Does Your Own Hunger Affect Lead Quality?

March 7, 2015 5 years ago in this very month, I funded 29 MCA deals for a total purchased amount of $608,000. 23 of those deals were renewals. It wasn’t my best month and it was also a different era. They were all split-processing accounts, not ACH. New deals could take six weeks to set up depending on the payment hardware. There was also no such thing as stacking then. The deals I was funding were from a good mix of warm leads, usually people who had filled out a form for financing somewhere online.

5 years ago in this very month, I funded 29 MCA deals for a total purchased amount of $608,000. 23 of those deals were renewals. It wasn’t my best month and it was also a different era. They were all split-processing accounts, not ACH. New deals could take six weeks to set up depending on the payment hardware. There was also no such thing as stacking then. The deals I was funding were from a good mix of warm leads, usually people who had filled out a form for financing somewhere online.

I didn’t always get warm leads. When I first started in sales in 2008, every rep got three or four actual leads a day. These were the golden geese, the Glengarry leads. The challenge was that they were sold to at least five ISOs at once so it was a race to get the merchant on the phone and establish a rapport with them first.

Caller number five was usually dead in the water. The least likable or least experienced of the remaining four would be cut by the merchant right away. That brought it down to 2 or 3 that the prospect would at least entertain.

None of these merchants had actually applied for a cash advance, but rather they had expressed an interest in business financing on a generic website and claimed that they accepted more than $5,000 in merchant account sales a month. Yet competing against four other companies to offer an expensive solution the merchant had never heard of was as good as the leads could possibly get. And if I started the day at 9 AM, then odds were I’d have made all 3 calls by 9:30.

I didn’t get paid a base salary so I couldn’t fake my way through the rest of the day. The remaining 9 hours were UCC lists and follow up calls with leads from previous days. I can’t imagine calling a UCC now in the age where stacking exists. The only option back then was to satisfy their outstanding advance in full with the proceeds of the new one.

Hi, my name is Sean Murray with ____________ and I’m calling about the advance you have with _____________. I know that company’s products can be awfully expensive and I was wondering if you were open to the opportunity of a lower holdback percentage, lower dollar for dollar cost of capital, and some additional money in your pocket.

I was notorious for cutting points off my upfront commission to get deals done. Sometimes I’d make nothing on the upfront commission but at least I’d get a new merchant account out of it and a backend cash residual. My residuals grew really fast.

Fast forward to 2011, I didn’t want to call UCCs anymore. I wanted the warmest leads possible. I was losing my edge on how to even approach UCCs because I had become so adjusted to higher quality material. I felt I had earned my way past them or that UCCs no longer offered the same value they once did.

So it was enlightening when I watched a junior account rep fresh out of college bring in more than 20 applications in his first week just from UCCs. Few funded, but I was impressed by his ability to engage prospects and bring in paperwork on leads I considered to now be crap.

He was hungry. He was new. He also realized that if he couldn’t bring in applications, that he’d be fired pretty quickly. He didn’t have the luxury of telling management that the leads sucked and to give him something else. This was all he would be given.

Watching him brought me back to my first few months as an underwriter in 2006 when there were very few MCA ISOs in existence. One day when deal flow was very slow, I was given a binder full of names and phone numbers of business owners who had applied for a mortgage in the past few years. The boss told me to “underwrite these files.” I learned immediately that all I was doing was cold calling random businesses. As a brand new hire, I was scared that if I didn’t “underwrite” them that I would be fired. So I started calling them with an offer to buy their future credit card receivables (the Merchant Cash Advance term was not widely adopted yet).

I got in applications and statements, I underwrote them, and then if approved, converted their merchant processing accounts and funded them. I didn’t get a commission because I was a salaried underwriter. All I hoped was that enough would fund (and not default) that I would be able to keep my job.

Eventually I was on a team where it was the responsibility of the underwriters to pitch the merchant on the product, gather the docs, close them on terms, underwrite the file, and fund it. The ISOs would just send us a lead and make 8-10 points if we somehow turned it into a funded deal. A few ISOs were sending us pure garbage, random names and phone numbers (literally a first name with no last name and a phone # of a non-lead) and passing them off as leads to see if our underwriting team could turn them into deals that they’d get paid on. Some were shocked when they heard we funded them. Others were mad that we weren’t funding enough.

As the company grew and the industry expanded, It eventually became normal to receive an application, 4 months merchant statements, 4 months bank statements, lease, voided check and a driver’s license and communicate with an ISO who did almost all of the legwork. All I had to do was underwrite the deal. When someone would submit much less, I got frustrated that I even had to look at it. My job was to underwrite files, not make half promises to ISOs based off of very little information. With so many completed files being submitted every day, I began to look at incomplete files differently. The fear that I would lose my job wasn’t there because I was already approving millions per month.

Fear was a huge motivator for me, especially in sales where I had no base pay. You either turned shit into gold or you lost.

It’s amusing to see how opinions vary today around the industry. Some ISOs still swear by UCCs, some stopped bothering with them years ago. Some say mailers are great. Others say they have tried them and they were terrible. Press 1s are the worst or Press 1s get deals funded. Web leads bring in too many annoying startups or web leads are the only type of leads that work.

What sucks and what doesn’t is undoubtedly affected by your attitude. If you’re used to the Glengarrys, then how patient will you be for what veterans consider to be junk?

In the upcoming March/April magazine issue that will be mailed out at the end of this month, I interviewed a 25-year old sales rep who had much more on the line than the fear of just losing his job. He became very successful after just a few years of cold calling.

