The Top Small Business Funders By Revenue

October 23, 2017The below chart ranks several companies in the non-bank small business financing space by revenue over the last 5 years. The data is primarily drawn from reports submitted to the Inc. 5000 list, public earnings statements, or published media reports. It is not comprehensive. Companies for which no data is publicly available are excluded.

| Company | 2016 | 2015 | 2014 | 2013 | 2012 |

| Square1 | $1,708,721,000 | $1,267,118,000 | $850,192,000 | $552,433,000 | $203,449,000 |

| OnDeck2 | $291,300,000 | $254,700,000 | $158,100,000 | $65,200,000 | $25,600,000 |

| Kabbage3 | $171,784,000 | $97,461,712 | $40,193,000 | ||

| Swift Capital4 | $88,600,000 | $51,400,000 | $27,540,900 | $11,703,500 | |

| National Funding | $75,693,096 | $59,075,878 | $39,048,959 | $26,707,000 | $18,643,813 |

| Reliant Funding5 | $51,946,472 | $11,294,044 | $9,723,924 | $5,968,009 | $2,096,324 |

| Fora Financial6 | $41,590,720 | $33,974,000 | $26,932,581 | $18,418,300 | |

| Forward Financing | $28,305,078 | ||||

| Gibraltar Business Capital | $15,984,688 | ||||

| Tax Guard | $9,886,365 | $8,197,755 | $5,142,739 | $4,354,787 | |

| United Capital Source | $8,465,260 | $3,917,193 | |||

| Blue Bridge Financial | $6,569,714 | $5,470,564 | |||

| Lighter Capital | $6,364,417 | $4,364,907 | |||

| Fast Capital 360 | $6,264,924 | ||||

| US Business Funding | $5,794,936 | ||||

| Cashbloom | $5,404,123 | $4,804,112 | $3,941,819 | $3,823,893 | $2,555,140 |

| Fund&Grow | $4,082,130 | ||||

| Nav | $2,663,344 | ||||

| Priority Funding Solutions | $2,599,931 | ||||

| StreetShares | $647,119 | $239,593 | |||

| CAN Capital7 | $213,402,616 | $269,852,762 | $215,503,978 | $151,606,959 | |

| Bizfi8 | $79,886,000 | $51,475,000 | $38,715,312 | ||

| Quick Bridge Funding | $48,856,909 | $44,603,626 | |||

| Funding Circle Holdings9 | $39,411,279 | $20,100,000 | $8,100,000 | ||

| Capify10 | $37,860,596 | $41,119,291 | |||

| Credibly11 | $26,265,198 | $14,603,213 | $7,013,359 | ||

| Envision Capital Group | $21,034,113 | $19,432,205 | $12,071,976 | $11,173,853 | |

| Capital Advance Solutions | $4,856,377 | ||||

| Channel Partners Capital | $2,207,927 | $4,013,608 | $3,673,990 | $2,208,488 | |

| Bankers Healthcare Group | $93,825,129 | $61,332,289 | |||

| Strada Capital | $8,765,600 | ||||

| Direct Capital | $432,780,164 | $329,350,716 | |||

| Snap Advances | $21,946,000 | ||||

| American Finance Solutions12 | $5,871,832 | $6,359,078 | |||

| The Business Backer13 | $19,593,171 | $11,205,755 | $9,615,062 |

1Square (SQ) went public in 2015

2OnDeck (ONDK) went public in 2014

3Kabbage received a $1.25B+ private market valuation in August 2017

4Swift Capital was acquired by PayPal (PYPL) in August 2017

5Reliant Funding was acquired by a PE firm in 2014

6Fora Financial was acquired by a PE firm in 2015

7CAN Capital ceased funding operations in December 2016 but resumed in July 2017

8Bizfi wound down in 2017. Credibly secured the servicing rights of their portfolio

9Funding Circle’s primary market is the UK

10Capify’s US operations were wound down in early 2017 and their operations were integrated with Strategic Funding Source. Capify’s international companies are still operating

11Credibly received a significant equity investment from a PE firm in 2015

12American Finance Solutions was acquired by Rapid Capital Funding in 2014, who was then immediately acquired by North American Bancard

13The Business Backer was acquired by Enova (ENVA) in 2015

Catching Up With Online Lending – A Timeline

October 21, 20177/17

- Online lender Upgrade, launched by former Lending Club CEO Renaud Laplanche, revealed it had already hired about 100 people

- Credit risk startup James closed $2.7M funding found led by Gaël de Boissard

7/18 – Former Bizfi COO Tomo Matsuo joined iPayment as an SVP to oversee its new merchant cash advance division

