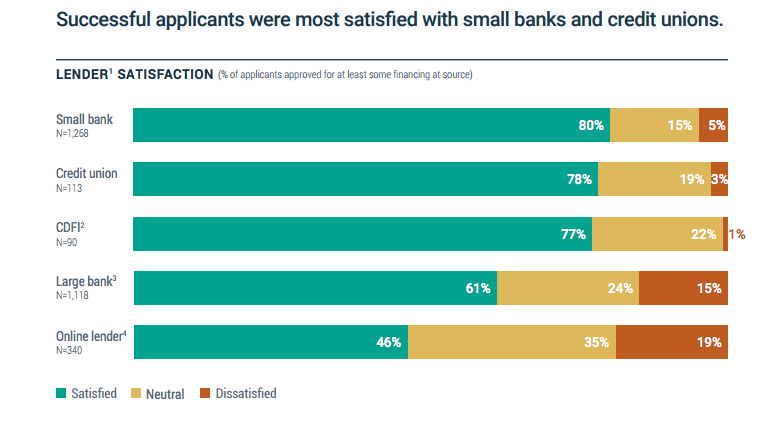

81% of Online Business Lending Borrowers Report Being Satisfied or Neutral

April 12, 2017The latest Small Business Credit Survey published by the Federal Reserve shows that 81% of small business borrowers were either satisfied or neutral about their online loan experience. Online lenders were defined as nonbank alternative and marketplace lenders, including Lending Club, OnDeck, CAN Capital, and PayPal Working Capital.

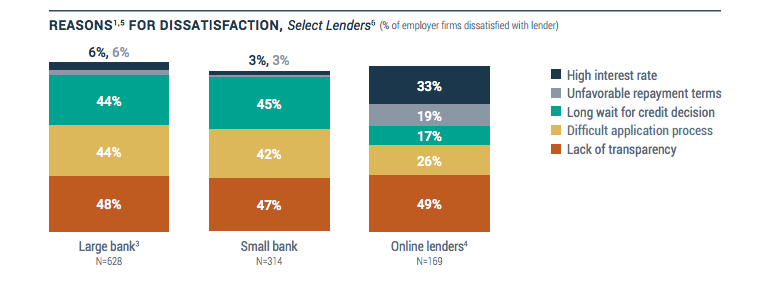

Of the 19% that were dissatisfied, nearly half cited transparency as a root cause. But that’s to be expected given that businesses dissatisfied with their loan from a large or small bank also cited transparency just as often.

While these charts indicate that there is still room for online lenders to improve, the 2016 report paints a more honest narrative than last year. Last year’s report used net satisfaction scores, which measured the difference between satisfied and dissatisfied borrowers. That methodology resulted in 15% net satisfaction for online lenders in 2015, which unless you read the fine print, easily misled even the most sophisticated of readers to conclude that only 15% of borrowers were satisfied. (Those readers included experts testifying in congressional hearings, the media, and government agencies, all of whom relied on that report to argue that online borrowers were terribly dissatisfied).

The 2016 report shows that businesses borrowing from an online lender were only slightly more likely to be dissatisfied than those that borrowed from a large bank (19% vs. 15%). And it’s the high interest rates that stand out to those dissatisfied online borrowers. 33% said that a high interest rate was the reason for their dissatisfaction. This is to be expected since non-banks inherently suffer from a higher cost of capital than banks.

Cash Advances?

Unfortunately, all of their data on “cash advances” is tainted. If they meant “merchant cash advances” or sales of future receivables, they should’ve specified such in the survey that went out to small businesses. Instead, the survey repeatedly asked about cash advances, a term most commonly associated with borrowing money through an ATM with a credit card. Those surveyed were also asked if they used personal loans, auto loans or mortgages so the multiple choice context suggests a credit card cash advance. Similarly, a cash advance could also mean a payday loan. With so many interpretations, the consequence is that it’s impossible to tell what the Federal Reserve meant or what those being surveyed thought they were being asked.