For anyone out there who has bought leads only to bash them afterwards, was it really because they were bad? Or was it because you weren’t hungry enough?

It makes all the difference.

Advice to New Loan Brokers, ISOs, and Funders

February 24, 2015 Some words of wisdom to avoid having a bad experience in this industry:

Some words of wisdom to avoid having a bad experience in this industry:

1. If you can’t afford a lawyer, don’t be a funder. This is a litigious business and despite the myth that commercial financing is unregulated, there are plenty of ancillary laws to adhere to. States, FTC, OCC, IRS, etc.

2. Have a lawyer review your contracts (merchant agreements, ISO agreements, syndication agreements, etc.) If you can’t afford one or don’t want to take the time to do it, this business might not be for you.

3. Don’t send your deal to someone with a free email address (yahoo, gmail, hotmail, etc.).

4. Don’t send your deal to some random company just because they posted something on a forum, LinkedIn, or somewhere else. Check them out on Google, ask other forum members to vouch for them. Be extremely smart and overly diligent about it.

5. This is not a get rich quick business or industry. You can lose money funding and syndicating. You can technically also lose money brokering on commission clawbacks for deals that go bad right away.

6. Leads are expensive. Do not launch an ISO with only 2 grand in the bank.

7. Learn to generate your own leads and you will save yourself a lot of stress down the road.

8. A wise man once told me it is better to build a book of business and a long lasting passive income than to grind it out for a quick buck month after month. What’s your strategy?

9. You will lose deals, commissions, arguments, and occasionally your mind. Accept your losses when they happen and focus on the next deal.

10. Use appropriate language. A company that buys future revenues is not a lender and their financial transactions are not loans. Loans have noticeable things like interest rates and fixed terms. Make sure you know which one you’re talking about at any given time.

More Red for OnDeck (ONDK)

February 24, 2015 Back in the red?

Back in the red?

It looked like the tide had finally turned. After 8 years and just in time for their IPO, OnDeck had pulled off their first quarterly profit, a meager amount of $354,000. But it was a start right? After their debut on the NYSE, the price swung heavily from a high of $28.98 to a low of $14.52. It closed at $19.37 right before the report was released.

OnDeck reported a $4.3 million loss for the 4th quarter and an $18.7 million loss for the year. Despite this, their margins are definitely improving.

The company issued $369 million in loans last quarter, bringing the 2014 total to $1.2 billion. Sales and marketing expenses doubled in 2014 over the prior year with CEO Noah Breslow and CFO Howard Katzenberg acknowledging on the call they’ve made a big go at TV and radio advertising.

Competition? What competition?

Noticeably, the average APR of loans originated in the fourth quarter was 51.2%, down from over 60% in Q4 of 2013.

One analyst asked if competitive pressures were leading to the reduction in interest rates but Breslow said that wasn’t the case. If anything their closing rate or “booking rate” has been improving and rates coming down is an initiative they’ve taken up on their own. Merchants are actually shopping less according to them.

“Overall this market is still characterized by extreme fragmentation,” Breslow said. “The behavior that we see with our customers is that they might research other competitive options online but then when they actually apply to OnDeck and receive that offer, they kind of have this bird in hand dynamic, and there’s so much search cost associated with going out and looking at other places and so much uncertainty around that, they typically just take that offer that OnDeck has provided to them.”

With their cost of capital down, closing rate up, and defaults steady, a net loss should arguably be a tough pill to swallow. In response to a question about potential regulatory threats, Breslow said there wasn’t really anything on the horizon.

With their cost of capital down, closing rate up, and defaults steady, a net loss should arguably be a tough pill to swallow. In response to a question about potential regulatory threats, Breslow said there wasn’t really anything on the horizon.

So was it just a weird quarter? Under Guidance for First Quarter 2015 and Full Year 2015 in their quarterly report, they suggest another long year of losses ahead.

To infinity and beyond!

The economic and regulatory environments couldn’t be any more favorable to a company that now has almost a decade worth of data under its belt. But unfettered growth still seems to be the number one priority on the agenda. Breslow and Katzenberg spoke optimistically about their recent entry in the Canadian market and the potential to set up shop in other countries. As for the OnDeck Marketplace… surprisingly they claimed its only real purpose is to diversify their funding sources. They are not aiming to become a marketplace but rather they view the OnDeck Marketplace as just one of many vehicles to sell off loans.

So when does the profit part come in? None of the analysts on the line asked about profit. They mostly all offered their congratulations on a “great quarter”. Coincidentally they were almost all from companies that originally underwrote their stock offering.

Six months ago I wrote that OnDeck’s lack of profits has been intentional. In An Insider’s Perspective, I wrote, “What scares their competitors though, is that this strategy has been intentional. Very few if any players in the industry have had the luxury, guts, or the purse to lose money for seven years as part of a coup to conquer the market.” Nothing has changed.

As long as they have cash in the bank, they’re going to keep pursuing growth. They had $220 million in cash and cash equivalents as of December 31st. So for now that means continuing to turn up the marketing heat to increase volume domestically while planting seeds in other markets like Canada.

But the question remains, at what point does profitability become important? Sure it’s tempting to be lending $2 billion or $3 billion a year instead of the $1.2 billion size they’re at now because it would mean they’ll be that much bigger right? Heck, maybe they can be a $10 billion a year lender. But if they are running in the red at a moment where their cost of capital is low, the credit markets are liquid, the economy is favorable, regulatory threats are nil, defaults are static, there is supposedly no competition, and their margins are at their peak, then what happens when one or two of those things change? What if all those things change at once?

