Why You Shouldn’t Overlook Selling Merchant Processing

January 4, 2016 Prior to daily fixed payment business loans, there was the traditional merchant cash advance (MCA). The MCA, being the only option, required merchants to tie their need for working capital to that of their merchant accounts, either directly or indirectly, through the use of either split-funding or a lockbox account.

Prior to daily fixed payment business loans, there was the traditional merchant cash advance (MCA). The MCA, being the only option, required merchants to tie their need for working capital to that of their merchant accounts, either directly or indirectly, through the use of either split-funding or a lockbox account.

DIRECT OR INDIRECT?

Split-funding is a direct method that requires the merchant to convert their merchant account over to a chosen Independent Sales Organization (ISO), you could also refer to the ISO as a Merchant Service Provider (MSP). The MCA company contracts with an ISO/MSP who then manages the flow of the merchant’s daily credit card processing volume. A percentage is withheld and forwarded to the buyer of those receivables.

The lockbox is an indirect method to manage the flow of funds. Rather than withhold funds from the ISO/MSP, a separate FDIC insured account is established on the side for all credit card processing receipts to settle into initially, with a percentage of that volume going to the buyer and the remaining amount “swept” into the merchant’s operating account.

Nevertheless, whether directly or indirectly, the merchant account of the business owner was the foundation of the MCA approval and facilitation. Because many MCA companies also offer alternative business loans today with fixed payments, a lot of the new broker entrants do not believe that learning about the field of merchant processing is as important today as it was years ago. However, I disagree with this notion, as the purpose of our industry is the long term relationship with the client, and in many ways the traditional MCA product provides more “benefits and value” to the merchant over time than today’s business loan. Just as new broker entrants get to know all about the MCA, they should also get to know all about merchant processing.

OVER TIME, CAN THE MCA BE THE BETTER CHOICE?

The alternative business loan requires no merchant account conversion as it doesn’t tie the merchant account to the facilitation of the working capital transaction. With these loans, a percentage of gross revenues are approved with fixed terms up to 36 months on daily or weekly payments. The main benefit of this product over the MCA is the awareness of payment frequency and quantity upfront, thus, enabling the merchant to better allocate their cash flow.

However, while the traditional merchant cash advance requires the tie-in of the merchant account, there’s no fixed terms nor fixed payments as it correlates with the merchant’s sales cycle, where they deliver more during busy times, less during slow times.

When selling the merchant the long term aspects of the MCA, why not seek to get their MCA funded using the split-funding method rather than a lockbox? Doing so would provide an additional revenue stream within your client portfolio. To properly seek out this opportunity and be able to consult, convince and convert the merchant over to your MCA firm’s ISO/MSP Partner, you want to fully understand what merchant processing is all about.

WHAT IS MERCHANT PROCESSING?

A merchant account is an unsecured line of credit provided to a business from a registered ISO/MSP. The credit line enables the business to benefit from accepting Visa and MasterCard (V/MC) along with other major bankcards from their customer base, to experience the benefits of acceptance which includes better fraud management, higher average tickets, customer loyalty due to convenience, and more. V/MC are just registered card brands that manage a group of banks called “member banks”, which are banks apart of a listing of V/MC bank associations. The member banks pay V/MC dues and assessments to market their brands. You have different types of member banks, you have the Issuing Banks and then you have the ISO/MSP along with the Sponsoring Banks.

The Issuing Banks issue credit cards with credit limits to consumers after they meet credit criteria. On the processing side, you have the registered ISO/MSP and Sponsor Banks, which approve a merchant for a merchant account and process payments through a front-end authorization network, then settles them through a back-end network.

During the processing of a credit card transaction, there’s a couple of different fees that are charged. Interchange is one of the fees charged, which is how the Issuing Banks are paid. These are wholesale prices for every type of card that a merchant could potentially run at the point of sale, with new interchange pricing charts released in April and October of every year. The ISO/MSPs are paid when they mark-up interchange as well as through fees such as an annual fee, statement fee and batch fee.

WHY IS MERCHANT PROCESSING A UNSECURED LINE OF CREDIT?

The merchant account is indeed an unsecured line of credit, because when a merchant’s customer runs an order on their credit card for $500, the merchant would rather have that entire $500 upfront rather than waiting for the customer to pay off their credit card balance in full, which could potentially take years. As a result, the ISO/MSP deposits the amount in their bank account within 48 hours rather than having the merchant wait until their customer pays their credit card balance in full.

Now, if the merchant’s customer initiates a chargeback of the $500 transaction and the merchant loses the case, the $500 would have to be refunded by the merchant plus the costs of the chargeback which includes a chargeback fee and retrieval fee. If the ISO/MSP goes to get the $500 from the merchant and there’s no money in their account (let’s say the merchant has gone out of business), then the ISO/MSP who underwrote the merchant account is on the hook for the charge.

WHY SHOULD YOU SELL MERCHANT PROCESSING?

When using split funding for a merchant cash advance deal, if you switch over their processing to an ISO/MSP that your MCA firm currently split funds with, you are looking at collecting the long term residuals from the processing and the compensation from future merchant cash advance renewals. In addition, split funding is much more efficient than using a lockbox, as a lockbox usually adds 1-2 business days to the settlement process for everyone involved. Withsplit funding, the merchant can continue to receive their processing deposits as normal.

There are different types of payment processing technologies depending on what the merchant needs, if they need a stand-alone solution then that’s available in the form of a landline terminal, wireless terminal, computer software or virtual terminal. If the merchant needs a comprehensive solution then that’s also available in the form of point-of-sale systems or operational management technologies, both of which integrate merchant processing into the system and other operational aspects such as accounting, payroll, human resources, etc.

Why not just have the merchant switch over their processing to an ISO/MSP that your MCA firm currently split funds with, and collect recurring merchant processing residuals along with recurring income from merchant cash advance renewals? After all, recurring income is the lifeblood of our business.

