.—announced that it would stop issuing new loans in Spain. The Spanish version of the company’s website says that it continues to monitor ongoing loans so investors receive monthly payments for the projects they have invested in.

A spokeswoman for Funding Circle said the company continues “to look at new geographies, but we have no immediate plans for expansion and are focused on building a successful business here in the U.S., U.K., Germany and the Netherlands.” She declined to comment further.

Without divulging too many details, a handful of U.S.-based alternative financiers say they continue to look at additional markets outside their home turf.

For its part, SoFi has announced plans to expand to Australia and Canada this year. The company’s chief executive has also talked about European and Asian expansion in the future.

On the international front, Affirm is currently evaluating markets that make the most sense for its business model, Metcalf says. Affirm is also looking at possible acquisitions in developed markets such as the U.K. and Sweden as well as considering “serious investment” in new distribution models in southeast Asia, Mexico and Brazil, he says.

LendingClub, meanwhile, last November announced a significant partnership with National Bank of Canada and its U.S. subsidiary Credigy. The agreement provides for Credigy to invest up to $1.3 billion over the subsequent twelve months. A spokeswoman for LendingClub said the company has nothing to share about plans for international expansion.

As for OnDeck, Young says the company is exploring a number of options; it’s a matter of finding markets where gaps exist in small business lending and where potential customers have a willingness to borrow online.

“We want to be the preferred choice for small businesses. It’s not necessarily defined geographically,” Young says. “We review markets all the time. There are a number of markets that are interesting to us.”

Catching Up With Marketplace Lending – A Timeline

June 13, 20174/11 Regions Bank recruited Kabbage’s chief technology officer, Amala Duggirala, to become its chief information officer

4/12 Federal Reserve Published their 2016 Small Business Credit Survey

4/13

- Marathon Partners, a minority shareholder of OnDeck, publicly called on the company to make changes

- Fifth Third Bank partnered with Accion to support lending to underserved small businesses

4/17 Affirm surpassed the mark of making more than 1 million loans since inception

4/20 YieldStreet surpassed $100M in loans funded since inception

4/21 Glenn Goldman stepped down as Credibly’s CEO

4/25

- SmartBiz Loans announced partnership with Sacramento-based Five Star Bank

- CommonBond begins offering loans to undergrads directly

4/26 State regulators sued OCC over fintech charter proposal

4/28

- IOU Financial announced that they loaned $107.6M to small businesses in Q1

- China Rapid Finance announced their IPO

5/2

- Funding Circle closed their online forum

- Elevate’s Debt facility with Victory Park Capital increased from $150M to $250M

5/3

- Prosper Marketplace disclosed that it miscalculated returns shown to retail investors

- Square announced that they loaned $251M to small businesses in Q1

- Nav raised $13M from investors that include Goldman Sachs and Steve Cohen’s Point72 Ventures

5/4

- Vermont governor signed into law new licensing requirements for anyone soliciting loans to Vermont borrowers.

- Lending Club announced that they loaned $1.96B in Q1

5/5 Thomas Curry steps down as OCC head, replaced by Acting Head Keith Noreika

5/8

- OnDeck announced it was substantially reducing its workforce as part of its plan to achieve profitability. The stock price proceeded to hit record lows.

- Dv01 announced reporting partnership with SoFi

- With no IPO on the horizon, SoFi revealed that they began letting their employees sell some of their stock

5/9

- In the United States District Court, The Southern District of New York ruled that a purchase of future receivables was not a loan largely because it was not absolutely payable. Colonial Funding Network, Inc. as servicing provider for TVT Capital, LLC v. Epazz, Inc. CynergyCorporation, and Shaun Passley a/k/a Shaun A. Passley

- The value of 1 Bitcoin surpassed $1,700.

5/10

- CFPB announces that it will begin work on small business loan data collection pursuant to Section 1071 of Dodd-Frank.

