Tech-based Lenders Clobbered On Dose of Bad Economic News

June 29, 2015How would tech-based lenders fare in a slumping market? Not very well apparently…

OnDeck (ONDK) and Lending Club (LC) set new record lows earlier today amid bad news coming out of Greece and Puerto Rico. OnDeck is down almost 43% from its IPO price and down 61% from its all time high. It was down more than 8% today even though the Dow was only down 2%.

$ONDK was unaware that it focused on Greek loans…. interesting 8.6% drop.

— Mark Holder (@StoneFoxCapital) Jun. 29 at 05:48 PM

The downward trend was dissected in a post that was published just hours before today’s further fall.

Meanwhile Lending Club is in new territory, down 3% from its IPO price and down 50% from its high. So what are investors saying about this?

$LC hmm i really dunno what to say about this…

— mike pham (@mincogneto) Jun. 29 at 05:30 PM

That’s kind of the overall gut feeling. Many feel this company is being unfairly dragged down and yet it continues to fall. A mounting campaign by the Puerto Rican government to declare bankruptcy and a Greek debt disaster clobbered everything today including Lending Club. One tweeter came up with a great idea last week, bail out Greece with a loan from Lending Club…

If all else fails with the IMF #Greece should just apply on @LendingClub pic.twitter.com/RbtnMm5JaO

— World First USA (@WorldFirstUS) June 22, 2015

Last week no one was even talking about Puerto Rico. Now all of the sudden they’re in a “death spiral.”

Watch the death spiral coverage on CNN

The market’s tech lending darlings might’ve gotten pummeled like everyone else but the ease with which they drop should probably be a warning sign. Neither offshore dilemma stands to have any impact on their businesses. So what would happen if a relevant issue were to arise such as a domestic disaster, a sudden rise in unemployment, a recession, a financial crisis, skyrocketing fuel prices, a steep increase in the fed funds rate, or even something no one dares talk about like a legal ruling that could jeopardize the entire bank charter model?

It’s quite possible that both companies haven’t bottomed out just yet….

——–

Note: I have no equity positions in either company. I do own Lending Club notes however.

Still Reviewing Paper Bank Statements? Stop

June 26, 2015 Are the bank statements you received legitimate? Underwriters in the business financing industry are scouring paper documents for abnormalities hoping to catch fraud in the inducement. And word on the street is that small business owners are doctoring statements and engaging in trickery in record numbers.

Are the bank statements you received legitimate? Underwriters in the business financing industry are scouring paper documents for abnormalities hoping to catch fraud in the inducement. And word on the street is that small business owners are doctoring statements and engaging in trickery in record numbers.

Technology has made it easier to create authentic looking documents and the rise in online lending seems to be bringing out the worst in people. Somebody in a desperate situation might not have the guts to look a banker in the eye and hand him a stack of fraudulent documents but they might roll the dice with somebody over the Internet they’ll never have to meet.

The fakes aren’t obvious anymore. Anyone can go online and buy doctored documents from professionals. The business is booming on Craigslist for example where fraudulent documents can be made to order in under an hour.

In the Miami area, fraud hucksters are even beginning to offer deals such as buy 2 fake documents, get 1 free.

Industry-wide, funding companies are complaining that attempted fraud is out of control. One broker recently took to the dailyfunder forum to share her frustration. “I can spot them a mile away!!! 2 different deals submitted this week with fraudulent statements!!!,” she vented.

Other brokers chimed in, sharing their stories such as a merchant whose doctored statements were only noticed because ATM withdrawals were listed with odd amounts like $90.83.

Oddly, nobody seems to be reporting this fraud to the authorities. It all seems to get swept under the rug as business as usual. Orchard co-founder David Snitkoff for example, was asked just last month about the rate of marketplace lending fraud and he apparently said, “No worries, none to date.” He seemed to be implying that fraudulent applicants are getting screened out. But that doesn’t mean people aren’t trying.

Seven months ago, merchant cash advance underwriter Pierre Mena wrote in detail about the challenges he faces in detecting fraud. He said:

Some of the more well hidden fraud can usually be found by comparing the summary page and last page of the bank statement to other statements. Typically, most banks and some credit unions offer you a snapshot of the starting balance, which should generally match up with the ending balance of the previous month. If it doesn’t, you should look for any transactions from the previous month that did not settle until the current month. If there is none, this is usually a red flag indicating that the merchant forgot that statements are continual time series financial data whose totals carry on to the following month.

-Pierre Mena, Rapid Capital Funding

A lot of these issues can be easily overcome by simply disregarding paper statements altogether. Microbilt’s instant bank verification tool for example, will allow you to pull the most recent 90 days worth of transaction data directly from the banks themselves. Funders using these automated checks swear by their effectiveness and the capability is essential for any company that wants to scale.

But a recent conversation with the owners of a broker shop in NYC said this is easier said than done. Merchants are still using fax machines to send statements or claiming they don’t have access to computers or email accounts, they said. They added that their clients would suffer if approvals were completely contingent upon online verifications.

But a recent conversation with the owners of a broker shop in NYC said this is easier said than done. Merchants are still using fax machines to send statements or claiming they don’t have access to computers or email accounts, they said. They added that their clients would suffer if approvals were completely contingent upon online verifications.

