Real Estate Crowdfunder Patch of Land Returns $25 mn to Investors

March 24, 2016Patch of Land has returned $25 million to investors this year, a quarter of its originations at $100 million.

The LA-based online lender for real estate loans also expanded its business to Hawaii, marking its presence in 36 states. The company uses a data-driven underwriting model and promises investors a risk adjusted return with extensive available data to support the underlying credit decision on each loan.

Earlier this month, Patch of Land started selling mid-term loan option for 2-5 years starting at 6 percent, extending its typical short-term loans starting at 10 percent for up to two years. It sells ‘bridge loans’ ranging from $100,000 to $5 million to cover the borrower until they can secure permanent capital or those who may not immediately qualify for long-term financing on properties that they rehabilitate and then hold as rentals. As far as demands for these loans go, the company’s CEO Jason Fritton said bridge loans generated $40 million in loan interest in less than two weeks since.

The three year old startup signed a $250 million agreement with an east coast based credit fund to purchase its loans in a forward flow arrangement. Last year, it raised a million in seed funding and $125,000 in debt in 2014, followed by $23 million in Series A funding last year when it funded more than 200 projects, with an average blended rate of return to investors of 12 percent.

CEO of RealtyShares, a real estate crowdfunding platform Nav Atwal in a Forbes post said enlisted reasons why commercial real estate is investor friendly — 12 percent annual returns, tax benefits, hedge against stock market and inflation being some of them. But for larger context, the commercial real estate environment is of caution among lenders towards big projects. Real estate firm CBRE said that it “conservatively” estimates that 18 percent of loans this year and 29 percent of loans next year to have refinancing problems as investors move away from commercial real estate bonds. CBRE estimates $43 billion to be in “troubled loans” over the next two years.

Bizfi Partners With West Coast Banking Group

March 17, 2016Bizfi will be the exclusive alternative finance solutions provider for small businesses that are members of the Western Independent Bankers, a trade association of community banks in the west coast.

Small businesses in the midwest and west coast in states including Alaska, Arizona, California, Colorado, Hawaii, Idaho, Montana, Nevada New Mexico, Oregon, Utah, Washington and Wyoming can benefit from this partnership. Bizfi’s marketplace partners with lenders like OnDeck, Funding Circle and Kabbage.

“WIB member banks are the leading funders of America’s small businesses,” said Michael Delucchi, President and Chief Executive Officer of WIB and WIB Service Corporation. “With Bizfi as a WIB Premier Solutions Provider we are able to offer their expertise in alternative financing and superior technology to our member banks and deliver a complete solution for small business funding.”

Earlier this month, Bizfi partnered with The New York State Restaurant Association to provide business financing for its 2,000 small businesses in the restaurant space.

Banks Admit They’re Scared of Startups

March 16, 2016If you cannot keep up with everything that is happening in fintech, you are not alone.

In the post financial crisis world, fintech startups perched themselves in the crevice between the big world of banks and the regulatory reform which controls their free reign. And since then, financial upstarts have only multiplied.

From P2P insurance, realty crowdfunding, marketplace loans and not to forget bitcoin, the capital infusion in fintech testifies for the market hype. In its report in November last year, CB Insights estimated that $24 billion has been invested in fintech startups and half that amount ($12.2 bn) was invested in 2015 alone.

It can be argued that some of these startups with multibillion dollar valuations are essentially smaller banks without the frills. Take SoFi for example, the San Francisco-based online lender is which worth $4 billion known for its touting we-are-not-a-bank image but provides most services from student loans, mortgage lending, personal loans to loan refinancing without the “bank branch.” The company also wants to start a hedge fund.

So, are the banks feeling left out? It depends on whom you ask, but a recent report from PwC surveying 544 CEOs, revealed that 23 percent believed their businesses were “at risk” by fintech innovation and 67 percent of the respondents said that they were under profit margin pressure.

“We thought we knew our customers, but FinTechs really know our customers,” the report quoted a senior bank official as saying. The report ranked consumer banking, payments and wealth management to be disrupted the most by these fintech startups.

The big bucks and the hype that follows it has made regulatory authorities sit up and take notice of the financial services upstarts and bring them under the supervisory purview. And while that may be legitimizing their foothold on the industry, the real questions around project revenues, possible exits and the companies’ wherewithal to handle a complex credit market remain unanswered.

Are we really at a tipping point of innovation or is it just new wine in old bottles?

Google Culls Online Lenders – Pay or Else?