- CFPB publishes a white paper on small business lending

- SoFi revealed that they will apply for an industrial bank charter

5/12 NY’s banking regulator sued the OCC over its proposed fintech charters

5/15

Prosper announced that they lent $585M in Q1 and had a net loss of $23.9M

5/16

- Media outlets reported that SoFi is expanding into wealth management

- Lending Club named PayPal’s former head of Global Credit Steve Allocca as President

- OnDeck’s share price hit a new all-time low

See previous timelines:

2/17/17 – 4/5/17

12/16/16 – 2/16/17

9/27/16 – 12/16/16

Are Small Business Borrowers Bank-Loyal to a Fault?

June 1, 2017 Applying for a small business loan is easier than it’s ever been. Online lenders have streamlined the process, brought it all online and whittled down approval times. Still, the majority of small business owners still think a bank is the only place to get a loan. They’re four times more likely to seek funding from banks than any other source; more than 80 percent of funding applications go to traditional financial institutions.

Applying for a small business loan is easier than it’s ever been. Online lenders have streamlined the process, brought it all online and whittled down approval times. Still, the majority of small business owners still think a bank is the only place to get a loan. They’re four times more likely to seek funding from banks than any other source; more than 80 percent of funding applications go to traditional financial institutions.

Big banks’ small business loan approval rates have dropped sharply thanks to tightened regulations and compliance costs post-Great Recession. Because the transaction costs on a $100,000 loan are roughly the same as a $1,000,000 loan, banks are passing right over small business owners seeking smaller amounts. And since the majority of small businesses want loans smaller than $100,000, they’re not being served by the institutions they turn to first.

Small Business Borrowers Turn to Banks First, But They’re Not as Loyal as They Seem

While it would seem that small business borrowers are loyal to a fault, a Lendio survey of 50,000 business owners found that 74 percent of them would move their account to a new bank if the new bank offered them a loan.

Business owners may be keeping their deposits at banks and turning there first when they set out to obtain funding, but when push comes to shove, they want the easiest path to accessing the capital that will keep their businesses afloat or help them to grow and scale.

Banks Realize They Can’t Rely on Customer Loyalty Alone

Banks have shifted some of their focus back to the small business loan market in the last couple of years. In this space where online lenders have made the process of applying for a loan much more customer-friendly, banks have realized that in order to remain competitive, become more effective and profitable, and ultimately retain customers, they must take a page from the book of online lending.

As little as two years ago, banks were closed off to the idea of outsourcing in the online lending space, while lending firms were armed with technology and ready to compete. Banks have caught on to the idea that investing in a fintech partnership is a quicker, less-expensive way to build technology and create a better customer experience without completely reinventing the wheel, allowing them to serve more of the small business borrowers they’ve been turning away. Now both parties are seeing the value in joining forces.

Recent partnerships in areas such as merchant services, researching, underwriting and accounting software have paved the way for more collaboration between banks and online lenders. Last year we saw banks begin to explore new strategies for converging with online lenders through licensing deals and partnerships, and this year we’ll see even more collaboration in the marketplace.

Partnerships, like JPMorgan Chase’s team-up with online lenders OnDeck and LiftFund, allow banks to leverage technology while expanding their loan offerings and revenue. ScotiaBank, Santander and ING have collaborated with online lender Kabbage to license its technology platform for automating a more efficient underwriting process and to provide more comprehensive lending solutions.

Bank-Alternative Lending Partnerships Are a Win-Win-Win

For banks, the benefits of an alternative lending partnership lie not only in cost savings and tech advances, but also in building and maintaining those loyal customer relationships that have served them for decades. Banks will be able to capture a new generation of customers while also retaining more of their existing customers’ deposits by providing them a better, more streamlined loan application and approval process.

And in such partnerships, online lenders and marketplaces win big too, with access to some of the built-in advantages of a bank: an existing customer base with a high level of trust, risk management experience, access to key data and the ability to offer low-cost capital.

