You Can Ask Alexa to Pay Your Credit Card Bill – Will Loans Be Next?

March 11, 2016 Very soon, you will be able to pay your bills just a second after you turn on that thermostat.

Very soon, you will be able to pay your bills just a second after you turn on that thermostat.

Capital One and Amazon want to give Alexa, the “skill” to become your personal teller and allow the home automation device to pay your bills, check balances and review transactions.

Starting next week, Capital One customers will be able to use the app through Alexa and instruct the digital assistant.

“Alexa, ask Capital One for recent transactions on my checking account”

“Alexa, ask Capital One for my Quicksilver Card balance.”

“Alexa, ask Capital One to pay my credit card bill.”

Of course, security concerns will remain key as Internet Of Things slowly finds a way into people’s homes. But for now, Alexa can take care of that outstanding cellphone bill.

If the feature catches on, it will only be a matter of time before loans become a thing you can wish for out loud and have Alexa make a reality.

Square’s Merchant Cash Advance Program Now Among Biggest in the World

March 10, 2016Square originated more than $400 million worth of merchant cash advances advances in 2015, according to their Q4 earnings report. Their average deal size was just shy of $6,000. The result is a 300% increase year-over-year and makes them one of the largest players in that industry worldwide.

RANKINGS

| Company Name | 2015 Funding Volume | 2014 Funding Volume |

| OnDeck | $1,900,000,000 | $1,200,000,000 |

| CAN Capital | $1,500,000,000 | $1,000,000,000 |

| Funding Circle | $1,200,000,000 | $600,000,000 |

| PayPal Working Capital | $900,000,000 | $250,000,000 |

| Bizfi | $480,000,000 | $277,000,000 |

| Fundry (Yellowstone Capital) | $422,000,000 | $290,000,000 |

| Square Capital | $400,000,000 | $100,000,000 |

| Strategic Funding Source | $375,000,000 | $280,000,000 |

A much longer list will be available in AltFinanceDaily’s March/April 2016 Magazine Issue. SUBSCRIBE FREE to make sure you obtain a copy.

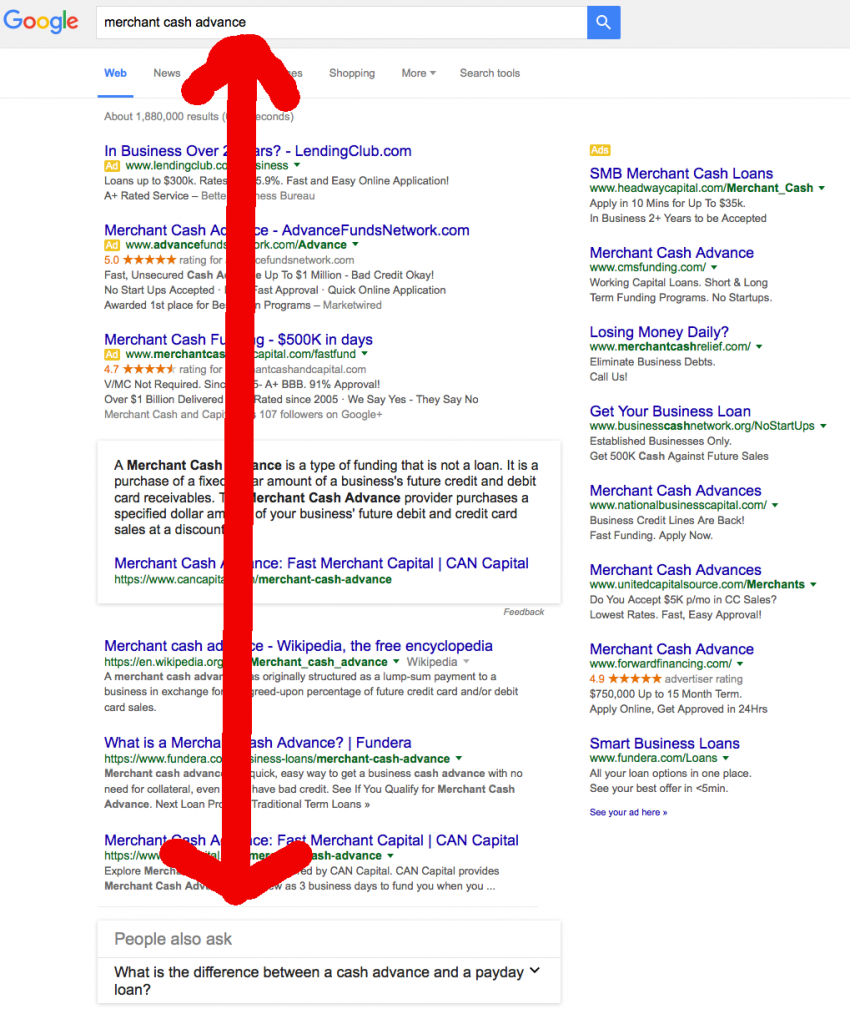

Google Serves Low Blow to Merchant Cash Advance Seekers

December 2, 2015 Almost eighteen months ago, I explored whether or not Google was rigging the search results to benefit two lending companies they had equity investments in, Lending Club and OnDeck. At the time, both companies ranked at the top for highly coveted keywords even if they weren’t directly related to the user’s search query.

Almost eighteen months ago, I explored whether or not Google was rigging the search results to benefit two lending companies they had equity investments in, Lending Club and OnDeck. At the time, both companies ranked at the top for highly coveted keywords even if they weren’t directly related to the user’s search query.

Now that those two companies are public, a company called Credit Karma seems to have inherited the top spots. And wouldn’t you know it, Google has also invested in them.