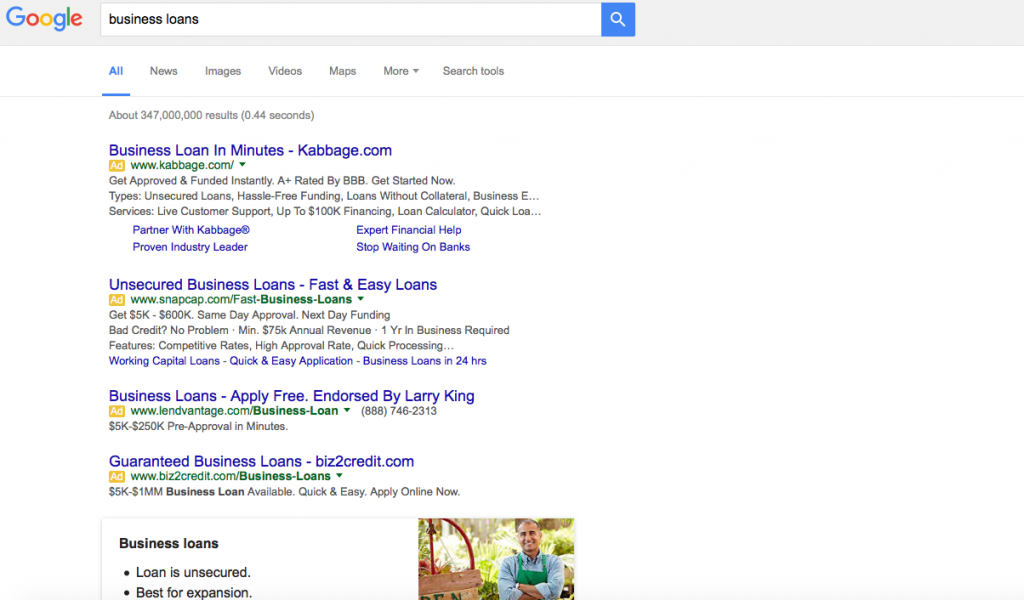

March 15, 2016Can you become one of the biggest or most successful online lenders without Google? A search layout update may be inadvertently culling the herd.

In late February, Google eliminated ads from the right side of the page while adding another layer to the top and bottom. When factoring in features like site links, the effects on organic search has been devastating. Non-paid links are now entirely below the fold for many commercial keywords, which means users may limit their selections entirely to ads. Here’s an example of a full screen browser window on a Macbook Air when searching for Business Loans:

Brad Geddes, a Google Adwords marketing author, expert and consultant, has said the Click-through rate (CTR) on this new 4th ad placement is skyrocketing. “Depending on the keyword, position 4 is going to have a 400%-1000% CTR increase,” he said on Webmaster world. And while side links and bottom links were never a huge factor anyway (less than 15% of click-throughs), Geddes believes a consequence of this change is that fewer ad slots means higher cost bids to rank on the 1st page. “Companies with thin margins are going to have a lot of words fall to page 2,” he wrote.

In summary: Fewer ad placements, higher costs per click, decreased likelihood of organic click-throughs.

And the online lending industry is already feeling the burn. Several funders and ISOs on the commercial side have told AltFinanceDaily in confidence that the online lead gen battle has been lost or that they have been temporarily sidelined by the increase in costs. At least one funder is refocusing their efforts entirely on the ISO channel after a horrible experience with Pay-Per-Click.

And it’s not just the costs, it’s the quality of leads, they say. The searchers clicking their expensive ads and running up their bills sometimes literally meet none of the qualifications their ads stipulate. Yet many searchers click anyway, rendering the ads’ carefully scripted messages moot. One study might explain why that is. In it, users spent around .764 seconds considering the first paid search result and a total of only 4.5 seconds scanning the first five results. That’s not a whole lot of time to read each ad, digest them and consider whether or not there’s an appropriate fit.

And it’s not just the costs, it’s the quality of leads, they say. The searchers clicking their expensive ads and running up their bills sometimes literally meet none of the qualifications their ads stipulate. Yet many searchers click anyway, rendering the ads’ carefully scripted messages moot. One study might explain why that is. In it, users spent around .764 seconds considering the first paid search result and a total of only 4.5 seconds scanning the first five results. That’s not a whole lot of time to read each ad, digest them and consider whether or not there’s an appropriate fit.

On one industry forum, ISOs have reported that the cost of acquiring a merchant cash advance or business loan deal from Pay-Per-Click is ranging from $700 to $1,200. “PPC for premium keywords as high as $40 at times. Ugly. Real ugly,” one user wrote. Another user wrote, “It’s not just Adwords that is saturated. The whole market is saturated. Lenders and the onslaught of new brokers are making it tough. Lenders with programs like Funding Circle and Kabbage, and with all the advertising money in the world to burn and get direct traffic.” And still another believes that online ads are simply inviting the lowest hanging fruit. “Internet leads have the highest level of fraud,” said one sales manager.

