Kabbage Boosts Platform Biz, Partners with Canadian Bank Nova Scotia

June 22, 2016Online lender Kabbage loans has partnered with Canada’s third-largest bank, Bank of Nova Scotia to offer online loans to small businesses.

Small businesses in Canada can apply for loans online and get a decision quickly. The program will be extended to businesses in Mexico later this year. Customers will have the flexibility to draw the funds as individual term loans, from as little as $1,000 in Canada and each loan can have its own repayment terms.

In an interview with AltFinanceDaily earlier this month, Kabbage co-founder Kathryn Petralia said that the company wants to grow its platform business with such partnerships. In April this year, Spanish bank Banco Santander said that it will use Kabbage’s technology to underwrite loans up to £100,000 the same day for loans that typically take 2-12 weeks to process.

Santander, Nova Scotia and ING together invested $135 million in Kabbage’s series E funding.

The Unsung Disruption in Online Lending – Stacking, Litigation and Questionable Debt Negotiators

June 22, 2016

Give a small business two options, a low APR 3-year business loan and a short term loan with a high factor rate, and you’ll find advocates for each product arguing over which is better and why. We’ve been led to believe that it’s one versus the other, that one is good and one is bad, and that’s all there is to the story. Entire business models have been developed along the lines of this thinking, algorithms deployed and merchants funded, along with narratives framed in the mainstream media about why one system is superior to others.

But to hear the men and women in the phone rooms tell it, when given a choice between one funding option or the other, small businesses are often choosing both at the same time. Reuters said that stacking is the latest threat to online lenders, and in many ways they’re right. The practice isn’t new of course, the tendency for merchants to take on multiple layers of capital (often times in breach of other contracts) has been a central cause of tension between funding companies for the last few years. But the reason the story is bubbling over into traditional news media now as the latest threat, is because opponents of stacking assumed that the practice would be eradicated by now. There was this false sense of hope that government agents in black suits would show up one day unannounced after hearing that a merchant had taken a third advance or loan despite having not yet satisfied the obligations of the previous two. And when that didn’t happen, some of the models heralded as better for the merchant started to show cracks. What happens to the forecasts when the merchants priced ever so perfectly for a low rate long term loan go and take three or four short term loans almost immediately after? Back in October, Capify CEO David Goldin argued that long dated receivables were already dangerous to a lender regardless because the economy could turn south. “You’re done. You’re dead. You can’t save those boats. They are too far out to sea,” he told AltFinanceDaily.

Sue everyone?

When it comes to disruption, nothing has changed the game as much as stacking, and companies must prepare for the likelihood that it could be around forever. That means forming a long-term business model that is equipped to deal with this practice. Several lawsuits have been waged in an attempt to generate case law to deter it, including one filed last year in Delaware by RapidAdvance against a rival. Patrick Siegfried, assistant general counsel of RapidAdvance told the Wall Street Journal last fall, “we’re doing it to establish the precedent,” he said. “This kind of thing is happening more and more.” At the time, a motion to dismiss the case entirely was pending. RapidAdvance since won that motion but only by a hair and with a judge that was very reluctant to move the case forward.

Last October, MyBusinessLoan.com, LLC, also known as Dealstruck, sued five companies at once, a mix of lenders and merchant cash advance companies after one of their borrowers defaulted, allegedly because of actions carried out by the co-defendants. They were greeted with several motions to dismiss for failure to state a claim.

Even if these funding companies don’t win, simply letting the world know that they’ll sue rivals for stacking can act as a deterrent. But it’s an expensive tactic, especially when some defendants are more than happy to litigate the claims. Litigation is definitely an underrated cost of doing business for online lenders and merchant cash advance companies. In one recent case, a merchant challenged the legitimacy of a contract with Platinum Rapid Funding Group, a company whom they sold a portion of their future receivables to. The merchant asked the judge to recharacterize the contract to a loan so that they could try to use a criminal usury defense. The judge refused in a well-written decision that called the merchant’s attempt to do that “unwarranted speculation.” But even with the precedent of a favorable ruling, countless merchants have attempted to come up with strategies to wriggle their way out of their agreements, sometimes with ample legal counsel at their side.

Debt negotiators and questionable characters

Stacking has become a cost of doing business, but something else is creeping in as well. An entire cottage industry of “debt negotiators” has set their sights on online lenders and merchant cash advance companies, and at times these self-professed business experts don’t even realize there’s a difference between the two. One MCA funder told altfinancedaily earlier this week that a merchant in default claimed to be represented by Second Wind Consultants, a debt restructuring firm that lists one Don Todrin as the CEO on their website. Not mentioned among Todrin’s accolades is that he is a disbarred attorney who pled guilty to federal bank fraud charges in 1994, according to an old report by the Boston Globe, after he filed at least nine false financial statements to acquire $1.4 million in loans.

Another purported debt negotiation firm, who has the irked the ire of merchant cash advance companies, is apparently trying to assert affiliation to a native American tribe and invoke tribal immunity in response to lawsuits against them, according to court filings in New York State.

And only three weeks ago, an attempted class action against a merchant cash advance company failed because each named class representative had waived its right to participate in a class action in exchange for business financing. The initial action, before being moved to federal court, was brought by a merchant represented by an attorney who had just been reinstated to practice law, following a long suspension for pleading guilty to identity theft.

On top of it all, there are merchants themselves that act in bad faith, with some preying on the perceived vulnerabilities of an online-only experience. In the November/December 2015 issue of AltFinanceDaily Magazine, attorney Jamie Polon said some applicants don’t even own businesses at all, they just pretend to. “They’re not just fudging numbers – they’re fudging contact information,” he told AltFinanceDaily. “It’s a pure bait and switch. There wasn’t even a company. It’s a scheme and it’s stealing money.”