Google: loans

Google: personal loan

But that’s not the worst of it. Thanks (or no thanks rather!) to a relatively new search result feature called “People Also Ask,” one keyword recently started serving up results with a different kind of hidden agenda.

While my captured results may not be identical for everyone, I have conducted tests with other people on other devices and from other areas and it was present each time. With this box, Google is subtly planting the negative seed that payday loans and merchant cash advances are basically so identical that other people just like you are wondering what the difference between the two are. But here’s the rub, the two have nothing to do with each other and it’s unlikely so many people are asking that.

Pay no mind to the fact that the box makes reference to a “cash advance” not a “merchant cash advance.” The painstaking mishap could be innocently chalked up to an algorithmic error if only googling just cash advance revealed the same box in the results. But it doesn’t. Only merchant cash advance brings this up.

Comparing merchant cash advances to payday loans is straight out of the anti-merchant cash advance propaganda playbook. At least one Google-owned business lending company is actively lobbying against short term business lending and merchant cash advances in Washington so the placement and comparison of the People Also Ask box in their results is highly suspicious.

It’s no secret that Google is also directly lobbying in the online lending space too. One month ago, right before Google magically started to suggest to searchers that merchant cash advances and payday loans were related, Google formed a lobbying organization called Financial Innovation Now with Amazon and Apple. On their main agenda is online lending.

Given the suspicious search rankings for companies they have an equity stake in, I would not doubt for a second that something like this was manually inserted. I admit that my evidence and my case are weak, but given the circumstances, it’s quite possible there’s something deliberate happening here.

What do you think? Do you see this when you google merchant cash advance?

Will the Wild West of alternative lending stay that way?

November 24, 2015Comments on the regulatory future of alternative lending were included in a joint report prepared by Lendio and Dealstruck:

Blake hopes that governing agencies will offer reasonable policies that will encourage best-in-class business practices (to weed out the bad actors) without damaging the innovation and growth in the industry. Furthermore, Lendio highly recommends that any new or additional regulations come from the Federal level, rather than through a state-by-state patchwork of laws that will impose inconsistent and costly regulations on the online lenders.

– Brock Blake, Lendio CEO

Thoughtful regulation to ensure operators are performing with honesty and transparency is a good thing. And good players are stepping up to the plate to take a proactive stance regarding fair and transparent lending practices, executed ethically and with integrity. Fortunately for the small business lending market, the key lenders and marketplaces in the industry have used a blueprint of best practices that were established and implemented in the consumer lending space. It’s fascinating to think about how much room they have left to grow.

– Ethan Sentura, Dealstruck CEO

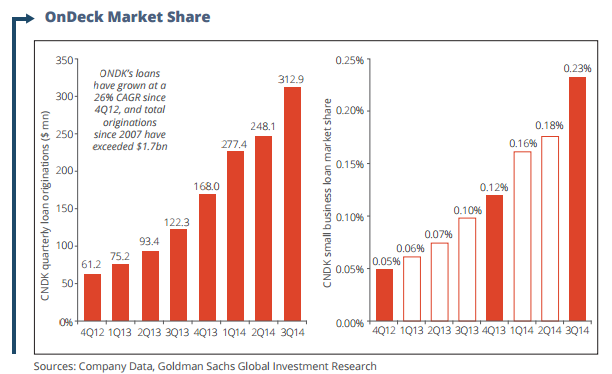

The report compiles other interesting pieces of data such as OnDeck’s share of the entire business loan market, which stood at less than a quarter of 1% just 1 year ago.

You can view Lendio and Dealstruck’s full report here.

Second Guessing Alternative Lending

August 21, 2015The best case scenario for the alternative lending industry is that every startup’s model is pure genius and all the founders’ assumptions are correct. To an extent, it kind of feels that way right now, that everyone’s riding this unstoppable growth train. I can barely go a half hour without getting an email alert telling me that yet another fintech player has raised millions to disrupt lending. The steady drumbeat of news validates ideas, concepts, and investments, and puts pressure on others to jump on board and join the party.

Meanwhile, industry conferences become self-reinforcing loops of assurance. They’re great places to hear what you already thought.

No, you’re brilliant!

No, you’re the brilliant one!

It’s incredibly easy to get caught up in it all. I am guilty of it myself sometimes. I know this because my pedestrian friends outside the industry have reacted to the investment opportunities in it with extreme skepticism.

“But isn’t this brilliant?!,” I ask them. Most are amused, but I’ve never convinced a pedestrian to invest in marketplace loans. They see flaws and risk all over it, and sometimes for reasons I hadn’t even considered. I compared these responses in my head with responses I’ve heard from industry professionals. Was the contrast in feelings reflective of differing philosophies? And do industry professionals just have more knowledge to think the way they do?

I had an epiphany when a colleague sent me a link to a short puzzle published on the NY Times website to see if I would arrive at the same conclusion that she did. I didn’t.

For the sake of fun and knowing what I’m talking about, you can take it here.

.

.

.

.

.

.

.

KEEP SCROLLING

.

.

.

.

.

.

.

.

.

.

.

.

KEEP SCROLLING

.

.

.

.

According to a sample, a mere 9 percent heard at least three nos — even though there is no penalty or cost for being told no. 78 percent never even got one no before they guessed the answer. “It’s a lot more pleasant to hear ‘yes’,” the research claims. “This disappointment is a version of what psychologists and economists call confirmation bias. Not only are people more likely to believe information that fits their pre-existing beliefs, but they’re also more likely to go looking for such information.”