But the question remains, at what point does profitability become important? Sure it’s tempting to be lending $2 billion or $3 billion a year instead of the $1.2 billion size they’re at now because it would mean they’ll be that much bigger right? Heck, maybe they can be a $10 billion a year lender. But if they are running in the red at a moment where their cost of capital is low, the credit markets are liquid, the economy is favorable, regulatory threats are nil, defaults are static, there is supposedly no competition, and their margins are at their peak, then what happens when one or two of those things change? What if all those things change at once?

Those rates are too high low

OnDeck’s price jumped in afterhours trading. The market is chalking up the results as a positive. It’s just another losing quarter in a long line of losing quarters for OnDeck and they’ve promised more of the same in the year ahead. Nothing to see here folks, business as usual.

OnDeck may have made it easier for small businesses to get a loan, but they have yet to prove since 2006 if their methodology can actually make money. That should be a wake up call to critics that complain their interest rates are too high.

It is quite possible that their interest rates are actually too low. At an average of 51.2% APR, that’s a heck of a theory to consider.

But it looks like it’s true.

Shark Tank, The Profit and Kitchen Nightmares

January 29, 2015 What do Shark Tank, The Profit and Kitchen Nightmares have in common? They’ve all featured merchants who’ve used merchant cash advances. Statistically it’d have to happen but there’s nothing more wild than watching Marcus Lemonis try to save a failing business I actually declined for funding.

What do Shark Tank, The Profit and Kitchen Nightmares have in common? They’ve all featured merchants who’ve used merchant cash advances. Statistically it’d have to happen but there’s nothing more wild than watching Marcus Lemonis try to save a failing business I actually declined for funding.

One deal I personally worked on has appeared on The Profit and there were a couple others that I’ve seen shopped around in the MCA space. Not sure if that restaurant on Kitchen Nightmares has used merchant cash advances? Just conduct a UCC search and find out!

No amount of underwriting could ever give you the perspective you get on TV. In between the lines of a business wanting help is usually a disaster or series of disasters that has the business on edge; All the employees are about to quit, the landlord wants them out, their vendors are mad at them, the owner’s an intolerable jerk, they don’t know how to market themselves, or the customer experience is horrible. It’s always something.

At least on Shark Tank the only thing scrutinized is the presentation of the product and the viability of it. On The Profit and Kitchen Nightmares, all the secrets are laid bare.

On the one hand it’s a glimpse into the struggles of running a small business, an experience I know firsthand from growing up working at two family owned restaurants. On the other hand, it’s a sobering reminder that there is so much risk in lending them money.

On The Profit, Lemonis hedges his risk by typically taking 50% (OR MORE!) equity in return. His famous pitch to these merchants who always come across as shocked is that, “I’m not a bank. I’m not a consultant. And I’m not the fairy godmother.”

"I'm not a bank. I'm not a consultant. And I'm not the fairy godmother." –@MarcusLemonis #theprofit https://t.co/sIUH2Tj21p

— CNBC's The Profit (@TheProfitCNBC) November 18, 2014

Deals go bad

And even that approach carries risk. Early last year on the show, Lemonis wired $190,000 to Brooklyn-based business A. Stein Meat in return for 100% of their Brooklyn Burger Brand. The business used the cash to make payroll and reneged on the transfer of the burger brand, claiming they thought the money was a loan. They never made any payments back on it.

Lemonis filed suit against them in the United States District Court for the Eastern District of New York which opens by stating:

This is an action to enforce the straightforward, bargained-for agreement entered into by and between defendant Stein Meats and Lemonis, by which Stein Meats agreed to sell its “Brooklyn Burgers” brand of hamburgers to Lemonis. The agreement is unequivocal, and was witnessed by the millions of viewers who have watched Episode 2 of the second season of the CNBC reality television series “The Profit” that first aired on March 4, 2014.

However unequivocal it may have appeared, the case is still going. A peek at the court records show bitter and unrelenting litigation. At the time of filming, Stein Meats was only 2 weeks away from bankruptcy and was reportedly sold to its competitor, King Solomon. King Solomon is also named as a defendant.

The Brooklyn Burger brand is still in use as I enjoyed one of their tasty burgers at a Nets game last month.

Wait, don’t I know this deal?

In another episode of The Profit, the owner of a business I declined for a merchant cash advance is fingered as a bad guy. He was unrepentant, suggesting that the bridges burned, lives ruined, and debts defaulted on along the way were worth it to get the business to where it was now. I distinctly recall being shocked by their mountain of debt, which became the reason I declined it. Their debt problems were even highlighted on the show!

I had the luxury of examining their Balance Sheet since their request was sizable. Had the request been smaller, it wouldn’t have been required. Thankfully they were transparent about their debt. Of the thousands of applications I’ve underwritten in my day, I learned that it is incredibly hard for a small business to supply a financial statement, and of the ones I got, it was difficult to ascertain their accuracy. I’ve seen Balance Sheets that didn’t balance, numbers that were completely illogical, or statements that were missing major line items.

I see only two ways to approach something like this. It’s either a decline or it’s going to be expensive. I don’t care what my algorithms say their social media score indicates. If the business doesn’t keep good books then I have no idea what I’m exposing myself to.