Notably, many of the top 8 funders are only competing for a limited number of competitive keywords or may not even be running Adwords at all. PayPal and Square for example, focus only on their existing payment processing customers despite being “online lenders.”

It’s too early to tell what effects Google’s ad changes will have on the online lending industry, though a couple of companies who were paying just enough to extract clicks from side ads have indicated the change is for the worse and they have suspended their campaigns.

The natural alternative to paid search, organic search, is seldom discussed anymore as a realistic strategy these days, in part because the rankings might be rigged anyway.

One irony that’s pervasive in the online lending industry is that borrowers are being targeted offline where it’s potentially more affordable. In a discussion thread that garnered 76 posts last fall, ISOs and funders suggested that direct mail, referrals, UCCs, cold calling, radio and even going out and shaking hands, were pegged as “what’s next” for marketing. Pay-Per-Click was only mentioned once and only in the context of it being something that had long ago been made too expensive for small and mid-size companies.

The cost of making these things work might be why so many funders are hoping that brokers can figure it out. “We decided that the best way to grow is to build relationships to avoid the overhead, compliance, training and manpower that a sales team would require,” said Nulook Capital’s Jordan Feinstein in an interview with AltFinanceDaily last month.

With Google becoming even more competitive now though, perhaps United Capital Source’s Jared Weitz summed it up best. “Marketing is getting more expensive and only the ones who can afford to pay can play,” Weitz said.

Yellowstone Capital Welcomed to New Office Location By City Mayor

March 8, 2016 It’s a change of scenery, insiders at Fundry subsidiary Yellowstone Capital say about their new office.

It’s a change of scenery, insiders at Fundry subsidiary Yellowstone Capital say about their new office.

The company has officially relocated from 160 Pearl Street in Manhattan to 1 Evertrust Plaza in Jersey City. On their first day in the new location, Jersey City Mayor Steven Fulop made an appearance and posed for a photo with company executives Isaac Stern and Jeff Reece to celebrate their arrival. Aside from outgrowing the NYC office that they operated from for years, Yellowstone was wooed to the State by the New Jersey Economic Development Authority to create jobs in the area in exchange for a tax incentive. The hundreds of employees they bring with them to the neighborhood now will also serve to stimulate Jersey City’s burgeoning economy.

The company originated close to half a billion dollars in funding for small businesses in 2015.

Just one stop from the Path Train’s World Trade Center station, Yellowstone’s new office environment makes it feel as if the company has been transported a million miles away. AltFinanceDaily was given a tour of the new space, which at 25,000 square feet, was easy to get lost in. One employee said the upgrade from their previous location felt so immense, that it felt like they had moved to Japan.

Just one stop from the Path Train’s World Trade Center station, Yellowstone’s new office environment makes it feel as if the company has been transported a million miles away. AltFinanceDaily was given a tour of the new space, which at 25,000 square feet, was easy to get lost in. One employee said the upgrade from their previous location felt so immense, that it felt like they had moved to Japan.

A clear view of NYC’s Freedom Tower from many of the floor’s windows assures them that they are not that far.

Bizfi Woos Restaurants With Lending Products

March 3, 2016The New York State Restaurant Association signed Bizfi to provide business financing for its 2,000 members.

The New York-based financial platform will be the designated funder of equipment financing, invoice financing, lines of credit, medium term financing, short-term financing, franchise financing and long-term loans from more than 45 partners.

“Restaurants have unique funding needs and owners often do not have time to spare in order to complete the long application process at traditional lenders,” said Stephen Sheinbaum, founder of Bizfi.

Bizfi’s lending partners include all the major lenders in the industry including OnDeck, Funding Circle, Kabbage, IMCA Capital, Bluevine, and SmartBiz and the company has funded over $1.4 to over 27,000 small businesses since 2005.

![]()

Lending Club Class Action Lawsuit Predicated on Madden v Midland Risk

March 2, 2016UPDATE: This case is unrelated to another class action filed against Lending Club on April 6th

Lending Club is the latest publicly traded online lender to get hit by a shareholder class action lawsuit (OnDeck was first). Filed in the Superior Court of the State of California, plaintiff alleges in the complaint that Lending Club misleadingly concealed the fact that:

- Lending Club had an unsustainable business model that was predicated on it being able to issue loans with extremely high and/or usurious rates across the country

- that their loan investors would not be able to enforce the extremely high and/or usurious rates imposed by Lending Club because they violated state usury laws

- that without the extremely high and/or usurious rates, the loans generated through Lending Club’s marketplace would not be attractive to investors because the loans had very high credit risk and were subject to issues concerning insufficient documentation

- that a substantial portion of its loans were issued with rates in excess of those allowed by applicable state usury laws

The action seeks “recovery, including rescission, for innocent purchasers who suffered many millions of dollars in losses when the truth about Lending Club emerged and the its stock price plummeted.”