The Times article is well…timely, because it’s possible there’s a running case of confirmation bias right here in the alternative lending industry. Nothing makes this more obvious than by the way Todd Baker ripped the industry to shreds in his August 17th article for American Banker. In Marketplace Lenders Are a Systemic Risk, he opens by writing, “Once again the markets have fallen in love with a group of young, aggressive and not very regulated lenders.”

The Times article is well…timely, because it’s possible there’s a running case of confirmation bias right here in the alternative lending industry. Nothing makes this more obvious than by the way Todd Baker ripped the industry to shreds in his August 17th article for American Banker. In Marketplace Lenders Are a Systemic Risk, he opens by writing, “Once again the markets have fallen in love with a group of young, aggressive and not very regulated lenders.”

The sobering viewpoint was immediately met with criticism, most notably by Mike Cagney, the CEO of SoFi. Cagney issued a direct response to Baker in own American Banker piece. Of Baker, he wrote, “While his intentions are good, his rationale is flawed.”

But whether or not you agree or disagree with what Baker wrote, he’s done the industry an enormous favor. He looked at it all and said “no.” According to the Times, “We’re much more likely to think about positive situations than negative ones, about why something might go right than wrong and about questions to which the answer is yes, not no.”

Keep that in mind when Baker wrote, “If an [Marketplace Lender] MPL can’t issue new loans — which will happen any time investors refuse to buy loans in the MPL marketplace — the transaction fees that are the MPLs’ main source of revenue and cash will instantly disappear, while expenses continue to mount. An MPL has to keep issuing loans to survive.”

Few people like to think about what would happen when or if investors refuse to buy loans. And when Cagney responds directly to this by saying, “The scenario he describes can’t happen,” one has to wonder if his rationale might be subject to confirmation bias. “If there is no buyer, MPLs simply stop lending,” he explained.

Rather than rebut Baker’s argument, he seems to confirm it. Without being able to issue loans, an MPL’s revenue will disappear, and therefore an MPL indeed has to keep issuing loans to survive. How else does an MPL stay in business if it stops lending?

Baker reminds us all that we have been here before. “When sentiment changes, the MPL investors’ rush to the exits will be no less swift than it was for traditional finance companies in 2007-8 or in the Russian and Asian debt crises of the late 1990s,” he writes. He alludes that large swaths of industry professionals have convinced themselves that things will be different this time even though history continues to repeat itself.

“There is too much money to be made before the inevitable blow-up,” he laments.

Baker’s opinion is one of the best pieces I have read about alternative lending this year, mainly because he was unabashed in his criticism. I’ve always believed that the best way to feel good about your decision is to hear a lot of reasons first about why you shouldn’t do something. Coincidentally, in the Times puzzle, I got nine nos before I felt confident about the game’s rule and successfully solved it. Only 9 percent of participants got three nos or more.

Baker’s opinion is one of the best pieces I have read about alternative lending this year, mainly because he was unabashed in his criticism. I’ve always believed that the best way to feel good about your decision is to hear a lot of reasons first about why you shouldn’t do something. Coincidentally, in the Times puzzle, I got nine nos before I felt confident about the game’s rule and successfully solved it. Only 9 percent of participants got three nos or more.

Nos are healthy and should be considered a welcome concept in this industry. Those working on credit models should remember that it’s not just about confirming your theories, but also about disproving them. Build your model and then try to destroy it. Test things that you think won’t work in addition to the things you think will work. Go out there and break things. Run worst case scenarios. Fund money to a deal that you think will go bad. See what happens.

“Often, people never even think about asking questions that would produce a negative answer when trying to solve a problem — like this one. They instead restrict the universe of possible questions to those that might potentially yield a ‘yes’,” says the Times. This flawed approach could lead to catastrophe.

In The Quants: How a New Breed of Math Whizzes Conquered Wall Street and Nearly Destroyed It, odd scenarios not accounted for in computerized trading models led to disastrous losses. At times, the quants’ computers refused to acknowledge events that were actually happening because the built-in models believed they were too statistically impossible.

So when SoFi’s Cagney says, “the scenario [Baker] describes can’t happen,” in regards to the potential of an MPL failing because there are too few loan buyers, it should be taken with a grain of salt. Of course it can happen.

But it should also be mentioned that SoFi is now worth about $4 billion. That means that in a room full of alleged geniuses, Cagney is a certifiable genius. But there’s no way someone in his position would raise a fresh billion dollar round of capital and then concede to American Banker that the whole system could be torn to shreds at any moment.

The danger is that others will point to Cagney as validation that their own lending aspirations are viable even when their own models and market positioning are substantially weaker. Not every new lending startup CEO is Mike Cagney. And there is plenty of truth in Baker’s opening line, “Once again the markets have fallen in love with a group of young, aggressive and not very regulated lenders.”

A lot of arguments have been put forth about why everything is different this time, that it is impossible to fail, but we may find out just as we have countless times before that this isn’t the case.

It’s refreshing to hear someone second guess the whole industry. Hopefully if you’re a player in this space, you’ve thought of reasons why your business might be flawed. If you’re like 78% of the population that’s too scared to even get one no before committing to an answer, you’re probably in big trouble…

The Rest of the Alternative Lending Industry’s Funding Numbers

July 1, 2015 Let’s be serious, the industry’s much bigger than we may have let on when we published the industry leaderboard (some mods have been made) in the May/June issue.

Let’s be serious, the industry’s much bigger than we may have let on when we published the industry leaderboard (some mods have been made) in the May/June issue.

Right after AltFinanceDaily sent the final file off to the printers in May, PayPal announced that the widely circulated $200 million lifetime funding figures were slightly outdated.

How off were they?