Bank-fintech partnerships offer both parties the opportunity to improve processes and reduce costs. And more importantly, they offer those bank-loyal small business borrowers more options, more efficiently when they turn to the banking institutions they know. When banks and online lenders collaborate to serve small business owners, it’s a win-win-win.

Fintech Sandbox? States, OCC Mull Regulatory Options

May 2, 2017It’s called the “New England Regulatory FinTech Sandbox.”

State banking regulators across the six New England states are exploring the creation of a regional compact that would allow financial technology companies to experiment with new and expanded products in “a safe, collaborative environment,” says Cynthia Stuart, deputy commissioner of the banking division at the Vermont Department of Financial Regulation.

Stuart asserts that she and her New England cohorts are adroitly positioned and uniquely qualified to oversee laboratories of finance. In Vermont, for example, she heads an agency that oversees regulation and examination of banks, trust companies, and credit unions as well as such nonbank financial providers as mortgage brokers, money transmitters, payday lenders and debt adjusters.

Financial watchdogs at the state level, Stuart observes, “are already witnesses to a wide breadth of financial services offerings and understand how they impact communities and consumers. As technology intersects with financial regulation,” she adds, “state regulators also appreciate the need to be open to technological innovation while balancing risk and return.”

The regional fintech sandbox is the brainchild of David Cotney, the former Massachusetts Commissioner of Banks, and Cornelius Hurley, director of Boston University’s Center for Finance, Law and Policy. The sandbox stitches together elements of Project Innovate, a development program for fintechs inaugurated by the U.K.’s banking regulator, and the European Union’s “passport” model for cross-border banking operations.

In the U.K., the Financial Conduct Authority is supporting both small and large businesses “that are developing products and services that could genuinely improve consumers’ experience and outcomes,” according to a 2015 report by the London agency. In harmonizing the regulatory regime for the sandbox across state lines of Maine, New Hampshire, Vermont, Massachusetts, Rhode Island and Connecticut, the program emulates the EU’s “passport.” Since 1989, a bank licensed in one EU country has been able to set up shop there while – thanks to the “passport” –operating seamlessly throughout the 28 states of the EU (soon to be 27 after “Brexit”).

“It’s still preliminary,” Cotney says of the proposed New England sandbox-cum-passport, “but we’ve talked to the financial regulators in all six states and there’s universal openness. Nobody want to be seen as being a barrier to innovation.”

(Barred by law from lobbying in Massachusetts, Cotney hands off the Bay State duties to Hurley while he meets with regulators and other officials in the five remaining New England states. In March, Cotney was named a director at Cross River Bank, a Fort Lee, N.J.-based, $600 million-asset community bank known for its partnerships with peer-to-peer lenders including Lending Club, Rocket Loans and Loan Depot.)

This nascent effort of financial Transcendentalism in New England is, meanwhile, taking place against the backdrop of an increasingly acrimonious battle between the Office of the Comptroller of the Currency and state banking authorities over the licensing and regulation of fintech companies. At issue is the OCC’s plan announced in a December, 2016 “whitepaper” to issue a “special purpose national bank” charter to nonbank fintechs.

Siding with the OCC are the fintechs themselves, including Lending Club, Kabbage, Funding Circle, ParityPay, WingCash. “A special purpose national bank charter for fintechs creates an opportunity for greater access to banking products, empowers a diverse and often underserved customer base, promotes efficiency in financial services, and encourages industry competition,” Kabbage wrote to the OCC in a sample industry comment to its whitepaper (which is on the agency’s website).

Also on board for the OCC’s fintech charter are powerful Washington trade associations such as Financial Innovation Now, the membership of which comprises Amazon, Apple, Google, Intuit and PayPal, and industry research organizations like the Center for Financial Services Innovation. The U.S. banking establishment also appears largely supportive of the OCC. While qualifying its imprimatur somewhat, the American Bankers Association declared that it “views the OCC’s intent to issue charters as an opportunity to further bring financial technology into the banking system…”

But an irate army of detractors is condemning the fintech charter outright. Consumer groups, small-business organizations, community banks, and state attorneys general number among the furious opposition. No cohort, however, has been more hostile to the OCC’s fintech charter than state banking regulators.

