Less Than Perfect — New State Regulations

December 21, 2018

You could call California’s new disclosure law the “Son-in-Law Act.” It’s not what you’d hoped for—but it’ll have to do.

That’s pretty much the reaction of many in the alternative lending community to the recently enacted legislation, known as SB-1235, which Governor Jerry Brown signed into law in October. Aimed squarely at nonbank, commercial-finance companies, the law—which passed the California Legislature, 28-6 in the Senate and 72-3 in the Assembly, with bipartisan support—made the Golden State the first in the nation to adopt a consumer style, truth-in-lending act for commercial loans.

The law, which takes effect on Jan. 1, 2019, requires the providers of financial products to disclose fully the terms of small-business loans as well as other types of funding products, including equipment leasing, factoring, and merchant cash advances, or MCAs.

The financial disclosure law exempts depository institutions—such as banks and credit unions—as well as loans above $500,000. It also names the Department of Business Oversight (DBO) as the rulemaking and enforcement authority. Before a commercial financing can be concluded, the new law requires the following disclosures:

The financial disclosure law exempts depository institutions—such as banks and credit unions—as well as loans above $500,000. It also names the Department of Business Oversight (DBO) as the rulemaking and enforcement authority. Before a commercial financing can be concluded, the new law requires the following disclosures:

(1) An amount financed.

(2) The total dollar cost.

(3) The term or estimated term.

(4) The method, frequency, and amount of payments.

(5) A description of prepayment policies.

(6) The total cost of the financing expressed as an annualized rate.

The law is being hailed as a breakthrough by a broad range of interested parties in California—including nonprofits, consumer groups, and small-business organizations such as the National Federation of Independent Business. “SB-1235 takes our membership in the direction towards fairness, transparency, and predictability when making financial decisions,” says John Kabateck, state director for NFIB, which represents some 20,000 privately held California businesses.

“What our members want,” Kabateck adds, “is to create jobs, support their communities, and pursue entrepreneurial dreams without getting mired in a loan or financial structure they know nothing about.”

Backers of the law, reports Bloomberg Law, also included such financial technology companies as consumer lenders Funding Circle, LendingClub, Prosper, and SoFi.

But a significant segment of the nonbank commercial lending community has reservations about the California law, particularly the requirement that financings be expressed by an annualized interest rate (which is different from an annual percentage rate, or APR). “Taking consumer disclosure and annualized metrics and plopping them on top of commercial lending products is bad public policy,” argues P.J. Hoffman, director of regulatory affairs at the Electronic Transactions Association.

The ETA is a Washington, D.C.-based trade group representing nearly 500 payments technology companies worldwide, including such recognizable names as American Express, Visa and MasterCard, PayPal and Capital One. “If you took out the annualized rate,” says ETA’s Hoffman, “we think the bill could have been a real victory for transparency.”

The ETA is a Washington, D.C.-based trade group representing nearly 500 payments technology companies worldwide, including such recognizable names as American Express, Visa and MasterCard, PayPal and Capital One. “If you took out the annualized rate,” says ETA’s Hoffman, “we think the bill could have been a real victory for transparency.”

California’s legislation is taking place against a backdrop of a balkanized and fragmented regulatory system governing alternative commercial lenders and the fintech industry. This was recognized recently by the U.S. Treasury Department in a recently issued report entitled, “A Financial System That Creates Economic Opportunities: Nonbank Financials, Fintech, and Innovation.” In a key recommendation, the Treasury report called on the states to harmonize their regulatory systems.

As laudable as California’s effort to ensure greater transparency in commercial lending might be, it’s adding to the patchwork quilt of regulation at the state level, says Cornelius Hurley, a Boston University law professor and executive director of the Online Lending Policy Institute. “Now it’s every regulator for himself or herself,” he says.

Hurley is collaborating with Jason Oxman, executive director of ETA, Oklahoma University law professor Christopher Odinet, and others from the online-lending industry, the legal profession, and academia to form a task force to monitor the progress of regulatory harmonization.

For now, though, all eyes are on California to see what finally emerges as that state’s new disclosure law undergoes a rulemaking process at the DBO. Hoffman and others from industry contend that short-term, commercial financings are a completely different animal from consumer loans and are hoping the DBO won’t squeeze both into the same box.

Steve Denis, executive director of the Small Business Finance Association, which represents such alternative financial firms as Rapid Advance, Strategic Funding and Fora Financial, is not a big fan of SB-1235 but gives kudos to California solons—especially state Sen. Steve Glazer, a Democrat representing the Bay Area who sponsored the disclosure bill—for listening to all sides in the controversy. “Now, the DBO will have a comment period and our industry will be able to weigh in,” he notes.

While an annualized rate is a good measuring tool for longer-term, fixed-rate borrowings such as mortgages, credit cards and auto loans, many in the small-business financing community say, it’s not a great fit for commercial products. Rather than being used for purchasing consumer goods, travel and entertainment, the major function of business loans are to generate revenue.

A September, 2017, study of 750 small-business owners by Edelman Intelligence, which was commissioned by several trade groups including ETA and SBFA, found that the top three reasons businesses sought out loans were “location expansion” (50%), “managing cash flow” (45%) and “equipment purchases” (43%).

The proper metric to be employed for such expenditures, Hoffman says, should be the “total cost of capital.” In a broadsheet, Hoffman’s trade group makes this comparison between the total cost of capital of two loans, both for $10,000.

Loan A for $10,000 is modeled on a typical consumer borrowing. It’s a five-year note carrying an annual percentage rate of 19%—about the same interest rate as many credit cards—with a fixed monthly payment of $259.41. At the end of five years, the debtor will have repaid the $10,000 loan plus $5,564 in borrowing costs. The latter figure is the total cost of capital.

Compare that with Loan B. Also for $10,000, it’s a six month loan paid down in monthly payments of $1,915.67. The APR is 59%, slightly more than three times the APR of Loan A. Yet the total cost of capital is $1,500, a total cost of capital which is $4,064.33 less than that of Loan A.

Meanwhile, Hoffman notes, the business opting for Loan B is putting the money to work. He proposes the example of an Irish pub in San Francisco where the owner is expecting outsized demand over the upcoming St. Patrick’s Day. In the run-up to the bibulous, March 17 holiday, the pub’s owner contracts for a $10,000 merchant cash advance, agreeing to a $1,000 fee.

Once secured, the money is spent stocking up on Guinness, Harp and Jameson’s Irish whiskey, among other potent potables. To handle the anticipated crush, the proprietor might also hire temporary bartenders.

When St. Patrick’s Day finally rolls around—thanks to the bulked-up inventory and extra help—the barkeep rakes in $100,000 and, soon afterwards, forwards the funding provider a grand total of $11,000 in receivables. The example of the pub-owner’s ability to parlay a short-term financing into a big payday illustrates that “commercial products—where the borrower is looking for a return on investment—are significantly different from consumer loans,” Hoffman says.

SBFA’s Denis observes that financial products like merchant cash advances are structured so that the provider of capital receives a percentage of the business’s daily or weekly receivables. Not only does that not lend itself easily to an annualized rate but, if the food truck, beautician, or apothecary has a bad day at the office, so does the funding provider. “It’s almost like the funding provider is taking a ride” with the customer, says Denis.

SBFA’s Denis observes that financial products like merchant cash advances are structured so that the provider of capital receives a percentage of the business’s daily or weekly receivables. Not only does that not lend itself easily to an annualized rate but, if the food truck, beautician, or apothecary has a bad day at the office, so does the funding provider. “It’s almost like the funding provider is taking a ride” with the customer, says Denis.