7/21 – SoFi Chief Revenue Officer Michael Tannenbaum departed the company

7/27

- Lending surpassed $500M in lifetime originations

- RealtyShares acquired marketplace platform Acquire Real Estate

7/28

- Former MB Financial Bank SVP Stan Scott became VP at Gibraltar Business Capital

- Prosper Marketplace shut down its Prosper Daily (formerly BillGuard) app

7/31 – First Associates Loan Servicing announced the opening of their new 1000-seat capacity operations center in Baja California, Mexico

8/1

- Ron Suber joined Credible.com as executive vice-chairman and a member of the board of directors

- PeerStreet integrated with Personal Capital

8/2

- Lending Loop raised $2M, launched automated investment platform

- PeerIQ secured $12M in Series A round

- OnDeck partnered with Payment Source in Canada

- Bread raised $126M in equity and debt

8/3 – Kabbage secured $250M in Series F round from SoftBank Group, was valued at more than $1.25B

8/9

- Former Capital One VP Heather Tuason became Chief Product Officer at StreetShares

- PayPal acquired Swift Capital

8/10 – Coinbase raised $100M at $1.6B valuation

8/11 – Former SoFi employee raised Brandon Charles filed a lawsuit against the company alleging among other things that he witnessed sexual harassment in the workplace

8/14

- Prosper closed $500M securitization, announced $775M in Q2 loan originations, $41.4M net loss

- Bitcoin surged past $4,000

8/15 – iPayment announced the formation of its new merchant cash advance division, iPayment Capital

8/16 – Fifth Third Bank made another equity investment in ApplePie Capital, agreed to purchase loans through the company’s marketplace

8/19 – Former CFO of Credibly became president of Western Funding

8/22 – Former SoFi employees filed a lawsuit against the company over wage issues

8/23 – Ellevest raised $32.5M

8/24 – AutoFi raised $10M in Series A

8/25 – Rep. Maxine Waters called for a congressional hearing on SoFi’s bank charter application and ILC charters in general

8/29 – Snap Finance secured $100M credit facility

8/30

- IOU Financial announced Q2 originations of $26.2M (US) and a net loss of $2.08M (CAD)

- ShopKeep launched ShopKeep Capital, a merchant cash advance service

8/31 – Bizfi wound down operations, sold servicing rights to its $250M portfolio to Credibly

9/2 – Bitcoin surpassed $5,000

9/5 – Former Chief Sales Officer of OnDEck, Paul Rosen, joined CoverWallet as COO

9/6 – Square revealed that they would apply for an ILC charter, following in the footsteps of SoFi

9/7

- Former Director of External Sales at OnDeck, Jared Kogan, joined Pearl Capital as Chief Revenue Officer

- First Internet Bank announces strategic partnership with Lendeavor, Inc.

9/11

- SoFi CEO Mike Cagney announced he had resigned as board chairman and would be resigning as CEO later in the year

- Lenda raised $5.25M Series A

9/12

- Groundfloor announced $100M loan purchase agreement with Direct Access Capital

- Orchard unveiled its Deals platform

- JPMorgan CEO Jamie Dimon called Bitcoin a fraud for stupid people

9/13 – dv01 closed $5.5M Series A

9/14 – SmartBiz surpassed $500M in lifetime SBA loan originations

9/15

- Amid more negative press, SoFi CEO Mike Cagney announced he was resigning as CEO immediately

- Enova announced $25M share repurchase program

9/20 – World Business Lenders acquired strategic assets of Bizfi including the company’s brand and marketplace

9/22 – Prosper Marketplace raised $50M in a Series G round at a 70% lower valuation of $550M

See previous timelines:

5/17/17 – 7/11/17

4/6/17 – 5/16/17

2/17/17 – 4/5/17

12/16/16 – 2/16/17

9/27/16 – 12/16/16

The Top Small Business Funders By Revenue

September 14, 2017Thanks to the Inc 5000 list on private companies and earnings statements from public companies, we’ve been able to compile rankings of alternative small business financing companies by revenue. Companies that haven’t published their figures are not ranked.