Maria T. Vullo, superintendent of New York State’s Department of Financial Services, has emerged as a firebrand. “The imposition of an entirely new federal regulatory scheme on an already fully functional and deeply rooted state regulatory landscape,” she wrote to the OCC earlier this year, “will invite serious risk of regulatory confusion and uncertainty, stifle small business innovation, create institutions that are too big to fail, imperil crucially important state-based consumer protection laws, and increase the risks presented by nonbank entities.”

Although big-state regulators from New York, California and Illinois have been in the vanguard of opposition, their unhappiness with the OCC is widely shared. Vermont regulator Stuart, who emphasizes the need for regulators “to embrace change,” nonetheless disparages the OCC’s endeavor.

“Of particular concern is the creation of an un-level playing field for traditional, full-service Vermont institutions to the advantage of the proposed nonbank charter,” she told AltFinanceDaily. “The special purpose national nonbank charter would not be subject to most federal banking laws and would be regulated with a confidential OCC agreement. The disparity in regulatory approaches is concerning.”

What had been confined to a war of words – rounds of angry denunciations packed into letters and press releases directed at the OCC — reached fever-pitch last week when, on April 26, the Conference of State Banking Supervisors filed suit against the OCC in federal court. The lawsuit seeks to prevent the agency “from moving forward with an unlawful attempt to create a national nonbank charter that will harm markets, innovation and consumers,” according to a CSBS statement.

Among other things, the conference’s complaint charges that by creating a national bank charter for nonbank companies, the OCC has “gone far beyond the limited authority granted to it by Congress under the National Bank Act and other federal banking laws. Those laws,” the conference’s statement continues, “authorize the OCC to only charter institutions that engage in the ‘business of banking.’”

Under the National Bank Act, the conference’s complaint asserts, a financial institution must “at a minimum” accept deposits to qualify as a bank. By “attempting to create a new special purpose charter for nonbank companies that do not take deposits,” the complaint adds, the OCC is acting outside its legal authority.

Christopher Cole, senior regulatory counsel at the Independent Community Bankers Association – a Washington, D.C. trade association of Main Street bankers known for punching above its weight — asserts that the state banking regulators are on solid ground. “The whole question comes down to what should a bank be for purposes of a national bank charter,” he says in a telephone interview. “The Bank Holding Company Act (of 1956), federal bankruptcy laws, and tax laws – all three – define banks as insured depository institutions. It’s right there in the statutes. So our recommendation,” he says, “is for the OCC to go back to Congress” and ask for the explicit authority to create a fintech charter.

Because the OCC has “short-circuited rule-making” protocol required by another law – known as the Administrative Procedures Act — “the process hasn’t been kosher,” Cole adds.

Many members of Congress are also expressing outrage at the OCC. Not only have Democratic Senators Sherrod Brown of Ohio and Jeff Merkley of Oregon strenuously objected to the OCC’s fintech charter, but on March 10, 2017, Jeb Hensarling, the chairman of the House Financial Services Committee, fired off a “hold-your-horses” letter to Comptroller Thomas J. Curry. Signed by 34 House Republicans, the March 10 letter reminded Curry that his term of office would officially be up at the end of April, 2017, and urged him not to “rush this decision” regarding the fintech charters.

Many members of Congress are also expressing outrage at the OCC. Not only have Democratic Senators Sherrod Brown of Ohio and Jeff Merkley of Oregon strenuously objected to the OCC’s fintech charter, but on March 10, 2017, Jeb Hensarling, the chairman of the House Financial Services Committee, fired off a “hold-your-horses” letter to Comptroller Thomas J. Curry. Signed by 34 House Republicans, the March 10 letter reminded Curry that his term of office would officially be up at the end of April, 2017, and urged him not to “rush this decision” regarding the fintech charters.