Notably, one question asked businesses if “portions of future sales” were used as collateral for a debt, but since merchant cash advances do not collateralize future sales (the future sales are actually sold, they don’t serve as collateral for a loan), it’s difficult to understand what they meant or how a respondent might interpret that.

Statistically representative?

The 2016 report also spends more time defending the Fed’s sampling methodology. Perhaps they are aware that their data is being put under the microscope.

Read the full Fed report here

Managing Risk in Small Business Lending

March 16, 2017 Two years ago, I left a promising career at PayPal, a major technology giant, for what some considered a risky move: I joined BlueVine, a young fintech startup. My title: vice president of risk.

Two years ago, I left a promising career at PayPal, a major technology giant, for what some considered a risky move: I joined BlueVine, a young fintech startup. My title: vice president of risk.

This year, I took on an even bigger role when I was named chief risk officer of the Silicon Valley company, which offers working capital financing to small and medium-sized businesses.

My promotion comes at a time when risk is becoming a bigger concern in fintech, which is ushering in big changes in banking and financial services.

Fintech revolutionizes financial services

Data science technology has dramatically improved access to financing and the way we manage our money. The fintech wave that began with my former company, PayPal, and the world of payments, has spread to other aspects of personal finance, from mortgages to student and auto loans to investing.

This expansion was accompanied by growing concern that the fintech boom is fraught with risks that, if left unchecked, could lead to a major bust in the financial services industry that could in turn cause harm to the broader economy.

In a speech in January, Mark Carney, the governor of the Bank of England, cited the need to “ensure that fintech develops in a way that maximises the opportunities and minimises the risks for society.” “After all, the history of financial innovation is littered with examples that led to early booms, growing unintended consequences, and eventual busts,” he said.

Risk management as key to success

Risk management certainly has been a focus area for BlueVine from the beginning.

BlueVine joined the revolution in small business financing in 2014 when it rolled out an innovative online invoice factoring platform.

Factoring is a 4,000-year old financing system that allows small businesses to get advances on their unpaid invoices by providing easy, convenient access to working capital. BlueVine transformed what had been a slow, clunky, paper-based solution into a flexible and convenient online financing system that enables entrepreneurs to plug cash flow gaps that often hamper business growth.

Because the BlueVine platform is based on cutting-edge data science technology that can process and analyze information to make quick funding decisions, managing risk inevitably became a major challenge in building our business. As Eyal Lifshiftz, our founder and CEO, recalled in a recent column, in BlueVine’s first month of operation, almost every other borrower defaulted.

In fact, that was partly the reason Eyal invited me to join his team. BlueVine serves small and medium-sized businesses seeking substantial working capital financing of up to $2 million. To succeed, we needed to build a robust data and risk infrastructure.

Small startup with big data needs

Joining BlueVine also posed a personal challenge.

At PayPal, where I started as a fraud analyst and then moved into the company’s data science division where I helped develop behavior-based risk models, I had enormous amounts of data to work with to do my job. Now, I was joining a young startup with very limited data history, but with big data needs.

This meant putting together exceptional and experienced teams of data scientists and underwriters and developing a technology that becomes progressively more precise and accurate as it draw lessons from our steadily expanding data and underwriting decisions. It was important for us to have a group of super smart, highly-motivated and technologically-strong people working closely with a team of experienced and sharp underwriters.

Here’s how the process works: Our underwriters develop a robust methodology which is then translated into detailed logic decision trees.

Each decision tree includes dozens, even hundreds of branches, made up of question sets on different underwriting situations.

For example, a decision tree could focus on approving new clients coming from a specific industry, such as transportation or construction, or on increasing the credit line for a client with a specific financial profile.

A typical decision tree would drill down on further financial questions: What’s the expected cash-flow of the business in three to six months? What’s the pace at which it has accumulated debt over the past year? Are the business sales seasonal in a material way?

The questions could also focus on non-financial areas: Does the company’s website look professional? How does it compare with major companies in its industry? Does the business actively maintain its Facebook and Twitter accounts?