Weeding out bad merchants is a job for the underwriting department but for the good merchants seemingly deserving of those 3-5 year loan programs, the future is not as easy to predict as it once was. They might stack regardless, no matter how favorable the terms are. And given that government agent ninjas aren’t likely to drop down from the sky to stop them any time soon, many funding companies are faced with hard choices. Are the initial forecasts still valid? Is it economically feasible to turn the client away for additional funds because they breached their original agreement, all while the cost to acquire that customer in the first place was really high? Do you sue your rivals, make them look bad in the press, or lobby for regulations that will hurt them? How do you handle the new breed of debt negotiators who use the same UCC lead lists as lenders and brokers?

Sure, things like marketing costs are going up and the capital markets are less inviting than they used to be. But once loans and deals are funded, making sure those agreements are lived up to can take time, resources, and undoubtedly a lot of lawyers. And realistically, these issues aren’t likely to change any time soon. Help, in whatever relief form some are hoping for, is not on the way. How’s that for disruption?

Taking Stock of China’s Changing Fortunes in Fintech

June 21, 2016

It’s been called the Wild West of the financial world, and it appears the sheriff is finally headed to town.

Chinese fintech, the P2P practice of connecting borrowers to lenders via the Internet, was supposed to bring much-needed competition and efficiency to the country’s outsized, government-run banking system, turning a sizable profit for a visionary group of investors in the bargain. Investors weren’t the only ones that stood to benefit from the boom. With large Chinese banks choosing to lend primarily to mammoth, state-owned corporations, the country’s small business community was similarly poised to profit.

That’s exactly how it played out for a while. Buoyed by bullish expectations, fintech startups with good marketing skills attracted large numbers of investors. This resulted in nearly a decade’s worth of easily amassed capital, dizzying returns in high interest rate bearing vehicles, and little in the way of meaningful regulation. Before you could say “Alibaba”, roughly one fifth of the world’s largest fintech firms hailed from China, with ZhongAn, an online insurance group backed by the e-commerce titan’s founder, Jack Ma, topping the list.

It was indeed the Wild West, but there was trouble on the horizon.

The twin villains irrational exuberance and negligent oversight eventually flipped the script, and China’s fintech sector has been reeling ever since. Returns derived from investing “captive capital” into funds that returned high spreads started drying up. Payment companies came under fire for questionable practices that at least one investment research firm, J Capital Research, likened to a Ponzi scheme. Doubt set in, followed by panic. Capital began flowing out of the country instead of into it, with investors that could head for the exit door doing just that.

By the end of 2015, nearly a third of all Chinese fintech lenders were in serious trouble, according to a recent article in the Economist, “trouble” being defined as everything from falling returns to halted operations to frozen withdrawals.

A few brave souls stuck to their guns, wrangling over how to make their finance models more sustainable for the long haul. Other so-called industry leaders simply skipped town. Literally. Enter “runaway bosses” into your preferred web search engine and the hits keep coming. According to the same Economist article, the delinquent bosses of some 266 fintech firms have fled over the past six months alone. It’s a worrying trend that pessimists say represents yet another nail in the coffin of China’s so called “Era of Capital.”

I wouldn’t be so sure.

Emerging trends will always be susceptible to periods of protracted volatility. It’s how industry leaders – and government officials – respond to such crises that lays the groundwork for what happens next. Now, the “maturation” process has begun in China. Unfortunately, to date it’s happened exclusively in the form of mass consolidation, with the state sector swooping in and taking over what was up until now a strictly private sector trend.

The Chinese government’s fondness for consolidating its interests is no state secret of course, but it would be a mistake for it to use the failings of the fintech sector to reassert the dominance of the country’s state-owned banking sector. The reason for this is straightforward enough. Big banks aren’t usually the biggest allies of small business, and every economy needs a robust small business sector in order to thrive.

Where could the Chinese government look for guidance? Not the US, unfortunately. If anything, the fintech market in America suffers from too much regulation. Everyone knows there’s no friendlier country on the planet for budding entrepreneurs than the US, and you certainly don’t have to look far to find examples of fast-growing American fintech success stories. You could go so far as to argue “disruptive innovation” in the financial sector is in our DNA, from the rise of Western Union to the emergence of giant credit card companies like Visa and Mastercard to the recent arrival of game changers like Lending Club, OnDeck and Venmo.

And yet, ask any fintech startup CEO about the thicket of regulation he or she has to routinely navigate in order to figure out which agencies have jurisdiction over, or which laws apply to, the various aspects of their businesses. Better yet, don’t. The alphabet soup of regulatory bodies they will be obliged to list – the SEC, the Fed, FINRA, OCC, FDIC, NCUA, CFPB, etc. – will put you both to sleep. The point is that these days the US lags behind other regions of the world in creating the environment the fintech industry needs to flourish. (One discouraging example: In the United States, the licenses needed to become a money services business (MSB) have to be acquired on a state-by-state basis; in the European Union, a single license is all it takes to do business in Berlin, Paris, Madrid, and Rome.)

Making finance safer is one thing, but blinding business with an unusually harsh regulatory spotlight isn’t the answer.

Why does it matter if the fintech sector goes belly up in China, the US, or anyplace else? To reiterate: Fintech isn’t some passing trend or get-rich-quick scheme. It’s one of the essential engines that drives small business development. According to the site VentureBeat.com, the World Economic Forum recently reported that a healthy fintech industry could close a $2 trillion funding gap for small businesses globally. You could drive a healthy uptick in the global GWP through a gap that size.