| SMB Funding Company | 2016 Revenue | 2015 Revenue | Notes |

| Square | $1,700,000,000 | $1,267,000,000 | Went public November 2015 |

| OnDeck | $291,300,000 | $254,700,000 | Went public December 2014 |

| Kabbage | $171,800,000 | $97,500,000 | Received $1.25B+ valuation in Aug 2017 |

| Swift Capital | $88,600,000 | $51,400,000 | Acquired by PayPal in Aug 2017 |

| National Funding | $75,700,000 | $59,100,000 | |

| Reliant Funding | $51,900,000 | $11,300,000 | Acquired by PE firm in 2014 |

| Fora Financial | $41,600,000 | $34,000,000 | Acquired by PE firm in October 2015 |

| Forward Financing | $28,300,000 | ||

| IOU Financial | $17,400,000 | $12,000,000 | Went public through reverse merger in 2011 |

| Gibraltar Business Capital | $16,000,000 | ||

| United Capital Source | $8,500,000 | ||

| SnapCap | $7,700,000 | ||

| Lighter Capital | $6,400,000 | $4,400,000 | |

| Fast Capital 360 | $6,300,000 | ||

| US Business Funding | $5,800,000 | ||

| Cashbloom | $5,400,000 | $4,800,000 | |

| Fund&Grow | $4,100,000 | ||

| Priority Funding Solutions | $2,600,000 | ||

| StreetShares | $647,119 | $239,593 |

Companies who were published in the 2016 Inc 5000 list but not the 2017 list:

| Company | 2015 Revenue | Notes |

| CAN Capital | $213,400,000 | Ceased funding operations in December 2016, resumed July 2017 |

| Bizfi | $79,000,000 | Wound down |

| Quick Bridge Funding | $48,900,000 | |

| Capify | $37,900,000 | Wound down |

The Google Battle for Lending and SMB Finance Keywords

September 14, 2017The online lending battle is at least in part being fought online. Below is a chart of organic page 1 rankings in Google for some of the industry’s biggest players, banks, and the SBA. (Hat tip to Fundera and NerdWallet):

| Keywords | OnDeck | Kabbage | Fundera | Lending Club | NerdWallet | National Funding | Traditional Banks | SBA.gov |

| business loan | 1 | 9 | 3 | 5 | 4,7 | 6 | ||

| merchant cash advance | 2 | 3 | 4 | 8 | ||||

| working capital | 9 | 4 | ||||||

| commercial loan | 3 | 2,7 | ||||||

| small business loans | 2 | 3 | 5 | 7 | 1 | |||

| business line of credit | 3 | 2 | 11 | 1,4 | 6,7,8,9,10 | 5 | ||

| fast business loan | 1 | 4 | 2 | 5,6 | ||||

| business loan with bad credit | 7 | 1 | 2 | 3 |

The Top 10 Google Search Results for Merchant Cash Advance in February 2012 compared to now:

| February 2012 | September 2017 |

| MerchantCashinAdvance.com | Wikipedia |

| Yellowstone Capital | OnDeck |

| Entrust Cash Advance | Fundera |

| Merchants Capital Access | NerdWallet |

| Merchant Resources International | Businessloans.com |

| American Finance Solutions | Bond Street |

| Nations Advance | Capify |

| Bankcard Funding | National Funding |

| Rapid Capital Funding | CNN |

| Paramount Merchant Funding | CAN Capital |

The top result in 2012 is a great example of how much easier it was to game Google’s system back then. After achieving rank #1 for MCA and 300 other related keywords, MerchantCashInAdvance.com, which was just a lead generation site, sold for $75,000 in December 2011. The site was later clobbered by Google Penguin for black hat SEO and banished from visibility.

A major shift has obviously taken place over the last 5 and a half years. Is the search results game rigged to advance Google’s own interests? Three years ago I put forth my theory on that.

One thing that’s different between then and now is that Google now has 4 paid links above the organic search results as opposed to 3 and the paid links blend in more with the organic results. With the organic results pushed further down the page, they’re not as visible as they were five years ago.

Read my previous analyses on the industry’s search war over the years:

December 2015 Google Serves Low Blow to Merchant Cash Advance Seekers

March 2015 Google Culls Online Lenders – Pay or Else?

October 2014 Merchant Cash Advance SEO War Still Raging

August 2014 Six Signs Alternative Lending is Rigged: Do Lending Club and OnDeck have a helping hand?

October 2013 Google Penguin 2.1 takes swing at the MCA industry

August 2013 Your merchant cash advance press release may be hurting you

December 2012 Is Google your only web strategy?