Oh, just by about $300 million or so. By May 7th, PayPal’s Working Capital program for small businesses had already exceeded $500 million. The industry leaderboard has been revised to reflect the news. PayPal says they are funding loans at the rate of $2 million per day, which puts them on pace for more than $700 million a year. Um, wow?

One name that’s missing from that list is Amazon, whose secretive short term business loan program is reported to have already generated hundreds of millions of dollars in loans. Given the $300 million discrepancy that PayPal let ruminate for months, we’re in no position to speculate on Amazon. Anyone could try to assess what they’ve been up to however, since they file UCCs on their clients under the secured party name “AMAZON CAPITAL SERVICES, INC.”

Of course if you’re craving specific numbers, an anonymous source inside Yellowstone Capital revealed that Yellowstone produced $35.5 Million worth of deals in the month of June alone. Yellowstone has a strategically diverse business model that allows them to either fund small businesses in-house (essentially on their own balance sheet) or broker them out to other funders. Yellowstone was listed on AltFinanceDaily’s May/June industry leaderboard at $1.1 Billion in lifetime deals and $290 Million in 2014. June’s figures indicate that they are probably well on their way to surpassing last year’s numbers.

Curiously, platform/lender/broker/marketplace company Biz2Credit has been hanging on to the same stodgy old number for more than a year.

Funded over $1.2 billion. 200,000+ happy customers.http://t.co/3h64lI4cgG #smallbusiness #Funding

— Biz2Credit (@biz2credit) June 19, 2015

They were touting that same $1.2 Billion number exactly 1 year ago. Surely they have done more since then? Biz2Credit’s service covers a much wider scope however so a direct comparison with their peers may not be appropriate. A lot of their loans are arranged through traditional banks which are typically transacted in amounts larger than the average $25,000 deal alternative lenders do.

A source familiar with Biz2Credit’s breadth said he observed a deal where the company helped a businessman in Mexico obtain financing to purchase a new helicopter, a transaction which apparently necessitated a team to fly down there to sign paperwork. Definitely not a standard transaction!

When we published the industry leaderboard initially, it admittedly omitted some of the industry’s largest players. Many firms are fairly secretive about the numbers they release and we’re in no position to disclose numbers that aren’t supposed to be public. Below is data that we hadn’t published previously.

The industry’s unsung behemoths

The industry’s unsung behemoths

The $300 million lifetime funding figure publicized by NYC-based Fora Financial can’t be that stale. It’s the number currently stated on their website and a late February 2015 company announcement revealed they were only at $295 million at the time. We feel comfortable enough to now have Fora Financial on the leaderboard.

In 2014, Delaware-based Swift Capital revealed that they had funded more than $500 million. It’s unclear how much that’s increased since then.

Credibly (formerly RetailCapital), has publicized that they’ve funded more than $140 million in their lifetime. Founded in Michigan, the company has opened offices in New York, Arizona, and Massachusetts. They’ve been added to the lifetime leaderboard.

New York City-based AmeriMerchant has a claim on their website that they have funded more than $500 million since inception. How much more exactly? We’re not sure.

Coral Springs, FL-based Business Financial Services keeps their figures mostly under wraps but a good guess would place their lifetime figures at somewhere between $700 million and $1.2 billion.

Miami, FL-based 1st Merchant Funding had reportedly funded close to $100 million in the Spring of 2014. It’s uncertain as to where they might be now.

Woodland Hills, CA-based ForwardLine surpassed $250 million in funding as far back as 2013.

Orange, CA-based Quick Bridge Funding disclosed more than $200 million in funding in late 2014.

Troy, MI-based Capital For Merchants has funded $220 million since inception. But there’s more to the story. Capital For Merchants is owned by North American Bancard, a merchant processing firm that acquired another merchant cash advance company, Miami, FL-based Rapid Capital Funding in late 2014. And coincidentally, Rapid Capital Funding had just acquired American Finance Solutions months earlier, which is an Anaheim, CA-based merchant cash advance company that had funded more than $250 million since inception. All told, North American Bancard owns at least three merchant cash advance companies: Capital For Merchants ($220 million), American Finance Solutions ($250 million+), and Rapid Capital Funding (undisclosed). There are rumors that they’re in talks to acquire at least one more company in the space, which, if true, would make North American Bancard one of the industry’s most powerful players.

Don’t bother counting up the above totals

These figures all barely scratch the surface as AltFinanceDaily’s database indicates there are literally hundreds of genuine direct funders in the industry.

Thanks to the company representatives that took the time to confirm their funding numbers with us directly. Anyone interested in sharing their figures can email sean@debanked.com. If there is a gross inaccuracy somewhere as well, please report it to us.

This page might be updated in the future so check back!

Investing in the Industry: Break Out of Your Bubble

June 29, 2015 Even if you’re already working in alternative lending and know a lot about your particular area, the industry is growing by leaps and bounds and you might be feeling a little overwhelmed by the multitude of investment opportunities. Amid all the options, finding the right place to invest your money can feel as challenging as picking out the proverbial needle in a haystack.

Even if you’re already working in alternative lending and know a lot about your particular area, the industry is growing by leaps and bounds and you might be feeling a little overwhelmed by the multitude of investment opportunities. Amid all the options, finding the right place to invest your money can feel as challenging as picking out the proverbial needle in a haystack.

“Most people don’t know everything that’s out there. There are huge opportunities,” says Peter Renton, an investor and analyst who founded Lend Academy LLC of Denver, Colorado, a popular resource for the online lending industry.

Indeed, there are a growing number of online alternative lending sites that theoretically allow a person to invest in all shapes and sizes of loans. There are sites like Lending Club and Prosper that allow smaller investors to tap into the burgeoning P2P market. There are also a plethora of platforms that cater only to wealthier, more sophisticated investors in a host of areas like small business, real estate, student loans and consumer loans.