Year of The Broker Concludes – 2015 Recap

December 31, 2015 It was the Year of the Broker, a phrase that often conjured up images of easy money and inexperience. Lenders like OnDeck reacted by reducing their dependence on them. Responsible for 68.5% of their deal flow in 2012, OnDeck only sourced 18.6% of their deals from brokers in the third quarter of 2015.

It was the Year of the Broker, a phrase that often conjured up images of easy money and inexperience. Lenders like OnDeck reacted by reducing their dependence on them. Responsible for 68.5% of their deal flow in 2012, OnDeck only sourced 18.6% of their deals from brokers in the third quarter of 2015.

But there’s money being made. One broker is on pace to do more than $100 million worth of deals annually after working as a plumber eight years ago. Another went from sleeping in his car to driving a Ferrari. Meanwhile, brokers like John Tucker are basically saying just the opposite. Tucker has repeatedly taken to AltFinanceDaily to preach things like “minimalism,” a practice of living below your means to a point where you can survive, and telling everyone it’s okay to embrace the satisfaction of a middle class life.

So is it the end of days or just the beginning?

In October, initial survey results of top industry CEOs revealed a confidence index of 83.7 out of 100, but out there on the street for the little guy, it’s been a tumultuous year. Things like commission chargebacks have hit brokers at unexpected times, with several funders privately telling us over the year that rogue brokers have closed their bank accounts or frozen the ACH debits in order to avoid giving the commissions back.

In 2015, brokers sued their sales agents and sales agents sued their employing brokers. Deals got backdoored, deals got co-brokered, and soliciting deals anonymously got banned from industry forums. Stacking continued mostly unfettered but is being pursued in the court system by funders allegedly injured by it. Brokers took over Wall Street and are supposedly being watched by regulators. Oh, and robo-dialing? Brokers should probably steer clear of that, just as underwriters should ditch paper bank statements.

It’s a lot to manage. Sometimes for a broker, just losing a deal can make them so sick that they have to go home. That’s apparently what happens when you don’t answer the phone fast enough. At least one said there’s no room left for more competitors so if you were thinking of starting a brokerage now, $2,000 won’t be enough.

But things could be worse. In 2015, IOU Financial was under attack by Russian nuclear scientists, a story that was more truth than exaggeration. In the end, Qwave Capital acquired a 15% stake in IOU.

An OnDeck class action lawsuit that looked bad at first turned out to be mostly based on the words of a convicted stock manipulator with a short position in the stock. The case is still ongoing and OnDeck’s stock price is down 50% from their IPO.

In 2015, two guys lost God but found $40 million (although numerous sources say that number is off).

“Madden” no longer means the football video game and Section 1071 is not a seating area in a stadium.

An RFI turned out to be something not to LOL about. Despite an overwhelming response from lenders and funders, the Treasury isn’t completely sold.

Things weren’t so automated in 2015 despite the cries of technological disruption. Maybe that’s why it feels like 1997. Manual underwriting still dominated and bank statements still matter as much as they ever did. God declined loan applications, Google rigged the search results, and a mayor declared war on merchant cash advance (and then never spoke about it ever again after being re-elected).

Things weren’t so automated in 2015 despite the cries of technological disruption. Maybe that’s why it feels like 1997. Manual underwriting still dominated and bank statements still matter as much as they ever did. God declined loan applications, Google rigged the search results, and a mayor declared war on merchant cash advance (and then never spoke about it ever again after being re-elected).

Lobbying coalitions formed. NAMAA became the SBFA. The CFPB lied and community bankers testified.

But things are looking up. Brokers can obtain outside investments, get acquired, or make millions through syndication.

Bad Merchants are now ending up in more than one bad database, though a deal for the ages slipped through the cracks. Other merchants went to jail. Square went public and brought merchant cash advances along with them. The industry beamed its message through Times Square and one Democratic congressman has asked God to bless it all.

It was a crazy year. Marketplace lending became an acknowledged term (and the name of a conference) and already companies under that umbrella have been linked to presidential candidate (and desperate loser) Jeb Bush and the San Bernardino Terrorists. The FDIC had a few things to say and SoFi went triple-A. Marketplace lending is making a lot of people money, but when looking at the tax implications is there something funny?

In 2015, the big boys shared their wisdom and their figures. Turns out, it was beyond hyperbole. Brokers experienced an incredible rise or they pawned their ferrari to the other guys. Some focused on a specific crop, while others are trying it over the top. California sucked, John Tucker tucked, and one lender got totally F*****. In 2015 some funders got tanked, so in 2016 we’ll all be AltFinanceDaily.

Happy New Year!

BizBloom Lights Up Times Square

December 24, 2015BizBloom’s “Yes, we’re local” campaign produced by industry veteran Thomas Costa is making its debut in New York City’s Times Square. Its mission, according to Costa, is to tell the story of the American Dream, particularly the struggles and accomplishments of entrepreneurs.

To do that, BizBloom intends to rely on the help of college students to interview small business owners all over the country. The stories that garner the largest social media responses will be featured in their slot airing over 43rd and Broadway. Additionally, for each story a student collects, BizBloom will donate to a special scholarship fund.

The campaign is already live and includes supporting endorsements from Quick Bridge Funding and AltFinanceDaily:

Got a Ferrari or Fine Art? If So, You May Have More Leverage Than You Think

December 23, 2015If you own a Ferrari, fine art or expensive wine, getting access to capital may be easier than you think.

Although it’s still a niche market, luxury asset-backed lending has been gaining traction lately, particularly with small and mid-size business owners. These executives are enticed by the ability to use certain high-priced valuables as a means of getting large amounts of cash quickly and often at a lower cost than other funding sources.

“People are increasingly learning that this is another option. It’s not for everybody, but it’s another option,” says Tom McDermott, chief commercial officer at Borro, a New York-based asset-backed lender that deals exclusively with luxury asset-based loans.