July 2012 The other 93% [of leads]

April 2012 The SEO war continues

February 2012 The SEO War for Merchant Cash Advance: The first story on this topic

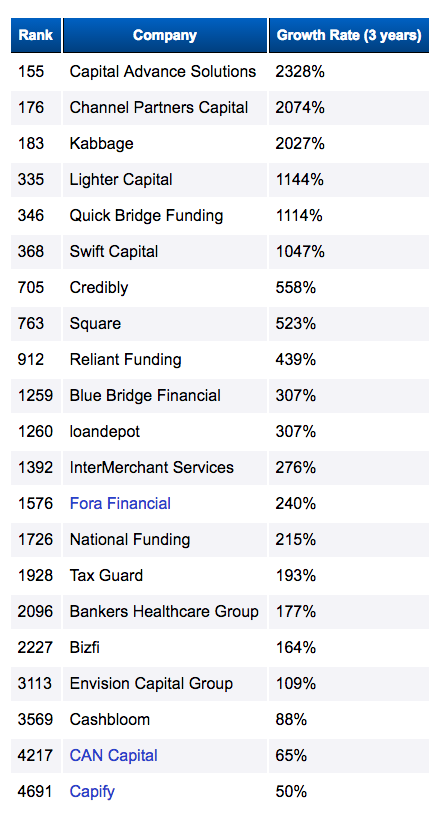

Where Alternative Finance Ranks on the Inc 5000 List

September 14, 2017Here’s where your peers rank on the Inc 5000 list for 2017:

| Ranking | Company Name | Growth | Revenue | Type |

| 15 | Forward Financing | 12,893.16% | $28.3M | MCA |

| 47 | Avant | 6,332.56% | $437.9M | Online Consumer Lender |

| 219 | OppLoans | 1,970.22% | $27.9M | Online Consumer Lender |

| 260 | US Business Funding | 1,657.42% | $5.8M | Business Lender |

| 361 | nCino | 1,217.53% | $2.4M | Software |

| 449 | Kabbage | 979.31% | $171.8M | Online Consumer Lender |

| 634 | Lighter Capital | 712.03% | $6.4M | Online Business Lender |

| 694 | Swift Capital | 652.08% | $88.6M | Business Lender |

| 789 | CloudMyBiz | 575.46% | $2.1M | IT Services |

| 1418 | loanDepot | 286.11% | $1.3B | Online Consumer Lender |

| 1439 | Nav | 281.98% | $2.7M | Online Lending Services |

| 1731 | United Capital Source | 224.85% | $8.5M | MCA |

| 1101 | ZestFinance | 165.99% | $77.4M | Online Lending Services |

| 2050 | National Funding | 184.74% | $75.7M | Online Business Lender |

| 2572 | Blue Bridge Financial | 136.73% | $6.6M | Online Business Lender |

| 2708 | Bankers Healthcare Group | 127.51% | $149.3M | Financial Services |

| 2714 | Tax Guard | 127.02% | $9.9M | Financial Services |

| 2728 | Fora Financial | 125.81% | $41.6M | Online Business Lender |

| 2890 | Reliant Funding | 121.61% | $51.9M | Online Business Lender |

| 4005 | Cashbloom | 70.47% | $5.4M | MCA |

| 4945 | Gibraltar Business Capital | 42.08% | $16M | MCA |

Compare that to last year’s list below:

Of the companies on the 2016 list, Capify and Bizfi were wound down while CAN Capital ceased operations but then later resumed them more than half a year later.

Why BFS Capital’s Glazer Is Passing the Torch

August 22, 2017

Marc Glazer co-founded BFS Capital in the early 2000s and has remained at the helm all this time – until now. Glazer has passed the torch over to Michael Marrache, effective last week. He isn’t going too far, as the former chief executive will remain chairman of the board working alongside Marrache on the next chapter for the MCA and small business lending company. Meanwhile the executive pair points to a future not only where there is sustainability but where there is growth.

“We’ve obviously grown the company year after year over the last 15 years, and as with every other type of business and industry there were ebbs and flows. Over the last couple of years with a significant amount of challenges going on, we as a company decided we want to continue to grow but we want to grow in a way that benefits the company from a profitability standpoint as well as serves our customers,” said Glazer.

In April 2017, BFS Capital surpassed $1.5 billion in financings since inception. The company expects to fund more than $300 million in new financings in this calendar year.

“We’ll increase our reliance on algorithmic solutions, transparency in the ISO and customer experience and we will increase the number of financing solutions. Culture is significant for us and we will continue to build on the legacy Marc created,” said Marrache.

Marrache takes the reigns at a time when the industry is at a crossroads that will leave some alt lenders in the dust while other rise to the occasion.