The goal is to build a risk infrastructure that steadily becomes more efficient in answering questions in an automated, large-scale and highly accurate manner. Our data scientists leverage multiple external data sources and use dynamic advanced machine learning models to answer these questions pretty much in real-time and with a high degree of accuracy.

So it’s a combination of technology and human input. There will always be gray areas, questions and situations that cannot immediately be addressed by our computer models.

But as the models get better and more robust, the gray areas will shrink. Our models are constantly and automatically enhanced, re-trained and expanded by the most recent data and input from our underwriters.

Think of it as the fintech version of Deep Blue and AlphaGo, the powerful computer programs that famously outplayed topnotch chess grandmasters. Both programs were based on similar principles: the more they played, the more knowledge they absorbed and the more formidable they became at chess.

Technology and teamwork

An even better example is the self-driving car powered by Google’s artificial intelligence technology. Human input is still required, but the more driving the car does, the smarter and more autonomous it becomes.

Building our risk infrastructure is an ongoing process for BlueVine. But it already has helped us steadily expand our reach, making us stronger, smarter and even faster in financing small and medium-sized businesses.

In just a couple of years, the strides we’ve made in managing risk more effectively enabled us to increase our credit lines to $2 million for invoice factoring and $100,000 for business lines of credit, which means we’ve been able to serve bigger businesses with bigger financing needs.

While we initially focused mainly on small businesses with annual revenue of under $250,000, today we have an increasing number of clients with annual sales of more than $1 million and increasingly, we’ve been able to serve clients with revenue of more than $10 million a year.

By the end of 2016, BlueVine had funded roughly $200 million. We’re on track to fund half a billion dollars by the end of this year.

We’ve accomplished this in a time of heightened skepticism about fintech in general and alternative business lending in particular. But rather than scoff at this skepticism, I’d point out two things.

First, fear often accompanies the rise of a new technology. Second, in the wake of the 2009 financial crisis, it’s prudent to raise hard questions about the rapid emergence of new financial technologies.

While building technologies and companies that can provide financial services faster and easier is a laudable goal, It’s wise to move cautiously and with humility.

The BlueVine experience underscores this.

Risk is still a challenge we take on every day. But we have found ways to take it on confidently and effectively with a vigorous combination of technology and teamwork.

Ido Lustig is Chief Risk Officer of BlueVine.

On The Line With BlueVine After a Big Year

March 13, 2017 Helping businesses get paid on their invoices faster is a big market. So big, in fact, that when I met up with BlueVine CEO Eyal Lifshitz at LendIt last week, his company had just recently secured a $75 million warehouse credit line with Fortress. BlueVine had also just come off of a big year in which they provided more than $200 million to small businesses, earning them a spot in our rankings.

Helping businesses get paid on their invoices faster is a big market. So big, in fact, that when I met up with BlueVine CEO Eyal Lifshitz at LendIt last week, his company had just recently secured a $75 million warehouse credit line with Fortress. BlueVine had also just come off of a big year in which they provided more than $200 million to small businesses, earning them a spot in our rankings.

BlueVine’s success comes at a time when some in the online lending space have lost their luster. Lifshitz feels his company, however, is positioned well. “The time of exuberance has disappeared,” Lifshitz says. “Investors are looking to create value.”

Part of what makes them different is that they not only factor invoices, but they also provide lines of credit to prime and near-prime customers. Factoring is still a bigger percentage of their overall business, Lifshitz says, but he asserts that their credit line segment is growing at a faster clip. And he insists that they are working on other products too, not just loans. It sounds like the beginnings of a bank, I tell him, while making references to SoFi and their ability to live on the threshold of banking without actually currently being one.

“People have been saying that PayPal would become a bank forever but they haven’t become one,” he points out.

Still, running a company as big as his does require prudent decisions. “We are very mindful of how we manage capital,” he says. I ask if he thinks his business model protects them from an economic downturn. “It doesn’t protect it,” he asserts. Instead, he explains, his model gives him the ability to make adjustments rapidly. Since BlueVine’s capital is typically repaid in a matter of months, they can react to economic changes quickly.