Cultural differences play a role in this according to Gil Zapata, the founder of Florida-based Lendinero. Zapata recently wrote that latino business owners over the age of 45 are not accustomed to doing business over the Internet, email, fax, or phone. “This group has a high level of distrust in doing business via the Internet,” he said.

So is there a middle ground? On the dailyfunder forum, Chad Otar, a managing partner of Excel Capital Management said that he tells merchants they can change their online banking passwords after a verification. And Andy McDonald of Yellowstone Capital wrote that verifying the bank data is beneficial for the merchants too. “It protects the merchant by allowing us to check their account to make sure our pulls aren’t going to bounce,” he wrote in a thread back in April. He also added that he comes across 2-3 applications PER DAY with altered statements.

Humans can only do so much. Pierre Mena actually wrote, “Some of these statements are doctored so well that you may have to zoom in upwards of 300% to find a comma that should actually be a period to separate dollars from cents.” At this point, an instant bank verification would probably work wonders.

Online business lender Kabbage might have the best model. On their website, applicants are instructed to enter their email address followed by their bank account username and password. Their system will analyze their bank transactions and if eligible, will then ask the applicant for their first and last name. It flies in the face of all the pushback that funders claim merchants give them over data privacy and security.

Four months ago Kabbage announced they were already up to funding $3 million per day. Obviously there is an entire segment of small business owners that are sucking up whatever concerns they had about bank verifications in order to get the capital they need.

The majority of the small business financing industry is still relying on paper statements and probably shouldn’t be. If you have to zoom in upwards of 300% to find a comma that should actually be a period and if con artists are offering discounts for bulk orders of fraudulent statements, it may be time to throw in the towel and join the rest of the world in using the Internet…

Dear Brokers, Investors Love You Too

June 25, 2015Hedge funds, private equity, and family offices have been all hot and bothered by lending marketplaces and direct funders for a while now, but there’s a new sexy stud that everybody wants to take to the dance, the brokers that originate the deals. An entire segment of the industry still calls them ISOs (Independent Sales Organizations) and in 2015, nobody can seem to shut up about them.

One minute brokers are being fingered as the source of the industry’s moral decline and the next minute they’re the lifeblood of it all.

Ever since World Business Lenders began acquiring broker shops and converting them into franchisees, the institutional investors suddenly woke up.

They’re Buying Brokers? BUT WHY?!

Over the years, dozens of funders have opened for business and then realized they don’t know how to get deals or where to get them from.

It’s not a build-it-and-they-will-come industry anymore. As much as certain people try to berate brokers, it’s widely believed that they still control up to 50% of the industry’s deal flow. Institutional investors examining portfolios have taken notice that some funders are successful only because they have a loyal group of broker shops. So if the brokers make the funder, then why not court the brokers?

And so they’re doing just that…

If you’re brokering less than a million a month though, you’re not really investment material yet. There’s thresholds. The more volume you produce, the more options at your disposal.

At this size, you’re really just a couple of dudes (or dudettes) sitting in a room with phones. There’s not enough action to get anyone excited. There may be some potential to get an investor to co-syndicate with you, but that’s it.

$1 Million/month to $4 Million/month

Congratulations, you’re not just a bunch of dudes anymore. If you’re using decent software, hopefully you can print out the necessary reports to woo investors. At this level you’re eligible for co-syndication, an advance rate to fund your own deals, or to be rolled up as a franchisee. If you’ve got a criminal record or have been banned by the SEC, then forget it though.

$4 Million+

If you’re not already funding your own deals at this point, you’re going to be encouraged to by an investor. They’ll want to set you up on a platform that they trust and participate in the funding in some way. You can get a credit facility. You’re also acquisition material. Funders and investors have little interest in acquiring a couple of dudes sitting in a room because there’s no actual assets to value. At $4 million a month and more, there may potentially be something beyond just the dudes running the company and therefore something to consider. If you can’t pass a criminal background check though, then forget it. And if you’re running scrappy like a $200k/month shop, then they’re not really going to be able to help you. It doesn’t help if you’re stack-heavy either.

But just because you do the volume, that doesn’t mean you can just show an investor an Excel spreadsheet and hope that they’ll fork over millions of dollars in return. You have to run your shop like a professional, not a dude (or dudette of course). And if you think you meet that criteria, that’s great news, because investors want to talk to you really badly.

But just because you do the volume, that doesn’t mean you can just show an investor an Excel spreadsheet and hope that they’ll fork over millions of dollars in return. You have to run your shop like a professional, not a dude (or dudette of course). And if you think you meet that criteria, that’s great news, because investors want to talk to you really badly.

Last year, every banker I sat down with told me they were looking to invest in the next OnDeck or CAN Capital. And what happened was, you had 200 bankers competing for the same handful of deals. This year, the conversations are all about brokers.

“Who wants to become a funder?”

“Who needs money to syndicate?”

“Who is serious about growing their broker shop?”

Did someone say Year of the Broker?

It damn sure is. If you’re funding more than a million a month, don’t rely on stacking, don’t have a criminal record, have actual reporting systems (not Excel), and want to be a funder or participate in more deals, then there’s a group of investors that are ready and willing to swipe right.