“The stories that were challenging in 2016 look good in 2017,” said Marrache, pointing to OnDeck’s forthcoming profitability, Kabbage’s lofty valuation, CAN Capital’s return to funding, PayPal’s acquisition of Swift Financial and Prosper looking good.

“We think alternative and non-bank lending are in a good place. And yes, some of the folks that are no longer operating in this space were overextended or may have exhibited irrational behavior for pricing or customer acquisition costs. We think what we’re witnessing is the normal lifecycle of the industry. There were lots of participants earlier. Now to participate the industry must show a bit more control and sophistication. If you execute well, the tomorrows will be better than 2016,” said Marrache.

And according to Glazer, because of the changes in the business environment over the last couple of years, it’s going to require a different skillset to take BFS Capital to the next level.

“There are clear differences between starting a company, growing a company and becoming a billion-dollar small business financing platform. We’ve needed to evolve at each stage and now again with Michael’s leadership,” he said.

For Glazer, Marrache was almost always the succession plan.

“To be fair, hiring Michael four years ago, maybe succession planning was in the back of my mind somewhat. But as our relationship developed and as he was COO for three-plus years and then president, it became apparent that Michael’s skill set, passion, desire and how he looked at culture were all similar to myself. Let’s grow, but let’s watch our numbers. Make sure we treat people fairly. And for the businesses we are financing — provide thoughtful capital to help them versus creating problems for them,” said Glazer.

More Funding

BFS Capital’s business model is comprised both of MCAs and small business loans. Alternative funding company CAN Capital does both MCAs and loans and had to pause lending until recently. For BFS, however, it’s all systems go. And that means unequivocally continuing to fund small businesses.

“Absolutely, yes. And there’s no quizzicality in mind. I would say we are going to continue funding small businesses and fund more of them this year than we did last year. And we will fund even more the year after. So absolutely,” Marrache said.

BFS Capital sells through both ISOs and directly to merchants, the former of which is where most originations derive. “There are a number of solutions we are putting together to benefit that network,” said Marrache, adding he doesn’t believe algorithmic solutions will replace underwriters.

“We have a strong legacy of customer underwriting. We believe lower level transactions can be significantly more automated. Above a certain level and certain amounts of origination, we think algorithms and data solutions at that point are a facilitator, not a replacement of our underwriting,” Marrache said.

The Legacy

There was a time when BFS Capital’s growth plans included debuting in the public markets. Those plans have since been sidelined amid a chilly investor reception for alternative lender stocks.

“We spent a lot of effort in our filing,” said Glazer. “But at the end of the day, the market for the space had softened. Going forward I think it’s really going to be a question of what the markets look like and what makes sense for our company. We will evaluate that as the situation warrants.”

IPO or not, it appears Glazer’s legacy is still being written.

“I co-founded the company 15-plus years ago. Before finance and accounting, at heart, I’m an entrepreneur. That’s what I do, what I enjoy. I love starting companies, having the vision and creating things,” he said.

As chairman of the board and a major stakeholder, Glazer will continue to be active in BFS Capital.

Tips From the Source: Small Businesses Told AltFinanceDaily How They Wanted Loans to be Marketed to Them

July 31, 2017

Small business owner Jim Moseley is inundated with calls from online funders—and he hates it. They frequently use unscrupulous tactics to try and get his attention. More than one has claimed to be a close friend so his assistant transfers their call. Then they try to reel him in with stories they’ve concocted about past personal connections. The unprofessional-sounding calls also irk him—where a salesman insists he’s local, but his voice sounds muffled and distant. In these instances, Moseley usually hangs up within a few seconds.

“The layer of sleaze is as thick as lard in the calls that I get,” he says.

Like many small business owners, Moseley, the chief executive of TransGuardian Inc., a shipping solutions company based in Petersham, Massachusetts, finds these types of calls extremely off-putting. In fact, it’s what made him hesitant to do online funding to begin with—until it became absolutely necessary since he couldn’t get a bank loan.

He’s not alone. As online financing proliferates, several small business owners say they are increasingly being bombarded with stacks of snail mail, multiple cold calls a day and numerous unsolicited emails offers—many of which they don’t understand and therefore won’t accept. Rather, small business owners say they prefer to work with companies that are forthcoming, provide sound advice and have taken steps to prove their credibility. They offer several tips on how funders can win more of their business.

Tip No. 1: Can the cold-calls

Several small business owners say they don’t mind when lenders follow up with them after a legitimate interaction. But they could do without the boiler-room tactics.