Big name backers aren’t afraid to show that they believe in this either since they have been funded by Lightspeed Venture Partners, 83NORTH, Correlation Ventures, Menlo Ventures, Rakuten Fintech Fund and other private investors. A recent announcement by BlueVine says that they are on track to fund approximately $500 million to small businesses in 2017.

Brief: Former CAN Capital CFO Moves On

March 9, 2017According to the WSJ, Aman Verjee, who was CAN Capital’s CFO up until late last year, has taken the COO position at 500 Startups. The company has invested in more than 1,800 startups across more than 60 countries. According to the website, “500 Startups was founded in 2010 by former PayPal and Google alumni Dave McClure and Christine Tsai, along with many other friends and supporters.”

CAN Capital has not yet named a replacement CFO.

The Top Small Business Funders of 2016

March 6, 2017The MCA and small business lending origination numbers for 2016 are in. In some cases, a company may have merely placed or facilitated an acquired customer with a partner or competitor (but still counted them in their annual volume) and thus the figures do not necessarily represent what actually went on balance sheet. The rankings omit some larger players for which no data could be confirmed and when a reasonable estimate could not be made.

| Company Name | 2016 Origination Volume | 2015 | 2014 |

| OnDeck | $2,400,000,000 | $1,900,000,000 | $1,200,000,000 |

| PayPal Working Capital | $1,500,000,000* | $900,000,000* | $250,000,000* |

| Kabbage | $1,250,000,000 | $1,000,000,000 | $400,000,000 |

| CAN Capital | $1,100,000,000* | $1,500,000,000* | $1,000,000,000* |

| Square Capital | $798,000,000 | $400,000,000 | $100,000,000 |

| Bizfi | $550,000,000 | $480,000,000 | $277,000,000 |

| Yellowstone Capital | $460,000,000 | $422,000,000 | $290,000,000 |

| Strategic Funding | $375,000,000 | $375,000,000 | $280,000,000 |

| National Funding | $350,000,000 | $293,000,000 | |

| BFS Capital | $300,000,000 | ||

| BlueVine | $200,000,000* | ||

| Platinum Rapid Funding Group | $180,000,000 | $100,000,000 | |

| IOU Financial | $107,600,000* | $146,400,000 | $100,000,000 |

*Asterisks signify that the figure is an estimate

AutoFi Unveils Online Multi-Lender Sales Solution for Used Car Dealers

February 27, 2017SAN FRANCISCO, CA (February 27th, 2017) – Today AutoFi, a financial technology company that is transforming the way cars are bought and sold, announced the launch of the first fully online sales and multi-lender financing solution for used car dealers. Financing on AutoFi’s platform will be provided by its lender network of banks, speciality lenders, and credit unions. Today, the company announced that its credit union financing will be offered in partnership with iLendingDIRECT.

- “People want buying a car to be fast, straight forward and more transparent. That’s why AutoFi is working with lenders and dealerships to make the process easier through online sales and financing.” said Kevin Singerman, CEO of AutoFi. “That’s why I’m so excited about our partnership with iLendingDIRECT. Bringing iLendingDIRECT’s network of credit unions onto the AutoFi platform means consumers will have even more competitive financing options to choose from when purchasing a car online.

- “This is the perfect e-commerce solution to get customers the auto financing they need and want in a quick and efficient manner, and enhance their car-buying experience,” said Nancy Fitzgerald, President and CEO of iLendingDIRECT.

The AutoFi platform is the first online point-of-sale solution for auto finance. It allows customers to purchase and finance a car completely online, either through a dealer’s website or an in-store digital experience. The company recently announced the world’s first online car sales and financing solution for new car dealers in partnership with Ford Motor Credit. Today’s announcement further expands AutoFi’s ability to serve the multi-billion-dollar used car sales market through its partnership with iLendingDirect.