“If the OCC proceeds in haste to create a new policy for fintech charters without providing the details for additional comment, or rushing to finalize the charter prior to the confirmation of a new Comptroller,” the letter from Hensarling et alia declares, “please be aware that we will work with our colleagues to ensure that Congress will examine the OCC’s actions and, if appropriate, will overturn them.”

Never mind the stern letter from Chairman Hensarling, or the fact that an impressive array of Congressmembers on both sides of the aisle are bipartisanly unhappy, or that state banking regulators’ have filed suit, or that Curry’s replacement as Comptroller is overdue: the OCC is pushing ahead. The agency will play host to a bevy of financial technology companies and other financial institutions on May 16 for two days of get-acquainted sessions in its San Francisco office.

Billed as “office hours,” the West Coast meetings will consist of one-on-one, hour-long informational meetings “to discuss the OCC’s perspective on responsible innovation,” Beth Knickerbocker, the OCC’s acting chief innovation officer, says in a press release.

The office hours, Knickerbocker adds, “are an opportunity to have candid discussions with OCC staff regarding financial technology, new products or services, partnering with a bank or fintech company, or other matters related to financial innovation.”

Back in New England, Hurley, the Boston University law professor advocating the regional sandbox, says: “No one knows where fintech is going. But one place it’s not going is away.”

Alternative Lending Is Dead

April 30, 2017At LendIt, Kabbage co-founder & CEO Rob Frohwein, blew the roof off the house with his presentation. Titled, “Alternative lending is dead, long live data,” he explained what he believes the industry should really be about.

On why the term alternative lending doesn’t make sense:

Think about Uber, when they talk about their business. Their tagline is ‘when you don’t feel like taking a taxi.’ They don’t call it alternative transportation at its best

On how most companies have been answering the wrong question:

The question answered by most online lenders is, ‘can you fill the void left by banks?’ I will tell you right now that the question that should’ve been answered by folks going into online lending would be ‘why aren’t banks filling this void?’ When you ask a different question, you get a different answer.

I’m not trying to prove that small businesses need capital. That is blatantly obvious. I’m trying to prove that there is a better way to do it.

Most online lenders tried to disrupt banks by proving they could grow fast and they could acquire capital, but there is only one problem with that approach. You don’t disrupt banks by focusing on the advantage that banks have over you. Banks have customers and money. That is mostly what they have. They have customers and money. So why disrupt the space with the two items that they actually have? The question that should’ve been asked and answered is, ‘why aren’t banks filling this void?’

The answer to that is, because they can’t profitably, for our industry, they can’t profitably serve small business customers. When you ask that question and you figure out the reason, you start building your business a little bit different

On why an online application doesn’t make you a technology company:

Most online lenders thought that by calling themselves a technology company, that they were one, but that wasn’t the case. The biggest piece of technology that most of them promote, is an online application. That’s it. If you think about it, it’s an online application. Everything else is manual. There is nothing, nothing special about an online application.

And outside the US, we’ve already launched in Australia, Spain, the UK, Canada and Mexico. And we’re going to be announcing two other territories in the next several weeks. And by the way, we have no employees in those markets, because we’re able to operate everything remotely because we’re a technology company.

If your business is scaling really fast, and your opex (operating expense) is doing anything but going down, you’re not operating a technology company. Everyone else is flat or up on opex, but we can continue to go down. If you’re running a technology company, you don’t have to lay people off at the slightest hint of trouble and do you know why? Because you don’t have too many employees. Your business scales. Right?