Among the Defendants is former US Treasury Secretary Larry Summers.

The complaint alleges that the truth about Lending Club began to emerge after “the Second Circuit affirmed [in Madden v Midland] that the business model used by Lending Club was not valid because loans sold by banks to non-banks, third parties (such as Lending Club and its investors) are not exempt from state usury laws that limit interest rates.”

–In actuality, no such affirmation was made. Lending Club does not specifically use Midland Funding’s business model and the case was not about Lending Club, nor was Lending Club mentioned in it.

“Specifically, the Second Circuit observed that assignees and third-party debt buyers could not rely on the National Bank Act to export interest rates that were legal in one state but usurious in another, to the states where those rates were impermissible,” the complaint states.

–Perhaps, but Lending Club’s bank makes loans under the Federal Deposit Insurance Act, not the National Bank Act.

As supporting evidence, the complaint cites statements from Moody’s analysts, Morgan Stanley, Cross River Bank CEO Gilles Gade, and Lending Club CEO Renaud Laplanche himself in a quarterly earnings call.

While the impact of Madden v Midland has been seriously overblown, Lending Club’s stock has no doubt taken a beating since its IPO. The complaint states a loss of 43% from the original offering price. Among the defendants are:

- LendingClub Corporation

- Renaud Laplanche

- Carrie Dolan

- Daniel Ciporin

- Jeffrey Crowe

- Rebecca Lynn

- John J. Mack

- Mary Meeker

- John C. (Hans) Morris

- Lawrence Summers

- Simon Williams

- Morgan Stanley & Co. LLC

- Goldman, Sachs & Co.

- Credit Suisse Securities (USA) LLC

- Citigroup Global Markets Inc.

- Allen & Company LLC

- Stifel, Nicolaus & Company, Incorporated

- BMO Capital markets Corp.

- William Blair & Company, L.L.C.

- Wells Fargo Securities, LLC

NOTE: This case is unrelated to another class action filed against Lending Club on April 6th

OnDeck Regains Their Swagger in Q4 Earnings Call – Lends $1.9 Billion in 2015

February 23, 2016 OnDeck’s chief executive Noah Breslow and chief financial officer Howard Katzenberg brimmed with confidence in their Q4 earnings call, assuring investors that it’s full steam ahead. After two previous quarters of profitability and getting no love from the market for it, they’re back to doing what they know best, growing.

OnDeck’s chief executive Noah Breslow and chief financial officer Howard Katzenberg brimmed with confidence in their Q4 earnings call, assuring investors that it’s full steam ahead. After two previous quarters of profitability and getting no love from the market for it, they’re back to doing what they know best, growing.

OnDeck loaned a record $557 million in Q4, an increase of 51% year-over-year. Despite market fears of an impending economic downturn, the company is just not seeing signs of the alleged doom in the performance of their loans. “We are not seeing weakness in our portfolio at this time,” Breslow said.

Later in the call they reemphasized that their early warning systems are not setting off any alarms. In fact, they said, origination growth is their main goal in 2016. “We currently believe we can grow annual originations by 45% to 50% in 2016,” Katzenberg said.

OnDeck reminded investors that their unique model is specifically built for economic downturns. Among their strengths are their short duration, pricing spreads and daily payments, they said. Those attributes (which are sometimes criticized by consumer groups today) will serve as the backbone of sustainability if the economy goes south.

Also coming back into the fold are outside brokers, which they refer to as “Funding Advisors.” OnDeck spent a lot of time recertifying those relationships in 2015 and the bulk of the effort associated with that is over, they said. The percentage of loans generated from brokers rose from 18.6% in Q3 to 20.1% in Q4.

They also rebuffed speculation that they were giving up their business model in favor of becoming a bank technology service. While they admitted finding value in the partnerships they’ve formed, particularly with JPMorgan Chase, their core business is and will continue to be lending to small businesses. According to Katzenberg, 2016 will have two key objectives however, “One, launching and refining our pilot program with Chase, and two, continuing to build out our infrastructure to add and support additional partners that understand the small business capital assets problem and are willing to invest in a great customer experience.” They expect to see bank service revenues really begin to scale in 2017 and 2018.

Breslow said in regards to the Chase deal, “Chase will be able to offer almost real-time approvals in the same or next day funding a dramatic improvement over a traditional loan process that might take weeks. Chase will hold the loans, which will be priced like bank products on their balance sheet and OnDeck will earn servicing and platform fees based on volume.”

Their 15+ Day Delinquency ratio was down.

Their partnerships with Minor League Baseball and Barbara Corcoran have been very successful.

They lent $1.9 billion in 2015 across the U.S., Canada, and Australia.