AutoFi’s platform will now allow used car buyers to research a vehicle on the dealership’s website; select “Buy Now”; receive an automated credit decision; and get loan offers from banks, specialty lenders and iLendingDIRECT’s credit union network who compete for the car buyer’s business in real time. Consumers can then customize their financing deal by selecting down payment and loan terms; choose vehicle protection products; and e-sign all financing documents online. The new platform gives used car dealers and buyers the ability to transact online with competitive financing options in a fully automated process.

# # #

About AutoFi

AutoFi is a technology company transforming the way cars are bought and sold. The company’s platform allows auto dealers to sell cars completely online by connecting buyers with lenders in a fast, easy and transparent process. AutoFi’s team includes industry leaders from enterprise software, finance, automobile and consumer sectors who previously worked at companies including Lending Club, PayPal, and SunGard. AutoFi’s investors include Ford Motor Credit Company, Crosslink Capital, Lerer Hippeau Ventures, Laconia Capital Group, Basset Investment Group, Eniac Ventures, 500 Startups and Silicon Valley Bank. For more information visit www.autofi.com

About iLendingDIRECT

iLendingDIRECT is a national Finance and Insurance marketing firm that focuses on Auto Refinancing. We offer smart financial solutions with the customers’ well‐being in mind – committed to setting our customers up for success by saving them money and educating them about what is best for their particular financial situation. For more information on iLendingDIRECT services, visit www.ilendingdirect.com.

The LendIt Story

February 12, 2017

The LendIt Conference was supposed to be a smallish local meetup for New York-based members of the online lending community. But founders Jason Jones and Bo Brustkern soon discovered they had the makings of a big annual industrywide national convention. And before long, they found themselves replicating their successful American show on other continents.

To understand how the trade show was born and how it’s matured, flash back about seven years. In 2010, Jones and Brustkern were putting together venture capital deals when they happened onto the fledgling peer-to-peer lending movement. “Consumer credit was something we weren’t all that knowledgeable about, but we could see the market was large,” recalls Jones. “There was a clear opportunity that was structural in the market, and there were stable, consistent returns.” So the two of them launched one of the first P2P funds.

Their lending business soon took off, but Jones and Brustkern felt they were working in a void. The industry lacked community, and they decided to do something about it. Jones contacted his friend, Dara Albright, who had been organizing a series of crowdfunding conferences for Wall Street starting in mid 2011.

To heighten the credibility of the new confab, Jones, Brustkern and Albright decided to seek the help of Peter Renton. They didn’t know Renton personally but considered him “the voice of the industry,” Jones says. Renton had nurtured and sold off two printing businesses and used the proceeds to take up online lending as a hobby. He had also launched the Lend Academy in 2010 to teach the world about peer-to-peer lending. Somehow, he had also found the time to develop a following for himself as a blogger.

In early January of 2013, Jones and Albright cold-called Renton to gauge his interest in putting on a show. As fate would have it, Renton had just made a New Year’s resolution to launch a conference for lenders and was receptive to joining up. Together, they put a plan in action.

The originators put up their own money and worked together daily from January to June of 2013, when the first show convened. They secured space that would contain 220 people and calculated their break-even point as 200 attendees. “This was never intended to be a profitable enterprise,” Jones says of those early days. “This was something we all wanted to do for the community. We thought that if we wanted it, others would want it.”

More than 400 people registered for that first conference. “We had a line literally out the door,” Jones notes. “We had to shut off registration. We ended up squeezing about 375 people into that first event. It was completely shocking to us.” From the beginning, attendees came from all over the world. “That’s when I learned China had a P2P industry,” Jones says.

After the initial event, Jones, Brustkern and Renton formed a unified company. Renton brought in Lend Academy, while Jones and Brustkern added their investment fund. The conference also became part of the united company. Ever since, a holding company has owned all three businesses. Dara went on to launch Fintech Revolution TV and continues to support LendIt.