Consider a cash advance made to a restaurant, for instance, that needs to remodel in order to retain customers. “An MCA is the purchase of future receivables,” Denis remarks, “and if the restaurant goes out of business— and there are no receivables—you’re out of luck.”

Still, the alternative commercial-lending industry is not speaking with one voice. The Innovative Lending Platform Association—which counts commercial lenders OnDeck, Kabbage and Lendio, among other leading fintech lenders, as members—initially opposed the bill, but then turned “neutral,” reports Scott Stewart, chief executive of ILPA. “We felt there were some problems with the language but are in favor of disclosure,” Stewart says.

The organization would like to see DBO’s final rules resemble the company’s model disclosure initiative, a “capital comparison tool” known as “SMART Box.” SMART is an acronym for Straightforward Metrics Around Rate and Total Cost—which is explained in detail on the organization’s website, onlinelending.org.

But Kabbage, a member of ILPA, appears to have gone its own way. Sam Taussig, head of global policy at Atlanta-based financial technology company Kabbage told AltFinanceDaily that the company “is happy with the result (of the California law) and is working with DBO on defining the specific terms.”

Others like National Funding, a San Diego-based alternative lender and the sixth-largest alternative-funding provider to small businesses in the U.S., sat out the legislative battle in Sacramento. David Gilbert, founder and president of the company, which boasted $94.5 million in revenues in 2017, says he had no real objection to the legislation. Like everyone else, he is waiting to see what DBO’s rules look like.

“It’s always good to give more rather than less information,” he told AltFinanceDaily in a telephone interview. “We still don’t know all the details or the format that (DBO officials) want. All we can do is wait. But it doesn’t change this business. After the car business was required to disclose the full cost of motor vehicles,” Gilbert adds, “people still bought cars. There’s nothing here that will hinder us.”

With its panoply of disclosure requirements on business lenders and other providers of financial services, California has broken new legal ground, notes Odinet, the OU law professor, who’s an expert on alternative lending and financial technology. “Not many states or the federal government have gotten involved in the area of small business credit,” he says. “In the past, truth-in-lending laws addressing predatory activities were aimed primarily at consumers.”

The financial-disclosure legislation grew out of a confluence of events: Allegations in the press and from consumer activists of predatory lending, increasing contraction both in the ranks of independent and community banks as well as their growing reluctance to make small-business loans of less than $250,000, and the rise of alternative lenders doing business on the Internet.

In addition, there emerged a consensus that many small businesses have more in common with consumers than with Corporate America. Rather than being managed by savvy and sophisticated entrepreneurs in Silicon Valley with a Stanford pedigree, many small businesses consist of “a man or a woman working out of their van, at a Starbucks, or behind a little desk in their kitchen,” law professor Odinet says. “They may know their business really well, but they’re not really in a position to understand complicated financial terms.”

The average small-business owner belonging to NFIB in California, reports Kabateck, has $350,000 in annual sales and manages from five to nine employees. For this cohort—many of whom are subject to myriad marketing efforts by Internet-based lenders offering products with wildly different terms—the added transparency should prove beneficial. “Unlike big businesses, many of them don’t have the resources to fully understand their financial standing,” Kabateck says. “The last thing they want is to get steeped in more red ink or—even worse—have the wool pulled over their eyes.”

California’s disclosure law is also shaping up as a harbinger—and perhaps even a template—for more states to adopt truth-in-lending laws for small-business borrowers. “California is the 800-lb. gorilla and it could be a model for the rest of the country,” says law professor Hurley. “Just as it has taken the lead on the control of auto emissions and combating climate change, California is taking the lead for the better on financial regulation. Other states may or may not follow.”

California’s disclosure law is also shaping up as a harbinger—and perhaps even a template—for more states to adopt truth-in-lending laws for small-business borrowers. “California is the 800-lb. gorilla and it could be a model for the rest of the country,” says law professor Hurley. “Just as it has taken the lead on the control of auto emissions and combating climate change, California is taking the lead for the better on financial regulation. Other states may or may not follow.”

Reflecting the Golden State’s influence, a truth-in-lending bill with similarities to California’s, known as SB-2262, recently cleared the state senate in the New Jersey Legislature and is on its way to the lower chamber. SBFA’s Denis says that the states of New York and Illinois are also considering versions of a commercial truth-in-lending act.

But the fact that these disclosure laws are emanating out of Democratic states like California, New Jersey, Illinois and New York has more to do with their size and the structure of the states’ Legislatures than whether they are politically liberal or conservative. “The bigger states have fulltime legislators,” Denis notes, “and they also have bigger staffs. That’s what makes them the breeding ground for these things.”

Buried in Appendix B of Treasury’s report on nonbank financials, fintechs and innovation is the recommendation that, to build a 21st century economy, the 50 states should harmonize and modernize their regulatory systems within three years. If the states fail to act, Treasury’s report calls on Congress to take action.

The triumvirate of Hurley, Oxman and Odinet report, meanwhile, that they are forming a task force and, with the tentative blessing of Treasury officials, are volunteering to monitor the states’ progress. “I think we have an opportunity as independent representatives to help state regulators and legislators understand what they can do to promote innovation in financial services,” ETA’s Oxman asserts.

The ETA is a lobbying organization, Oxman acknowledges, but he sees his role—and the task force’s role—as one of reporting and education. He expects to be meeting soon with representatives of the Conference of State Bank Supervisors (CSBS), the Washington, D.C.-based organization representing regulators of state chartered banks. It is also the No. 1 regulator of nonbanks and fintechs. “They are the voice of state financial regulators,” Oxman says, “and they would be an important partner in anything we do.”

The ETA is a lobbying organization, Oxman acknowledges, but he sees his role—and the task force’s role—as one of reporting and education. He expects to be meeting soon with representatives of the Conference of State Bank Supervisors (CSBS), the Washington, D.C.-based organization representing regulators of state chartered banks. It is also the No. 1 regulator of nonbanks and fintechs. “They are the voice of state financial regulators,” Oxman says, “and they would be an important partner in anything we do.”

Margaret Liu, general counsel at CSBS, had high praise for Treasury’s hard work and seriousness of purpose in compiling its 200-plus page report and lauded the quality of its research and analysis. But Liu noted that the conference was already deeply engaged in a program of its own, which predates Treasury’s report.

Known as “Vision 2020,” the program’s goals, as articulated by Texas Banking Commissioner Charles Cooper, are for state banking regulators to “transform the licensing process, harmonize supervision, engage fintech companies, assist state banking departments, make it easier for banks to provide services to non-banks, and make supervision more efficient for third parties.”

While CSBS has signaled its willingness to cooperate with Treasury, the conference nonetheless remains hostile to the agency’s recommendation, also found in the fintech report, that the Office of the Comptroller of the Currency issue a “special purpose national bank charter” for fintechs. So vehemently opposed are state bank regulators to the idea that in late October the conference joined the New York State Banking Department in re-filing a suit in federal court to enjoin the OCC, which is a division of Treasury, from issuing such a charter.

Among other things, CSBS’s lawsuit charges that “Congress has not granted the OCC authority to award bank charters to nonbanks.”

Previously, a similar lawsuit was tossed out of court because, a judge ruled, the case was not yet “ripe.” Since no special purpose charters had actually been issued, the judge ruled, the legal action was deemed premature. That the conference would again file suit when no fintech has yet applied for a special purpose national bank charter— much less had one approved—is baffling to many in the legal community.

“I suspect the lawsuit won’t go anywhere” because ripeness remains a sticking point, reckons law professor Odinet. “And there’s no charter pending,” he adds, in large part because of the lawsuit. “A lot of people are signing up to go second,” he adds, “but nobody wants to go first.”