This brings us back to China. Chinese regulators may be tempted to capitalize on the country’s fintech troubles to reassert their influence, but they should strongly resist the urge. Instead, they might focus their efforts on taking steps to create a healthy ecosystem for the country’s fintech sector, one with regulatory controls that are clear, efficient, and properly implemented. Transparency will be key. One of the things American fintech companies do right is publishing essential information about those seeking loans, including their credit history, employment status, and income. This is to ensure that the investors putting up the money know what they’re getting into. It’s a critical confidence-builder, and China’s fin-tech model will need to be similarly transparent if it wants to succeed.

I happen to believe that it will succeed, and that it will continue to attract big money. The case could be made that it’s already happening. In December 2015, Yirendai, the consumer arm of P2P lender CreditEase, became the first Chinese fintech firm to go public on an overseas exchange, listing on the NYSE with a valuation of around $585 million. In January of this year, Lufax, a platform for a range of products, including P2P loans, completed a fundraising round that valued the company at $18.5 billion, setting the stage for a highly anticipated IPO.

Both companies pride themselves on their transparency protocols and risk controls.

The bottom line is this: No financial sector benefits from descending too far into a Wild West of laissez-faire everything, and China’s regulators were right to ride to the rescue. They would do equally well not to strong arm the sector’s brightest leaders. The country should strive to create a safe, healthy environment for third-party service providers to prosper and grow. If they do, it won’t just be investors in mobile transactions and digital currencies who benefit.

China’s entire economy will.

Balance Letters, Payoff Letters, And Not Letting Go

June 10, 2016

The following is a guest-authored opinion piece on the business financing space

Everyone is struggling to keep their head above the water. Just imagine the scene in the movie Titanic. Currently we are in the scene where they zoom out to show the ship sinking slowly with more people in the water trying to survive than on the ship. “Never letting go” is something everyone is doing and clinging on to whatever floats is the only way to survive. The decline in submissions and quality of funded deals is one aspect that many Funding Companies are realizing. No one is letting go of a piece of their portfolio without a fight.

For many A/B paper (for those who go by the grade system) or the Prime to Sub-Prime, 1st position companies know what I am talking about and it’s time to come clean on the truth and the real perception of why things are the way they are.

You can’t get that payoff letter because that Funding Company does not want to let go of their good paying Merchant. Whether the funding was originated from a Broker or organically, that Business is in bed with that funding company and did not have any intention of breaking a relationship until the option was brought to their attention. Whether this Merchant was solicited by another Broker or the Merchant decided to take it upon themselves to seek additional funding, there is one thing that will most often happen.

As soon as the Funding Company receives a request for a payoff letter or balance letter, they will ask why it is needed or delay the process in releasing one or not give one at all until the Merchant is 100% positive and the reasoning and demand is final. Is there anything wrong with this?

To a Broker? Yes. To a Business Owner? No. As many Brokers will fight and try to justify the circumventing of their Merchants, in this case, this is not circumventing at all. The Business has a contract with the Funding Company and until they have a zero balance, that Funding Company has the right to review their account and offer additional funds or discounts to keep their business. This is how it is with any company. Try calling your cable company to cancel your service. What do they do first? They transfer you to the reconciliation department to try to appease you, offer you free or discounted features, and find out what they did wrong or what company you are switching to. Companies are always trying to improve their service and give their clients the best experience.

Throughout the years, if the original Funding Company could offer a better rate or term than what the competing offer is, it has always been in the best interest of the Merchant to continue with that original Funding Company. It is NOT in the best interest nor is it ethical to put the Merchant in another position that will hurt the business or “double up” contracts to equal an amount if ONE company cannot adhere to the request. “Stacking” by offering a second position is one thing, squeezing in as many positions is another, and over time it has hurt many 1st position Funding Companies.

Fast forward to now, the rise in funded accounts that have “defaulted” may have fallen victim to the promises of something better. There is no one educating or clearing the air that there probably isn’t something better… but that advice won’t make anyone commissions and those Funding Companies still rely on Brokers to bring in submissions.

There has been no recourse on this issue, rather growth, and those who have paved the way have found their path covered in dirt. Stomping in this path are other funding companies who have adopted practices from veterans but feel the need to set hierarchy to something they can’t control.

So, with that said, who really sets the rules to what is fair when we are all walking on egg shells? The cost of acquiring a customer and the cost of losing one is an expensive and tricky loss. It is safe to say that once a Merchant is stacked- there is no going back. Should ethics rule over the choices and fate of a Business? Should we put more emphasis on realistic expectations before and after a Business is funded?

A simple request for a payoff letter can open a can of worms. The underlying factors of the difficulties companies face in our industry are all brought upon by the decisions we make when working with each Merchant. At the end of the day you have to ask yourself- am I helping or am I hurting the Business?

Shanda Group Now Owns 15% of Lending Club

June 8, 2016 It’s time for that update in the Lending Club saga.

It’s time for that update in the Lending Club saga.

After exiled CEO Renaud Laplanche sold 1.2 million shares worth $5.3 million, in the company he founded, Chinese billionaire Tianqiao Chen raised his stake in the company to 15 percent from 11 percent.

Chen’s company Shanda Group had upped its stake to 11 percent last month, making it the lender’s largest shareholder without an active management role.

Last week (June 8th) Renaud Laplanche was said to be in talks with banks and hedge funds to take the company private while the beleaguered lender was in negotiations with three hedge funds – Och-Ziff Capital Management, Soros Fund Management and Third Point to fund potentially $5 billion in loans and earn rights to own equity.

Prior to that, the San Francisco-based company had postponed its annual shareholder meeting from June 7th to June 28th and raised interest rates by 55 basis points while reducing the debt to income criteria by 12 percent.

“Given the developments of the last few weeks, the company is not yet in a position to provide its stockholders a complete report on the state of the company,” the company wrote in a SEC filing.

Below is a timeline of what 2016 has been like for Lending Club.

May

On May 9th, CEO Renaud Laplanche resigned after the board found that the company had sold an investor loans worth $22 million which violated terms given by the investor.