You might not be the next OnDeck and that’s okay. If you’ve got the flow, you can get the dough. <3 😉

Coming to the Rescue: Consolidation Can Save Merchants

June 24, 2015 In the last 18 months, funders have begun offering consolidations that combine more than one advance. First, the funders buy out the merchant’s existing advances. Then funders lower the percentage collected from a merchant’s card receipts or debited by ACH. Sometimes, consolidation can even include an infusion of cash for the merchant.

In the last 18 months, funders have begun offering consolidations that combine more than one advance. First, the funders buy out the merchant’s existing advances. Then funders lower the percentage collected from a merchant’s card receipts or debited by ACH. Sometimes, consolidation can even include an infusion of cash for the merchant.

“Consolidations are a way to help merchants avoid defaulting,” said Chad Otar, managing partner at New York-based Excel Capital. Consolidation works if the buyout price is low enough and the terms allow enough room to handle the obligation.

“It can free up some cash and give the merchant some room to breathe, sustain the business and avoid taking on more debt,” he noted.

It’s helpful to think of consolidation as the equivalent of refinancing a house, according to Stephen Halasnik, managing partner at Payroll Financing Solutions, a Ridgewood N.J.-based direct lender. Payroll has been offering the service for about six months, he said.

Brokers and funders can benefit from consolidation because it puts a merchant back on track towards long-term sustainability, said a broker who requested anonymity. Moreover, the broker said that one in three of the potential deals he sees have multiple advances outstanding, which means companies could lose an alarming chunk of market share by declining too many potential funding candidates. “That’s what I believe the catalyst was to opening the doors to consolidation,” he contended.

SECRET TO SUCCESS

Success in consolidation lies in finding merchants worthy of another chance, said Otar. Clients who have taken two or three advances but stick to the new plan and stop stacking advances from other brokers have a reasonably good chance of succeeding, he said. His company can work with a merchant that has as many as three advances outstanding if they have sufficient revenue.

Otar provided the example of a merchant who’s diverting 20% of his gross revenue to three advances. Together, the advances have led to a total of $50,000 in future revenues sold. If the merchant generates enough monthly revenue to qualify for $100,000, Excel can buy out the three advances, provide the merchant with $50,000 in cash, and lower the payment to 8% to 12% of gross revenue. “All of a sudden they have all this cash flow to play with that really wasn’t there,” he said of merchants in that situation. “They tend to do really well.”

Halasnik of Payroll Financing Solutions offered the example of a trucking company that had taken three advances and was delivering a total of $1,138 a day on average to the funders. Payroll bought out the three funders and is charging the trucker $615 a day.

One of Payroll’s clients needed to repair a commercial vehicle but already had too many advances and couldn’t get another, Halasnik said. Payroll consolidated the positions and lowered the payment, enabling the merchant to save enough money in two weeks to have the vehicle fixed.

To qualify for a consolidation, the merchant has to meet the “50% Rule” by netting 50% of what Excel is offering, Otar said. Between 40% and 50% of the distressed merchants that the company considers for consolidation meet that criterion, he said. An additional 30% of the merchants can meet that standard in the near future, once they’re further along on their agreements.

Under the 50% Rule, a merchant that is still obliged to deliver $70,000 and qualifies for $100,000 would not be a candidate for consolidation, Otar said. In that situation, a merchant can wait until he has delivered more of the sold revenues to the funders and then get a consolidation, he said. “In the meantime, don’t take on any more debt,” Otar tells the merchants. That too could impact their ability to sell additional revenue streams in return for cash upfront down the road.

Some merchants combine debt and advances, seeking advances only after maxing out their credit lines, said Otar. More commonly, however, it’s a matter of stacking advances, he said. “When we see there are three, four, five, six, seven cash advances out, that’s a merchant we tend to stay away from,” he noted.

Some merchants combine debt and advances, seeking advances only after maxing out their credit lines, said Otar. More commonly, however, it’s a matter of stacking advances, he said. “When we see there are three, four, five, six, seven cash advances out, that’s a merchant we tend to stay away from,” he noted.

Brokers should also bear in mind that every deal’s different, cautioned Steven Kamhi, who handles business development and ISO relationships at Nulook Capital, a Massapequa, N.Y.-based direct funder. “It has to be the right deal,” he advises.

Brokers can identify distressed merchants within the first two minutes of a phone conversation when they say things like, “I need the money right now,” Otar said. Looking at the paperwork, the broker can see within 10 minutes whether the potential client is hard-pressed.

Asking the right questions helps reveal distress quickly, sources said. That can include asking how many advances the merchant has outstanding, how much in future sales they still have to deliver and how much revenue they’re grossing monthly. Asking what company advanced them cash can reveal a lot if they’re working with less-reputable companies.

Listening’s under-rated, too. Merchants sometimes explain that they’re coming up with more ways of making money and are, therefore, making themselves a better bet for sustainability, Otar said.

OTHER WAYS OF HELPING

Brokers can make deals more palatable to some distressed merchants by deducting payments weekly instead of daily, Otar said. “It’s something I’m seeing a big migration toward,” he noted. “It’s a big selling point.” Manufacturers and contractors don’t have customers swiping cards every day and especially appreciate the change. More widely spaced payments can also fit better with some clients’ seasonal cash flow.

Besides consolidation, brokers can help distressed merchants by providing traditional accounts-receivable financing, which can prove particularly helpful for manufacturers and construction companies, Otar said.