Catching Up With Marketplace Lending – A Timeline

April 20, 20172/17

- Prospa, an online small business lender based in Australia, was valued at $235M (AUD) in a $25M capital raise

- Square announced funding $248 million worth of business loans in Q4 2016

2/21 A Massachusetts state court vacated a merchant cash advance COJ

2/24 SoFi raised $500M in a financing round led by Silver Lake Partners that reportedly gave SoFi a $4.3B valuation

2/27 Prosper Marketplace closed a loan purchase agreement with a consortium of lenders for up to $5 billion of loans that has a provision that also enables the lenders to buy up to 35% of the company

2/28 BlueVine secured a warehouse line of up to $75M from Fortress

3/1 Lendio launched a new franchise program, allowing local offices around the country to become Lendio franchisees

3/3 Citing Madden v Midland, Colorado regulator brought a federal lawsuit against Marlette Funding for violating the state’s usury cap

3/5 Two trade associations, the Innovative Lending Platform Association (ILPA) and the Coalition for Responsible Business Finance (CRBF), joined forces. The merged company will continue to be known as ILPA

3/6 Upstart raised $32.5M

3/7

- It’s reported that former CAN Capital CFO Aman Verjee is now the COO of 500 Startups

- Kabbage priced a $525M securitization. It was oversubscribed

3/9 Citing Madden v Midland, Colorado regulator brought a federal lawsuit against Avant for violating the state’s usury cap

3/13

- Melvin Chasen, the founder of Rewards Network (originally Transmedia Network, Inc.) passed away. He was 88.

- The New York State Assembly rejected the Governor’s proposal to grant the Department of Financial Services (DFS) regulatory authority over any online lender doing business in the state

3/15

- The New York State Senate also rejected the proposal to further regulate lending

- The OCC published a manual on how it will evaluate charter applications from fintech companies

- The New York DFS published a statement rejecting the OCC’s plans

- The WSJ reported that Marlette Funding was cutting nearly 1/5th of its workforce

3/16 WebBank announced that it had a net income of $29.2M for 2016 and that it had a market valuation of $319.4M

3/20 Prosper Marketplace announced that it had originated $2.2B in loans in 2016, down from $3.7B in 2015, and had a net loss of $119M.

3/21 It’s reported that Kabbage will set up its European headquarters in Ireland

3/22 OnDeck expanded its credit facility with Deutsche Bank by $52M to a total of up to $214M

3/27 IOU Financial wins Gold Stevie Award for Best Use of Technology in Customer Service

3/30 In Advance Capital announced that they had secured access to an additional $50M

4/5

- Budget passes in New York. Proposed lending legislation was not included in it.

- Kabbage surpasses $3 billion funded to small businesses

See previous timelines:

12/16/16 – 2/16/17

9/27/16 – 12/16/16

New York’s State Government is Competing With Online Lenders on Pay-Per-Click and Misinforming Small Businesses

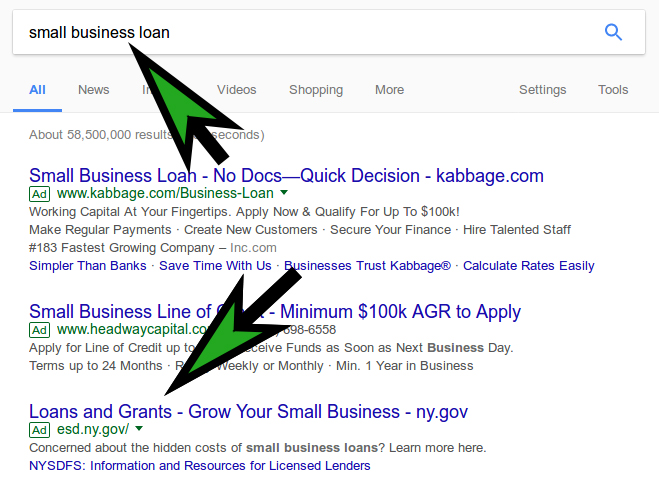

March 10, 2017Move over online lenders, New York’s financial regulator is apparently shelling out big bucks to steer away New York’s online small business loan searchers to THEMSELVES. As someone who has historically kept tabs on Google’s search results for lending related keywords, this new result is one of the more interesting developments I’ve seen yet.