Treasury’s recommendation that states harmonize their regulatory systems overseeing fintechs in three years or face Congressional action also seems less than jolting, says Ross K. Baker, a distinguished professor of political science at Rutgers University and an expert on Congress. He told AltFinanceDaily that the language in Treasury’s document sounded aspirational but lacked any real force.

“Usually,” he says, such as a statement “would be accompanied by incentives to do something. This is a kind of a hopeful urging. But I don’t see any club behind the back,” he went on. “It seems to be a gentle nudging, which of course they (the states) are perfectly able to ignore. It’s desirable and probably good public policy that states should have a nationwide system, but it doesn’t say Congress should provide funds for states to harmonize their laws.

“When the Feds issue a mandate to the states,” Baker added, “they usually accompany it with some kind of sweetener or sanction. For example, in the first energy crisis back in 1973, Congress tied highway funds to the requirement (for states) to lower the speed limit to 55 miles per hour. But in this case, they don’t do either.”

Ingo Money QuickConnect Allows for Push-to-Card Payments

December 14, 2018

Yesterday, Ingo Money announced the launch of Ingo Money QuickConnect, a new solution that allows companies that issue payments – including loans – to disperse funds directly to a merchant’s debit card. Ingo Money has partnered with Visa Direct to facilitate these direct payments.

This is the official announcement for a product that has been in the works for over a year. OnDeck announced its partnership with Ingo Money last October, but didn’t start using it until it was ready earlier this year, according to an OnDeck spokesperson. So far, OnDeck only uses the Ingo Money QuickConnect service to provide same-day disbursements to their line of credit customers. The spokesperson said they have seen great demand among customers for receiving money instantly.

“Ingo Money QuickConnect allowed us to get to market faster than we ever believed possible and with minimal time, cost and hassle,” said Sam Verrill, OnDeck’s Director of Product Management. “The solution has thoughtfully solved for all the pain points and hurdles to deploying a new payment solution, making it quick and easy to begin delighting customers and cutting costs with digital real time disbursements.”

Chief Product Officer for Ingo Money Lisa McFarland told AltFinanceDaily that OnDeck was their first client in the lending category, and that they now have a few other lending clients, but declined to mentioned which.

“What’s exciting about Ingo Money QuickConnect is that customers can access money the minute they need it,” McFarland said. “At night, on weekends and holidays.”

The Ingo Money QuickConnect solution is also being used in other ways, including insurance companies paying claims and child support payments where the government is an intermediary. Use in payment of airlines vouchers to customers and by the IRS to people who are owed money are also being considered, according to McFarland.

“We’ve heard time and again from customers that they need to deploy a push-to-card payment solution but are intimidated by the time and effort required,” said Ingo Money CEO Drew Edwards. “Ingo Money QuickConnect removes the burden and allows a company to almost immediately begin offering real-time payments through Visa Direct, while retaining the ability to easily expand the solution later to include payments to online wallets like PayPal and Amazon or even cash out Moneygram locations.”

The Google Battle for Lending & SMB Finance Keywords Revisited

August 29, 2018When it comes to Google’s organic search for major keywords, companies like Nerdwallet and Fundera still dominate. A few players, however, have gained or lost significant ground since last year.

The Small Business Administration relinquished its place on the first page for words like “business loan” and “business line of credit” while PayPal and Credit Karma have begun to make major appearances as their activity in these markets increases.

Take a look:

| Keywords | Fundera | Fundera | PayPal | PayPal | Credit Karma | Credit Karma | Kabbage | Kabbage | OnDeck | OnDeck |

| Date | 9/14/17 | 8/29/18 | 9/14/17 | 8/29/18 | 9/14/17 | 8/29/18 | 9/14/17 | 8/29/18 | 9/14/17 | 8/29/18 |

| business loan | 1 | 1 | 2 | 3 | 4 | 5 | ||||

| merchant cash advance | 3 | 2 | 2 | 4 | ||||||

| working capital | 8 | 9 | ||||||||

| commercial loan | 3 | 1 | 5 | |||||||

| small business loans | 2 | 1 | 3 | 5 | 4 | |||||

| business line of credit | 2 | 2 | 5 | 3 | 3 | |||||

| fast business loan | 4 | 5 | 1 | 4 | ||||||

| business loan with bad credit | 7 | 5 |

| Keywords | Lending Club | Lending Club | Nerdwallet | Nerdwallet | National Funding | National Funding | Traditional Banks | Traditional Banks | SBA.gov | SBA.gov |

| Date | 9/14/17 | 8/29/18 | 9/14/17 | 8/29/18 | 9/14/17 | 8/29/18 | 9/14/17 | 8/29/18 | 9/14/17 | 8/29/18 |

| business loan | 9 | 6 | 3 | 7,8 | 5 | 4,7 | 6 | |||

| merchant cash advance | 4 | 1 | 8 | 9 | ||||||

| working capital | 4 | |||||||||

| commercial loan | 2,7 | 3,8,9,10 | ||||||||

| small business loans | 9 | 3 | 7,8 | 5 | 7 | 1 | 2 | |||

| business line of credit | 11 | 1,4 | 1 | 6,7,8,9,10 | 4,6,7,9,10 | 5 | ||||

| fast business loan | 2 | 3 | 5,6 | 8 | ||||||

| business loan with bad credit | 1,4 | 1 | 2 | 2 | 3 |

As mentioned in previous posts, this is not a scientific analysis. Keywords are measured using a wiped browser on my own computer.

The value of a Page-1 ranking too, is not as valuable as it once was, due to the heavy placement of paid ads above the search results. Ads, however, are not a factor for the keyword “merchant cash advance” since Google banned all advertising for that search term last Fall. Originally it was theorized that the ban was accidental, but ten months later it is still in place.

No such ban exists on Bing.

Read my previous analyses on the industry’s search war over the years:

September 2017 The Google Battle for Lending and SMB Finance Keywords

December 2015 Google Serves Low Blow to Merchant Cash Advance Seekers

March 2015 Google Culls Online Lenders – Pay or Else?

October 2014 Merchant Cash Advance SEO War Still Raging

August 2014 Six Signs Alternative Lending is Rigged: Do Lending Club and OnDeck have a helping hand?

October 2013 Google Penguin 2.1 takes swing at the MCA industry

August 2013 Your merchant cash advance press release may be hurting you

December 2012 Is Google your only web strategy?

July 2012 The other 93% [of leads]

April 2012 The SEO war continues

February 2012 The SEO War for Merchant Cash Advance: The first story on this topic

The Seven-Minute Loan Shakes Up Washington And The 50 States

August 19, 2018 It takes seven minutes for Kabbage to approve a small-business loan. “The reason there’s so little lag time,” says Sam Taussig, head of global policy at the Atlanta-based financial technology firm, “is that it’s all automated. Our marginal cost for loans is very low,” he explains, “because everything involving the intake of information – your name and address, know-your-customer, anti-money-laundering and anti-terrorism checks, analyzing three years of income statements, cash-flow analysis – is one-hundred-percent automated. There are no people involved unless red flags go off.”

It takes seven minutes for Kabbage to approve a small-business loan. “The reason there’s so little lag time,” says Sam Taussig, head of global policy at the Atlanta-based financial technology firm, “is that it’s all automated. Our marginal cost for loans is very low,” he explains, “because everything involving the intake of information – your name and address, know-your-customer, anti-money-laundering and anti-terrorism checks, analyzing three years of income statements, cash-flow analysis – is one-hundred-percent automated. There are no people involved unless red flags go off.”