Three days later, on May 12th, a consortium of 200 community bank suspended their purchases of Lending Club loans.

On May 17th, Lending Club was subpoenaed by the Justice Department.

On May 23rd, the company revealed that a group led by Chinese billionaire Chen Tianqiao had upped its stake in Lending Club to 11.7%, giving it significant influence in the company.

On May 24th, the US Solicitor General published a legal brief that argued that the US Court of Appeals for the Second Circuit erred in its ruling on Madden v Midland, reducing the odds that the US Supreme Court will hear the case, and diminishing the potential negative impact that the ruling could have on Lending Club’s business model.

On May 25th, the WSJ reported that a fund Lending Club controls had strayed from its intended parameters and bought riskier loans than it had intended.

April

Ironically, in April, Lending Club along with Funding Circle and Prosper had joined forces to create a collaborative non-profit body, i.e. a trade association to promote transparency in lending.

In a SEC filing on Thursday (April 21), Lending Club notified the bureau that it will increase interest rates by 23 basis points in grades D-G and also updated its loss projections.

Later that month, the firm was in talks with Goldman Sachs and Jefferies Group to put together its first big bond offering backed by unsecured loans.

March

Lending Club filed its revised Loan Receivables and Sale Agreement and Marketing Agreement with WebBank as part of its 8-K filing on March 2nd. This revision was made to give WebBank more of a stake in the risk of each loan.

On March 8th, in an interview with Bloomberg, Renaud Laplanche said that he sees no credit deterioration and justified the rate hikes done in February as a means to cover losses should the economy slow down.

On March 22nd, the lender said that it was shifting its focus back to retail investors and invest in technology to serve them better, going back to its marketplace roots and reducing its dependence on Wall Street hedge funds and banks.

February

In February, perhaps taking cues from the Madden vs Midland case, Lending Club announced that it had changed its fee model with WebBank and also raised rates it charged to borrowers.

Completing a year since IPO, the company swung to a profit of $4.6 million, its second quarterly profit.

Earlier in February, JP Morgan acquired Lending Club loans worth $1 billion for a premium, in which borrowers had a 700 FICO score on average. This was a month after Santander sold Lending Club loans worth $1 billion in January.

‘We Serve a Fragmented Market That is Ripe for Disruption,’ says Patch of Land CEO

June 3, 2016$484 million: That’s how much real estate crowdfunding platforms attracted in 2015, which was three times of that the previous year. There are an estimated 125 such portals and the new SEC rule which allows non accredited investors some leniency to invest in these projects. To demystify real estate crowdfunding, AltFinanceDaily spoke to Patch of Land’s CEO Paul Deitch to unravel the concept, measure the momentum of investor interest and the regulatory environment. Here are excerpts from the interview.

What’s on the horizon for Patch of Land this year?

Now that Patch of Land’s model is proven, we will be adding complimentary products for the real estate entrepreneur and investor, accompanied by a broadening of funding strategies. For example, we recently launched the new midterm loan product that addresses the opportunity in the $4 trillion single-family rental space.

How is the investment momentum different from that in ‘08-’09?

One of the biggest changes between then and now has been the enactment of the JOBS Act, which actually came about as a result of investment conditions in ‘08-’09. Peer-to-peer lending came into existence during the 2008 Recession when consumers and small businesses could not rely on banks for their funding needs. In 2012, President Obama signed a historic bill called the JOBS Act (Jumpstart Our Business Startups Act), allowing companies to raise working capital in the form of debt and equity via a crowdfunding model. When the SEC implemented Title II of the JOBS Act in 2013 it allowed companies to publicly solicit, via Internet marketing, their equity and debt offerings; private placements could now be advertised. Marketplace lending is an evolution of peer-to-peer lending, defined by the participation of traditional financial institutions purchasing the loans being issued by P2P lenders.

Whom do you consider your competition in the industry and how do you differentiate yourself from them?

We approach the competition question from a different perspective. One would think that other online lenders or real estate crowdfunding companies are our competition but they are not. We are all working towards creating more efficiency, transparency and access to real estate and investments. The market that Patch of Land is serving is fragmented, locally delivered, and highly manual — it is ripe for disruption. Banks are exiting the space due to capital and liquidity constraints and hard money lenders are limited by a single source of capital and local footprint. Unlike these offline incumbents, Patch of Land has a national footprint, and uses proprietary software to quickly and reliably make first lien position loans, pre-fund those loans, and then crowdfund the financing from thousands of investors (both individuals and institutions) on a fractional or whole loan basis.

Who regulates P2RE? And what are the challenges there?

P2RE and the real estate crowdfunding sector is regulated by the SEC. Patch of Land operates under Title II, Regulation D, Rule 506(c) whereby we can only accept investments from accredited investors, as defined by the SEC. This is a strict regulation that requires thorough diligence and vetting of the accredited status of the investor. The biggest challenge we face is that we have many retail investors who want to invest with us and we cannot accommodate them.

How are the ripples in the capital markets affected or will affect business?

Capital markets volatility has not had an adverse effect on our business. Our capital sources are very diversified and are not dependent on large capital market players. Over 90 percent of our loan volume has been, and continues to be, funded by crowd capital. We have on-boarded multiple institutions of various sizes that buy loans on a fractional basis, in addition to the whole-loan forward flow agreements in place.

How is crowdfunding for real estate different from marketplace lending specifically?

