Jack Dorsey Reveals Tweeting Irrelevant with Square

August 23, 2011Posted on May 1, 2011 at 11:33 AM

Twitter co-founder Jack Dorsey built his original company with toothpaste makers in mind. He might even say, “Thanks to Twitter, people in Istanbul can finally get tips on what makes the smiles in Shanghai so white. Tips on scrubbing those molars are transmitted in real time from Rio de Janeiro to Moscow!”

That’s good news for companies like Colgate, but for companies involved in technology, Dorsey reveals that Twitter is basically useless. “No one is following your company’s mundane tweets. No one cares if the Square card reader got a thumbs up from a business owner in Maine.” Of course he hasn’t actually said this in words, but his actions speak volumes.

Dorsey is also the founder and CEO of Square (https://squareup.com/), a credit/debit card reader that can plug right into an iPhone, iPad, or Android. We follow them on Twitter to keep an eye on news that might be worth sharing. But the only news, is no news. What’s up with that?

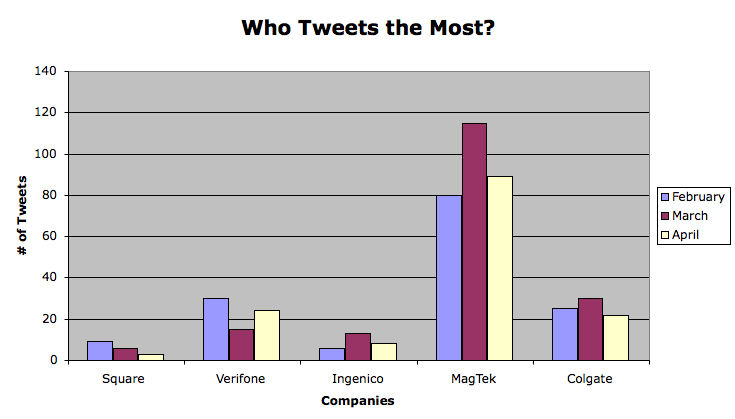

We compared Square’s tweets to three POS hardware companies, Verifone, Ingenico, and Magtek. We threw in Colgate for good measure.

Square, led by Twitter’s Dorsey, ranks last among peers in average monthly tweet volume. As Square seeks a permanent place for itself in the electronic payments world, it has undertaken a massive public relations campaign. None of which includes tweeting. Thank you Mr. Dorsey for revealing what most of the world already suspected, that commercial tweeting is useless.

Verifone just ate a bologna sandwich #yum

Ingenico just donated a credit card machine to a school in Sudan #charity

Magtek was mentioned in a newspaper in Andorra #werule

Colgate just came out with purple toothpaste #purple

Square just stole everyone’s customers while our competitors were tweeting about bologna #winning

Follow:

http://twitter.com/#!/VeriFone

http://twitter.com/#!/ingenico

http://twitter.com/#!/ColgateSmile

– AltFinanceDaily

Revenue Based Financing Continues to Spread at Global Pace

September 30, 2025 Earlier this month, Uber Eats joined the revenue-based financing movement by partnering with Pipe Capital.

Earlier this month, Uber Eats joined the revenue-based financing movement by partnering with Pipe Capital.

Karl Hebert, Vice President of Global Commerce and Financial Services at Uber, said of it, “We are happy to team up with Pipe to bring working capital to Uber Eats. Restaurants are our partners at Uber, and the backbone of our communities, yet many struggle with access to capital.”

It’s an unsurprising step considering rival DoorDash rolled out a merchant cash advance program nearly four years ago, though Uber arguably began experimenting with MCAs nearly ten years ago. And Uber is hardly doing it just to do it. Uber, for example, rolled out Uber Eats Financing, a revenue based financing product in Mexico through a partnership with R2 this past January, which went so well that they also rolled it out in Chile months later.

📢 Announcing a big milestone for R2 & @Uber!