From the initial attendance of 375, the U.S. conference grew to 975 attendees in 2014, 2,500 in 2015, 3,500 in 2016 and a projected 5,000 for this year. About 33 percent of attendees come from the fintech industry, 23 percent are investors, 23 percent are service providers, 14 percent are banks and 2 percent come from government, the media and other backgrounds, Jones says. At first, many of the attendees come from the ranks of CEOs and managing partners, but that’s changing as the industry comes to view the conference as an annual convention where lower-ranking members of an organization can learn about the business, he notes.

Meanwhile, the exhibition floor is becoming an increasingly important component of the show. The gathering attracted 18 exhibitors in 2013, followed by 47 in 2014, 112 in 2015, 177 last year and an expected 210 this year. “We’re transforming from a conference-led event to an expo-led event,” Jones says. This year, exhibitor booths will occupy a 120,000 square-foot hall in New York’s Jacob K. Javits Convention Center.

The U.S. LendIt conferences alternate between San Francisco and New York City, renting larger spaces as the show has grown, Jones explains. Two years ago, the gathering seemed cramped in the gigantic New York Marriott Marquis near Times Square, he says, necessitating this year’s move to the Javits Center. Javits is designed for conventions with at least 10,000 attendees so the show is a little small for that venue, he admits. But the facility could become LendIt’s long-time New York home as growth continues, he predicts.

Jones traces some of the growth in exhibitors to the expansion of the fintech industry. “You have a meeting of the start-ups with the more traditional players who are rethinking their businesses and how to apply the new technology that’s being developed into their businesses,” he says.

Conferences that compete with LendIt in the fintech category are proliferating because of the nature of industry, in Jones’ view. As soon as fintech companies are launched, the internet quickly makes them national or even international in scope, he says. At the same time, the anonymity of cyberspace creates a need for gatherings that provide face-to-face meetings, he maintains. “They live online,” he says. “The spend their year online so there is a need for a convention to meet with their peers, their clients, their service-providers, their customers, their suppliers. There is a need for that physical connection.”

The increase in fintech conferences is also driven by content-related companies that provide articles on fintech innovation. Those sites have regarded conferences as money-makers that complement their journalistic endeavors, Jones says. For example, TechCrunch, an online publisher of technology industry news, puts on the TechCrunch Disrupt conferences in San Francisco, New York City, London and Beijing. In another example, Business Insider conducts the IGNITION conference.

Those forces – the internet, globalization and web-based publishing – are making themselves felt in the convention business in general, not just in fintech, Jones notes. Event-related companies trade at roughly 12 times EBITDA (earnings before interest, tax, depreciation and amortization), he says, characterizing the convention business as “a very healthy category of our economy.”

Still, the fintech field’s crowded with more than 30 conferences, but LendIt is succeeding because of its early start and an emphasis on community, according to Jones. “We come from the industry,” he contends. “People are happy with what we can produce. They love our content so they come to learn.” Because the conference has become established, the media outlets focus on covering it, which encourages businesses to use it as a stage for introducing products or announcing mergers and acquisitions, he maintains.

Jones views LendIt and Money20/20 as the largest pure-play fintech conferences. The latter, which attracts 11,000 attendees, focuses on payments and contains a “layer” of fintech, while LendIt specializes in lending and likewise offers a “layer” of fintech, he says. Payments and lending represent the two biggest categories in fintech, so the structure of the shows makes sense, he suggests. By chance, Money20/20 occurs in the fall and LendIt takes place in spring, creating what he considers a “nice balance” that encourages prospective attendees to go to both shows.

Finovate holds a rival fintech conference that focuses more narrowly on innovation than do the LendIt and Money20/20 shows, Jones says. A competing bank securitization conference offers information on lending but doesn’t address fintech in great detail, he says.

While LendIt has been coming of age in the U.S., it’s also gained siblings in Shanghai and London. The Chinese edition of the show, which made its debut in 2014, ranks as the largest fintech show in Asia. The Chinese fintech market has grown to at least five times the size of any other market in the world, and it’s home to four of the world’s five largest fintech companies, Jones says. “We were completely blown away,” he says of learning about the industry during a visit to China.