One salient testament to Kabbage’s automation: Fully $1 billion of the $5 billion in loans that it has made to 145,000 discrete borrowers since it opened its portals in 2011 were made between 6 p.m. and 6 a.m.

Now compare that hair-trigger response time and 24-hour service for a small business loan of $1,000-$250,000 with what occurs at a typical bank. “Corporate credit underwriting requires 28 separate tasks to arrive at a decision,” William Phelan, president, and co‐founder of PayNet—a top provider of small-business credit data and analysis – testified recently to a Congressional subcommittee. “These 28 tasks involve (among other things): collecting information for the credit application, reviewing the financial information, data entry and calculations, industry analysis, evaluation of borrower capability, capacity (to repay), and valuation of collateral.”

A “time-series analysis,” the Skokie (Ill.)-based executive went on, found that it takes two-to-three weeks – and often as many as eight weeks—to complete the loan approval process. For this “single credit decision,” Phelan added, the services of three bank departments – relationship manager, credit analyst, and credit committee – are required.

The cost of such a labor-intensive operation? PayNet analysts reckoned that banks incur $4,000-$6,000 in underwriting expenses for each credit application. Phelan said, moreover, that credit underwriting typically includes a subsequent loan review, which consumes two days of effort and costs the bank an additional $1,000. “With these costs,” Phelan told lawmakers, “banks are unable to turn a profit unless the loan size exceeds $500,000.”

According to the National Bureau of Economic Research, the country’s very biggest banks — Bank of America, Citigroup, J.P. Morgan Chase, and Wells Fargo—have been the financial institutions most likely to shut down lending to small businesses. “While small business lending declined at all banks beginning in 2008,” NBER’s September, 2017 report announces, “the four largest banks” which the report dubs the ‘Top Four’—“cut back significantly relative to the rest of the banking sector.”

NBER reports further that by 2010—the “trough” of the financial crisis—the annual flow of loan originations from the Top Four stood at just 41% of its 2006 level, which compared with 66% of the pre-crisis level for all other banks. Moreover, small-business lending at the “Top Four” banks remained suppressed for several years afterward, “hovering” at roughly 50% of its pre crisis level through 2014. By contrast, such lending at the rest of the country’s banks eventually bounced back to nearly 80% of the pre-crisis level by 2014.

That pullback—by all banks—continues, says Kenneth Singleton, an economics professor at Stanford University’s Graduate School of Business. Echoing Phelan’s testimony, Singleton told AltFinanceDaily in an interview: “Given the high underwriting costs, banks just chose not to make loans under $250,000,” which are the bread-and-butter of small-business loans. In so doing, he adds, banks “have created a vacuum for fintechs.”

All of which helps explain why Kabbage and other fintechs making small business loans are maintaining a strong growth trajectory. As a Federal Reserve report issued in June notes, the five most prominent fintech lenders to small businesses—OnDeck, Kabbage, Credibly, Square Capital, and PayPal—are on track to grow by an estimated 21.5 percent annually through 2021.

Their outsized growth is just one piece—albeit a major one—of fintech’s larger tapestry. Depending on how you define “financial technology,” there are anywhere from 1,400 to 2,000 fintechs operating in the U.S., experts say. Fintech companies are now engaged in online payments, consumer lending, savings and investment vehicles, insurance, and myriad other forms of financial services.

Fintechs’ advocates—a loose confederacy that includes not only industry practitioners but also investors, analysts, academics, and sympathetic government officials—assert that the U.S. fintech industry is nonetheless being blunted from realizing its full potential. If fintechs were allowed to “do their thing,” (as they said in the sixties) this cohort argues, a supercharged industry would bring “financial inclusion” to “unbanked” and “underbanked” populations in the U.S. By “democratizing access to capital,” as Kabbage’s Taussig puts it, harnessing technology would also re-energize the country’s small businesses, which creates the majority of net new jobs in the U.S., according to the U.S. Small Business Administration.

But standing in the way of both innovation and more robust economic growth, this cohort asserts, is a breathtakingly complex—and restrictive—regulatory system that dates back to the Civil War. “I do think we’re victims of our own success in that we’ve got a pretty good financial system and a pretty good regulatory structure where most people can make payments and the vast majority of people can get credit.” says Jo Ann Barefoot, chief executive at Barefoot Innovation Group in Washington, D.C. and a former senior fellow at Harvard’s Kennedy School. But because of that “there’s been more inertia and slower adoption of new technology,” she adds. “People in the U.S. are still going to bank branches more than people in the rest of the world.”

Barefoot adds: “There are five agencies directly overseeing financial services at the Federal level and another two dozen federal agencies” providing some measure of additional, if not duplicative oversight, over financial services. “But there’s no fintech licensing at the national level,” she says. And because each state also has a bank regulator, she notes, “if you’re a fintech innovator, you have to go state by state and spend millions of dollars and take years” to comply with a spool of red tape pertaining to nonbanks.

At the federal level, the current system— which includes the Federal Reserve, Office of the Comptroller of the Currency (OCC), and the Federal Deposit Insurance Corporation (FDIC)—developed over time in a piecemeal fashion, largely through legislative responses to economic panics, shocks and emergencies. “For historical reasons,” Barefoot remarks, “we have a lot of agencies” regulating financial services.

For exhibit A, look no further than the Consumer Financial Protection Bureau created amidst the shambles of the 2008-2009 financial crisis by the 2010 Dodd-Frank Act. Built ostensibly to preserve safety and soundness, the agencies have constructed a moat around the banking system.

Karen Shaw Petrou, managing partner at Federal Financial Analytics, a Washington, D.C. consultancy, is a banking policy expert who frequently provides testimony to Congress and regulatory agencies. She wrote recently that the country’s banking sector has been protected from the kind of technological disruption that has upended a whole bevy of industries.

“The only reason Amazon and its ilk may not do to banking, brokers and insurers what they did to retailers—and are about to do to grocers and pharmacies,” she observed recently in a blog—“is the regulatory structure of each of these businesses. If and how it changes are the most critical strategic factors now facing finance.”

Cornelius Hurley, a Boston University law professor and executive director of the Online Lending Policy Institute, is especially critical of the 50-state, dual banking system. State bank regulators oversee 75 percent of the country’s banks and are the primary regulators of nonbank financial technology companies. “The U.S. is falling behind other countries that are much less balkanized,” Hurley says. “Our federal system of government has served us well in many areas in our becoming a leading civil society. It’s given us NOW (Negotiable Order of Withdrawal) accounts, money-market accounts, automatic teller machines, and interstate banking. But now it’s outlived its usefulness and has become an impediment.”

Take Kabbage, which actually avoids a lot of regulatory rigmarole by virtue of its partnership with Celtic Bank, a Utah-chartered industrial bank. The association with a regulated state bank essentially provides Kabbage with a passport to conduct business across state lines. Nonetheless, Kabbage has multiple, incessant, and confusing dealings with its bank overseers in the 50 states.

“Where the states get involved,” says Taussig, “is on brokering, solicitation, disclosure and privacy. We run into varying degrees of state legislative issues that make it hard to do business. Right now we’re plagued by what’s been happening with national technology actors on cybersecurity breaches and breach disclosures. We are required to notify customers. But some states require that we do it in as few as 36 hours, and in others it’s a couple of months. We’ve lobbied for a national breach law of four days,” he adds, which would “make it easier for everyone operating across the country.”