Following a successful launch in Mexico, we’ve expanded our partnership with Uber Eats to Chile — bringing frictionless access to capital to thousands of merchants across the region. https://t.co/61WgP1ZtHy

— Roger Larach (@rogerlarach) April 30, 2025

In Chile with R2, the service is described as taking place entirely within the Uber Eats Manager App with a 5-minute application process and payments made automatically and deducted by a fixed percentage from sales made using the platform.

In the US with Pipe, it says that the Uber Eats App Manager will show capital offers from Pipe that are customized based on restaurant revenue, cash flow, and business performance.

Uber joins Amazon, Walmart, Shopify, Intuit, Stripe, DoorDash, PayPal, Square, GoDaddy, Wix, Squarespace and others in offering a revenue-based financing product.

Revenue-based financing as a product type is available in but not limited to the US, Canada, Mexico, Chile, UK, Germany, Ireland, Spain, South Africa, Nigeria, India, Hong Kong, Netherlands, Australia, Japan, Brazil, Singapore, and more.

The Great Concession, How the MCA Product Effectively Proved It Was Right All Along

September 26, 2025 There was no greater irony than the State of Texas banning ACH debits from sales-based financing providers at the same time that the State of Washington was celebrating the coming age of sales-based financing. In Texas, for example, the motivation for curbing sales-based financing was built on the premise that “this type of financing has raised significant concerns about predatory lending and that state attorneys general as well as the Federal Trade Commission have obtained high-profile judgments against such financing for predatory practices.” Meanwhile, in Washington, the motivation for the state holding the opposite opinion was that sales-based financing “increases access to capital for small businesses in Washington state, particularly those that have been historically underserved or underbanked.”

There was no greater irony than the State of Texas banning ACH debits from sales-based financing providers at the same time that the State of Washington was celebrating the coming age of sales-based financing. In Texas, for example, the motivation for curbing sales-based financing was built on the premise that “this type of financing has raised significant concerns about predatory lending and that state attorneys general as well as the Federal Trade Commission have obtained high-profile judgments against such financing for predatory practices.” Meanwhile, in Washington, the motivation for the state holding the opposite opinion was that sales-based financing “increases access to capital for small businesses in Washington state, particularly those that have been historically underserved or underbanked.”

How did these states reach the opposite conclusion?

There’s no caveat to how the Washington State program works. The State’s Department of Commerce partnered with Grow America and the operation is backed by a federal grant (SSBCI-21031-0048) to roll out and administer a revenue-based financing program as part of Washington’s State Small Business Credit Initiative. It’s sales-based financing or in this case revenue-based financing (which is the more common phrase these days). Grow America’s revenue-based financing program utters a very familiar phrase in its marketing.

“The months you generate more revenue, you pay a higher amount, when business is slower you pay less,” the company advertises.

This was at one time the signature calling card of a merchant cash advance, but now such features have been repackaged and rebranded into something similar but different, and everybody is doing them.

The Grow America program applies a 20% holdback on adjusted monthly revenue and requires a minimum monthly payment of $1,000 if the 20% holdback does not generate at least $1,000 for the month. Merchants can get approved for anywhere from $50,000 to $1 million. The product is marketed as having a 1.24 factor rate and an estimated 14.27% APR with a 3-year term. As industry participants are aware, increasing sales would translate into increasing payments, which means a rapidly paid off loan could potentially result in a final outcome APR in the triple digits, far and away from the “estimate.”

The irony is that the notable benefits of a similar product, merchant cash advances, which have no minimum monthly payments, no fixed term, and are not absolutely repayable, are eliminated when restructured in this way and presented as “revenue-based financing loans.” Revenue-based financing loans take the underlying structure of MCAs (payments tied to sales) and then strip away the benefits. However, when structured as loans, the argument often goes that they are likely to be cheaper, which may be true on average, but is not always true.

Indeed, Grow America leads specifically with price as for why its product, similar to its privately owned competitors, are the better option:

“There are a lot of online lenders offering revenue-based loans that promise instant approvals, but their terms are intentionally confusing, and the fees are high,” Grow America advertises. “Our lenders aren’t like that. They’re mission driven.”