Despite the language barrier and the challenges of dealing with an unfamiliar culture, LendIt has managed to prosper in China. Through a joint venture with a local financial think tank, LendIt helped produce annual Chinese events known as the Bund Summit for two years with attendance capped at 500. For the third year, LendIt parted ways with its partner and recast the show as a larger event. After the change, the confab, now called the Lang Di Fintech Conference, attracted 1,200 attendees, making it China’s largest. “There’s a ton of future opportunity,” Jones predicts of the China endeavor. “We want to be the annual convention for the Chinese fintech industry.”

Although it’s difficult to set up operations in China, cooperation has prevailed there in at least some areas. “The government has been quite supportive,” Jones says of of Chinese officials. “They appreciate what we’re trying to do there.” In January, LendIt launched its Chinese language daily news feed.

Thousands of miles away, the European-based LendIt confab ranks second in size on that continent only to the European version of Money20/20, Jones says. Attendance at the London-based LendIt show numbered 450 in 2014, which was its initial year. It climbed to 800 in 2015 and reached 925 last year.

Putting on the European event requires much less effort than the Asian version because it’s almost an extension of the U.S. original, he says. It’s dominated by firms from the United Kingdom but draws a smattering of companies from other European nations. Crossing borders presents challenges for European fintech companies, which keeps the industry’s companies smaller there than in the U.S. and China, but that may change, he believes. “There’s a lot of innovation there, but they still have a ways to go,” he says.

To handle its far-flung operations, LendIt relies on 20 full-time employees, 11 contractors and 10 people working in a joint venture in China for a total of 41 staff members. “These events are incredibly large shows, and we constantly feel understaffed,” Jones says. That feeling prevails despite recent additions to the staff, he notes.

And additional opportunity beckons in myriad locations. “The challenge is, do you have a bunch of conferences all over the world, or do you do a beachhead and pull people to those three events?” Jones wonders aloud when asked about the future. “For the moment, we have made the strategic decision to stick with these three events and go deeper with them. But there are so many opportunities all around the world. We’re constantly being asked to come to different countries.” Then, too, LendIt could convene smaller, one-day events around the glove as feeders to the three main conventions, he allows. “That’s something we’re batting around now.”

The established two-day conferences could also grow into three-day affairs – but not right away, Jones suggests. “We’re totally running out of time,” he says of trying to cram in all the speakers and exhibitors that LendIt would like to present. Stretching the format could create conflicts because some participants attend other events immediately before or after LendIt.

Notable LendIt speakers have included Larry Summers, who’s served as Harvard president and U.S. Treasury Secretary; Karen Mills, former administrator of the U.S. Small Business Administration; John Williams, president and CEO of the Federal Reserve Bank of San Francisco; and Peter Thiel, venture capitalist and member of the Trump transition team. This year, attendees can look forward to meeting the robot that represents Watson, the IBM computer. Watson will take the stage to field questions about fintech. For Jones, however, creating a conference isn’t just about the big-name speakers be they human or mechanical. “People who are lesser-known can be really fascinating,” he says.

Whoever handles the speaking duties, the LendIt Conference executives vow that they’re in it for the long run as the fintech industry’s annual convention during both boom times and economic slumps. As Jones puts it: “We want to be a reflection of our industry.”

Ford Credit and AutoFi Debut Platform for Faster, Smoother, Simpler Digital Vehicle Buying and Financing

January 24, 2017- New platform allows customers to purchase and finance a new vehicle via the dealer website; platform introduced at Ohio dealership and will roll out over time to more U.S. Ford and Lincoln dealerships

- Platform makes it fast and convenient to finance a new Ford or Lincoln at a time when many U.S. adults say they want to spend less time at dealerships, while still going to their dealer to “sign and drive”

- Ford Credit makes equity investment in AutoFi as Ford Credit continues pursuing technology to make the financing experience better

There’s a new way for customers to purchase or finance a new Ford vehicle in minutes – right from a dealership website from anywhere, on any device – through a new platform from Ford Motor Credit Company and financial technology company AutoFi.