“It feels like a loan shark situation,” says Sean Riley, co-founder of DUDE Wipes, a Chicago-based company that makes flushable wipes for men. Riley, who has several good experience obtaining loans through Kabbage, finds the constant phone calls from firms he doesn’t know particularly vexing. He suggests lenders drop the high-pressure routines and find more effective ways to promote their services to small businesses. “These companies could be very credible. I don’t know. But I don’t perceive them as credible—and perception is reality,” he says.

Tip No. 2: Step up legitimate marketing efforts

Donna Cravotta chief executive and founder of Social Pivot PR, a Bedford, New York social media and marketing communications firm, says online funders should seek out simple, cost-effective ways to get their name in front of small businesses. For relatively little money they can sponsor local small business events. She also suggests that online lenders volunteer to speak at small business events and teach small businesses how to leverage online lending opportunities. They could also appear as guests on financial podcasts or broadcast Webinars to the small business community, says Cravotta, who has taken a few loans to fund her business, two of which were with Lending Club.

R.T. Custer, co-founder and chief executive of Vortic Watch Company in Fort Collins, Colorado, offers some additional advice: Customers don’t believe when you self-publish your testimonials. When he sees a review on a website, he wants to know how much a company has paid for that review. Instead, he relies on third party confirmations of a company’s worth. “When it’s clearly something that is not paid for, that is the best kind of advertising,” says Custer, an OnDeck customer whose business turns antique pocket watchers into wrist watches.

Tip No. 3: Deliver personal attention

As much as they hate aggressive salespeople, small businesses love personal attention from their lenders. Dana Donofree, founder and chief executive of AnaOno Intimates, a Philadelphia-based company that designs and sells apparel for breast cancer survivors, appreciates the stellar customer service she gets with OnDeck. The sales rep follows up appropriately to make sure everything is going well, but doesn’t bombard her constantly. She gets an occasional email asking if she needs more funds—but the communications aren’t overly aggressive. “Some institutions can really be sales pushy and call you several times a day. I’ve blocked more numbers than I would like to admit,” she says.

Tip No. 4: Be a resource for small business owners

Online lenders can also gain traction by helping customers better understand the financing process; many small business owners often don’t know much about financing and would appreciate getting sound advice from lenders, according to Sandy Lieberman, who co-owns Artemis Defense Institute in Lake Forest, California.

She and her husband started the business a few years ago to offer reality-based training to law enforcement, military personnel and civilians. When the business needed cash, Lieberman began searching online for a bank loan, but wound up taking a merchant cash advance instead. After a few rounds, she started getting bombarded with solicitations. “I think the stacks of mailings from companies must have been four-inches thick,” she recalls.

After additional research, she reached out to Lendio to broker an $85,000 term loan; she later took another loan for $204,000 through Lendio. While these funds have brought her business to a better place—and she has learned a lot in the process—she feels online lenders are missing out on a prime teaching opportunity.

“Some lenders think business owners know more than they already do. Some really don’t know a lot and could use more hand-holding,” she says.

In hindsight, Lieberman—who nearly destroyed her personal credit while trying to run her business—wishes a funding company had offered her a short class on financing; she would have attended, even for a small cost. Access to a finance coach—someone at the lending company who could help business owners plan proactively without ruining their personal credit—would also be a boon, she says.

“Small business owners are wearing many hats—customer service, payroll, financing, strategic planning. In the midst of all that they don’t know necessarily know how to make wise funding decisions,” she says.

Tip No. 5: Advertise

There are plenty of small businesses that need funds, but many simply don’t know where to turn. Consider a TD Bank survey of 553 small business owners in late March that found 21 percent have or will seek a loan or line of credit in the next 12 months. While the majority of these businesses plan to try their bank first, a sizeable number—11 percent—don’t know how to seek credit when they are ready. While many small businesses have found lending partners by Googling for information, others simply feel stymied by the process.

Take the case of Scott Deuty, who is having trouble obtains funds for Coolbular Inc. in Cheyenne, Wyoming, which serves as an umbrella for his kiddie ride business and his writing and publishing services. He wants to raise funds but has bad credit and doesn’t meet the revenue requirements for certain lenders. There are so many lenders; he doesn’t know how to find the right one—or one that might be willing to take a chance on him. “It’s very difficult,” he says.

Deuty’s case is an example of the paralysis that can happen when small businesses don’t know where to turn. It’s an opportunity for alternative funders to gain a leg up by marketing more appropriately to small businesses that may not know they exist—or how to find them.

Custer, of Vortic Watch, reached out to OnDeck for a bridge loan after seeing a television ad that ran during an episode of Shark Tank. He also suggests funders use online advertising to gain broader exposure. “If a business owner is trying to find a loan, they are going to Google, ‘I need a loan,’” he says.