Even though there is a surplus of options, prudent investing is not quite as simple as depositing ample funds in an account and clicking the “go” button. Before you get started, you need to carefully consider factors such as your own finances and risk tolerance. You should also have a good handle on the specifics about the online platform—how it works, its history and track record, the types of investments it offers, the platform’s management team, technology and your ability to diversify based on available investment opportunities.

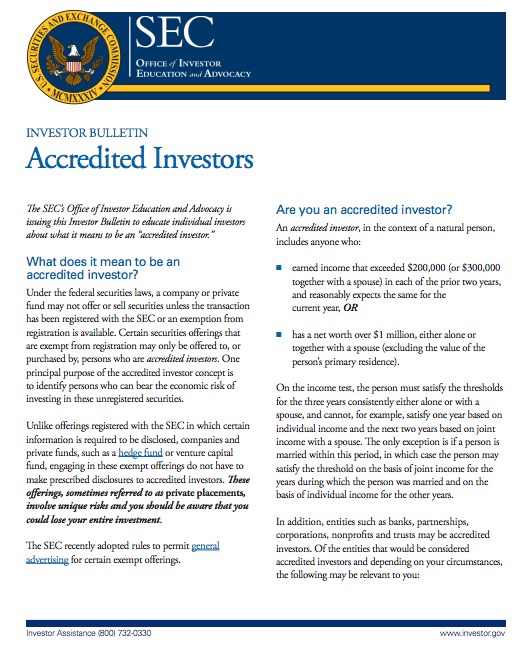

One of the first things you’ll have to think about as a potential investor is whether you have the financial wherewithal to be considered accredited by the SEC. If the answer’s yes, you’ll have a lot more choices of online marketplaces to choose from as well as types of investments. Basically, to meet the SEC’s threshold, you’ll need to have earned income that exceeded $200,000 (or $300,000 together with a spouse) in each of the prior two years, and reasonably expect to earn the same for the current year. Alternatively, you need to have a net worth over $1 million, either alone or together with a spouse (excluding the value of your home). (Check out the SEC’s website for more detailed info.)

If you don’t fit the definition of accredited investor, it’ll be more difficult for you to find out about all the investment possibilities that are on the market today. That’s because the platforms that cater to accredited investors aren’t allowed by SEC rules to solicit, so many online marketplaces are hesitant to say much of anything for fear their words will be misconstrued by regulators as an attempt to drum up new business. With limited exceptions, you won’t be able to get more than very basic information from and about these platforms’ unless you are accredited.

If you don’t fit the definition of accredited investor, it’ll be more difficult for you to find out about all the investment possibilities that are on the market today. That’s because the platforms that cater to accredited investors aren’t allowed by SEC rules to solicit, so many online marketplaces are hesitant to say much of anything for fear their words will be misconstrued by regulators as an attempt to drum up new business. With limited exceptions, you won’t be able to get more than very basic information from and about these platforms’ unless you are accredited.

But smaller investors do have options. Two San Francisco-based online lending platforms, Lending Club and Prosper, cater to individual investors, and you can still make a pretty penny plunking down money with these venues. You’ll also find a wealth of information about investing with them by perusing their websites as well as by reading the blog posts of media-savvy financiers.

“Right now, Lending Club and Prosper provide a great entry point for people who want to get involved in investing in alternative lending,” says Renton of Lend Academy.

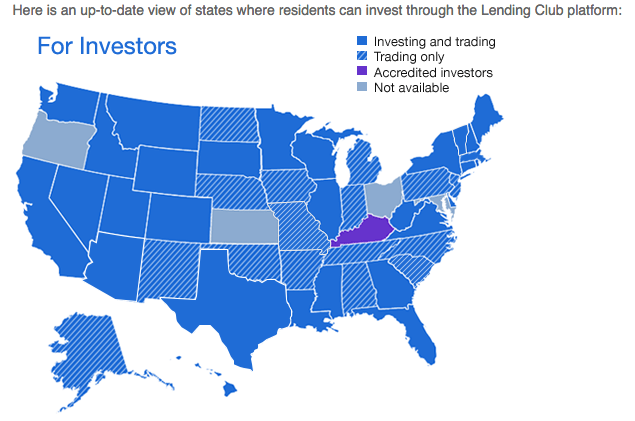

The caveat is that these platforms aren’t yet open to investors in every state, so if yours isn’t on the list you’re out of luck for now. However, with each marketplace you’ve got more than a 50 percent chance your state is on the approved list, so it’s worth digging deeper.

Assuming you meet their respective suitability requirements, you can choose to invest on one platform or both. To be sure, they are alike in many ways. Both allow you to invest with as little as $25 and fund one loan, however they recommend you buy at least 100 loans to be properly diversified, which you can do for as little as $2,500. You can manually choose which loans to buy, or enter your investment criteria so loan picking is automated. You can also invest retirement money in an IRA through Lending Club or Prosper.

There’s no fee to get started investing on either platform. For Lending Club, investors pay a service fee equal to 1 percent of the amount of payments received within 15 days of the payment due date. Prosper charges investors 1% per year on the outstanding balance of the loan. As the loan gets smaller, the servicing fee, which is charged monthly, gets smaller too.

To invest in Lending Club, in most cases you’ll need either $70,000 in income and a net worth of at least $70,000, or a net worth of at least $250,000. There may be other financial suitability requirements that vary slightly depending on the state you live in. For Prosper, individual investors must be United States residents who are 18 years of age or older and have a valid Social Security number.