It’s notable that luxury asset-based lending by alternative funders is gaining ground at a time when unsecured money is so easy to come by. There are several reasons business owners are attracted to the idea of leveraging their valuables to attain cash. First off, they don’t need stellar credit or a proven track record in business to qualify. Secondly, they can typically get larger sums of money and at better rates than they might through other financing channels. A third reason is that many of them have already tapped out other funding options and leveraging their assets allows them to obtain additional funds quickly.

“A lot of small business owners have assets, so it’s something else for them to utilize in getting access to attractive small business financing,” says Steven Mandis, chairman of Kalamata Capital LLC, an alternative finance company in Bethesda, Maryland.

Here’s how the process typically works at most luxury asset-based lenders. Say a business owner wants to borrow against a high-priced item such as a top-of-the-line car, fine art or wine, jewelry or a luxury watch. First the luxury-based lender hires a third-party to appraise the item. Generally, depending on the asset and its marketability, lenders will lend 50 percent to 70 percent of the asset’s value. If the owner moves forward, the item or items are held and insured in a lender’s secure storage area until the loan is paid back. Default rates on these types of loans are relatively low, lenders say.

“People don’t want to put their house at risk when they need capital,” says McDermott of Borro. “They’d rather lose the Maserati or a lovely piece of art than the house,” he says. And even then, it doesn’t happen very often, he says. Borro clients only default on their loans about 8 percent of the time, McDermott says.

Barriers to Entry

To be certain, luxury-based lending is not a business that every funder wants to be in. For starters, there are a lot of regulatory hoops a funder has to jump through in order to do it. You need a pawnbroker’s license and a second-hand dealer license. You also need a secure facility or facilities to house the collateral, have secure ways of transporting the valuables, and you need to carry large amounts of insurance for the transfer of the items as well as during the holding period.

Indeed, keeping the items secure is critical. PledgeCap, a Lynbrook, New York-based funder, says on its website that it uses “cutting edge technology, top of the line bank vaults and armed guards” to keep a customer’s items safe. What’s more, all items are insured during transit and storage. All items are shipped through secured and insured FedEx shipping vendors for pickups and drop-offs.

“There aren’t a lot of players in the market because there are a lot of operational and legal requirements to adhere to. There are a lot of barriers to entry,” says Gene Ayzenberg, the company’s chief operating officer.

Putting Things in Perspective

Luxury asset-based lending is only a small subset of the overall asset-based lending market, which as a whole has been gaining ground in the past few years. After getting badly burned in the most recent recession, many lenders have come to appreciate the security blanket that collateral offers. According to the Commercial Finance Association’s quarterly Asset Based Lending Index, U.S. ABL loan commitments rose 7.2 percent in the second quarter, compared with the year-earlier period. In addition, new ABL credit commitments were 6.3% higher than the same period a year ago.

“Asset-based lending at one time used to be the lending of last resort. Now it’s the type of lending that it is accepted globally,” says Donald Clarke, president of Asset Based Lending Consultants Inc., a Hollywood, Florida-based company that provides due diligence services for lenders. “Today, everybody wants an asset.”

There’s not a lot of public data to gauge the size of the luxury market within the broader asset-based lending market. But a 2014 report that focuses on art lending gives more perspective to at least one facet of luxury asset-based lending.

Thirty six percent of the private banks polled said they offer art lending and art financing services using art and collectibles as collateral. That’s up from 27 percent in 2012 and 22 percent in 2011, according to the report by consulting firm Deloitte and ArtBanc, a company that provides art sales alternatives, valuations and collections management services.

Meanwhile, 40 percent of private banks said this would be a strategic focus in the coming 12 months, up considerably from the 13 percent who named this as a priority in 2012.

These market changes are likely driven by client demand. The Deloitte/ArtBanc survey found that 48 percent of establishes art collectors polled said they would be interested in using their art collection as collateral for a loan, up from 41 percent in 2012.

Many big banks won’t touch asset-based lending deals unless they are worth north of $5 million. Some community banks will do smaller deals, but many don’t have the necessary infrastructure or skill sets, explains Clarke, of Asset Based Lending Consultants. This, of course, leaves an opening for alternative funders to capture market share.

Luxury asset-based lending expected to experience growth

Some lenders say they expect demand for luxury asset-based loans to continue to increase over time as more people accumulate big-ticket items and they become more aware that they can satisfy their capital needs by leveraging those assets. “A lot of times they don’t even know they have this option available to them,” says Ayzenberg of PledgeCap.

He says most of his company’s customers are small and mid-size business owners. Often they have temporary cash flow issues, but bank loans aren’t necessarily an option for them for any number of reasons. For instance, some may have bad credit. Others may have excellent credit but not enough of a business track record to qualify for a bank loan. Others may not have the cash flow to secure the amount of money they need, or they may need the money very quickly. Asset-based lenders can generally make the money available within a day, whereas bank loans require a lot of paperwork and can take months to obtain.

Mandis, of Kalamata Capital, says his company has seen an increased willingness by business owners to put up their luxury assets as collateral in order to get larger amounts of money at more favorable terms. Many times business owners have a high-priced asset that they don’t want to sell and pay a tax or can’t easily unload within a short-time frame. By borrowing against the luxury asset, they will get the capital to take advantage of a short-term opportunity and make an attractive return quickly without having to worry about finding a buyer or paying taxes on the sale of the asset, he explains.

Certainly luxury asset-based lending is not for every customer. Not only do you have to have a valuable asset to be used as collateral, but you also have to be willing to part with the item while the loan is outstanding. The risk of default and not getting the item back may also be a barrier for some people.

“I would be very hesitant to put up my wife’s diamond ring for my business. I don’t think it’s typically someone’s first choice,” says Ami Kassar, chief executive and founder of Multifunding LLC, a company in Ambler, Pennsylvania that helps small businesses find the best loan for their business. He remembers considering this option for a client only once in the past several years and the client ultimately chose another funding source.

But companies that focus on luxury asset-based lending say there is a viable market for their services that will continue to grow as more people hear about it and use it successfully to fulfill their funding needs. People have been taking their small items to pawn shops for many years. Working with a licensed lender to leverage their larger and often more expensive items gives them an option they may not have had previously. “You can’t just drive a tractor into a local pawnshop and say, ‘Here just put this in your safe,’” says Ayzenberg of PledgeCap.