Then there’s the meaning of “What is a broker?’” says Taussig, who as a regulatory compliance expert at Kabbage sees his role as something of an emissary and educator to regulators and politicians, the news media, and the public. “The definitions haven’t been updated since the 1950s and now we have wildly different interpretations of brokering and solicitation,” he says. “The landscape has changed with e-commerce and each state has a different perspective of what’s kosher on the Internet.”

Washington State is a good example. It’s one of a handful of jurisdictions in which regulators confine nonbank fintechs to making consumer loans. In a kabuki dance, fintech companies apply for a consumer-lending license and then ask for a special dispensation to do small-business lending.

And let’s not forget New Mexico, Nevada and Vermont where a physical “brick-and-mortar” presence is required for a lender to do business. Digital companies, Taussig says, would have to seek a waiver from regulators in those states. “Many companies spend a lot of money on billable hours for local lawyers to comply with policies and procedures,” Taussig reports, “and it doesn’t serve to protect customers. It’s really just revenue extraction.”

All such restraints put fintechs at a disadvantage to traditional financial institutions, which by virtue of a bank charter, enjoy laws guaranteeing parity between state-chartered and federally chartered national banks. The banks are therefore able to traverse state lines seamlessly to take deposits, make loans, and engage in other lines of business. In addition, fintechs’ cost of funds is far higher than banks, which pay depositors a meager interest rate. And banks have access to the Fed discount window, while their depositors’ savings and checking accounts are insured up to $200,000.

The result is a higher cost of funds for fintechs, which principally depend on venture capital, private equity, securitization and debt financing as well as retained earnings. And that translates into steeper charges for small business borrowers. A fintech customer can easily pay an interest rate on a loan or line of credit that’s three to four times higher than, say, a bank loan backed by the U.S. Small Business Administration.

Kabbage, for example, reports that its average loan of roughly $10,000 typically carries an interest rate of 35%-36%. It’s credits are, of course, riskier than the banks’. The company does not report figures on loans denied, Taussig told AltFinanceDaily, but Stanford’s Singleton says that the fintech industry’s denial rate is roughly 50 percent for small business loans. “Fintechs have higher costs of capital and they’re also facing moderate default rates,” notes Singleton. “They’re not enormous, but fintechs are dealing with a different segment. Small businesses have much more variability in cash flows, so lending could be riskier than larger, established companies.”

Even so, venture capitalists continue to pour money into fintech start-ups. “I’ve gone to several conferences,” Singleton says, “and everywhere I turn I’m meeting people from a new fintech company. One of the striking things about this space,” he adds, “is that there are lot of aspiring start-ups attacking very specific, very narrow issues. Not all will survive, but someone will probably acquire them.”

Even so, venture capitalists continue to pour money into fintech start-ups. “I’ve gone to several conferences,” Singleton says, “and everywhere I turn I’m meeting people from a new fintech company. One of the striking things about this space,” he adds, “is that there are lot of aspiring start-ups attacking very specific, very narrow issues. Not all will survive, but someone will probably acquire them.”

Contrast that to the world of banking. Many banks are wholeheartedly embracing technology by collaborating with fintechs, acquiring start-ups with promising technology, or developing in-house solutions. Among the most impressive are super-regionals Fifth Third Bank ($142.2 billion), Regions Financial Corp. ($123.5 billion), and BBVA Compass ($69.6 billion), notes Miami-based bank consultant Charles Wendel. But many banks are content to cater to familiar customers and remain complacent. One result is that there’s been a steady diminution in the number of U.S. banks.

Over the past ten years, fully one-third of the country’s banks were swallowed whole in an acquisition, disappeared in a merger, failed, or otherwise closed their doors. There were 5,670 federally insured banks at the end of 2017, according to the Federal Deposit Insurance Corp., a 2,863-bank, 33.5% decrease from the 8,533 commercial banks operating in the U.S. in 2007.

It does appear that, to paraphrase an old expression, many banks “are going out of style.” In recent years there have been more banking industry deaths than births. Sixty-three banks have failed since 2013 through June while only 14 de novo banks have been launched. In Texas, which is known for having the most banks of any state in the country, only one newly minted bank debuted since 2009. (The Bank of Austin is the new kid on the Texas block, opening in a city known as a hotbed of technology with its “Silicon Hills.”)

One reason there’s so little enthusiasm among venture capitalists and other financial backers for investing in de novo banks is that regulators are known to be austere. “If you’re a company in the U.S.,” says Matt Burton, a founder of data analytics firm Orchard Platform Markets (which was recently acquired by Kabbage), “and you tell regulators that you want to grow by 100 percent a year – which is the scale you must grow at to get venture-capital funding – regulators will freak out. Bank regulators are very, very strict. That’s why you never hear about new banks achieving any sort of scale.”

But while bank regulators “are moving sluggishly compared to the rest of the world” in adapting to the fintech revolution, says Singleton, there are numerous signs that the status quo may be in for a surprising jolt. The Treasury Department is about to issue (possibly by the time this story is published) a major report recommending an across-the-board overhaul in the regulatory stance toward all nonbank financials, including fintechs. According to a report in The American Banker, Craig Phillips, counselor to Treasury Secretary Steven Mnuchin, told a trade group that the report would address regulatory shortcomings and especially “regulatory asymmetries” between fintech firms and regulated financial institutions.

Christopher Cole, senior regulatory counsel at the Independent Community Bankers Association—a Washington, D.C. trade association representing the country’s Main Street bankers—told AltFinanceDaily that, among other things, the Treasury report would likely recommend “regulatory sandboxes.” (A regulatory sandbox allows businesses to experiment with innovative products, services, and business models in the marketplace, usually for a specified period of time.)

That’s an idea that fintech proponents have been drumming enthusiastically since it was pioneered in the U.K. a few years ago, and it’s something that the independent bankers’ lobby, whose member banks are among the most threatened by fintech small-business lenders, says it too can support. Treasury’s Phillips “has said in the past that he’d like to see a level playing field,” the ICBA’s Cole says. “So if (regulators) are going to allow a sandbox, any company could be involved, including a community bank. We agree with him, of course, because we’d like to take advantage of that.”

In March, 2018, Arizona became the first state to establish a regulatory sandbox when the governor signed a law directing that state’s attorney general (and not the state’s banking regulator) to oversee the program. The agency will begin taking applications in August with approval in 90 days, says Paul Watkins, civil litigation chief in the AG’s office. Watkins told AltFinanceDaily that he’s been most surprised so far by “the degree of enthusiasm” from overseas companies. With the advent of the sandbox, he adds, “Landlocked Arizona has become a port state.”

The OCC, which is part of the Treasury Department, may also revive its plan to issue a national bank charter to fintechs, sources say (EDITOR’S NOTE: This had not yet been implemented before this story went to print. The OCC is now accepting such applications) – a hugely controversial proposal that was put on ice last year (and some thought left for dead) when former Commissioner Thomas J. Curry’s tenure ended last spring. At his departure, the fintech bank charter faced a lawsuit filed by both the New York State Banking Department and the Conference of State Bank Supervisors. (Since then, the lawsuit was tossed out by the courts on the ground that the case was not “ripe” – that is, it was too soon for plaintiffs to show injury).

The OCC, which is part of the Treasury Department, may also revive its plan to issue a national bank charter to fintechs, sources say (EDITOR’S NOTE: This had not yet been implemented before this story went to print. The OCC is now accepting such applications) – a hugely controversial proposal that was put on ice last year (and some thought left for dead) when former Commissioner Thomas J. Curry’s tenure ended last spring. At his departure, the fintech bank charter faced a lawsuit filed by both the New York State Banking Department and the Conference of State Bank Supervisors. (Since then, the lawsuit was tossed out by the courts on the ground that the case was not “ripe” – that is, it was too soon for plaintiffs to show injury).