At any given time, Lending Club has more than 1,000 loans visible on the platform and new ones get added every day, according to Scott Sanborn, chief operating officer and chief marketing officer. Prosper, meanwhile, on average has more than 200 loans for people to invest in, says Ron Suber, president.

Returns tend to be favorable compared with other fixed income investments—a major reason investing in online loans is becoming more desirable. Of course, actual returns will depend on what loans you invest in and the level of risk you take—typically the more risk you take on, the greater your potential return will be. At Lending Club, for instance, Grade-A loans have an adjusted net annualized return of 4.89%, compared with 9.11% for Grade-E loans, according to the company’s website.

Returns tend to be favorable compared with other fixed income investments—a major reason investing in online loans is becoming more desirable. Of course, actual returns will depend on what loans you invest in and the level of risk you take—typically the more risk you take on, the greater your potential return will be. At Lending Club, for instance, Grade-A loans have an adjusted net annualized return of 4.89%, compared with 9.11% for Grade-E loans, according to the company’s website.

To encourage more people to start investing, some savvy investors have started to self-publish online the quarterly returns they accumulate through the Lending Club and Prosper platforms. Renton, of Lend Academy, reported a balance of $476,769 on Dec. 31, 2014 and a real-world return for the trailing 12 months of 11.11 percent. Another well-known P2P investor and blogger, Simon Cunningham—the founder of LendingMemo Media in Seattle—reported a 12-month trailing return of 12.0 percent over the same time period, with a published account value of $41,496. Both investors say they expect returns to drop back somewhat over time, however, as the online marketplaces continue to lower interest rates to attract more borrowers.

Of course, if you’re an accredited investor, you will have access to even more online marketplaces. For instance, there’s SoFi of San Francisco for student loans, Realty Mogul of Los Angeles for real estate loans and Upstart of Palo Alto, California, that focuses on loans to people with thin or no credit history. The list of possibilities goes on and on.

Generally speaking, the more money you have to invest, the more options you have. “In this country today, you’ve got well over a hundred options if you’re willing to put seven figures in,” Renton says.

The minimums at venues that focus on accredited investors tend to be more than you’d find at Lending Club or Prosper. At SoFi, accredited investors need at least $10,000 to begin investing in the company’s unsecured corporate debt. SoFi’s been in the lending business for several years now and currently focuses on student loans, mortgages, personal loans and MBA loans. Investors, however, can’t currently invest in these loans, says Christina Kramlich, co-head of marketplace investments and investor relations at SoFi. The company plans to eventually offer investment opportunities in the areas of mortgages and personal loans, she says.

At Funding Circle USA in San Francisco, accredited investors can buy into a limited partnership fund for at least $250,000. Or they can buy pieces of small business loans for a minimum of $1,000 each, though the recommended minimum is $50,000, explains Albert Periu, head of capital markets. There may also be upper limits on your investment, based on your financials. If you’re part of the pick-and-choose marketplace, you’ll pay an annual servicing fee of 1%. With the fund, you’ll also pay an administration fee of 1%. Trailing 12-month net returns for investors are north of 10%, Periu says.

At Funding Circle USA in San Francisco, accredited investors can buy into a limited partnership fund for at least $250,000. Or they can buy pieces of small business loans for a minimum of $1,000 each, though the recommended minimum is $50,000, explains Albert Periu, head of capital markets. There may also be upper limits on your investment, based on your financials. If you’re part of the pick-and-choose marketplace, you’ll pay an annual servicing fee of 1%. With the fund, you’ll also pay an administration fee of 1%. Trailing 12-month net returns for investors are north of 10%, Periu says.

Because it’s still so new, it can be hard for investors to know how to compare marketplaces. For starters, consider the platform’s historical performance. There are a lot of new marketplaces popping up, but it takes time to develop a proven track record. This isn’t to say you shouldn’t dabble with the newer platforms, but if you do, you’ll want above-average returns to balance out the higher risk, says Sanborn of Lending Club. “About three years in, we started to build a track record. At five years in, it was very solid,” he says. “You need time to see how a basic batch of loans is going to perform.”

Before investing, you’ll want to get a sense of how committed senior management is to the company and try and get a sense of whether the company seems to have enough capital for the business to run well. Try to find out about the cash position of the company, how the loans are going to be serviced, what entity is doing the underwriting and how and where your cash will be held.

“It’s not just assessing the risk of the asset and the investment, it’s assessing the risk of the enterprise that is making it available to you,” Sanborn says.

It’s also important to ask questions about the loans themselves. Where do they come from and is the volume sustainable? Ideally, a platform should offer a variety of loans so investors can properly diversify, or you might need to consider investing with multiple platforms to achieve your desired balance.

Before you get started, you’ll also want to ask about the company’s compliance procedures and controls and how you can recover your money if you no longer want to invest. Data security is another area to explore. Not every company is as protective of customer data as perhaps they should be.

Before you get started, you’ll also want to ask about the company’s compliance procedures and controls and how you can recover your money if you no longer want to invest. Data security is another area to explore. Not every company is as protective of customer data as perhaps they should be.

When you’re asking all these questions, try to get a sense of how receptive the platform is to the feelers you’re putting out. Investors should only work with companies that are willing to be open about how they are investing your money, their historical returns and other important data. “I can’t stress transparency enough,” says Periu of Funding Circle.

The technology the platform uses is another key element. Is the technology easy to use, or does the platform create stumbling blocks for investors? Are there ways to automate lending, or do you have to log on every day and manually invest in loans?

Suber of Prosper says investors should also consider whether platforms work with a back-up servicer in case there’s a disruption and whether they run regular tests to make sure everything works as expected. “It’s just like a backup generator and you have to test it every once in a while and make sure it goes on.”