Crowdfunding for real estate, specifically when referencing debt, is a subset of marketplace lending. Patch of Land is a ‘real estate marketplace lender’ because we focus specifically and exclusively on debt and do not offer any equity projects for funding. Equity deals are crowdfunding deals, not marketplace lending deals. Therefore, a real estate marketplace lender that transacts with individual investors can be considered a crowdfunding platform, and a crowdfunding platform that does not transact in debt is not a marketplace lender. Two other elements that differentiate crowdfunding from marketplace lending are: 1) prefunding, where the platform fully funds the loans upfront and therefore is not engaging in crowdfunding that usually involves raising capital first, before disbursing it to the sponsor/borrower; 2) marketplace lending includes institutional and individual investors who participate in loan purchases, whereas a crowdfunding model is focused exclusively on individual investors.

How is crowdfunding poised to change real estate investing?

Traditional real estate (debt or equity) can be highly time consuming. We offer an alternative to have real estate debt as part of a portfolio, bringing both new and experienced investors all the data they need to make a decision. Most would never have the time to aggregate this much data on their own, through traditional methods. Crowdfunding allows capital to flow more easily to across the nation, rather than locally, to places and projects that might have been shut out or simply left behind because they were too difficult to assess, evaluate and understand, or were the purview only of local investors and gatekeepers “in the know”. Crowdfunding puts investors in the driver’s seat, giving them the power to pick and choose investments that meet their personal risk/return needs. It allows for investment strategies that are both more “bespoke,” and yet more diversified -both in the way of product type and geographies, all through fractional investments across a technology enabled, online platform. Investors not only have broader choices of where to invest, but they can do it from their mobile phones in seconds.

New Funder Doing 12-Month Deals With Weekly Payments (Guess Who)

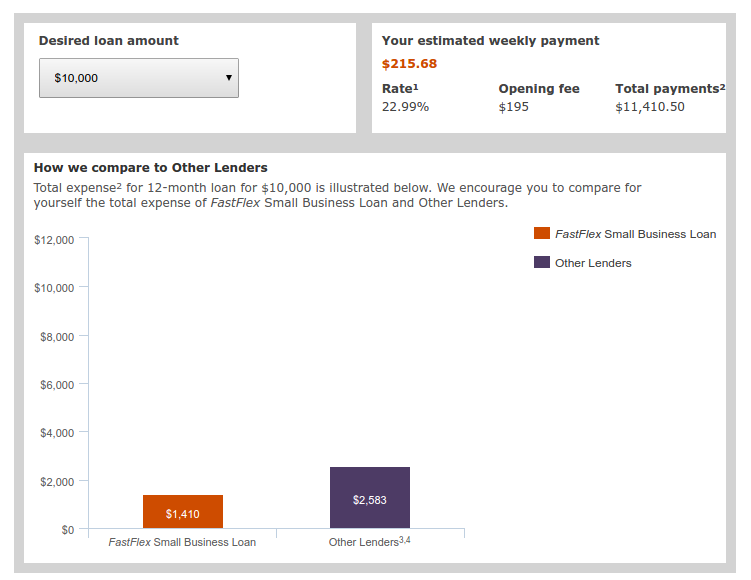

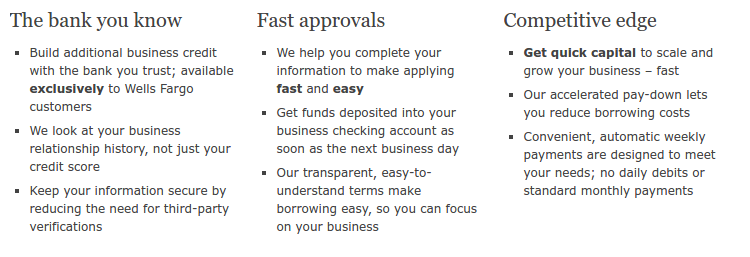

June 3, 2016 Merchants doing at least $4,100 a month in gross deposits are eligible for funding on a 12-month term with weekly ACH debit payments, a new funder revealed. Interest rates start as low as 13.99% but the max funding size is only $35,000. Underwriting decisions can be made instantly online with funds available the next day. “We consider your existing business checking history — not just your credit score,” they advertise.

Merchants doing at least $4,100 a month in gross deposits are eligible for funding on a 12-month term with weekly ACH debit payments, a new funder revealed. Interest rates start as low as 13.99% but the max funding size is only $35,000. Underwriting decisions can be made instantly online with funds available the next day. “We consider your existing business checking history — not just your credit score,” they advertise.

The name of the funder? Wells Fargo Bank.

The caveat is that applicants must have banked with Wells Fargo for at least 1 year to be eligible. The upside is that little documentation is required to apply outside of the application. The loan is unsecured and the closing fee is only $195. Dubbed FastFlex, the product is clearly meant to compete against online business lenders because well, they mention CAN Capital, OnDeck, and Kabbage in the footnotes on their loan calculator page.

Using their loan calculator, Wells Fargo estimated a 10k loan on a 1.14 over twelve months with weekly ACH payments.

Wells Fargo’s marketing message sounds awfully familiar:

Next day funding, not just your credit score, weekly payments…

Wells Fargo is not alone in their attempts to attack online lenders. Discover Bank for example, is targeting Lending Club directly. By going after the same borrower profile and offering better terms, Discover hopes to cut into Lending Club’s newfound market share.

Unsurprisingly, it is the non-bank prime lenders that will feel the growing bank threat the most. Companies offering small business loans or merchant cash advances to small businesses with damaged credit or complex situations are unlikely to find their target customer pool become bankable any time soon.

Merchant Cash Advance Accounting Q&A

May 25, 2016

As a successful and knowledgeable Merchant Cash Advance accountant I often receive questions from MCA business owners and syndicators. In the last tax season, my accounting firm recognized that many of the questions we receive are distinctly similar. In the following article I address the most common questions my accounting office receives.

Question #1: When I am accounting for my Merchant Cash Advance company isn’t a cash advance accounted for in the same way as a loan? It looks the same on a spreadsheet so isn’t the interest calculated in the same way as a normal loan?