The real world’s not so bad after all

I can’t help but notice that one of the best guys in the small business space takes a similar no-nonsense approach. You give Lemonis half of your business or he walks. Being on the show might boost sales but taking his money is not charity.

The only difference I’ve discovered between business financing deals made in real life and ones made on TV is that the ones on TV are more expensive. It’s the opposite of what you might expect.

If Lemonis thought his agreement witnessed by millions of people was unequivocal, then shouldn’t an online lender who has never met their client, nor visited their business, feel slightly less comfortable about their agreements?

I would think so.

Inc reports that Lemonis spends eight full days with each business but on twitter he claims it’s much more than that.

“@DominoTheGreat: how long do you film each show for? Few days, week? Does it vary from show? #asktheprofit #TheProfit” couple months

— Marcus Lemonis (@marcuslemonis) October 15, 2014

During filming, Lemonis can be seen going through the financial statements, interviewing employees, negotiating deals with vendors, trying out the products, and scrubbing toilets. With that experience and knowledge under his belt, he presents his cold hard deal, money for a massive equity stake. The terms are aggressive but he’s steadfast in his role as a businessman and not a fairy godmother.

Contrast that experience with a merchant cash advance company that has almost nothing to go off of by comparison; a few bank statements, a credit report, and maybe some online data points. With only this, they’re supposed to wire out $5,000, $50,000 or $150,000 to a business across the country and get no equity in return.

The two things that I’ve learned from these celebrity businessmen is that their underwriting is more personal and they manage to be even more expensive. They promise their expertise is what makes up the difference.

I’d love to say that every situation is different but it’s gotten to the point that we’re working on the exact same deals. If a merchant can get a better deal off TV than on it, I’d say things are pretty good right now.

Mayor Rahm Emanuel Declares War on Merchant Cash Advance

January 16, 2015 FOX 32 in Chicago is reporting that Mayor Rahm Emanuel is going on the offensive against merchant cash advance companies. Specifically it says,

FOX 32 in Chicago is reporting that Mayor Rahm Emanuel is going on the offensive against merchant cash advance companies. Specifically it says,

Mayor Rahm Emanuel will call on state and federal agencies to regulate business to business lenders. Emanuel said cash advance companies have accelerated their marketing efforts in recent months, resulting in small businesses taking loans they cannot afford.

The article states that business owners have turned to the City of Chicago for help in paying back loans with high rates of interest.

While the mention of APRs reaching into the ranges of triple digits is supposed to shock you, one business lender that charges such rates recently went public and had been backed by Google Ventures, Fortress Investment Group, Goldman Sachs, and Peter Thiel.

Less than 30 days ago we were celebrating these companies as the solution to a problem that has plagued small businesses for all time, access to capital.

While Emanuel is obviously famous for being the 23rd White House Chief of Staff and Obama’s right hand man for a period in his first term, he is not the first mayor to consider the role merchant cash advance companies and high interest business lenders have in cities across America.

All the way back in 2008, the U.S. Conference of Mayors (USCM) adopted a resolution titled, Protecting Main Street Small Business Owners from Predatory Lenders, from which some of the excerpts below are from:

WHEREAS, merchant cash advance companies have already lent approximately $2 billion at egregious rates and have been quoted in leading main stream media publications such as Forbes, Business Week, Dallas Morning News, and American Banker claiming that their new originations have increased 75% in the first half of 2008

WHEREAS, as with payday lenders and predatory lenders in the home mortgage community, Mayors need to take a leadership role to scrutinize predatory merchant cash advance companies, educate small business owners of the dangers posed by these firms, and increase awareness and promotion of alternative, more affordable funding sources to support this vital segment of our economy

BE IT FURTHER RESOLVED, that to protect the general health and viability of their small business communities, cities should investigate whether they can effectively regulate or ban merchant cash advances.

3 months after this resolution was passed, Lehman Brother’s collapsed and the economic crisis was in full swing.

According to a few industry leaders familiar with the 2008 mayoral resolution, UCSM privately retreated from their stance when all other types of commercial lending had dried up. Their seeming reversal, though not publicly stated invited merchant cash advance companies into their communities at the moment when Main Street was arguably at its weakest.

According to a few industry leaders familiar with the 2008 mayoral resolution, UCSM privately retreated from their stance when all other types of commercial lending had dried up. Their seeming reversal, though not publicly stated invited merchant cash advance companies into their communities at the moment when Main Street was arguably at its weakest.

Who do they think rolled up their sleeves and kept local economies alive when things were at their worst?

While non-bank funding can obviously be expensive, countless business owners have praised merchant cash advances in particular as a solution that came through when none other were available.

Emanuel will learn that companies such as Square and PayPal are part of the crowd that provides merchant cash advances. This is not a shadow industry. Non-bank business-to-business financing is already becoming less expensive nationwide.

According to Fox, the Commissioner of the Chicago Department of Business Affairs and Consumer Protection said the goal is to offer small business owners loans at affordable rates with full disclosure.

Merchant cash advance companies would undoubtedly feel the same way. The dilemma is that advocates of affordable rates tend to really mean single digit rates. When single digit rates are not possible given the risk, they seem to argue that no financing should be given at all, leaving the business to fail or miss out on an opportunity. That’s the exact type of flawed thinking alternative financing companies address…

Ironically, a report from the Federal Reserve Bank of Cleveland last week concludes that small business job creation is lagging with a possible culprit being a lack of access to credit.