Certainly it pays to do your homework before you invest your hard-earned cash with an online platform. Ask around, attend industry conferences and absorb all you can from publicly available data. The good news is that there will probably be even more information for you to tap into as the industry continues to grow.

“Two years ago [marketplace lending] was very esoteric. A year ago it was still esoteric,” says Funding Circle’s Periu. Now, more and more investors are hearing about marketplace lending and want to make it part of their broader fixed income bucket. Even so, more has to happen for it to become a mainstream investment. “Awareness and education need to continue,” he says.

Once more people understand the extent of what’s out there, Suber of Prosper expects investing in online marketplaces will take off even more than it already has. “A lot of people still don’t know this as an investment opportunity,” he says.

Bless You, Fund Me: What Words Predict About Loan Performance

June 7, 2015 Way back in 2006 when I was just a baby merchant cash advance* underwriter, I encountered a book store that was borderline qualified. The final phone interview would make or break their approval so I grabbed my pen and paper and dialed their number.

Way back in 2006 when I was just a baby merchant cash advance* underwriter, I encountered a book store that was borderline qualified. The final phone interview would make or break their approval so I grabbed my pen and paper and dialed their number.

I went through the checklist of questions and they passed. But what really convinced me that it was a deal worth doing was the amount of times the owners made references to God. They were clearly religious people which indicated to me that they were probably also of high moral character. It didn’t matter what religion it was or if their beliefs aligned with mine, I was simply captivated by their values.

After approving the deal and funding them, they actually mailed me a handwritten letter to express their gratitude. It concluded with, “God Bless You!” and I hung it up on the wall of my cubicle to remind myself of the good I was doing for small businesses.

A few weeks later, the payments stopped. All of their contact numbers were disconnected and the owners of the store could not be located. They completely disappeared along with almost all of the money. Looking up at the note on my wall, a shiver went up my spine. Had I been duped? And did they use religion as a tool to influence my decision?

I thought that surely they must’ve encountered legitimate financial difficulty but I believed that even if so, people with their values would’ve been more forthcoming about it. Instead they just took the money and split and were never heard from again.

I learned a lesson about being emotionally influenced on a deal and it turns out there were clues this outcome might happen all along.

Bless you

In a study titled, When Words Sweat: Written Words Can Predict Loan Default, Columbia University professors Oded Netzer and Alain Lemaire, and University of Delaware professor Michal Herzenstein analyzed the text of more than 18,000 loan requests made on Prosper’s website. Applicants that used the word God were 2.2x more likely to default on their loans. And the phrase Bless you correlated higher on the default scale as well, though not as high as other non-religious words.

On the list of words more likely to be mentioned by defaulters are, I promise, please help, and give me a chance. Statistics actually show that someone promising to pay is less likely to pay than someone that doesn’t explicitly promise.

Among the other more common words likely to be mentioned by defaulters is hospital. This word holds special significance to me because in my last year as a sales rep, almost all of my underperforming accounts were supposedly due to the business owners or their family members being in the hospital.

Among the other more common words likely to be mentioned by defaulters is hospital. This word holds special significance to me because in my last year as a sales rep, almost all of my underperforming accounts were supposedly due to the business owners or their family members being in the hospital.

And it wasn’t just me. It seemed like every deal that was going bad in the office involved the hospital. Any time one of us was due to contact an account with an issue, we made bets that a hospital would come up in the story. (Seb, if you’re reading this, apparently it’s not a coincidence.)

I express no opinion regarding whether or not their stories were true, but statistics show that borrowers that mention hospital are more likely to default.

In the study’s Abstract, the professors wrote:

Using a naïve Bayes analysis and the LIWC dictionary of writing styles we find that those who default write about financial hardship and tend to discuss outside sources such as family, god and chance in their loan request, while those who pay in full express high financial literacy in the words they use. Further, we find that writing styles associated with extraversion, agreeableness and deception are correlated with default.

While the study focused on Prosper, their almost identical competitor, Lending Club, may have realized this trend earlier. In March 2014, Lending Club announced that investors would no longer be able to view the free-form writing portion of the borrower loan application. Citing “privacy reasons,” investors lost a valuable clue into the repayment probability of their notes.

But would it really have helped? The researchers wrote:

Using an ensemble learning algorithm we show that leveraging the textual information in loan requests improves our ability to predict loan default by 4-5.7% over the traditionally used financial information.

Nothing to see here folks, move along and approve

Curiously, Lending Club doesn’t want its investors to have access to a data point with such significant importance. Perhaps it’s because of disasters like this, where one borrower used the free-form writing section to spew profanities. Ironically, the loan was approved and issued anyway.

For tech-based platforms like Lending Club however, they noticed the “story” aspect of a loan had become less relevant because of overwhelming investor demand. Investors weren’t evaluating the written portion of the loan application as much anymore. According to their blog post at the time of the announcement, “Fewer than 3% of investors currently ask questions and only 13% of posted loans have answers provided by borrowers. Furthermore, loans are currently funding in as little as a few hours – well before borrower answers and descriptions can be reviewed and posted.”

It had become all algorithms and APIs where loans were fully funded by investors before the written portions could even be published on the website. Had anyone actually taken the time to read the above loan application answers, they probably wouldn’t have allocated money towards it.

But while removing the storyline from the data might give investors fewer methods to detect a good loan, it could actually protect them from getting drawn into a bad loan.

One of the authors of the above referenced study, Professor Michal Herzenstein of University of Delaware, found in 2011 that borrowers could manipulate lenders into not only approving them, but giving them more favorable terms.