Also, unlike pawn shops, luxury asset-based lenders say they aren’t looking to sell the items to make a quick buck and will only sell the item as a last resort if a customer defaults and they can’t reach agreeable terms. “We want them to keep their items,” says Ayzenberg whose company has been in business since 2013. For every 100 loans, there are only a small percentage of customers that default and lose the items, he says.

Every lender runs their business slightly different. At Borro, for example, loans typically range between $20,000 and $10 million and span in time frame from three months to three years. Rates start in the mid-teens and are based on the size of the loan, the time frame and how easy the asset would be to sell. In order to work with Borro, the asset typically has to be worth more than around $40,000, McDermott says.

Borro, which has been in business since 2009, deals with customers directly. But it also gets a good number of referrals from other lenders. Let’s say a customer needs $500,000 and a particular lender can only offer a maximum of $350,000. That lender might refer the client to Borro, which kicks in $150,000 based on the value of a leveraged asset. The referring company gets a commission based on the loan value and doesn’t lose the whole deal. “It’s a way to keep your customers tied in with you,” McDermott says, adding that Borro has no intention of getting into other types of lending. “We complement each other. We don’t compete.”

PledgeCap also focuses exclusively on asset-based lending. The company typically funds loans between $1,000 and $5 million. The length of each loan is four months. Customers don’t have to pay every month, though most do. For every month the loan is outstanding customers pay a rate of 3 percent on average. Other fees, payable at the end of the loan, are assessed based on costs PledgeCap incurs and depend on factors such as the cost of insurance, the appraisal fee and the cost of transporting the item to the secure facility.

PledgeCap also focuses exclusively on asset-based lending. The company typically funds loans between $1,000 and $5 million. The length of each loan is four months. Customers don’t have to pay every month, though most do. For every month the loan is outstanding customers pay a rate of 3 percent on average. Other fees, payable at the end of the loan, are assessed based on costs PledgeCap incurs and depend on factors such as the cost of insurance, the appraisal fee and the cost of transporting the item to the secure facility.

By contrast, Kalamata Capital, which has been in business since 2013, offers asset-backed loans in connection with several other small business financing options—such as working capital loans, SBA loans, lines of credit, merchant cash advance and invoice factoring—to give customers more flexibility in terms of rates.

In Kalamata’s case, it will evaluate the cash flow and other assets of a small business for financing options. Kalamata then combines both the amount it would lend against an asset and the amount it would lend to the small business, possibly giving the business a lower rate—and more options—in the process.

While it’s not a type of funding that works for everyone, Mandis, the chairman of Kalamata, expects to see continued growth in this area. “I don’t think the loan market for luxury assets is as large as many of the traditional small business finance areas, but it is something that can be helpful to small business owners,” he says.

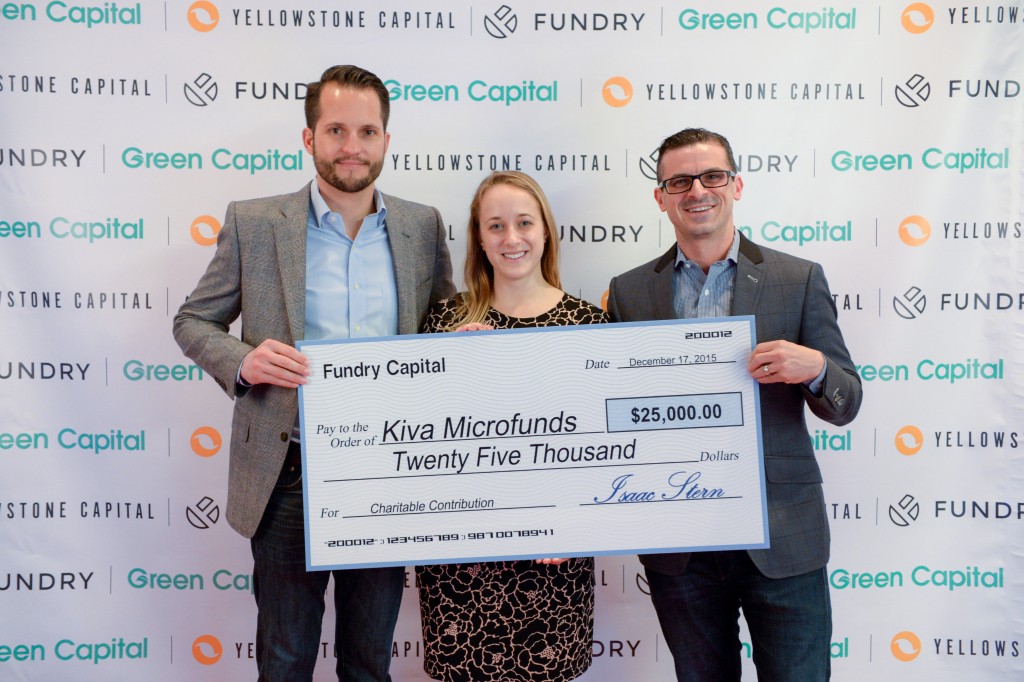

Fundry Donates $25,000 to Kiva at Red Carpet Event

December 22, 2015Fundry, the parent company of Yellowstone Capital and Green Capital, hosted a red carpet event last Thursday evening in New York City where they presented a donation of $25,000 to Kiva. Kiva is a non-profit organization with a mission to connect people through lending to alleviate poverty.

The event, which also celebrated their 2015 success, was attended by more than 300 people. All told, Fundry originated nearly half a billion dollars in small business funding for the year.