From a New York IP, querying Google with the keyword small business loan produced not only an ad for Kabbage and other online lenders, but also prominent paid placement from New York State with a sitelink extension to the New York Department of Financial Service’s page about licensed lending requirements.

While there’s nothing that weird about marketing state-assisted development programs, the main Google ad link directs visitors to “Navigate the Lending Landscape” by clicking a “Learn More” button.

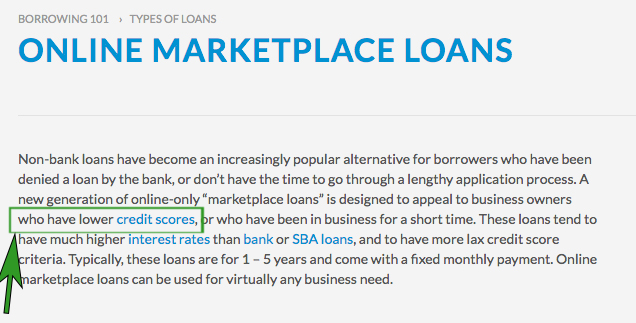

That takes you to Venturize.org, operated by Opportunity Finance Network, a Community Development Financial Institution (CDFI) that New York is apparently really doing the advertising for. And there’s a major problem with that.

The information across that site is wildly incorrect. It explains online marketplace loans as “designed to appeal to business owners who have lower credit scores, or who have been in business for a short time.” That’s a pretty broad statement especially when many online marketplace lenders are in fact designed to appeal to business owners who have higher credit scores and have been in business for a long time.