Taussig, the regulatory expert at Kabbage, reports that the Comptroller of the Currency, Robert J. Otting, has promised “a thumbs-up or thumbs-down” decision by the end of July or early August on issuing fintechs a national bank charter. He counts himself as “hopeful” that OCC’s decision will see both of the regulator’s thumbs pointing north.

The Conference of State Bank Supervisors, meanwhile, has extended an olive branch to the fintech community in the form of “Vision 2020.” CSBS touts the program as “an initiative to modernize state regulation of non-bank financial companies.” As part of Vision 2020, CSBS formed a 21-member “Fintech Industry Advisory Panel” with a recognizable roster of industry stalwarts: small business lenders Kabbage and OnDeck Capital are on board, as are consumer lenders like Funding Circle, LendUp and SoFi Lending Corp. The panel also boasts such heavyweights in payments as Amazon and Microsoft.

Working closely with the fintech industry is a “key component” of Vision 2020, Margaret Liu, deputy general counsel at CSBS, told AltFinanceDaily in a recent telephone interview. CSBS and the fintech industry are “having a dialogue,” she says, “and we’re asking industry to work together (with us) and bring us a handful of top recommendations on what states can do to improve regulation of nonbanks in licensing, regulations, and examinations.

“We want to know,” she added, ‘What the main friction points are so that we can find a path forward. We want to hear their concerns and talk about pain points. We want them to know the states are not deaf and blind to their concerns.”

Snapchat to Terminate Payment Service Snapcash (And its x-rated subculture?)

July 24, 2018 Snapchat will be terminating its payment service platform, Snapcash, on August 30. Launched in 2014, Snapcash allows users to send money to each other (via a cash app) in a fast and free way. Money goes to users’ bank accounts that are linked to their debit cards and the payment processing is handled by Square.

Snapchat will be terminating its payment service platform, Snapcash, on August 30. Launched in 2014, Snapcash allows users to send money to each other (via a cash app) in a fast and free way. Money goes to users’ bank accounts that are linked to their debit cards and the payment processing is handled by Square.

“Snapcash was our first product created in partnership with another company – Square,” a Snapchat spokesperson told Techcrunch in a statement. “We’re thankful for all the Snapchatters who used Snapcash for the last four years and for Square’s partnership!”

Snapchat’s decision to discontinue the payment service may come because of steep competition from Venmo, PayPal, Zelle and Square Cash, which all specialize in payments. But Snapcash may also be a liability for the company since it’s reportedly been used for X-rated activities. When Snapcash was first introduced, a story on Motherboard suggested that it would enhance Snapchat’s lingering subculture of amateur pornography. By the following year The New York Times reported that although the payment activity attributed to such pursuits was small, both strippers and adult video stars (male & female) were indeed using the service to charge users for personalized photos.

Although Square’s partnership with Snapchat will be coming to an end, Square made it clear in a statement to Techcrunch that its peer to peer Square Cash product is still alive and well with more than 7 million monthly customers.

It is unclear if the phase-out of Snapcash will result in job cuts at the company. But Snap Inc., which owns Snapchat, already laid off about 200 employees in March of this year. The company went public last year on the New York Stock Exchange as SNAP. Snap Inc. also has a hardware division called Spectacles, which sells sunglasses with a camera in it. According to a Cheddar story today, the chief of Spectacles, Mark Randall, has left Snap Inc. to start his own company.

Snap Inc. was founded by in 2011 by CEO Evan Spiegal, Bobby Murphy and Reggie Brown. The company is headquartered in Los Angeles.

Tech Changes Lending And Payments The World Over

June 25, 2018 On a business trip to China last summer, Matt Burton had plenty of money in his wallet but it was practically useless.

On a business trip to China last summer, Matt Burton had plenty of money in his wallet but it was practically useless.

Case in point: He had a lengthy standoff with a Shanghai taxi driver who insisted on a mobile-phone payment. “I spent 20 minutes arguing with the cabbie,” says Burton, one of the founding partners at Orchard Platform, a leading provider of technology and software to the alternative lending industry. “You’d think that — out of all of the professions — a taxi driver would accept cash.”

The New Yorker finally convinced the cab driver to take the payment in renminbi, China’s paper currency. The incident, meanwhile, is illustrative of how deeply and widely mobile payments have penetrated the huge Chinese market. “No one in China carries wallets anymore,” Burton reports. “Everyone pays with their smart-phones. Even the elderly women selling vegetables on the side of the road accept mobile payments,” he adds. “Cash has become a hassle.”

Welcome to China’s financial technology revolution. Almost overnight, China’s population graduated from calculating with the 16th-century abacus to showcasing what is arguably the world’s most sophisticated system of mobile payments. Thanks to financial technology, China is fast becoming a cashless economy. China is just one place outside the U.S. where financial technology is catching on in a big way. As Americans remain, for the most part, wedded to suburban drive-in banks, walk-up automated teller machines, and plastic credit and debit cards, the rest of the world is rapidly embracing digital solutions. And nowhere is that happening more dramatically than in China.

According to the most recent figures released by China’s Internet Network Information Center, the country had 724 million mobile phone users at the end of June 2017. China’s Ministry of Industry and Information Technology reports, moreover, that consumers paying for everything from food and clothing to utility bills to movie tickets and – you guessed it, cab fare — engaged in 239 billion mobile payment transactions in 2017, a surge of 146 percent over the previous year.

Mobile payments have become a $16 trillion industry in China, the ministry adds, accounting for about half of all such transactions in the world.

And there’s ample room to grow. The World Bank discloses that there are now 772 million Internet users in China, more than double the entire population of the U.S. Yet that leaves 50% of China’s population – mostly in the countryside and rural areas – who are not yet plugged in to the Internet.

Two Chinese mobile-payment platforms dominate the industry. Ant Financial is the 800-pound-gorilla, its Alipay program boasting 520 million global users on its website. It’s an affiliate of publicly traded Alibaba Group Holding, an online merchandiser known as the “Amazon of China” which was founded by entrepreneur Jack Ma, reputedly the richest man in China.

Two Chinese mobile-payment platforms dominate the industry. Ant Financial is the 800-pound-gorilla, its Alipay program boasting 520 million global users on its website. It’s an affiliate of publicly traded Alibaba Group Holding, an online merchandiser known as the “Amazon of China” which was founded by entrepreneur Jack Ma, reputedly the richest man in China.

Alipay not only has bragging rights to roughly 60 percent of China’s digital and online payments market but, in 2013, it overtook PayPal as the global leader in third-party payments. With deep roots in e-commerce, Alipay is the go-to payments option for online shoppers, who are steadily migrating from laptops to mobile devices.

WeChat Pay is the upstart in the duopolistic rivalry. Launched in 2013, nearly a decade later than its rival, it’s a unit of conglomerate Tencent Holdings, a social network and messaging platform often compared to Facebook. As WeChat continues to add subscribers, its Tenpay app has been growing accordingly, eroding Alipay’s market share as new users gravitate to the e-payments program. While WeChat records fewer payments than Alipay, Forbes magazine reports that it claims more users.

Whatever WeChat’s virtues, Ant Financial continues to chew up the scenery. It recently topped the charts as the world’s “most innovative” fintech in 2017, as reckoned by a research team formed by accounting giant KPMG and H2 Ventures. China scored a hat trick, moreover, as two additional homegrown fintechs — online property-and-casualty insurer ZhongAn and credit-provider Qudian Inc. — took second and third place, respectively, in KPMG/H2’s rankings. For good measure, China also claimed five of the top ten spots on the “most innovative” list, edging out the U.S., which had four.