Coming out of the most recent recession, however, job creation by small businesses has lagged, and the new business formation rate continues to fall. While it is not clear that these trends are driven by weaker borrowing or limited access to loans, it is evident that businesses need adequate credit to succeed and grow. As such, policy makers should not lose sight of the trends related to small business credit, even with the recent positive reports showing improvements.

And of course in a supposed exposé on merchant cash advances that aired on Chicago Public Radio in November, clips of an interview I did with them were aired to fit the narrative of merchant cash advance as predatory. When asked by the interviewer what a small business owner should do if they didn’t understand a contract, I advised that they hire an attorney or an accountant, and if they couldn’t afford those then to find somebody they felt qualified to offer an opinion. “They should always get a 2nd set of eyes to review a contract if they don’t understand,” I said.

My advice did not air, nor did my explanation that there were two separate types of products that they were confusing as one, one being loans and the other being purchases of future receivables. I suppose it didn’t fit the characterization they were going for.

As quoted in Fox, Financial Advisor Kent Travis advised business owners to “read the documents, don’t sign anything on the spot, make sure you read it thoroughly and if you have trouble understanding it seek the advice of an advisor, CPA, an attorney or a financial planner.”

I couldn’t have said it better myself because I already did.

And in an interview I had with former Congressman Barney Frank, a chief architect of the Dodd-Frank Wall Street Reform and Consumer Protection Act, Frank voiced his opposition to regulations on business-to-business lending in early 2014.

There’s one thing the Fox story does mention that’s hard to argue with and that’s the need for greater transparency. I am all in favor of that.

—————–

For those that haven’t already signed up, this is a reminder that the Law Office of Pepper Hamilton LP is hosting a lunch at their office in New York on January 27th to specifically discuss the merchant cash advance industry’s future.

Interested in discussing legal issues, best practices, and the path forward for alternative business financing? Are you an ISO or funder interested in sharing your thoughts? Send me an email to let me you know if you’d like to attend. sean@debanked.com.

—-

Watch the Fox news report about merchant cash advances:

Recording Merchant Cash Advance Transactions

January 13, 2015This is question #3 and #4 in an interview between AltFinanceDaily’s Sean Murray and accountants Yoel Wagschal, CPA and Christina Joy Tharp.

- 1. Merchant Cash Advance How to Guide Intro

- 2. Do I Need a Special MCA Accountant?

- 5. Merchant Cash Advance Accounting Pitfalls

- 6. Revenue recognition for Merchant Cash Advance

- 7. Q&A – Real questions that MCA companies or syndicators have

Q: ISOs and funders are often asked by their clients or their accountants how to record selling their future sales on their taxes. Should merchants just record it as a loan?

A: No, No, No, and absolutely NO. “Loan” is a dangerous word. MCA’s do not handle loans because if these cash advances were loans then you could not charge such a high percentages. These percentages on “loans” would be against usury laws. Never, ever, use the word “loan”. Take it off of your websites. Take it off your business letters. Remove “loan” from your vocabulary entirely. The funder is buying and the merchant is selling “future sales”.

Q: How should a funder record buying future sales from a GAAP perspective? From an IRS tax perspective?

A:The IRS does not have any special provisions for the MCA industry so follow GAAP. If you have a departure from GAAP for tax purposes, it is the same as in any other industry.

Here is the typical debit and credit entry for most every normal sale:

The company pays for product XYZ with 1,000 USD:

| Account | Debit | Credit |

| Inventory/Purchases | 1,000 | |

| Cash | 1,000 |

The company sells product XYZ and collects 1,500 USD:

| Account | Debit | Credit |

| Cash | 1,500 | |

| Sales | 1,500 |

Very simple. Here you have a profit of 500 USD and this is what you see in your bank account. If the 500 USD is not in the bank it could be for various reasons which is why you need to reconcile.

Of course, there is much more to the merchant cash advance business than these simple transactions but we want to stay focused on this for a little while.

Now remember the business model of the supermarket? Every day the supermarket does thousands of orders and each order has dozens of items. We have to do the accounting for all of those transactions in order to reconcile the proper balances with the inventory. If done manually, we would need an entire staff of accounting clerks just to do those transaction entries.

That’s why everyone in the retail industry understands that they need a good point of sale (POS) system in order to record the information. What do you think the accountant does? The accountant prints out a report at the end of the day/week/month and from that report the accountant creates one entry in the general ledger showing the summary of the day.

I.E.: The summary tells the accountant that registers have rung up the total of 300,000 USD in sales of which 280,000 USD was paid in cash and 20,000 USD was paid on credit.

| Account | Debit | Credit |

| Cash | 280,000 | |

| A/R | 20,000 | |

| Sales | 300,000 |

The idea is that you can sell as many items as you want in a single period but that your accountant should not have more than one transaction to post to the general ledger.

When you want to micro manage you look at the point of sale system. How do you know that the POS system is correct? What is the end goal? Where does the buck stop? Yes, the buck stops in your bank!

If the POS summary is being put in the general ledger, and the general ledger is matching up with the money in your bank – BINGO! If it doesn’t match – TROUBLE!

With this simple transaction in mind we see that the MCA industry has two big challenges:

1) Finding the right management software

2) Finding an accountant who really understands how to reflect these numbers in the general ledger

Unlike in a regular retail business (where you sell a product for money) the product that you are selling here actually is underlying money. It is not a loan, but a purchase of future sales. As this is the case, your bank account becomes the point of sale system. However, a bank typically doesn’t have point of sale capabilities when it comes to reporting and accounting.