The Broker’s Future Part Two

December 16, 2015THE ROBOTS ARE COMING

Merriam-Webster and Dictionary.com both agree, that a “robot” is a machine that is created to do the work of a person, carrying out a complex series of actions automatically, all controlled by a computer. Sometimes a robot can resemble a human being in likeness, but often times a robot is simply a piece of software, a piece of hardware, a piece of machinery, or a cloud based infrastructure called the internet (online networks). Professor Kaku is a futurist from City College of New York, a futurist is someone who makes what one would consider “fairly accurate” predictions about what the future holds and how these future events might emerge from present day events. Professor Kaku believes the following:

Merriam-Webster and Dictionary.com both agree, that a “robot” is a machine that is created to do the work of a person, carrying out a complex series of actions automatically, all controlled by a computer. Sometimes a robot can resemble a human being in likeness, but often times a robot is simply a piece of software, a piece of hardware, a piece of machinery, or a cloud based infrastructure called the internet (online networks). Professor Kaku is a futurist from City College of New York, a futurist is someone who makes what one would consider “fairly accurate” predictions about what the future holds and how these future events might emerge from present day events. Professor Kaku believes the following:

The job market of the future will consist of those jobs that robots cannot perform. Our blue-collar work is pattern recognition, making sense of what you see. Gardeners will still have jobs because every garden is different. The same goes for construction workers. The losers are white-collar workers, low-level accountants, brokers, and agents.

A RECAP OF PART ONE

Back in June 2015, I did an article for AltFinanceDaily about the Broker’s Future, speculating if the good times were indeed over for the brokers as it pertains to their level of profitability and survivability going forward.

- I examined the 2000 – 2007 and 2008 – 2013 time periods, speculating that the “Era of the Broker” was indeed between the 2000 – 2013 period.

- Then, I examined the current time period which begins around the middle of 2014, that is seeing so much of a mass new entrance of brokers into the space, that AltFinanceDaily had to compose a cover story on the phenomenon for the March/April edition of AltFinanceDaily Magazine. The only issue with this current time period is that, in my sole objective opinion, we are in the “Era of the Strategic Networks”, and no longer in the “Era of the Broker.”

- I concluded the article in June with the following: those just now trying to come in and ride the wave will soon discover that just like with the Stock Market, the real money has already been made and most of the future returns are already capitalized.

AN INTRODUCTION TO PART TWO

My analysis shows that the current time period is all about Strategic Networks, which are mainly three networks to be exact, which include the following, all designed to produce competitive market advantages, positioning, strategies, qualified leads, etc:

- The Center Of Influence Network: this includes entities such as banks, credit unions, processors, accountants, VCs, credit bureaus, etc., that allow access to exclusive leads, exclusive data, equity financing, debt financing, mergers, etc.

- The Mom and Pop Network of random independent agents across the country who resell on a 100% commission basis, providing free marketing in a way that collectively they produce a significant amount of volume (even though individually most of the agents cannot make a living from this activity).

- The Online Network with exclusivity on the growing online marketplace of merchants seeking financing, education and options via the internet.

For Part Two Of The Broker’s Future, I want to focus in on The Online Network, which in my opinion will be one of the main destroyers of opportunities in our space for the majority of brokers going forward.

DEATH OF A B2B SALESMAN

For about $499, you can read a very comprehensive report from Forrester on the death of B2B salespeople. Forrester predicts that by 2020, over 1 million B2B salespeople will lose their jobs to the growing force of IT/Robotics, which includes various forms of technology, automation and of course the internet in general through E-commerce.

In relation to our industry of merchant services, merchant cash advance and alternative business loans, I don’t believe that we have to wait until 2020 to see significant changes, I believe these changes are already in full effect and the major players within our space are the ones that are truly capitalizing on The Online Network, giving them major exclusivity on the growing online marketplace of merchants seeking financing, education and options via the internet.

MERCHANT SERVICES HAS BEEN AFFECTED

The Online Network phenomenon has totally destroyed the feet on the street MLS (merchant level salespeople) over on the merchant services side. Before the rise of the Online Network, MLS were valuable to merchants as information on merchant processing, interchange, how the bankcard transactional process worked, etc., were not readily available and most banks did not handle direct sales of the service. So the MLS would park their car down the street, randomly walk into merchant locations, and provide the education via brochures, terminal samples, etc.

They would explain how the merchant processing process works, how accepting credit cards could boost sales through more impulse purchases and consumer convenience, and more. The MLS would then go over the different options of payment processing technology, commit the merchant to a 24 – 48 month lease of the technology, and make his/her commission off the leasing sales and eventually also off the residuals. However, the rise of the Online Network completely shattered this business model:

- The Online Network now allows the merchant to comprehend merchant services on his own, without the help of the MLS, by researching interchange and conducting his own “rate analysis”. The merchant can also now see the true cost of the processing equipment, thus to no longer sign up for leases for $100 a month for 24 months ($2,400) for a $350 terminal at best.

As a result, the MLS can no longer prospect on “rate savings” nor prospect based on the equipment such as through leases or even through free terminals anymore, due to the merchant’s knowledge that the terminal is worth $350 at best. As a result, the direct sales of merchant services has become a value-add to other services, requiring yesterday’s MLS to transform into something totally different such as a financing or payroll specialist, trying to convert merchant accounts over on the side, as part of the sale.

ALTERNATIVE LENDING HAS BEEN AFFECTED

The merchant cash advance and alternative business loan products are more popular today than they have ever been before, due mainly to the massive media attention that they have received with companies going public, CEOs landing interviews on major media outlets, talking heads debating the products across a number of media mediums, and more. 7 – 15 years ago (2000 – 2008), if you were to look up a product online called “merchant cash advance”, you would not have produced many search results. As a result, to inform and educate the merchant on the product, you needed an actual human being (a broker) to sit down and explain the nuances of said services referred to as “split funding”, “revenue purchases”, and “holdback percentages.”

Compare this to today, where a simple search for “merchant cash advances” gives you pages upon pages of articles, promotional ads that follow you across the internet, company websites, press releases, and more. The merchant can easily learn about the merchant cash advance as well as other new forms of alternative financing by going online and scrolling through the vast amount of information. They can educate themselves on the products, companies, and payback procedures. They can fill out a form and get 10 quotes from 10 companies within a couple of hours and in a lot of cases, receive funding from one of the companies by the next business day. The phenomenon is so big that companies in our space are now just referred to as “Online Lenders,” totally shunning the fact that many operate with traditional brick and mortar locations and still employ brokers to still resell the products like they did “in the old days”.