There’s a new way for customers to purchase or finance a new Ford vehicle in minutes – right from a dealership website from anywhere, on any device – through a new platform from Ford Motor Credit Company and financial technology company AutoFi.

In addition, Ford Credit has made an investment in AutoFi as Ford Credit continues pursuing technological advances to make the financing experience better.

“By combining our fast and efficient credit-decision process with AutoFi’s online capability, we are making the customer experience faster, smoother and simpler,” said Lee Jelenic, Ford Credit director of mobility. “With its experience in used-vehicle online financing and well-developed platform, AutoFi makes it easier for us to adopt new technology quickly to meet evolving consumer expectations.”

The AutoFi platform can be used now at Ricart Ford in Groveport, Ohio, and will roll out over time to more Ford and Lincoln dealerships across the United States. The introduction comes as 83 percent of Americans say they would like to spend as little time at the dealership as possible when shopping for or buying a car, according to a new survey of more than 1,000 U.S. adults conducted online by Harris Poll on behalf of Ford Motor Company. Many of those same people, however, still want to touch and feel their new vehicle before signing on the dotted line. The new platform provides the best of both worlds.

Through the dealer website, customers have a transparent and seamless purchase and finance experience from anywhere on their mobile phone, tablet or computer. Once the online part of the transaction is complete, all customers need to do is sign the paperwork when they collect their new Ford.

Consumers may shop for a new Ford in the showroom or from anywhere via the Ricart Ford website. After selecting a vehicle, they can apply for credit and receive a decision, choose the financing terms that make sense for them, and then review and select optional vehicle protection products – completely online on their own time. Customers then can review a final summary of the financing terms and schedule time to complete the transaction and pick up the vehicle.

“AutoFi’s platform will help cut the time people spend arranging financing and improve the experience dealerships can deliver for their customers, no matter where they are in the car-buying journey,” said Kevin Singerman, CEO of San Francisco-based AutoFi. “We think this will be a game changer for both consumers and dealers, and we are thrilled to work with Ford Credit to make this happen.”

“Technology is transforming just about every type of financed consumer purchase, and this new digital capability will help make that change for automotive purchases and deliver great experiences,” said Rick Ricart, Sales and Marketing vice president at Ricart Ford. “We are excited to be the first Ford dealership in the pilot.”

# # #

About Ford Motor Credit Company

Ford Motor Credit Company is a leading automotive financial services company. It provides dealer and customer financing to support the sale of Ford Motor Company products around the world, including through Lincoln Automotive Financial Services in the United States, Canada and China. Ford Credit is a subsidiary of Ford established in 1959. For more information, visit www.fordcredit.com or www.lincolnafs.com.

About AutoFi

AutoFi is a technology company transforming the way cars are bought and sold. The company’s platform allows auto dealers to sell vehicles completely online by connecting buyers with lenders in a fast, easy and transparent process. AutoFi’s team includes industry leaders from enterprise software, finance, automobile and consumer sectors who previously worked at companies including Lending Club, PayPal, and SunGard. AutoFi’s investors include Ford Motor Credit Company, Crosslink Capital, Lerer Hippeau Ventures, Laconia Capital Group, Basset Investment Group, Eniac Ventures, 500 Startups and Silicon Valley Bank. For more information, visit www.autofi.com.

About the Survey

This study was conducted online within the United States by Harris Poll on behalf of Ford Motor Company between November 28 and December 5, 2016, among a nationally representative sample of 1,217 adults ages 18 years and older. This online survey is not based on a probability sample and therefore no estimate of theoretical sampling error can be calculated.

Contacts

Ford Credit

Margaret Mellott

313.322.5393

mmellott@ford.com

or

AutoFi

Justin Hamilton

202.630.5426

Media@autofi.com