To successfully track every cent of your transactions a good cash advance company must have excellent management software. The software must provide a mirror image of the transactions in your bank accounts.

The only way you can do that is if you have one bank account designated to handle only transactions that are reflected in the management software. If you decide to pay a phone bill from this “software transaction only” account, it will be just like a supermarket owner that takes a 100 bill from a cash register in order to pay the store’s phone bill.

Once you establish the “software transactions only” account, (and you have an accountant who can record the summaries into the general ledger while understanding how the general ledger ties into the bank account) then and only then will you be in good shape.

The understanding of the cash advance accounting journal entries can be very confusing if you don’t understand the small steps that make up the big picture. Research reveals sparse results. As that is the case, I will only illustrate a basic example (with no fees).

Please keep in mind that each MCA has different ways of doing some things. This example will cover the basic standards but for modifications and special needs, you will need to find an accountant that understands the eccentricities of your own company’s business model.

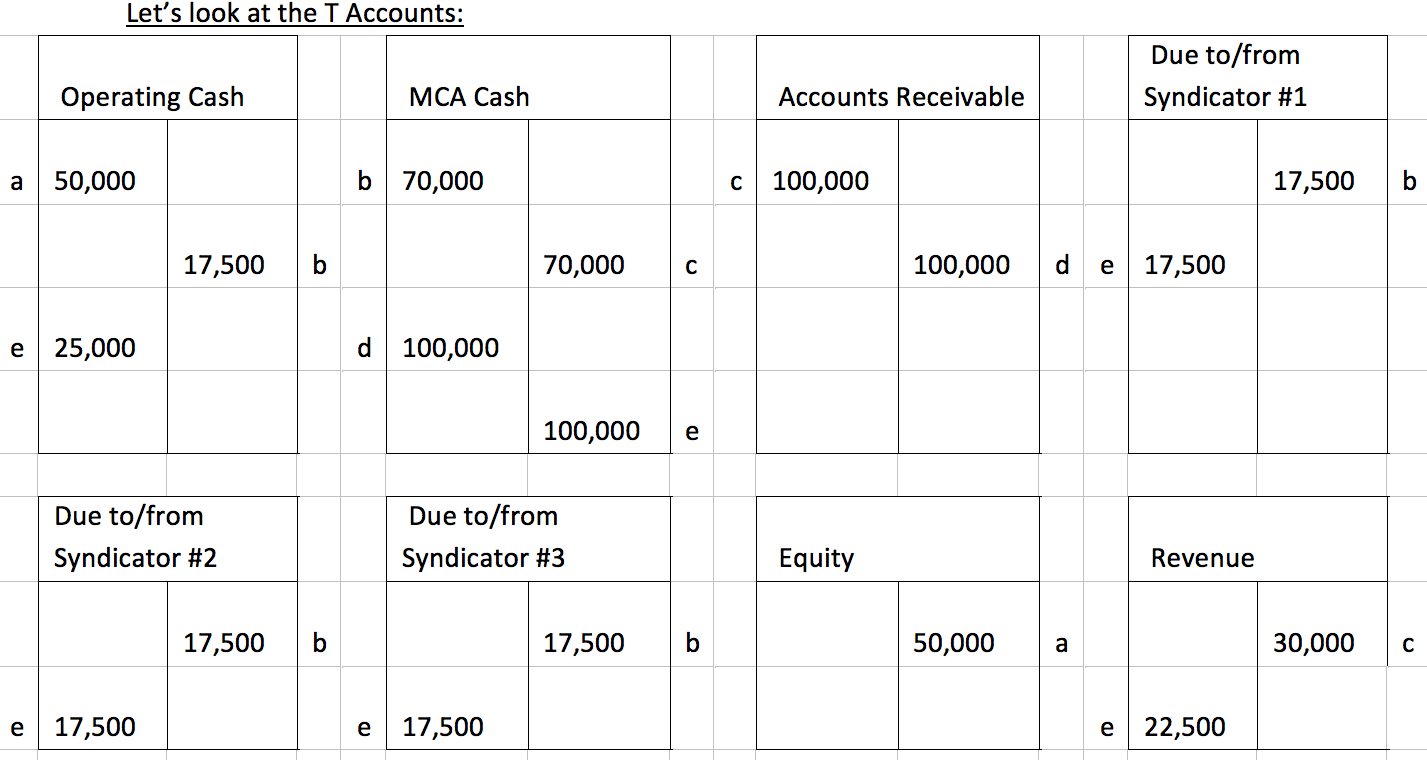

Our MCA model starts with the formation of a small fictional cash advance business. We will start this MCA business with 50,000 USD seed money and we make contact with three investors who we will refer to as syndicators. Yes, I know that some of you reading this call these investors or syndicators by different names, which is part of the confusion out there. To avoid further expatiation, we will use only the term “syndicator” in this article.

On day one “ABC merchant” wants to sell 100,000 USD of their future sales to our MCA business for the discounted rate of 70,000 USD. We reach out to the aforementioned syndicators. They agree to contribute 25% each.

Future sales will be scheduled in terms of 1,000 USD per day for the next 100 days

We are going to have 30,000 USD in profit and it is going to be split among 4 people, each receiving 7,500 USD.