Suppose Customer A owes a contractor $100, Otar said by way of example. The contractor can get $90 from the factor, and the factor collects the $100 from Customer A. The client pays the cost of the financing upfront but reduces the waiting time to receive the cash and avoids daily or monthly payments.

Accounts-receivable financing costs merchants much less than a cash advance, Otar noted. But putting the deal together takes longer than approving an advance, and merchants in immediate need of cash might not be able to wait.

In another example of helping merchants, Payroll had a client who was a bicycle shop owner with good credit and equity in a home, so it granted him an advance that gave him time to go to a bank and get a home equity loan. “I counseled him to do that and then buy us out,” Halasnik said.

PREVENTING DISTRESS

On the sales side of the business, brokers can help distressed merchants by preventing stacking from occurring in the first place, sources said. Otar recommended, “listening to the customer, understanding the business and offering a product that is going to benefit the customer in the long run.” That way, the broker positions himself to work with the client for years, not two or three months. “At the end of the day, they appreciate that,” he said.

Halasnik relies on his experience as a small-business owner who has operated a printing company, staffing company and nurse registry to help him understand aspects of a client’s business that people from a purely financial background might not fathom.

Brokers seeking long-term relationships should know a client’s business well enough to advise against taking on more financial obligations when the time isn’t right, agreed Payroll’s Halasnik. However, after the broker urges caution, the decision rests with the business owner, he maintained. “We are on the same page as the client,” Halasnik said. “We are looking out for their best interest because, ultimately, we have to get paid back.”

THE CASE AGAINST CONSOLIDATION

Some members of the industry prefer to avoid the consolidation trend. “The guy’s already shown that he’s going to go and take three or four advances,” said Isaac Stern, CEO of New York-based Yellowstone Capital. “Doesn’t history just show he’s going to do the same thing over again?”

Some members of the industry prefer to avoid the consolidation trend. “The guy’s already shown that he’s going to go and take three or four advances,” said Isaac Stern, CEO of New York-based Yellowstone Capital. “Doesn’t history just show he’s going to do the same thing over again?”

When a merchant’s overextended, he should wait before taking another advance, Stern said. But when some merchants are denied another advance, they immediately seek out another funder, he maintained.

Yellowstone has put together a few consolidations but chooses not to create too many, Stern said. Some merchants find themselves a month or two away from going out of business unless they can find a source of cash, he observed. “They’ve been declined for that last credit card, and things are getting really rough,” he said.

Some members of the industry advocate coming together to improve standards and provide training. Wall Street’s testing and licensing could serve as an example, suggested one source. Background checks could also help root out unethical players, he noted.

But creating a training and certification infrastructure would prove a formidable task, according to Stern. The industry would have a hard time agreeing upon who should head a trade association to administer the standards, he said. He views the industry as a collection of Type A personalities – sometimes defined as ambitious, over-achieving workaholics – who would resist consensus. “It’s a nice idea, but I don’t see it working,” he said.

REASON TO BELIEVE

Though industry players are contending with some distressed merchants, Stern noted that the average credit score of his company’s clients is beginning to rise as the economy improves.

Though statistics on distressed merchants aren’t readily available, other industry veterans feel they’re not encountering as many now as a year ago. However, they said they may see fewer cases of distress because bigger players are beginning to offer consolidations.

“A year ago, nobody would consider doing it,” a broker said of consolidation. But as funders become more open to the product when they see competitors using it to gain market share. “It’s becoming more mainstream,” he said.

How brokers market their services can also determine how many distressed merchants they encounter, sources said. Using the same prospect lists that competitors use can lead to calling on overextended clients, they maintained.

Whatever the number of distressed merchants may be, stacking sometimes makes sense, said Halasnik. What if a client needs $30,000 to win a contract, and a funder is willing to provide only $15,000, he asked rhetorically. Perhaps another funder will put in $15,000, too.

Problems arise, however, if the two funders don’t know the merchant has made two deals because they happened the same day. It’s the kind of situation that sours some members of the alternative-funding community to consolidation. As Halasnik put it: “You’re dealing with somebody who’s in trouble. It’s the highest risk a lender could take.”

Merchant Cash Advance: Do You Know What You’re Selling?

June 22, 2015 Continuing on with the Year of The Broker discussion, I want to now shift focus to the continued wave of new broker entrants that are not receiving sufficient training. I don’t believe that it’s so much the fault of the brokers, as it’s the fault of the companies they are reselling for. Those companies usually fail to provide a structured training regime. Training provided to new broker entrants is typically centered around the memorization of sales scripts, the practice of outdated rebuttals, and the repetition of lines that can end up sounding very canned and robotic.

Continuing on with the Year of The Broker discussion, I want to now shift focus to the continued wave of new broker entrants that are not receiving sufficient training. I don’t believe that it’s so much the fault of the brokers, as it’s the fault of the companies they are reselling for. Those companies usually fail to provide a structured training regime. Training provided to new broker entrants is typically centered around the memorization of sales scripts, the practice of outdated rebuttals, and the repetition of lines that can end up sounding very canned and robotic.

If I had to recommend new age sales training, I’d have to go with my favorite, which is Diagnostic Selling, promoted by the likes of Jeff Thull from Prime Resource Group (www.primeresource.com). Thull explains that as the sales consultant, you should be a valued source of business advantage for your client, rather than just a person that goes through a series of sales material regurgitation. You should have access to products, services, platforms, big data, knowledge, key players, new solutions, forecasts, trends, etc., that the merchant does not have access to, which allows them to see you as a “valued extension” of their organization. This leads to not just new client acquisition, but the real key to making money in our space, and that’s client longevity.