Tip No. 6: Ramp up business referrals

Tip No. 6: Ramp up business referrals

Another way small businesses hear about lending opportunities is through business referrals. Azhar Mirza, founder of SomaStream Interactive, an e-learning solutions provider in Berkeley, California, says funders should actively seek out more referral partnerships. In 2015, his company couldn’t afford its online marketing costs. Then a lifeline came its way. Mirza received an offer from Google telling him his company was eligible for a loan to help finance the online advertising it was doing through the Google AdWords program. The offer was part of a new pilot program between Google and Lending Club to extend credit to smaller companies that use Google’s business services. SomaStream got access to the funds it needed, but in lieu of cash, the company received advertising credits with Google.

The pilot program between Google and Lending Club ended in the first quarter of 2016, but Mirza believes similar partnerships would be a great tool for online lenders. Certainly for Mirza, the timing was precipitous, he says.

Push notifications from trusted business partners can also be an effective marketing tool, when used in moderation. When Yvonne Denman-Johnson, co-founder of HootBooth Photo Booth, a Lago Vista, Texas, manufacturer of photo booth kiosks, needed money, she happened to receive a notice from Shopify, the company’s e-commerce software and hosting provider, talking about its merchant cash advance services. She has one outstanding advance through Shopify, which she is working to pay off.

Tip No. 7: Be transparent

Denman-Johnson got the funds she needed, but she feels MCA providers need to be more transparent about the effective interest rate—at the advertising stage, not at the approval stage—so small businesses can make more informed decisions without having to do all the calculations themselves. Otherwise, some small businesses might decide not to pursue this form of funding because of the unknowns. Her company almost walked away, but decided to go through the full application process. At this point, Shopify provided the effective interest rate, which was in the 12 percent range. Other funders she researched were in the 30 percent range—which she describes as “outrageously” expensive.

Indeed, small business owners want to work with funders that outline the terms clearly and offer comparisons. Lisa Ayotte, founder of Soul’y Raw, a specialty pet food provider in San Marcos, California, has had good experiences with Kabbage, On Deck and Fundbox.

Indeed, small business owners want to work with funders that outline the terms clearly and offer comparisons. Lisa Ayotte, founder of Soul’y Raw, a specialty pet food provider in San Marcos, California, has had good experiences with Kabbage, On Deck and Fundbox.

She wishes, however, that all online lenders offer more detailed information about the loan programs they offer on their website—so small businesses can weigh their options before they go through the actual application process. Small businesses want to know, for instance, whether a lender offers debt consolidation. They also want funds to spell out clearly on their websites the various types of loans offered and the underwriting criteria. Ayotte also suggests lenders provide links to online loan calculators so small businesses can understand what the terms mean to them.

Small business owners want to be told like it is. That’s one major appeal of online lending—if you’re going to be turned down, you typically know right away says Ricardo Picon, the co-owner of The Sandwich Shop, a restaurant and catering business in Williamsburg, New York.

He took an $88,000 loan in February issued by Excelsior Growth Fund, a U.S. Treasury-certified Community Development Financial Institution, but in the future, he says he would consider using a different type of online lender. It would depend on the rates, the economic times, monthly payments and closing fees, among other things. “I want transparency. I want to know if they are going to give me the money or not so I can move on. This way there are no false hopes,” he says.

Tip No. 8: Make the process as easy as possible

Small business owners also prefer to work with online lenders that make the process seamless. AJ Saleem, founder of Suprex Learning, a Houston-based private tutoring and test prep company, was proactive about searching for online lending options. He chose a loan with Lending Club in part because the process was so easy. Some applications he started, but never finished because the process was too onerous. With Lending Club, the process was quick, there were fewer questions asked and the funder asked for less documentation than some competitors, Saleem says.

To be sure, rates are really important to small businesses, but they also want to work with funders they feel are on the up-and-up. “We want a square deal,” says Moseley, the chief executive of TransGuardian. “Tell us what the deal is in an honest and professional way and if we like it we’ll do business.”

Fintech Remains Loyal to Prosper & Suber

July 10, 2017

When AltFinanceDaily reached out to fintech market participants for comment on Ron Suber’s sudden departure as Prosper’s president, the responses were the same — ‘anything for Ron.’ Dubbed the Godfather of fintech, Suber might deserve superhero status given the recapitalization that he and the Vermuts led half a decade ago to save Prosper Marketplace. That type of rescue inspires the kind of loyalty that investors and other fintech participants are displaying not only for Suber but also the Prosper brand.