THE FUTURE

Based on my sole objective analysis, The Future is going to be all about the three networks of Strategic Partnerships, which includes The Online Network. Without a shadow of a doubt, those that control these networks will be the major players going forward, as they will have the leveraged resources, knowledge, experience, financing, and connections that the newer market entrants just do not have.

The 80/20 dynamic will continue, where 20% of the players produce 80% (or more) of the production, and the other 80% of the players will fight over the remaining 20% (or less) of the production, which just will not be enough to sustain profitability going forward.

As fast as these new entrants rush in, will be as fast as they burn out. Burning through their savings and retirement funds, and/or running up the utilization rate on their credit cards, trying to take advantage of a “market opportunity” that they “heard about”, but is pretty much already capitalized on, by those who have been here long before they came on the scene.

Bizfi Secures $65 Million in Financing

December 15, 2015NEW YORK–(BUSINESS WIRE)–Bizfi (www.bizfi.com), the premier FinTech company whose online small business finance platform combines aggregation, funding and a participation marketplace, announced that Metropolitan Equity Partners (“Metropolitan”) has provided a structured financing facility of $65 million to the company to drive growth.

Closing this financing round enables Bizfi to:

- Expand its suite of funding programs, increasing its ability to fund America’s small business capital needs.

Increase the speed at which funding applicants access direct financing from Bizfi. - Develop and implement a national marketing campaign designed to increase the awareness of the Bizfi brand and platform within the small to medium-sized business community.

- Bizfi and its proprietary marketplace and funding technologies have provided in excess of $1.3 billion in financing to over 26,000 small businesses across the United States since 2005. Since Bizfi launched its aggregation platform in 2015, the Company has experienced 72% growth in year-over-year gross originations.

“The Bizfi platform is the simplest, fastest and most frictionless process for small businesses to access funding. Metropolitan’s financing will propel our growth plans to the next stage,” said Stephen Sheinbaum, founder of Bizfi. “Every day more and more businesses are turning to Bizfi because of our strong channel partners, enabling business owners to compare all their funding options in one place. The Metropolitan partnership provides Bizfi with additional capital to develop new products and fund more small businesses from its own branded product set.”

Metropolitan’s investment provides the financial flexibility and strength to support Bizfi’s growth plans. The new investment expands upon Metropolitan’s prior involvement as an active buyer of loan participations and a mezzanine lender to the Company for the past three years.

Bizfi’s proprietary technology and aggregation platform efficiently gathers applicant information from a wide variety of sources to quickly offer commercial funding products including loans and other capital products to small businesses. Bizfi’s technology is further strengthened by strategic relationships with more than 45 funding partners, including OnDeck, Funding Circle, IMCA Capital, Bluevine and Kabbage. Bizfi also participates as a lender on the platform. Regardless of what kind of capital is sought from any of the funding partners, the small business owner is guided through the entire process by a Bizfi funding concierge that is assigned specifically to him or her.

Paul Lisiak, managing partner of Metropolitan Equity Partners stated, “Metropolitan believes that the future of small business lending is being built by Bizfi. Their aggregation and direct lending marketplace is disrupting the fast growing FinTech industry. Our new investment is the result of the impressive performance we have directly experienced as a lender and participant in the company’s financing products over the past three years. In the rapidly evolving FinTech space, Bizfi’s management team has elegantly expanded their product offerings to create a platform that holistically meets the dynamic funding needs of small businesses. We look forward to being a part of Bizfi as they further solidify their position as a leader in the financial technology space.”

Metropolitan has been an active investor in the alternative lending and FinTech space with over $100 million committed in 2015 including investments in JH Capital Group, Debt Away, New Credit America and PledgeCap.

Mr. Sheinbaum concluded, “Bizfi has seen radical growth over the last 18 months. Not only have we developed one of the most robust FinTech platforms for the small business lending space, but we have cultivated significant deals with third party companies that service small businesses. These companies will utilize white label versions of Bizfi’s platform to offer financing to their clients. Now, with the Metropolitan financing supporting our growth, we can continue to expand our products, increase our market share and provide solutions to the critical financing needs of the companies that fuel our economy.”

About Bizfi

Bizfi, is the premier FinTech company combining aggregation, funding and a participation marketplace on a single platform for small businesses. Founded in 2005, Bizfi and its family of companies have provided more than $1.3 billion in financing to over 26,000 small businesses in a wide variety of industries across the United States.

Bizfi’s connected marketplace instantly provides multiple funding options to businesses from more than 45 funding partners and real-time pre-approvals. Bizfi’s funding options include short-term financing, medical financing, lines of credit, equipment financing, invoice financing, medium-term loans and long-term loans guaranteed by the U.S. Small Business Administration. The Bizfi API provides a turnkey white label or co-branded solution that easily allows strategic partners to access the Bizfi engine and present their clients with financial offers from Bizfi lenders all while maintaining their customer’s user experience. A process that once took hours, now takes minutes.

About Metropolitan Equity Partners

Metropolitan Equity Partners Management, LLC is an alternative investment manager that provides expansion capital to growing private companies via collateralized loan structures. Metropolitan was founded by Paul Lisiak who has 20 years of experience investing in private U.S companies through both debt and equity. Metropolitan traces its roots to a successful equity strategy managed by the current Metropolitan Principals which was backed by the Man Group plc. Since 2008, Metropolitan has committed over $300MM in collateralized debt investments through call funds, blind pools and institutional managed accounts. Metropolitan is based in New York City.