Now we will give it some familiar terms:

Funding amount = 70,000

Payback amount = 100,000

Daily ACH = 1,000

| Account | Debit | Credit |

| Operating Cash | 50,000 | |

| Equity | 50,000 |

| Account | Debit | Credit |

| MCA Cash | 70,000 | |

| Due to/from Syndicator #1 | 17,500 | |

| Due to/from Syndicator #2 | 17,500 | |

| Due to/from Syndicator #3 | 17,500 | |

| Operating Cash | 17,500 |

| Account | Debit | Credit |

| Accounts receivable | 100,000 | |

| MCA Cash | 70,000 | |

| Revenue | 30,000 |

| Account | Debit | Credit |

| MCA Cash | 1,000 | |

| Accounts Receivable | 1,000 |

Although the next step depends on when a MCA company repays its syndicator investments, we will assume the syndicators are all paid at once to allow for a simple transaction example. There is a credit to cash and debits to the syndicator accounts for the principal and the revenue account or an offset account for their share of the profit. The share that I have to split with syndicators wasn’t really my own revenue in the first place.

Multiply this transaction for the number of days (in our example, 100 days). The net effect on this particular transaction will look similar to this:

| Account | Debit | Credit |

| Due to/from Syndicator 1 | 17,500 | |

| Due to/from Syndicator 2 | 17,500 | |

| Due to/from Syndicator 3 | 17,500 | |

| Revenue | 22,500 | |

| Operating Cash | 25,000 | |

| MCA Cash | 100,000 |

| Cash | 57,500 |

| Total Assets | 57,500 |

| Equity | 57,500 |

| Revenue | 7,500 |

After you examine all of the transactions, you’ll see that the chips fall in the right places. We started out with 50,000 USD and received profit from our 25% participated in a merchant funding deal. That deal ended with total revenue of 7,500 USD. It’s all there!

If you truly understand these transactions and you have the proper system in place, then this process should be very easy to follow (even if each of these transactions happens a million times a day).

However, if you don’t understand then you should be very careful because only proper accounting measures can save you from losing tens of thousands or even hundreds of thousands of dollars without ever knowing it. Unfortunately, I have seen it happen with my own eyes. Just like the grocery store example above, the sale of money to MCAs is just like the sale of tomatoes is to grocery stores. If left unaccounted for, those tomatoes could go missing without the store owner even noticing. Don’t let that be you with your money!

Phone (845) 875-6030

Fax (845) 678-3574

Email: cjt@ywcpa.com

http://ywcpa.com

Please consult with an accountant to assess your particular situation and needs.

Merchant Cash Advance Accounting – A How To Guide

January 13, 2015This is the introduction and first question in an interview between AltFinanceDaily’s Sean Murray and accountants Yoel Wagschal, CPA and Christina Joy Tharp.

- 2. Do I Need a Special MCA Accountant?

- 3. and 4. Recording Merchant Cash Advance Transactions on the Books

- 5. Merchant Cash Advance Accounting Pitfalls

- 6. Revenue recognition for Merchant Cash Advance

- 7. Q&A – Real questions that MCA companies or syndicators have

Funding small businesses is the easy part of merchant cash advance. Anyone can fund. It’s what comes after that’s tricky and I don’t just mean capturing those receivables you’ve purchased, but also recording everything in such a way that you’re not scrambling around tax time.

I have a B.S. in Accounting but I asked the experts Yoel Wagschal, CPA and Christina Tharp his staff accountant for their insight on managing the books for a merchant cash advance company. We’re still a ways off from April 15th so now is your opportunity to fix whatever you might not have done in 2014 and start off on the right foot for this year. Thanks again to Yoel and Christina for answering these questions.

Q: As a funder, what systems should I have in place to make sure I can:

a. Prepare business tax filing

b. Be ready for an audit to raise capital

c. Know whether or not I am making money

A: First of all you have to understand that every type of business has this exact same question. The answer is that you need to have proper accounting entries and records which will then aid you in creating the financial statements (ie: balance sheet, income statement, statement of retained earnings, and statement of cash flows).

Whether it is a tax filing, a bank audit, or an internal inquiry, the solution is identical because all of those situations require the same financial material in order to answer them. In order to prepare a business tax filing a company must provide its profits and losses. That is the same information provided in an audit to raise capital and it is the same information a business owner needs to see how much money they are making (or losing!).

The exact system is obviously custom fit to your individual business model but it should follow these very basic steps:

i) Think the entire process through from cradle to grave

ii) Be sure to codify where funds are coming in from:

a. Investments from syndicators

b. Payments from merchants

c. Commissions

iii) Be sure to codify where funds are being sent to:

a. Funds to merchants

b. Funds to syndicators

c. Commissions

iv) Be sure there is a system of checks and balances which will alert you to the following common errors:

a. Funds not received from/sent to syndicator

b. Funds not received from/sent to merchant

c. Commissions not received

v) The bank account is the authority while the system is only a representation:

a. Your system balance should reconcile with your bank account

b. It is advisable to have a separate bank account for funding transactions

You will also want to pull up trial balances and earnings reports, which must be input correctly from the very beginning in order for these reports to be accurate and effectual.

What makes this industry different is that an accounting system can make or break an MCA company. For example, a supermarket usually has good POS software for inventory control. If an employee drops a “box of tomatoes” it’s not the end of the world. The loss is either immaterial or if it is material the accounting system will pick up the big monetary discrepancy.

In the MCA industry a “box of tomatoes” could be anything from a $0.05 loss to a $500,000 loss. Because the MCA industry deals with money as its product and is often processing transactions at breakneck speed, there needs to be safeguards in the system to catch any and all mistakes in real time.