In order to truly achieve this level of sales consultancy, it’s important that you truly understand the products being sold because, firstly, you want to be able to distinguish between the products you are selling so that you can provide a valued consultation. You might find yourself selling one product when you should be referring another. Secondly, understanding these products is important from a regulatory standpoint as the legal connotations of the products must be disclosed properly or mistakes in disclosure, marketing, or funding agreements could become costly.

If you are an independent broker in the alternative commercial lending space, you are usually going to be selling one or multiple of the following products:

- The Merchant Cash Advance

- The Alternative Business Loan

- Equipment Leasing

- Accounts Receivable Factoring

- Accounts Receivable Financing

- Purchase Order Financing

To begin, let’s discuss the Merchant Cash Advance…

Product Value Points

Don’t Let The Critics Win

Critics of the product focus mainly on its high cost and it can be very expensive, but when used properly the product is a great leveraging tool.

Critics fail to shed light on the value of the product in terms of the merchant’s usage. Going back to that Growth Investment example, if the product had not been available, then what were the other sources available for the merchant to take advantage of the growth opportunity? In actuality, there were no other credible sources. Had the Merchant Cash Advance not been available, that investment would not have been made, and a ton of national, state and local economic activity would not have taken place, such as:

- The Equipment Manufacturer’s sale of the equipment

- The Merchant’s generation of $300,000 in revenue based on having the equipment

- The Purchaser’s revenue from borrowing costs incurred from the client using the advance

- My individual commission

- Then all of the federal, state and local taxes that would have been paid as a result

All of that economic activity vanishes if said transaction does not take place. Despite the high cost of the product, the fact is that this transaction would have been a win across the board for all parties involved including the Manufacturer, the Client, the Purchaser, Myself, as well as the Federal/State/Local Government. The true value of business capital, no matter if it’s conventional or alternative, is that the capital should produce enough new revenues so that it truly pays for itself.

Bless You, Fund Me: What Words Predict About Loan Performance

June 7, 2015 Way back in 2006 when I was just a baby merchant cash advance* underwriter, I encountered a book store that was borderline qualified. The final phone interview would make or break their approval so I grabbed my pen and paper and dialed their number.

Way back in 2006 when I was just a baby merchant cash advance* underwriter, I encountered a book store that was borderline qualified. The final phone interview would make or break their approval so I grabbed my pen and paper and dialed their number.

I went through the checklist of questions and they passed. But what really convinced me that it was a deal worth doing was the amount of times the owners made references to God. They were clearly religious people which indicated to me that they were probably also of high moral character. It didn’t matter what religion it was or if their beliefs aligned with mine, I was simply captivated by their values.

After approving the deal and funding them, they actually mailed me a handwritten letter to express their gratitude. It concluded with, “God Bless You!” and I hung it up on the wall of my cubicle to remind myself of the good I was doing for small businesses.

A few weeks later, the payments stopped. All of their contact numbers were disconnected and the owners of the store could not be located. They completely disappeared along with almost all of the money. Looking up at the note on my wall, a shiver went up my spine. Had I been duped? And did they use religion as a tool to influence my decision?

I thought that surely they must’ve encountered legitimate financial difficulty but I believed that even if so, people with their values would’ve been more forthcoming about it. Instead they just took the money and split and were never heard from again.

I learned a lesson about being emotionally influenced on a deal and it turns out there were clues this outcome might happen all along.

Bless you

In a study titled, When Words Sweat: Written Words Can Predict Loan Default, Columbia University professors Oded Netzer and Alain Lemaire, and University of Delaware professor Michal Herzenstein analyzed the text of more than 18,000 loan requests made on Prosper’s website. Applicants that used the word God were 2.2x more likely to default on their loans. And the phrase Bless you correlated higher on the default scale as well, though not as high as other non-religious words.

On the list of words more likely to be mentioned by defaulters are, I promise, please help, and give me a chance. Statistics actually show that someone promising to pay is less likely to pay than someone that doesn’t explicitly promise.

Among the other more common words likely to be mentioned by defaulters is hospital. This word holds special significance to me because in my last year as a sales rep, almost all of my underperforming accounts were supposedly due to the business owners or their family members being in the hospital.

Among the other more common words likely to be mentioned by defaulters is hospital. This word holds special significance to me because in my last year as a sales rep, almost all of my underperforming accounts were supposedly due to the business owners or their family members being in the hospital.

And it wasn’t just me. It seemed like every deal that was going bad in the office involved the hospital. Any time one of us was due to contact an account with an issue, we made bets that a hospital would come up in the story. (Seb, if you’re reading this, apparently it’s not a coincidence.)

I express no opinion regarding whether or not their stories were true, but statistics show that borrowers that mention hospital are more likely to default.

In the study’s Abstract, the professors wrote:

Using a naïve Bayes analysis and the LIWC dictionary of writing styles we find that those who default write about financial hardship and tend to discuss outside sources such as family, god and chance in their loan request, while those who pay in full express high financial literacy in the words they use. Further, we find that writing styles associated with extraversion, agreeableness and deception are correlated with default.