Yoel Wagschal CPA: No. Merchant Cash Advance companies do not have interest. If you have interest then what you have is a loan business, not a Merchant Cash Advance business. Loans use an entirely different method of accounting. If you are still accounting for your Merchant Cash Advances as loans with interest then you will have regulatory issues. If you tell an IRS agent that you are not a loan company but they see your books are exactly like a loan company, how do you think that will end for you? Loans and interest are in a different world. You are the last person who wants to combine those two worlds. You need to see how they do their books at an accounts receivable factoring company and model yourself after them. They do it the way my accounting firm presents it.

Question #2: Your article mentions two ways in which Merchant Cash Advance Companies can account for transactions (cash basis and accrual). Are those the only two ways in which my accounting can be processed?

Yoel Wagschal CPA: I guarantee you would have a big argument if you brought 100 accountants together and asked them all this question: How do I recognize revenue in an accrual basis (from a GAAP standpoint) if I am allowed to take the entire income this year? You would have all kinds of voices and differences of opinions because there is no guidance for this industry. I have done the research and structured an accounting methodology. I’ve spoken with the biggest firms and dealt with the biggest names in this industry. I do have a passion for MCAs. When it comes to a tax standpoint, if you file a cash basis and you want to minimize your exposure, there is really only one way to do it. Those two ways (cash and accrual) can be kept so that they are converted from one to the other at the end of the year. Hence, if you want to prorate the income portion of your receivable (cash basis) I would still keep the books on accrual then convert it at the end of the year. You could do this with a single journal entry because it simplifies the bookkeeping process. You end up with an accrual basis financial statement and a cash basis tax return.

Question #3: I keep being told that my tax liability is based on the difference between what I spend (including funding merchants) and what I receive. For example, if we fund 100K and collect 140K in 140 days how should we keep our books? Right now we don’t recognize any income until we get back the initial funding, even if we renew the merchant over and over. Please elaborate on how revenue should be accounted for. I want to minimize my tax liability but I also want to be sure that this is the correct way to go about it.

Yoel Wagschal CPA: I have a very simple quiz:

YWCPA: Do you trust your accountant?

MCA: Yes. Yes, I do.

YWCPA: You should not. Even if you were my own client I would tell you the same thing. Why do you trust your accountant?

MCA: Because they are a professional. This is what they went to school for. This is what they do for a living.

YWCPA: Do you consider yourself a smart person?

MCA: Yes, I do.

YWCPA: Is it possible that you are smarter than your accountant? Is it possible that they simply learned a different trade than you?

MCA: Yes, that is possible.

YWCPA: Ok, then you should use your own IQ to see if what your accountant says makes sense. If your accountant tells you something that doesn’t make sense about your own business, and you believe your accountant because this is their job then you are not using your high IQ. This is especially true if you have strong negative feeling towards what you are being told. I am not telling you to jump to conclusions. I am saying you should ask questions. Think about this for as long as it takes. Your accounting should be clear and understandable to you.

I am a college professor. When I teach the principals of accounting I always start with debits and credits. I start here because students must know this concept through and through in order to be good accountants. It is the basis of all accounting. New students struggle with the logic behind this principle and I always respond that there are two options: The first option is simply to trust me. They can memorize the information and never know what it means. The second option is to completely understand. This is the option that both my students and Merchant Cash Advance business owners must choose. You, as the business owner, must understand where your own numbers come from. You must understand the foundation of your own accounting. You are entitled and responsible to understand it because of what you must sign on your company’s tax returns.

YWCPA: Do you know what you are signing on the tax return?

MCA: Do I know…?

YWCPA: Do you know what the fine print says directly above where you sign? It says:“Under penalty of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge and belief they are true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.” That is what you sign. Now, do you know what the preparer has to sign?

MCA: The same thing…?

YWCPA: The preparer signs an acknowledgement that they got paid! What I am saying is that you, the business owner, is ultimately responsible for the numbers that are on your tax return. It is you, not the preparer, who certifies that the numbers are legitimate. Of course, accountants are bound by Circular 230 and code of ethics but the level of responsibility is much higher proportionately to the tax payer than to the tax preparer.

Recognizing income only when a deal pays off is clearly, in my humble opinion, “Fraud and Tax Evasion”. I would not sign off on such a tax return. It goes even further that a lot of people who are saying this type of stuff will add that a renewal is an extension of payment and you don’t have to recognize this until the renewal is completely paid off. In this theory you can be in business for 50 years making billions of dollars and pay zero tax. If you were an IRS agent, would you accept that position?

MCA: Mmmm… What’s your point?

YWCPA: Just answer the question. If you were the IRS agent, would it help if the taxpayer told you “my accountant said it was fine”?

MCA: NNNnno.

YWCPA: That’s my point.

Question #4: When my company advances funds to a merchant how do I account for this? Also, how do I account for my company’s income with cash basis (tax return)?

Yoel Wagschal CPA: Ok, we know that in cash basis accounting we don’t recognize revenue before it is actually received. For instance, a grocery store that lets a customer take an order on credit doesn’t recognize revenue at that point. Income is recognized when funds come in.

Now we will think about the Merchant Cash Advance industry. Let’s start with when you advance funds to a merchant. For this example you advance 100k to a merchant and the payback is 140k. The 100k you send to that merchant should not be expensed. That 100k should stay on your balance sheet. You don’t recognize any income because you haven’t collected any income yet.

At the end of the year we have collected half of the advance. It started with 100k funded and 140k to collect. Now we have collected 70k. The most rational way to decide which part of the 70k goes down on the balance sheet and which part should be recognized as income is to prorate it. You should show that half has been collected which means that half of your income should be recognized now. We show it now because you have, in fact, collected revenue.

Question #5: For cash basis (tax return) purposes, when do we realize a loss? How do you show and what do you call the write off of uncollectible merchant cash advances?