“Ron is an incredible business partner. His word is always good. He doesn’t overpromise, and he always follows through. We were honored to work with a guy like that,” said Matt O’Malley, co-founder and president of Looking Glass Investments, which has been investing on the Prosper platform since 2008.

Perhaps he has never seen him overpromise but in recent weeks he and many other investors on the Prosper platform did observe an overstatement of returns. O’Malley calls it a forgivable mistake.

“In my view, it is our responsibility to track our returns. Prosper provides an extremely robust data set. We have the ability to calculate our returns daily,” said O’Malley, pointing to a nascent fintech market that is still evolving. “This asset class is new. If you compare it to investing in stocks and bonds, it’s in its infancy. When preparing returns, it’s very challenging to determine what they are,” he said.

Looking Glass has been investing in individual loans on the Prosper platform since before Suber’s time and has watched as the former Wells Fargo executive has transformed the peer-to-peer lender to welcome institutional investors.

“He didn’t have to let us stay on the platform. They could have chosen to replace the little guy. But that isn’t how he does business. He knew the investment banks and [other] banks would get involved, however he knew there was enough room for everyone,” said O’Malley.

That day is here, evidenced by Prosper’s previously announced deal with a consortium of institutional investors to purchase $5 billion worth of loans via the Prosper platform over the next couple of years.

FT Partners was the lead advisor on that deal.

“When they needed capital they could have chosen anybody to help. We were excited to be the chosen one to help them on the deal. It was one of fintech’s largest deals and certainly the largest of its kind,” said Steve McLaughlin, founder of FT Partners.

McLaughlin went on to explain the unique circumstances surrounding the transaction, including a lack of diversification tied to Prosper’s capital sources, which he added was a learning experience not only for the peer-to-peer lender but for all of fintech.

“They were focused on getting capital from hedge funds in a steady stream. When the capital markets had a blip, lots of that capital backed away. It was an unprecedented thing to go out and get a $5 billion forward agreement from a series of investors. “There was nothing cookie cutter about it,” said McLaughlin.

Since then the rest of fintech seems to be catching on.

“FT Partners is getting a lot of attention and a lot of calls for all of the other activity we are doing in the space as well. We raised capital for Prosper and a bunch of other companies, including Earnest, GreenSky, Upstart, Kabbage and others. We get a lot of calls, and we’re doing a lot of deals in the space. It’s a lot of fun,” McLaughlin said.

Much of the success of the multi-billion dollar Prosper deal was thanks to Suber.

“A lot of people are very familiar with Ron and the Prosper story and view Prosper as a high-end institution that while having some issues on financing had a very big and long-term future. Lots of Ron’s connections from before came into play in the round,” said McLaughlin.

Now that Suber is out of the picture in an official capacity, investors have every right to be disappointed. But as McLaughlin pointed out, Suber remains a big shareholder in Prosper and the peer-to-peer lender’s greatest supporter, two things that the FT Partners founder does not expect to change.

“This is not a major blow for Prosper. They maintain Ron as a friend of the firm and as an advisor. He has great friends and colleagues at Prosper. He is not going to work for anybody else. He won’t be doing anything with any other lending companies, I don’t think. He may be able to do more good from the outside than the inside at Prosper. I think Ron will always be part of the Prosper family,” McLaughlin said.

Why Now?

If things were going so well for Suber ushering Prosper into its chapter that included expanding the role of institutions on the platform then why is he leaving now? While Suber himself was not available to answer that question, the answer seems to be that it is personal. The fintech community knows Suber for his role in advancing this new asset class but what people might not know is that he is also a husband and a father.

“I think he just feels like this is more of a personal shift,” McLaughlin said.

O’Malley’s impression was similar. Upon joining the fintech startup, Suber made it a point to get to know the Looking Glass team.

“Ron invited us to breakfast. We did this three times. I remember meeting him and thinking this guy is exactly what we need – extra bright, charismatic and he talked lovingly about his children and his wife. He even joked that marriage is like yoga – it’s harder than it looks,” O’Malley said. “My guess is they are going to spend some time together as a family. And he is going to come back bigger and better than ever.”

Meanwhile Both O’Malley and McLaughlin were familiar with Prosper before Suber came on board, and both will remain engaged with Prosper even after Suber’s departure.

“They’re terrific and we have a great relationship. If they do something, we’re definitely the banker for it,” said McLaughlin.

O’Malley’s commitment is steadfast “We will remain loyal,” he said.