While the study focused on Prosper, their almost identical competitor, Lending Club, may have realized this trend earlier. In March 2014, Lending Club announced that investors would no longer be able to view the free-form writing portion of the borrower loan application. Citing “privacy reasons,” investors lost a valuable clue into the repayment probability of their notes.

But would it really have helped? The researchers wrote:

Using an ensemble learning algorithm we show that leveraging the textual information in loan requests improves our ability to predict loan default by 4-5.7% over the traditionally used financial information.

Nothing to see here folks, move along and approve

Curiously, Lending Club doesn’t want its investors to have access to a data point with such significant importance. Perhaps it’s because of disasters like this, where one borrower used the free-form writing section to spew profanities. Ironically, the loan was approved and issued anyway.

For tech-based platforms like Lending Club however, they noticed the “story” aspect of a loan had become less relevant because of overwhelming investor demand. Investors weren’t evaluating the written portion of the loan application as much anymore. According to their blog post at the time of the announcement, “Fewer than 3% of investors currently ask questions and only 13% of posted loans have answers provided by borrowers. Furthermore, loans are currently funding in as little as a few hours – well before borrower answers and descriptions can be reviewed and posted.”

It had become all algorithms and APIs where loans were fully funded by investors before the written portions could even be published on the website. Had anyone actually taken the time to read the above loan application answers, they probably wouldn’t have allocated money towards it.

But while removing the storyline from the data might give investors fewer methods to detect a good loan, it could actually protect them from getting drawn into a bad loan.

One of the authors of the above referenced study, Professor Michal Herzenstein of University of Delaware, found in 2011 that borrowers could manipulate lenders into not only approving them, but giving them more favorable terms.

You can trust me 😉

In a story that appeared on UD’s website in 2011, titled Good Storytelling May Trump Bad Credit, Herzenstein’s research discovered that borrowers who constructed a trustworthy picture of themselves “could lower their costs by almost 30 percent and saved about $375 in interest charges by using a trustworthy identity.”

The study referred to six possible categories or identities that borrowers would try to impress upon lenders to describe themselves (trustworthy, successful, economic hardship, hardworking, moral, religious). The story explains:

The more identities the borrowers constructed, the more likely lenders were to fund the loan and reduce the interest rate but the less likely the borrowers were to repay the loan – 29 percent of borrowers with four identities defaulted, where 24 percent with two identities and 12 percent with no identities defaulted.

It’s a case of measurable borrower manipulation.

“By analyzing the accounts borrowers give and the identities they construct, we can predict whether borrowers will pay back the loan above and beyond more objective factors like their credit history,” said Herzenstein. “In a sense, our results offer a method of assessing borrowers in ways that hark back to the earlier days of community banking when lenders knew their customers.”

Today’s tech-based lenders that are dead set on removing this human aspect from the equation may be taking a shortsighted approach after all as they evidently still struggle to make predictions with their numbers-only approach.

For example, a poster on the Lend Academy forum recently wrote this to me about early defaults in today’s algorithmic environment, “It would be nice if LC could predict who is going to default in the first few months of the loan and deny them, but I don’t think that is entirely possible.”

It reminded me of a big merchant cash advance deal I approved years back that passed all of the qualifying criteria with flying colors and still defaulted on the very first day. The merchant’s response to why he defaulted on day one? He felt like screwing us over… “Come sue me,” he said.

In a later meeting to review the deal’s paperwork, a group of managers agreed that I had done all I could to make the approval decision except one. I failed to account for the asshole factor.

Far from satire, it is not uncommon for financial companies to refer to an asshole factor in some regard. It’s a very subjective variable but it can make all the difference between an applicant that’s going to pay and one that’s not. Suddenly none of the hard data matters.

Is the applicant an asshole?

In a recent blog post by loan broker Ami Kassar, titled The Single Most Important Rule in Our Company, Kassar wrote, “if a customer, employee, or partner acts like a jerk – we don’t want to do business with them. If you want to be less diplomatic, you can call the rule – the no ###hole rule.”

In a recent blog post by loan broker Ami Kassar, titled The Single Most Important Rule in Our Company, Kassar wrote, “if a customer, employee, or partner acts like a jerk – we don’t want to do business with them. If you want to be less diplomatic, you can call the rule – the no ###hole rule.”

In many circumstances, the measure of someone being an asshole is relative to another person’s perception. There’s even an entire book on that subject if you’re interested. But what’s trickier, is that according to some studies, being an asshole is a positive thing in business. Would that also make them better borrowers statistically?

Referring back to the original cited study, one has to wonder if there might potentially be a list of words that more closely correlate with being an asshole. I don’t think anyone’s ever examined the Prosper data for that before.

You might not be able to quantify asshole-ishness from the text, but something as basic as a person’s pronouns can speak volumes about their personality or intentions. According to Professor James Pennebaker in the Harvard Business Review:

A person who’s lying tends to use “we” more or use sentences without a first-person pronoun at all. Instead of saying “I didn’t take your book,” a liar might say “That’s not the kind of thing that anyone with integrity would do.” People who are honest use exclusive words like “but” and “without” and negations such as “no,” “none,” and “never” much more frequently.

But saying “I” over “we” doesn’t necessarily make you less of a liar. Pennebaker discovered that depressed people use the word “I” much more often than emotionally stable people.