Yoel Wagschal CPA: This is a very good question. There are some weird things going on in this industry because normally in a business you don’t exchange money to make money. On a cash basis tax return you would not see a receivable on the cash basis balance sheet. Concurrently, you would not see any bad debt.

Bad debt is usually not something that you see on a cash basis tax return. However, if you really look at the IRS regulations they do understand that even in a cash basis business there are bad debt expenses. Why wouldn’t you usually see bad debt expense? It is because you never recognize any income from the money you didn’t receive. Even with a cash basis tax payment, when a taxpayer lends money to a vendor (in a ‘normal business situation’) and that vendor doesn’t pay the taxpayer back, we know the taxpayer is entitled to take a bad debt expense.

In the Merchant Cash Advance situation, where we exchange money to make money, what could be more of a ‘normal business situation’? This is how your business works so if a merchant does not pay you back then you are entitled to a bad debt expense (of course, the actual realizable cash loss). This bad debt expense gets realized when the Merchant Cash Advance company is certain they are not going to get paid. In the rare situations where you have already written off a bad deal and the merchant does end up paying, you will need to reduce your bad debt expense for the following year or you can add it to your income for the following year.

As far as labeling, I believe the IRS wouldn’t care what you call it. I understand why you want to label it differently. The truth is that this comes only out of the fear that an amateur might look at it. A real trained knowledgeable professional will understand it. Bottom line is, it is perfect (although not normal) for a cash basis taxpayer to have a bad debt expense. But, you can see nothing here is the norm. So do we care for the amateur or for the expert?

Question #6: (This is for “syndicators” which we define here as entities who provide funds to MCA companies before those funds are sent to merchants). Should I do my books whenever I get a payment, week to week, or in one lump sum? From a GAAP or accounting perspective do we use immediate revenue recognition or the deferred method?

Yoel Wagschal CPA: If you want to simplify your bookkeeping I suggest after the fact accounting. Just be sure to maintain absolute consistency. At the end of the year your accountant should be able to take your information, adjust it to a proper trial balance, and create your year end reports. However, if you do not maintain the highest degree of accuracy and consistency then your accounting work will be much more time consuming and potentially flawed.

In my office we have all different types of clients. We have clients who want their books maintained on a live basis. This means we are responsible for taking the information off their MCA platforms and processing it in the accounting system.

We also have clients who want weekly reports. This is a more tempered measurement of the MCA activity. It paints the MCA picture in broader strokes while still maintaining absolute control where tax liability is concerned.

Finally we have clients who only want monthly or yearly reports. This almost completely separates the deal-to-deal MCA activity from the accounting activity. It leaves my accounting firm with the responsibility of tax liability and accounting while the MCA company does their own MCA deal tracking. Whichever approach works best for the individual companies is what you should choose.

In all of these cases there is one fundamental accounting rule and that is 100% consistency. I teach all of my clients to be very disciplined. We recommend having one bank account that is strictly used for funding and receiving money and a completely separate account for operations. For the larger clients we recommend they fund from one account and receive in another account. There is no problem shifting money between these accounts because when an accountant looks at your books it is very easy to follow your transactions.

After you have separated the accounts we can do the actual accounting work for you. However, as we are about to explain the basic journal entries for MCA accounting we caution you to remember this ‘Breaking Bad’ example. In the TV Show Breaking Bad the show’s star (Walter White) explains why he is irreplaceable. Someone else cannot simply step in and recreate his product. His argument is that he is a chemist with multiple advanced degrees as well as years of experience and research. He cannot simply impart all of the knowledge he has to someone in a matter of days. No one can match his intellect simply by watching his actions. His explanation is that a less experienced person would not be able to know if something was off. How would a less experienced person know if one of the ingredients was the wrong type? How would they know if the temperature was slightly off or the cooling phase took too long?

The same practical concept must be applied here, when you are doing the accounting for your MCA transactions. If there was an error in the journal entries, if a procedure was misunderstood and then applied over and over again, if a large transaction was classified incorrectly – how would you know? Only a highly skilled accountant with knowledge of the MCA industry will be able to look over your work and make sure that all of the procedures have been followed correctly. We are about to provide the most basic journal entries for MCA accounting. However we insist you use caution in implementing these entries. We stress that you should consult with a trained accountant who can understand the procedures and recognize mistakes.