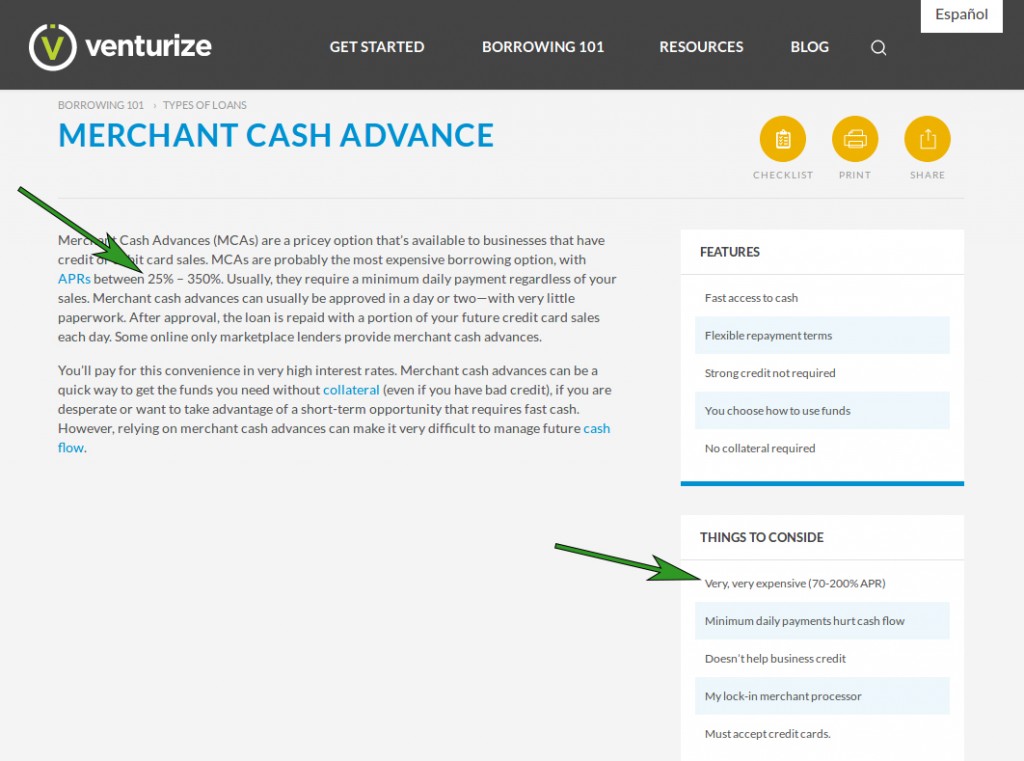

The description of merchant cash advances is even worse. Whoever wrote it has no understanding of them in the slightest. Good thing New York State is paying up to $100 a click with our tax dollars for premium keywords to teach businesses absolute nonsense! I quote what the website says below and my comments are in red next to them.

- “Usually, they require a minimum daily payment regardless of your sales.” – Um, no

- “After approval, the loan is repaid with a portion of your future credit card sales each day.” They’re not loans. This is mostly well settled in the New York Court system. Recently, see this and this

- “You’ll pay for this convenience in very high interest rates” – There are no interest rates

- “MCAs are probably the most expensive borrowing option, with APRs between 25% – 350%.” – Wrong. No APRs can be calculated on a purchase transaction

- “if you are desperate” – That’s a pretty unfair statement to say that a methodology is only for the desperate. New York State is insulting its small business constituency, private companies, and the jobs that have been maintained or created all at the same time

There are also typos and spelling errors throughout the page, as well as conflicting information. The very same page describes MCAs as having between 70% – 200% APR on one side and between 25% – 350% APR on the other side. You don’t need anymore proof that whoever wrote this stuff was just winging it on the fly to make it sound bad. These are the kinds of misleading figures that the CFPB sues financial institutions for and perhaps they should actually take a look at this.

It also says that businesses must accept credit cards. That’s not true either.

It’s strange that a CDFI would go to such great lengths to deliberately misinform small businesses, let alone have a state government foot the bill for them to do it.

Furthermore, as someone who recently used an online marketplace loan for my business, I’m personally offended that my state government would pay to market information that says it was designed to appeal to business owners who have lower credit scores. As my FICO score is over 800, the writer clearly does not understand the product, the market, or the appeal.

More troublesome of course, is that the NYDFS hopes to regulate these industries through language snuck in Governor Cuomo’s budget proposal. Given the above, what could possibly go wrong?

The Top Small Business Funders of 2016

March 6, 2017The MCA and small business lending origination numbers for 2016 are in. In some cases, a company may have merely placed or facilitated an acquired customer with a partner or competitor (but still counted them in their annual volume) and thus the figures do not necessarily represent what actually went on balance sheet. The rankings omit some larger players for which no data could be confirmed and when a reasonable estimate could not be made.

| Company Name | 2016 Origination Volume | 2015 | 2014 |

| OnDeck | $2,400,000,000 | $1,900,000,000 | $1,200,000,000 |

| PayPal Working Capital | $1,500,000,000* | $900,000,000* | $250,000,000* |

| Kabbage | $1,250,000,000 | $1,000,000,000 | $400,000,000 |

| CAN Capital | $1,100,000,000* | $1,500,000,000* | $1,000,000,000* |

| Square Capital | $798,000,000 | $400,000,000 | $100,000,000 |

| Bizfi | $550,000,000 | $480,000,000 | $277,000,000 |

| Yellowstone Capital | $460,000,000 | $422,000,000 | $290,000,000 |

| Strategic Funding | $375,000,000 | $375,000,000 | $280,000,000 |

| National Funding | $350,000,000 | $293,000,000 | |

| BFS Capital | $300,000,000 | ||

| BlueVine | $200,000,000* | ||

| Platinum Rapid Funding Group | $180,000,000 | $100,000,000 | |

| IOU Financial | $107,600,000* | $146,400,000 | $100,000,000 |

*Asterisks signify that the figure is an estimate