Whatever WeChat’s virtues, Ant Financial continues to chew up the scenery. It recently topped the charts as the world’s “most innovative” fintech in 2017, as reckoned by a research team formed by accounting giant KPMG and H2 Ventures. China scored a hat trick, moreover, as two additional homegrown fintechs — online property-and-casualty insurer ZhongAn and credit-provider Qudian Inc. — took second and third place, respectively, in KPMG/H2’s rankings. For good measure, China also claimed five of the top ten spots on the “most innovative” list, edging out the U.S., which had four.

Financial analysts recently surveyed by the Financial Times reckon Ant Financial’s market valuation at $150 billion, catapulting the company into the rarified status of not just a “unicorn,” but a “super-unicorn.” (Named after the rarely seen mythical one-horned horse, “unicorns” are start-ups valued at $1 billion). So robust is Ant Financial’s market valuation that the global investment community is salivating over its impending initial public offering.

(Ant’s progenitor, Alibaba, holds bragging rights as the largest IPO ever, according to the Financial Industry Regulatory Authority. It raised $21.8 billion in 2014; its NYSE-listed stock was trading at $194.36 in mid-May, essentially in the same league as Apple and Facebook, trading at $188.80 and 187.08, respectively, on Nasdaq.)

“Four of the largest fintech unicorns in the world are coming out of Asia,” notes Dorel Blitz, the Tel Aviv-based head of fintech at KPMG. “The companies are getting bigger and stronger,” he adds, “and you’re beginning to see more direct investment in public fintech companies as well.”

Adds Orchard’s Burton: “I think it shows you how massive the opportunities are outside the U.S.”

Ant Financial and WeChat are also serving as a world-class demonstration project on how fintechs can turn a tidy profit while opening up financial services to large populations who lack access to basic financial services, thereby providing entry to the middle class. The two platforms have provided “financial inclusion for tens of millions, if not hundreds of millions of people” who previously were on the periphery of the banking and financial system, says Kai Schmitz, a fintech lender at International Finance Corporation that lends to private businesses in the developing world.

Once people are making electronic payments on their mobile devices, Schmitz notes, it creates a “pathway” to a whole panoply of financial services, including personal and business loans, savings, insurance, and investments.

“You can create a user profile so that a large part of the population that could not be reached (by traditional financial institutions) are now making payments and can be followed on the data track,” he says.

The World Bank reports that two billion adults and 200 million businesses in the developing world are currently unable to access even basic financial services. Through IFC, the World Bank has invested $370 million in fintech companies operating throughout Asia, the Middle East, Africa and Latin America. The fintechs, an IFC communications manager told AltFinanceDaily, offer “a range of products and services — from e-wallets, virtual banks, lending, and online payments to retail payment points and exchanges.” IFC, she adds, also invests in fintech funds.

Anju Patwardhan is the U.S.-based managing director at CreditEase Fintech Investment Fund, a $1 billion Chinese venture capital firm that invests in fintechs delivering financial services to “unbanked” and “underbanked” populations. “They are living in Africa, Bangladesh, China and elsewhere on less than two dollars a day and have no access to financial services,” she says.

“But there are also a very large number of people who may be technically included in the financial system but still don’t have access to a full range of financial services at reasonable prices,” she adds. “If someone is borrowing from a moneylender or pawnbroker, it doesn’t count (as financial inclusion). In that case, the number of people is very much more than two billion.”

Once phone towers are built and a payments infrastructure is in place, fintechs promising more sophisticated financial services can operate similarly to the settlers who followed pioneers in the U.S.’s westward expansion. That’s been the story in Kenya and other African countries where M-Pesa (“pesa” is Swahili for money) and other mobile-phone payments systems set up shop a decade ago.

Branch International, based in San Francisco but doing business exclusively in emerging and frontier markets for only three years, is one of the settlers. It boasts that it now has the “No. 1 finance app in Africa.” In March, Branch raised $70 million in a second-stage round of debt and equity financing from a group of venture capitalists led by Trinity Partners that included Patwardhan’s CreditEase and the IFC. Patwardhan will serve as an advisor to Branch’s board.

Branch’s principal business is making loans and micro-loans ranging from as little as $2 to $1,000 in Nigeria, Kenya, and Tanzania. Despite its name, Branch touts itself as a “branchless bank”, all of the credit transactions taking place on mobile devices, says Matt Flannery, Branch’s chief executive and founder. Its average loan amount is $25.

Branch’s principal business is making loans and micro-loans ranging from as little as $2 to $1,000 in Nigeria, Kenya, and Tanzania. Despite its name, Branch touts itself as a “branchless bank”, all of the credit transactions taking place on mobile devices, says Matt Flannery, Branch’s chief executive and founder. Its average loan amount is $25.

Many of Branch’s customers are individuals and businesses who often had trouble obtaining credit from established financial institutions or were ineligible for loans. But, according to Branch’s website, it’s possible for a prospective borrower to obtain a loan in just a matter of minutes. “Branch eliminates the challenges of getting a loan by using the data on your phone to create a credit score,” the website says. Branch promises privacy, fees that are “fair and transparent,” and terms that “allow for easy repayment” with no “late fees or rollover fees”. “As you pay back on time,” the website also says, “our fees decrease, and you unlock larger loans with more flexible terms.”

The platform, CEO Flannery says, has lent out $100 million dollars to roughly that same number of people. “The formal financial system in African countries is generally composed of old-fashioned banks that are risk-averse and fairly slow to make lending decisions,” he says. “People really appreciate us,” Flannery adds. “I’d say we’re like Uber and they’re the horse-and-buggy.”

The company is growing by 20 percent month-over-month and expects to disburse more than $250 million in 2018. Asked to describe Branch’s typical borrower, Flannery says: “We have some rural users (of Branch’s finance app). But in general we’re serving the commercial middle-class — shopkeepers and entrepreneurs – in urban capitals.” Want to know precisely who Branch’s customers are? “Just go to downtown Lagos (the capital of Nigeria and the largest city on the African continent) and you’ll see all different kinds of businesses and single-owner merchants on street corners,” Flannery says.

Jeff Stewart, the founder and chairman of Lenddo (which recently merged with competitor EFL) asserts that his firm’s machine learning technology and risk modeling techniques, which are being deployed in emerging countries from Costa Rica to The Philippines, have the capacity to assess the “creditworthiness of everyone on the planet.” In the absence of credit history in much of the developing world, he explains, this can done by constructing a risk profile combining both “psychometrics” and a “digital footprint.”

Psychometrics is a behavioral assessment tool based on a prospective borrower’s “Big Five” personality traits: openness to experience, conscientiousness, extraversion, agreeableness, and neuroticism (OCEAN for short). “What we’ve been able to show,” Stewart asserts, “is that certain personality types have a positive and negative correlation with repayment. It’s not 100 percent accurate. But you can predict the statistical recovery ratio on repayment. You can say that, for a person with a high score, something like 88 out of 1,000 people (with his or her profile) would not repay.”

Psychometrics is a behavioral assessment tool based on a prospective borrower’s “Big Five” personality traits: openness to experience, conscientiousness, extraversion, agreeableness, and neuroticism (OCEAN for short). “What we’ve been able to show,” Stewart asserts, “is that certain personality types have a positive and negative correlation with repayment. It’s not 100 percent accurate. But you can predict the statistical recovery ratio on repayment. You can say that, for a person with a high score, something like 88 out of 1,000 people (with his or her profile) would not repay.”