Being emotionally stable would probably make for a better borrower than a depressed one, but with all these influential and conflicting language clues, how can an underwriter possibly make the right choice?

For instance, if the following line appeared on the free-form writing portion of an application, how should it be interpreted?

Using all of the mentioned research as a guide, I’m inclined to consider the applicant a: trustworthy depressed lying asshole that’s not going to pay.

I = Depressed

We = Liar

God = 2.2x more likely to default

Have always been able to pay back = trustworthy

Hurry up and fund me = asshole

We could easily get caught up in the language here and ignore the obvious positives about this hypothetical applicant, such that they have an 800 FICO score and a solid six figure income. Shouldn’t that weigh more heavily? It’s easy to get distracted.

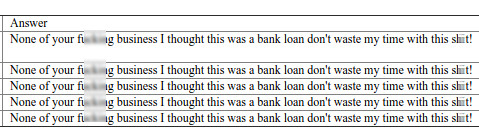

Perhaps Lending Club’s removal of the free-form writing section was for the investors’ own good. Even the borrower that repeatedly wrote, “None of your f**king business I thought this was a bank loan don’t waste my time with this sh**t!” is still current on all their payments after two and a half years.

To brokers like Kassar, the asshole factor is not so much about the likelihood of default anyway, but peace of mind. “Why invest emotional energy in putting up with shenanigan’s when there are so many good people who need our help,” he wrote.

Word is bond?

Regardless of what one study revealed about applicants that invoked God said about the likelihood of default, declining applicants on the basis of writing or talking about God could certainly be argued as religious discrimination. In many instances, religion is a protected class. Sometimes you have to ignore correlations because they can be deemed discriminatory.

One thing is for sure though, back in 2006 the upstanding characters I had created in my mind about the religious book store owners were upended when they disappeared into the night with all the money. Their words got in my head and I approved them perhaps because of it.

Years later, an asshole defaulted on the first day and not long after that, there would be a mysterious spate of accounts whose poor performance would be attributed to supposed hospital related events.

What’s buried in a person’s words? The answers allegedly. I promise…

There’s No Room for More Competition

June 2, 2015 In the next 6 months, (MANY) Broker Companies will start dying out. To the surprise of many, just when the Year of the Broker was in full bloom, chaos was forming on the horizon and the realization that there is no more room for “new” messes. Simply because we aren’t finished cleaning up and organizing the messes we have now!

In the next 6 months, (MANY) Broker Companies will start dying out. To the surprise of many, just when the Year of the Broker was in full bloom, chaos was forming on the horizon and the realization that there is no more room for “new” messes. Simply because we aren’t finished cleaning up and organizing the messes we have now!

There are basic facts that we can take from the “Broker Boom”

– Not enough beginning knowledge about this industry and how the Merchant Cash Advance process works.

– No time to make strong relationships: The concept of having “more” is usually more harmful than having a handful of trusting relationships.

– Overhead costs: the make-up costs from the spending on dead leads and the “start-up” costs of having an office, staff, draws – gave the wrong perception of what a “MCA” is when the rate mark ups pay for those expenses.

– Quick turnover when the top dog can’t fool the sales rep out of commissions any longer: Rep goes out into the world and starts their own company. This can lead to recycled bad practices or the few who want to do right.

– Co-Brokering: Everyone’s done it. I’ve done it. Edited agreements taken from other brokers/funders don’t always cover everything leading to many debacles that turn into “Jerry Springer” Forum threads. P.S. Don’t think merchants can’t see the forum either.

It’s absolutely exhausting to explain to someone from the mortgage industry or any industry that comes into the MCA space the “Rights” and “Wrongs” and the teachings. Most new Broker Company Owners and their sales come from those who don’t believe in “Best Practices” anyway.

Marketing and Leads in the Broker Space is affecting Brokers and Funders Alike – Are brokers ruining leads as well?

So, your questions about Marketing and Leads have the same answer- It does not matter what type of leads you get, it’s all about your presence, knowledge, and your “Handle”. These are the answers from actual merchants who get calls from UCCs. (This information came from old merchants that I had, I shortened the answers and stuck to the points).

- They don’t trust you because of your approach

- They tried before and was promised “X” and got a bunch of “Y” with excuses on how so many “Y’s” = “X”

- Backdoor calls- Sometimes the money isn’t the biggest savior- it’s the relationship that goes with it

- They don’t need it that bad to pay 30%. If they do need it- they want something structured to build their credit and keep their business afloat

When people think of getting money for their business- they used to think “Go to the Bank”. Professionalism, a structure that is always the same for each type of program, and knowledgeable staff they can rely on. They made the choice to come to your bank because of what is offered. Now, all but the “Capital” part is missing from this equation, but merchants still want to have that one consistent place to go to for their business needs.

I think we all lost sight of this Industry.

Brokers = Resellers and Marketers of Direct Funding programs. The Broker takes the programs from these Direct Funders and builds a portfolio of which each tier and industry and credit rating is satisfied by which funders he can qualify them to. The options are given to the merchant to satisfy their need for working capital.

You work for the Funder – Your Sales Target is the Merchant.

The Merchant has put everything into starting and maintaining their business. Most of them wanted the “American Dream” of owning a business since childhood. They have it now, and you come in and try to tell them what they need. Some believe you- some are money hungry and know the game. It’s all a numbers game no matter what kind or type of leads you buy.