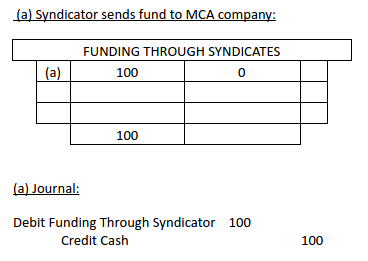

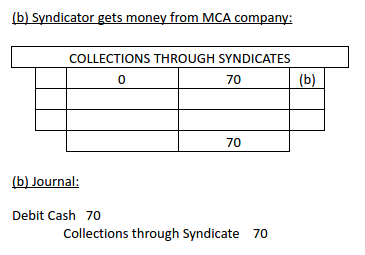

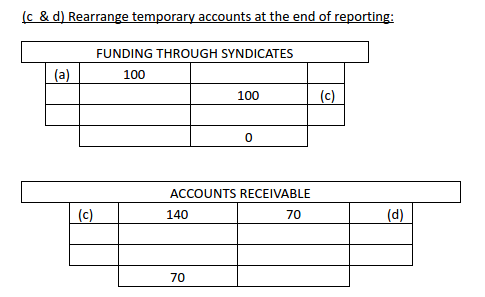

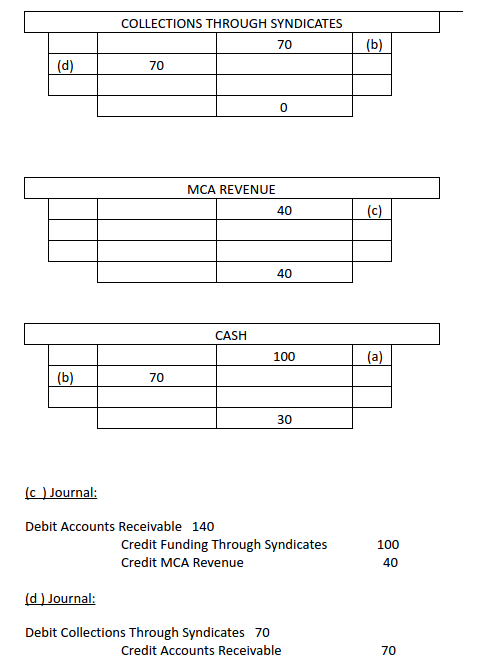

First, we start by looking at an entity who sends funds to an MCA company. As this is where the money trail starts, this is where we will start as well. When a syndicator sends funds to an MCA company they should set up a temporary ledger account. We usually call this “funded thru syndicates”. Every time they send money to the MCA company this entry will show a credit to cash and a debit to this temp account. It won’t have any meaning now but it will have a lot of meaning at the end of the year when they need to produce their financial statements. When this syndicator receives back their money they should debit cash and credit a different account. We usually call this different account ‘collections through syndicates’.

Now, the number of this type of transaction is going to depend entirely on how many deals the syndicator gets involved with and how often they receive cash back from the MCA company. Let’s say there are an accumulation of small transactions that happen over the year. Their outcome is going to be that their ‘funding through syndicate’ account is going to have a debit balance. For the sake of this example, we will make that debit balance 100k. Their ‘collections thru syndicate’ account is going to have a collective credit balance. For this example we will say the credit balance is 70k. As we said, these transactions will not have much meaning when you are processing them individually, but now they will show the bigger picture to your accountant (and hopefully to you!).

The ‘funded through syndicate’ account is at 100k because the syndicator provided the MCA company with 100k (which then went to merchants). Of course, they are not only getting 100k back. In this business the syndicators must make money on the funds they provide. For the sake of this example, the syndicator will look to get back 140k. Now you see that balance outstanding is 70k.

The MCA receivable has a debit balance of 70k, which is what they owe and their revenue is 40k. That’s the difference between the 140k and the 100k.

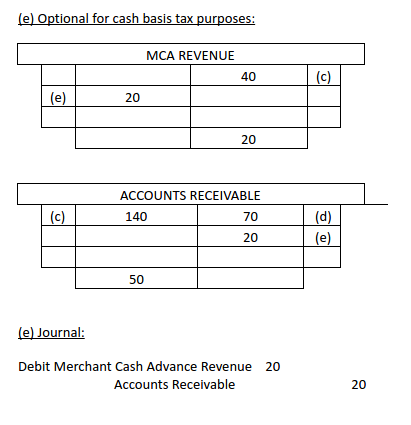

Now the temp accounts are down to zero. The next step looks at the 70k receivable. We know that 20k of it is uncollected revenue. Based on what we have before, which is used for cash basis purposes, I will add another journal entry crediting merchant cash receivable 20k. This will bring down my receivable to 50k which represents the principal portion of the 100k. This shows the syndicator gave the MCA company 100k and half of it is collected. Now we debit MCA revenue and that brings down the syndicator’s revenue from 40k to 20k for cash basis.

As far as GAAP is concerned we don’t have special guidance for this industry. The industry is very unique. We do have the principal of industry practices constraint. I have been very involved in this industry for years. I had a lot of talks with dozens of people all over the country. Investors, funders, creditors, ISO’s, professionals, etc, basically all walks of life connected to this industry. I do feel and believe that the way everyone wants and expects to see the reporting is the way I explained it. As far as MCA companies are concerned they do recognize revenue when your performance obligation has been completed; that is funding. Everything the funder does in the future is collecting their money. There is no performance that this merchant wants from the funder. As a matter of fact the merchant (customer) would be very happy if the funder ceases his activity which is strictly collections. In all other cases where we see revenue being deferred the company still has an obligation to perform. For example, prepaid phone service or insurance both provide services after the bill has been paid. Regarding uncertainty, I feel that this is no different than uncollected receivables. This is why we have a bad debt provision. The bad debt is based on historical performance of each one’s experience. As a side note, I do see a pretty consistent ratio across the line. Uncertainty leads you to the subject of derivatives. Derivatives are uncertain and unknown. Everything is underlined by a future event in the market value of a later date. This is different, as I explained. For instance, a grocery store’s AR is not certain in regards to how much they are going to collect. That is why we always work with fair estimates.

Question #7: How does this journal entry affect my tax returns? Won’t the IRS want it explained? Do they need to see it on each merchant cash advance or all in one entry?

Yoel Wagschal CPA: The IRS is not in the habit of asking to see your internal accounting unless they are performing an audit. They want to see the final result which is your tax return. This is the final report you provide to them. If you are audited then you have to substantiate your numbers and they ask for your ledger. If this happens they will see one journal entry (the one we just discussed) and they will ask how you got to those numbers. Here you will need to provide all the necessary backup, which you will undoubtedly have in your excel sheets, platforms, and correspondence. My accounting firm keeps a detailed record of all financial information we receive. When we do the final journal entry we keep and file all of the source documents that were used to calculate those numbers. We suggest you do the same not simply because the IRS may ask for them but because your investors may ask, your partners may ask, or you may need to present this information in order to diversify your business portfolio. The most important reason to have accurate and reliable financial information is, of course, that it will be used by the business owner – YOU!

Phone (845) 875-6030

Fax (845) 678-3574

Email: cjt@ywcpa.com

http://ywcpa.com