The digital footprint, which is the second “critical component,” Stewart says, analyzes a prospective borrower’s reliability by reconnoitering their smartphone usage. “We’ll look at everything on your phone,” he says, “How you use the phone. Whom you interact with. When you use your phone. There are thousands of features that generate a digital footprint. Everything from meeting someone at a sports bar to the apps on your phone to things like e-mailed receipts that show your financial activity.”

Such methods help build credit for those lacking credit history while rehabilitating those whose credit history is blemished. And all that’s needed is a smartphone. “We’ve turned the smartphone into a credit bureau,” Stewart says.

The acquisition of smartphones is taking place at a blistering pace, Stewart notes, now that cell phone costs are “at the bottom of the cost pyramid” in many countries. For example, a “low-end Android” now fetches as little as $25 in Africa. “One credible study I’ve seen shows that every 10% percent rise in access to smartphones translates into a 1/2 percent rise in a country’s gross domestic product,” Stewart says.

While the private sector is driving the trend to financial inclusion in China and Africa, India’s government-driven model “is setting a new global standard in using financial technologies to support financial inclusion,” declares Patwardhan of CreditEase, who also lectures at Stanford. “The country has become a giant testing ground for financial inclusion and innovation,” she argues in a recent academic paper, “and may become a role model for other emerging economies.”

India’s state-run effort includes a $1.3 billion digital identity program known as Aadhaar. Under Aadhaar (which means “foundation”), the state issues residents a 12-digit identity number that’s based on their biometric data –such as fingerprints and iris scans — and personal information. The ID number covers more than 1.19 billion residents. In just the first two years after Aadhaar’s 2009 debut, Patwardhan says, more than 250 million Indians were able to open bank accounts.

Jo Ann Barefoot, chief executive at Barefoot Innovation Group in Washington, D.C. and a senior fellow emerita at Harvard’s Kennedy School of Government, agrees. She notes that Aadhaar opened up access to both fintech services and bank accounts to women who were long treated as second-class citizens by the social and economic system. “India’s digital ID program means that wives and daughters have identity now,” she says.

“In the past,” she adds, “only (male) heads of households would have family identity documents and a government card — which would be the equivalent of having a Social Security number in the U.S. But the wife wouldn’t have her own card. So this is a massive door-opener to fintech growth. And it’s also opening up (all areas of) finance to millions and millions of people.”

India’s “digitalization” program, moreover, has entailed development of a national payments network called “unified payments interface,” or UPI. The combination of UPI and Aadhaar as well as other digital initiatives have resulted in “a surge of online lending platforms,” says Patwardhan, citing Capital Float, NeoGrowth, Faircent, LendingKart, Quiklo, IndiaLends, CreditExchange, and Onemi.

The homegrown fintechs, however, will be up against tremendous external pressure as India, with 1.3 billion people and poised to overtake China in population growth, is generating enormous interest from global fintechs. Among outside platforms piling into the country are China’s Ant Financial and WeChat. The former took a $1 billion stake in Paytm, an Indian mobile payments and e-commerce company. Similarly, competitor WeChat’s parent, Tencent, has invested in Hike, a mobile wallet valued at $1.4 billion last June, according to CNBC, exciting investor interest as a unicorn.

U.S. companies are getting into the act too. Google launched digital payments app Tez last September, which “is taking advantage of India’s infrastructure and has already gotten 30 million downloads,” Patwardhan says. In February, Facebook rolled out a peer-to-peer payments feature on WhatsApp. Even Branch’s Flannery has announced that his “branchless bank” plans to earmark part of its $70 million war chest to offer $2-to-$1000 loans on the subcontinent.

Having banned high-denomination paper bills as a way to rein in corruption and aiming at a cashless economy, India has been innovating in ways that “have gone the Chinese one better,” marvels Patwardhan. “Their payment systems going through the UPI network are interoperable,” she notes, for example. “You don’t have to be on the same app or with the same bank. India is now on the cutting edge.”

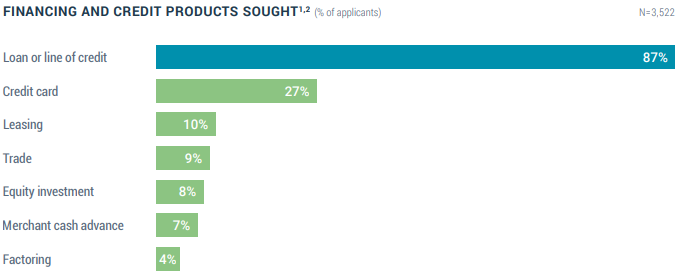

More Small Businesses Seeking Merchant Cash Advances Than Factoring

May 23, 2018 Seven percent of small employer firms in the US that applied for financing in 2017 applied for a merchant cash advance, the latest report by the Federal Reserve shows, while only 4% applied for factoring. Small employer owned firms were defined as businesses that have 1 to 499 full-or part-time employees. 69% of those surveyed generated less than $1 million in revenue last year. That revenue demographic may be on the low end for the factoring industry though. Factoring’s popularity in that demographic, however, decreased in 2017, according to the report. The 4% figure of small businesses that applied for factoring in 2017 was down from 7% in 2016.

Seven percent of small employer firms in the US that applied for financing in 2017 applied for a merchant cash advance, the latest report by the Federal Reserve shows, while only 4% applied for factoring. Small employer owned firms were defined as businesses that have 1 to 499 full-or part-time employees. 69% of those surveyed generated less than $1 million in revenue last year. That revenue demographic may be on the low end for the factoring industry though. Factoring’s popularity in that demographic, however, decreased in 2017, according to the report. The 4% figure of small businesses that applied for factoring in 2017 was down from 7% in 2016.

Auto and equipment loans had the highest approval rates among all financing options available to small businesses, at 82%. Merchant cash advances followed behind them at 79%. Lines of credit and business loans carried approval rates of 69% and 62% respectively. SBA loans came in at 54%.

When it comes to satisfaction, online lenders such as Lending Club, OnDeck, CAN Capital, and PayPal, have markedly improved over time, the report shows. The net satisfaction score of online lenders has increased from 19% in 2015 to 35% in 2017.

On transparency, online lenders rank at about the same level as large banks, though applicants were more likely to be dissatisfied with the interest rates of an online lender and the long and difficult application process with a large bank.

Kabbage Reveals Plans for a ‘Reverse Play’

May 22, 2018 When it comes to lending, the business models of Square and PayPal may be too good to ignore.

When it comes to lending, the business models of Square and PayPal may be too good to ignore.

According to Reuters, Kabbage plans to launch its own payment processing service by year-end. “The monoline businesses have a hard time succeeding long term,” Kabbage co-founder Kathryn Petralia is quoted as saying.

While Square and PayPal started off in payments and added lending, Kabbage sees the value proposition of the reverse play, to start off in lending and add payments.

But another Square and PayPal rival may not. Back in October, AltFinanceDaily questioned OnDeck CEO Noah Breslow during an interview about this very thing. At the time, Breslow responded that they were not going to sell merchant processing. “Never say never,” he said, “but not in the near future.”

Square and PayPal’s lending businesses differ from other online lenders in that they can solicit their existing payments customer base at virtually no cost. OnDeck, meanwhile, spent $53 million last year alone on sales and marketing to acquire loan customers.

Square’s acquisition of payments customers is not cheap, however. The company spent $253 million in sales and marketing last year. The advantage is in not needing to shell out additional cost to convert them into loan customers.

OnDeck still held the lead over both Kabbage and Square last year in loan originations at $2.1B vs $1.5B and $1.17B respectively. PayPal was not ranked.