All that am I saying is, the way this industry is looked at from a “Brokers” and “New-Age Funders” point of view vs. a “Veteran Broker” or “Veteran Funder” is two totally different aspects.

Unfortunately, there is no immediate solution for new “Brokers” and many solutions for the “New-Age Funders” to be on the path of “Best Practices” and less shenanigans.

There is no room for competition as we don’t know what we are competing for and rather than creating a solution so those leads can understand the growth and structure of what we are offering, we are too busy trying to find out how to get leads that won’t stick.

The Broker’s Future: Are The Good Times Over?

June 1, 2015 As we continue the Year Of The Broker discussion, we must take an honest look at The Future. Due to the low barrier to entry into our space, there isn’t a week that goes by that I don’t see another recruiting ad informing the reader that all they need is a heartbeat, a UCC list, and an industry list of SIC Codes to make big money in our space. But is everything really as rosey as promoted, or if you are a new broker, should you consider investing your capital (time, energy, money and mental health) in another industry?

As we continue the Year Of The Broker discussion, we must take an honest look at The Future. Due to the low barrier to entry into our space, there isn’t a week that goes by that I don’t see another recruiting ad informing the reader that all they need is a heartbeat, a UCC list, and an industry list of SIC Codes to make big money in our space. But is everything really as rosey as promoted, or if you are a new broker, should you consider investing your capital (time, energy, money and mental health) in another industry?

The Past

To understand The Future, sometimes we have to look at The Past. Instead of a year of the broker, there was instead an actual era of the Broker, and that was from 2000 to about 2013:

(( 2000 – 2007 ))

Few firms offered a “Merchant Cash Advance” as either a direct sell or value add, and very few merchants were receiving telephone solicitations in regards to the having “working capital” other than those involved in the Equipment Leasing or A/R Factoring sectors. While the market was wide open, most merchants wouldn’t entertain an advance for 6 months with a 1.25 – 1.30 factor rate when banks were lending pretty well at much lower borrowing costs.

(( 2008 to 2013 ))

When the economy and markets took a downturn in 2008 creating The Great Recession, and banks halted most of their lending to small business applicants, the Merchant Cash Advance product was more aggressively sold by the pioneers of the industry through their Merchant Processing ISO relationships, direct selling, online advertisements, and more. The pioneers also introduced risk based pricing and premium priced products, allowing them to appeal to the higher credit graded merchants who were finally entertaining the product due to banks not lending as efficiently as previously. The pioneers also introduced multiple formats of repayment including through ACH, which allowed them to service merchants that they couldn’t tie the repayment to their merchant processing volume due to the merchant’s inability to switch or the merchant’s low monthly processing volume.

Awareness of the Merchant Cash Advance skyrocketed, hundreds of millions in equity capital began pouring in, major media outlets such as CNBC gave the product coverage, and annually the industry was funding over $1 Billion to small business applicants.

This boom period also started the trend of new lenders and brokers popping into the industry overnight using mainly the same marketing strategies such as UCC Lists, SEO, PPC, Bankcard Portfolio Marketing, and Cold Calling Various SIC Codes. These strategies worked in a decent fashion until the flood of new direct lenders and brokers coming into the industry continued, with these new entrants using mainly the same strategies. Profits were being driven down, new client acquisitions were being driven down, and because a funder’s UCC filings were being called so much, they decided to begin filing them under fake names or only filing them on riskier merchants, or never filing a UCC at all. Also most of the Online Marketing methods became too expensive, pricing the little guy out of the market.

The Future

Now we are in 2015 and new broker entrants are mainly using the exact same strategies from 2008 – 2013, discovering that UCC lists and Cold Calling SIC Codes just will not work efficiently going forward. The Future of profitability and new client acquisition in our space is going to be through Strategic Partnerships. There are three sections of your Strategic Partnerships and they are your Professional Network, Mom and Pop Network, and Online Network.

• Professional Network – The creation of a professional network from referrals such as Banks, Credit Unions, Accountants, Business Brokers, Merchant Processing ISOs, etc., to bring in a high amount of consistent leads of small business applicants who are currently seeking capital.

• Mom and Pop Network – The creation of an external independent broker channel that includes hundreds of random brokers that you sign up to resell your services. You would use the same tongue and cheek, everything is rosey, recruiting ads that I see every week just to get a rush of people on the telephone making cold calls to SIC codes, trying to compete in online marketing, or calling the remains of UCC lists, all with the dream of making a lucrative payday. The volume produced on an individualized basis will be so small it’s irrelevant, but as a collective, they will make up a major chunk of volume. This why I call these sources Mom and Pop.

• Online Network – This is your SEO, PPC, High Traffic Website Ads, and other online advertising methods. These methods will become more expensive going forward and only those with large marketing budgets will be able to truly capitalize in this area with positioning, listings, etc.

Summary

Our space is changing and new broker entrants might want to reconsider investing their capital (time, energy, money and mental health) into this venture. Only direct lenders with team members that were pioneers of this space as well as with the right networks and equity sources, are capable of truly seizing The Future. Those just now trying to come in and ride the wave will soon discover that just like with the Stock Market, the real money has already been made and most of the future returns are already capitalized. As a new broker, you more than likely will fall into that dreaded Mom and Pop category, which isn’t a good position to be in for The Future.