Contacts

KCSA Strategic Communications

Abbie Sheridan, 212-896-1207

asheridan@kcsa.com

or

Kenneth Cousins, 212-896-1254

kcousins@kcsa.com

or

Bizfi Sales:

855-462-4934

bizfisales@bizfi.com

or

Bizfi Marketing:

212-545-3182

marketing@bizfi.com

CAN Capital: Beyond Hyperbole

December 11, 2015 It’s usually risky to say “first,” “largest” or “best,” but CAN Capital invites those superlatives and more.

It’s usually risky to say “first,” “largest” or “best,” but CAN Capital invites those superlatives and more.

Asked whether the company’s the biggest in the alternative funding business, CEO Dan DeMeo hedges only a little with qualifiers like “might” or “probably” before proudly announcing that the company has provided access to more than $5.5 billion in working capital through 163,000 fundings to merchants operating in over 540 different kinds of businesses.

Glenn Goldman, the company’s CEO from 2001 to 2013 and now Credibly’s chief executive, doesn’t mince words about his former employer when he calls CAN Capital the biggest and most profitable small business alternative finance company in the U.S.

Cofounder and Chairman Gary Johnson proclaims without hesitation that CAN Capital was the first alternative small business finance company. His wife and cofounder, Barbara Johnson, came up with the idea of the Merchant Cash Advance in 1998 when she had trouble raising funds to promote her business, he said.

CAN Capital developed the first platform to split card receipts between the merchant and funder, and it gave birth to the idea of daily remittances, Johnson continued. Within a few years of its founding the company was turning a profit, another first in alternative finance, he claimed.

The innovation continued from there, according to Andrea L. Petro, executive vice president and division manager of Lender Finance, a division of Wells Fargo Capital Finance. She cited a couple of possible firsts she’s witnessed in her dealings with CAN Capital.

When CAN Capital received a loan from Wells Fargo in 2003, it may have been the first sizeable placement in the alternative finance industry by a major traditional financial institution, Petro said. In 2010, CAN Capital was among the first alternative funders to offer direct loans, she noted.

Petro stopped short of characterizing CAN Capital as the best in the alternative finance business, but she praised the company’s management and lauded its systems for underwriting and monitoring funding. “They continually upgrade their systems, upgrade their software, upgrade their people,” she said.

Calling CAN Capital one of the best comes naturally to Kevin Efrusy, a partner at Accel Partners and a CAN Capital board member. Accel saw opportunity in alternative finance because banks were reluctant to lend at the same time that an explosion of data on small businesses was informing the underwriting process. When Accel sought a position in the industry, it contacted CAN Capital, he said.

“Frankly, CAN Capital didn’t need or want our money,” Efrusy said. “We approached them.” Five years ago, Accel convinced CAN Capital that additional resources could help the company grow, and it bought a stake in the company.

With so many extolling the virtues of CAN Capital, AltFinanceDaily asked DeMeo for a look at the thinking that underlies the success.

PLOTTING STRATEGY

CAN Capital pursues a strategy that DeMeo visualizes as a honeycomb. In the center cell, he places the objective of “helping small businesses succeed.” The compartmental element above that provides a place for the goal of serving as “the preferred provider of financial solutions to small business,” he said. The company’s cultural values, summarized as “Care, Dare and Deliver,” reside in the compartment below the center cell as table stake underpinnings, he added.

DeMeo also describes the company as driven by four strategic planks: “1) Expand the market, 2) broaden the product set, 3) deepen relationships with customers, and 4) achieve operating excellence,” he said.

What does success look like to the company? To DeMeo, it’s dramatic growth in the number of customers, resulting in increased revenue, a more valuable company and better career opportunities. “Digital automation and customer experience are at the center of those efforts,” he said.

CAN Capital operates with a “huge appetite for ‘test and learn,’” according to DeMeo. “That’s how we keep innovation alive,” he said.

And the result of all that? The company has increased fundings by 29 percent (CAGR) and revenue by 24 percent (CAGR), with corresponding growth in earnings, DeMeo said. It has also grown its digital business by 600 percent since 2014, he noted.

AT THE WHEEL

AT THE WHEEL

DeMeo, the man at the top of CAN Capital, joined the company in 2010 as chief financial officer and became CEO early in 2013. He was previously CFO at 1st Financial Bank, and also served as CFO for JP Morgan Chase’s consumer and small business unit. DeMeo also was chief marketing officer and ran business development head for GE Capital’s consumer card unit. His career began at Citibank, where he held senior roles in marketing and customer analytics.

“I was very fortunate to work for some pedigree companies earlier in my career,” DeMeo said. “Those companies emphasized market based training and development, and I worked with very smart and hardworking people. I also had great experience in unsecured lending.” His formative years left him with great appreciation for “behavioral analytics and the quantitative, information-based approach to business finance.”

Experience convinced him, as a CEO, the importance of attention to the balance sheet and income statement. It’s vital to combine that with innovation and growth orientation, DeMeo said. He seeks to lead, inspire and motivate employees, he emphasized.

DeMeo grew up in Atlantic City, NJ, with parents who valued hard work, education and maximizing opportunity. His wife and three children have supported him in his career despite the long hours and dedication necessary for success.

At CAN Capital DeMeo has faced the challenge of managing the business through internal and external cycles. Running the company often comes down to balancing what customers want with what makes economic sense, he said. “Pigs eat, and hogs get slaughtered,” he maintained. “You can’t get too greedy.”

DeMeo runs the company without the help of a President or Chief Operating Officer. While DeMeo serves as the public face of the company, he also devotes himself to every aspect of operations, he said.

WHAT’S IN A NAME?

Although CAN Capital’s drive for technological innovation and its measured approach to fundings have remained constant, the company has renamed itself several times to fit changing times.

In November 2013, it rebranded itself publicly as CAN Capital, and the company now provides access to business loans through CAN Capital Asset Servicing Inc, and Merchant Cash Advances through CAN Capital Merchant Services.

With the CAN Capital rebranding, it dropped the umbrella name of Capital Access Network. At the same time, it retired the AdvanceMe, New Logic Business Loans and CapTap names.

Most of the company’s old names applied to products or distribution channels, DeMeo said. The company had added them when it presented a new product, such as loans, or introduced a way of going to market, like end-to-end digital technology.