You can trust me 😉

In a story that appeared on UD’s website in 2011, titled Good Storytelling May Trump Bad Credit, Herzenstein’s research discovered that borrowers who constructed a trustworthy picture of themselves “could lower their costs by almost 30 percent and saved about $375 in interest charges by using a trustworthy identity.”

The study referred to six possible categories or identities that borrowers would try to impress upon lenders to describe themselves (trustworthy, successful, economic hardship, hardworking, moral, religious). The story explains:

The more identities the borrowers constructed, the more likely lenders were to fund the loan and reduce the interest rate but the less likely the borrowers were to repay the loan – 29 percent of borrowers with four identities defaulted, where 24 percent with two identities and 12 percent with no identities defaulted.

It’s a case of measurable borrower manipulation.

“By analyzing the accounts borrowers give and the identities they construct, we can predict whether borrowers will pay back the loan above and beyond more objective factors like their credit history,” said Herzenstein. “In a sense, our results offer a method of assessing borrowers in ways that hark back to the earlier days of community banking when lenders knew their customers.”

Today’s tech-based lenders that are dead set on removing this human aspect from the equation may be taking a shortsighted approach after all as they evidently still struggle to make predictions with their numbers-only approach.

For example, a poster on the Lend Academy forum recently wrote this to me about early defaults in today’s algorithmic environment, “It would be nice if LC could predict who is going to default in the first few months of the loan and deny them, but I don’t think that is entirely possible.”

It reminded me of a big merchant cash advance deal I approved years back that passed all of the qualifying criteria with flying colors and still defaulted on the very first day. The merchant’s response to why he defaulted on day one? He felt like screwing us over… “Come sue me,” he said.

In a later meeting to review the deal’s paperwork, a group of managers agreed that I had done all I could to make the approval decision except one. I failed to account for the asshole factor.

Far from satire, it is not uncommon for financial companies to refer to an asshole factor in some regard. It’s a very subjective variable but it can make all the difference between an applicant that’s going to pay and one that’s not. Suddenly none of the hard data matters.

Is the applicant an asshole?

In a recent blog post by loan broker Ami Kassar, titled The Single Most Important Rule in Our Company, Kassar wrote, “if a customer, employee, or partner acts like a jerk – we don’t want to do business with them. If you want to be less diplomatic, you can call the rule – the no ###hole rule.”

In a recent blog post by loan broker Ami Kassar, titled The Single Most Important Rule in Our Company, Kassar wrote, “if a customer, employee, or partner acts like a jerk – we don’t want to do business with them. If you want to be less diplomatic, you can call the rule – the no ###hole rule.”

In many circumstances, the measure of someone being an asshole is relative to another person’s perception. There’s even an entire book on that subject if you’re interested. But what’s trickier, is that according to some studies, being an asshole is a positive thing in business. Would that also make them better borrowers statistically?

Referring back to the original cited study, one has to wonder if there might potentially be a list of words that more closely correlate with being an asshole. I don’t think anyone’s ever examined the Prosper data for that before.

You might not be able to quantify asshole-ishness from the text, but something as basic as a person’s pronouns can speak volumes about their personality or intentions. According to Professor James Pennebaker in the Harvard Business Review:

A person who’s lying tends to use “we” more or use sentences without a first-person pronoun at all. Instead of saying “I didn’t take your book,” a liar might say “That’s not the kind of thing that anyone with integrity would do.” People who are honest use exclusive words like “but” and “without” and negations such as “no,” “none,” and “never” much more frequently.

But saying “I” over “we” doesn’t necessarily make you less of a liar. Pennebaker discovered that depressed people use the word “I” much more often than emotionally stable people.

Being emotionally stable would probably make for a better borrower than a depressed one, but with all these influential and conflicting language clues, how can an underwriter possibly make the right choice?

For instance, if the following line appeared on the free-form writing portion of an application, how should it be interpreted?

Using all of the mentioned research as a guide, I’m inclined to consider the applicant a: trustworthy depressed lying asshole that’s not going to pay.

I = Depressed

We = Liar

God = 2.2x more likely to default

Have always been able to pay back = trustworthy

Hurry up and fund me = asshole

We could easily get caught up in the language here and ignore the obvious positives about this hypothetical applicant, such that they have an 800 FICO score and a solid six figure income. Shouldn’t that weigh more heavily? It’s easy to get distracted.

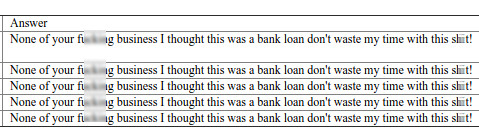

Perhaps Lending Club’s removal of the free-form writing section was for the investors’ own good. Even the borrower that repeatedly wrote, “None of your f**king business I thought this was a bank loan don’t waste my time with this sh**t!” is still current on all their payments after two and a half years.

To brokers like Kassar, the asshole factor is not so much about the likelihood of default anyway, but peace of mind. “Why invest emotional energy in putting up with shenanigan’s when there are so many good people who need our help,” he wrote.

Word is bond?

Regardless of what one study revealed about applicants that invoked God said about the likelihood of default, declining applicants on the basis of writing or talking about God could certainly be argued as religious discrimination. In many instances, religion is a protected class. Sometimes you have to ignore correlations because they can be deemed discriminatory.

One thing is for sure though, back in 2006 the upstanding characters I had created in my mind about the religious book store owners were upended when they disappeared into the night with all the money. Their words got in my head and I approved them perhaps because of it.

Years later, an asshole defaulted on the first day and not long after that, there would be a mysterious spate of accounts whose poor performance would be attributed to supposed hospital related events.

What’s buried in a person’s words? The answers allegedly. I promise…