Our accounting firm has seen where people built attractive systems which seemed good to the funder. However, if the funder lacks accounting knowledge when this “box of tomatoes” falls out they may not be able to place exactly where the loss occurred. Or even worse, they may not realize a loss has taken place until it is too late. For example, if you wait until the end of the tax year and then discover that merchant payments have been missed how do you recoup those funds? It’s the same situation if incorrect amounts are funded to merchants, if incorrect commissions are paid out, or if syndicators have not invested the funds they were expected to.

Phone (845) 875-6030

Fax (845) 678-3574

Email: cjt@ywcpa.com

http://ywcpa.com

Please consult with an accountant to assess your particular situation and needs.

Despite FinTech Disruptions, Many Thing Stay The Same

January 5, 2015 2014 was an unbelievable year!

2014 was an unbelievable year!

I kicked off last year by opening an account with Lending Club so that I could understand their product. Today I have tens of thousands of dollars invested on their platform and picking up new loans has become part of my daily routine. You could say I’m not surprised they went public a few weeks ago.

I also launched the industry’s first trade publication and ran it as both publisher and chief editor. We produced 6 issues and distributed more than 20,000 print copies combined. Unfortunately the publication will not be continuing further. It is wild to think that it both started and concluded in 2014 as the magazine had a cult-like following.

7 conferences in 4 cities. Las Vegas (twice), San Francisco, New Orleans, and here in New York. I spoke at two of them. Hoping for at least 1 Miami conference this year. Please??? It’s so cold here right now.

OnDeck Capital took a lot of flak in 2014 from both industry insiders and the media. They shrugged it all off and went public on December 17th. Considering they’ve operated on the fringe of the merchant cash advance industry for so long, it was one of those things you had to see to believe. I didn’t get inside the building but I saw the IPO was real from the outside.

I started off 2014 not knowing what a Bitcoin was. Now I have a copy of the entire blockchain, operate a full node (don’t worry I have port 8333 open), have 10 dedicated mining devices running 24/7, have made purchases with bitcoin, conducted countless transfers, and just finished coding a working prototype application using Coinbase’s API. And when I realized that bitcointalk.org and my cryptography books weren’t enough to satisfy my appetite, I found myself talking about bitcoin on IRC; #bitcoin and #bitcoin-pricetalk on irc.freenode.net. I also know who Satoshi Nakamoto really is now too but he made me promise not to tell anyone.

I rebranded Merchant Processing Resource to AltFinanceDaily, retiring a name I’ve used for 4 years.

I interviewed former Congressman Barney Frank, one of the two architects of the Dodd-Frank Wall Street Reform and Consumer Protection Act (it was only a few questions).

I got asked by a credible movie producer if I would help him on a storyline for a script about Wall Street and the alternative business lending industry. Don’t worry I turned it down!

I jumped on the payment disruption bandwagon and used Square to process credit card transactions all year. You should know that I previously did merchant account sales. I could’ve boarded my own account and set my own fees but I went with Square anyway.

I finally got set up to syndicate on merchant cash advances.

I ran my first 5k in Central Park.

I moved to a different part of Manhattan.

Of course a whole lot more happened. It was a roller coaster year which leads me to believe that 2015 will be impossible to predict. There’s a lot more room to grow in FinTech but it might be time for fresh ideas. Everyone and their mom built an online lending marketplace platform in 2014.

Similarly, it’s also a tough time to become a loan broker or MCA ISO especially if you’re undercapitalized. The easy profit ship has sailed. Press 1s and UCCs aren’t winning business models, at least not ones that will invite outside capital or ensure survival long term.

2014 changed finance but in many ways it stayed the same.

It still takes 2-4 days to confirm an ACH didn’t reject! This is annoying all around. If I add funds to Lending Club on a Monday, it’s not accessible until Friday evening. If you debit a merchant on Monday, you won’t really know if you have it until a few days later. Believe it or not I actually mailed out more checks in 2014 than in any other year of my life. The ACH system appears to be fine until you use something that is far more advanced, something I will probably write about over the next month. Instantaneous payments, low transaction fees, no bank involvement. Yeah, it’s time for ACH to go away…

And with banks, well… I have opened business bank accounts over the last few years with 3 different banks. The one I opened in 2014 required a two hour in-person interview, a process that involved filling out forms by hand and being threatened that the government would shut everything down in a heartbeat if they found out that I so much as breathed wrong on an ATM. It was a repeat of prior account opening experiences. Although I’ve never had an account closed for doing anything wrong (because I’m not actually doing anything wrong), it is easy to see how much regulatory pressure banks are under. Swiping your debit card upside down could cause the entire bank to get an Operation Choke Point subpoena. They want your business but they’re scared to death of anything you might do with a bank account.

All the major peer-to-peer platforms of 2014 became centralized. Lending Club and Prosper don’t even fall in the p2p category anymore. The market trend has been to create a platform designed for the little guys and then hand it over to a bank or institutional money to do all the funding. In some ways it’s easier to deal with a handful of big players instead of thousands or millions of retail investors. But with the regulatory environment uncertain on so many new investment products, it’s probably also safer to deal with institutional investors, lest the regulators claim they violated a consumer protection law they thought up this morning.

Banks continue to be the biggest obstacle to innovation because at the end of the day, all payments flow through them. How can one deBank and truly disrupt?

Hopefully we’ll find out in 2015. Happy belated New Year.