Consolidating the names reflected the company’s decision to put its direct marketing efforts on equal footing with business generated by partner companies, DeMeo said. Having just one name would result in a more efficient approach to building a stronger brand, he noted.

“The opportunity is to create one brand, multiple products and omni channel distribution under one company,” he said. “For a company our size, it would be hard to create brand awareness if you had to put significant promotional support behind every one of those sub brands.”

CAN Connect is a sub-brand that has survived. “That’s not a product name or distribution channel name,” DeMeo said. “It’s the technology suite we use to connect with partners so that we can exchange information in real time.”

CAN Connect is a way to speed up the process and eliminate friction for customers and partners. For example, a partner is able to link their CRM directly into CAN Capital’s decision engine, eliminating manual steps in submitting and generating offers. For partners with a customer-facing portal, CAN Connect enables an offer to be made available in real time to a small business owner, taking advantage of data sharing APIs to tailor the marketing message to fit the prospective customer’s needs.

Attention to detail pays off in repeat business for CAN Capital, in DeMeo’s view. “Almost 70% of our merchants return for another contract,” he said

THE GENESIS

By all accounts, CAN Capital is a company born of necessity. Barbara Johnson, who had the brainstorm that became CAN Capital, was running four Gymboree playgroup franchises in Connecticut and needed funds to finance summertime direct marketing efforts for fall enrollment.

But her company didn’t have much in the way of assets to pledge, so banks weren’t interested in providing funds. Why, she reasoned, couldn’t she just borrow or receive an advance against the credit card receipts she knew would flow in when the kids came back in the autumn? Thus, she gave birth to an industry.

Barbara Johnson and her husband, direct marketing executive Gary Johnson, cofounded the company as Countrywide Business Alliance and put up their own money to build a computerized platform to split card revenue, Gary Johnson said.

Then they persuaded a card processor to partner with them. Once they were operating and had signed their first customer, venture capital began flowing their way to grow the business. These days, the Johnsons remain major shareholders.

“What made it an interesting concept was how huge the market potential was,” Gary Johnson said. “That’s what the attraction still is today.” Although Merchant Cash Advances may now seem commonplace, they were startling at first, he said. “When we first went out in the marketplace, everybody thought it was a crazy idea,” he noted.

The company earned patents on processing related to Merchant Cash Advances and daily remittances, Gary Johnson said. At first, the patents deterred potential competitors from entering the business, but the company was unable to defend the patents successfully in court. Rivals then entered the fray.

Just the same, the company became profitable early on through “deliberate decision-making, having the right people in place and being bigger than everybody else,” he said.

Much of the company’s early business came through firms that provide merchants with transaction services, and that remains the case today, DeMeo said. Many were placing point of sale terminals in stores and restaurants to accept credit cards, and working capital became an upsell or cross-sell, he noted.

The large base of business CAN Capital built with merchant services companies means it will always be an important channel for the company. Recently, new merchant sign-ups have come from more diverse channels, including cobranded and referral partners, and the fast-growing direct marketing channels.

From the beginning, the merchants receiving capital used it to grow their businesses, DeMeo said. “That feeds the whole economic system and creates jobs,” he said.

TODAY’S NUTS AND BOLTS

TODAY’S NUTS AND BOLTS

Daily remittances give CAN Capital nearly constant insight into how well customers are performing, which enables the company to discover potential issues quickly and take action. Such close monitoring also provides the company with enough information to enable funding opportunities that competitors might pass up, DeMeo said.

“The basis for our decisions is how the business performs and business-specific indicators, such as capacity and consistency, versus looking at the personal credit history of the business owner,” DeMeo noted.

Having that data also helps the company create models it can use to serve other businesses in the same classification, DeMeo said. “It’s poured into machine learning for future decisioning,” he maintained. “It’s a cool concept, right?”

The company’s 450 or so employees work in several locations. Three hundred of the total are attached to the office in Kennesaw, GA, the region where the company first set up operations. To this day, that’s where the company conducts most of its business, DeMeo said.

About 25 employees work in technology and operating support in offices in Salt Lake City because the area offers a strong talent pool and provides the company with additional time zone coverage, DeMeo said.

Some of the company’s former executives came from Western Union, which had a presence in Costa Rica. About a hundred employees are now stationed there, working on technology, maintenance and development. That location also houses back-office redundancy for the company, too.

On Manhattan’s 14th Street, the company has 30 or so employees, who include digital engineers, marketing and business development teams, the human resources lead, the chief financial officer, the chief legal officer, and the chief executive officer. The company moved its executive office there from Scarsdale, NY to take advantage of the digital boom, he said, adding that, “Google’s right around the corner.”

On Manhattan’s 14th Street, the company has 30 or so employees, who include digital engineers, marketing and business development teams, the human resources lead, the chief financial officer, the chief legal officer, and the chief executive officer. The company moved its executive office there from Scarsdale, NY to take advantage of the digital boom, he said, adding that, “Google’s right around the corner.”

Compared with most companies in alternative finance, CAN Capital has little venture capital as part of its ownership structure, DeMeo said. “It’s a self-sustaining business. We’re not forced to approach the capital market to cover our burn rate. We’re cash-flow positive.” Competitors have to borrow to fund their growth, he noted.

The company has taken on infusions of debt financing, not equity financing. In the latter, a company is selling part of itself, DeMeo said. “We raised $650 million from a syndicate with five new banks and 10 banks in total.” The company completed a securitization of $200 million the year before, he said.

CAN Capital recently introduced the new TrakLoan product that has no fixed maturity date, with daily payments that are based on a fixed percentage of card receipts. This way, payments ebb and flow with the merchant’s card sales. CAN Capital is also testing “bank-like” installment loans of as much as $500,000 with a payback period of up to four years.

And there’s nowhere to go but up, in the view of CAN Capital executives. With a market of 28 million small American merchants and penetration of between 5 and 10 percent, they see plenty of potential to keep earning superlatives.