In Texas, the author of the bill that banned debits from such financing providers “informed the [legislative] committee that commercial sales-based financing has become a popular financing option for small businesses desperate for credit and that, unlike traditional loans, this type of financing is repaid as a percentage of future sales or revenue.”

Indeed, it is very popular. The largest providers or brokers of such financing today whether structured as a purchase or loan, are household names like Amazon, Walmart, Shopify, Intuit, Stripe, DoorDash, PayPal, Square, GoDaddy, Wix, Squarespace and more. Some structure them as a purchase and call it a merchant cash advance and some structure it as a loan and call it revenue-based financing. In either case, payments are tied to the percentage of future sales or revenue.

In egregious cases of wrongdoing one way or another, such incidents have historically been a result of deceptive marketing or payments from a merchant exceeding the contracted amount. In New York, when transactions are structured as a purchase, courts generally look to make sure that the agreements have a reconciliation provision in the agreement, whether the agreement has a finite term, and whether there is any recourse should the merchant declare bankruptcy. Legally speaking, the products have become pretty well defined and understood in the court system.

Like Washington State, GoDaddy, which recently announced its new merchant cash advance program, markets its product in an almost identical fashion.

“If your sales go up, the MCA will be paid sooner; if the sales are slow, it’ll take longer,” GoDaddy says.

Same message.

Washington State requires merchants to make a minimum payment every month and a balloon payment if not fully repaid within 3 years. GoDaddy, by contrast, advertises no minimum payment amount, no set payment schedule, no penalties, and no late fees. One’s a loan, one’s a purchase.

While the best course of action is best left to the merchants, there appears to be a near-universal concession that the underlying nature of how merchant cash advance agreements were contemplated, payments tied to sales, made strong logical business sense all along. Washington State emphasizes this fact.

“We know that your business has its own needs and loans with fixed payment amounts may not be the best option for you,” they advertise. “The revenue-based financing fund offers loans with flexible payback terms so you can grow your business immediately and pay back your loan based on your varying revenue.”

Recent studies also now highlight the benefits of cash-flow-based underwriting.

In Sharpening the Focus: Using Cash-Flow Data to Underwrite Financially Constrained Businesses, “The paper finds that adding cash-flow information substantially increases the predictive signal of models that rely primarily on the business owners’ personal credit scores and firm characteristics.”

There’s also Square, the largest revenue-based financing provider in the US, that has explained why this system just works better. Square says that they can fund more businesses and have higher payment success rates than if they were to follow more conventional methods of underwriting and repayment.

“Square Loans addresses [the credit] gap by using near real-time business data to assess creditworthiness, evaluating metrics such as transaction volume and revenue patterns to offer short-term loans — with repayment on average in 8 months,” Square wrote in a White Paper. “This allows for a more accurate and timely understanding of a business’s capacity to borrow and repay. And loan repayments are higher during periods when business is stronger and reduced when sales are lower.”

What’s the sentiment these days on payments tied to sales revenue? The market has spoken.

FICOs Are 580 and Below, Repayment Rates Are Above 97%

September 23, 2025Block recently published an interview with Juan Hernandez, the company’s Head of Credit and Underwriting for its consumer lending divisions. Among the most interesting details Hernandez revealed is that 70% of Cash App Borrow customers have FICO scores of 580 or below, but their repayment rates are above 97%.

“That is only possible because our models are continuously learning from customer activity across Cash App and Afterpay,” Hernandez said of it.

Block sees income, deposits, spending patterns, savings behavior, and repayment behavior across the spectrum of its ecosystem and is able to use that data to make better predictions than legacy third party credit indicators.

“The future of credit will be based on actual repayment ability, not outdated proxies,” Hernandez said. “With near real-time data and modern modeling, we can finally build a system that is more inclusive and safer than traditional credit scores that look backward, update slowly, and often misclassify people who are capable of managing credit.”

“The future of credit will be based on actual repayment ability, not outdated proxies,” Hernandez said. “With near real-time data and modern modeling, we can finally build a system that is more inclusive and safer than traditional credit scores that look backward, update slowly, and often misclassify people who are capable of managing credit.”

Block has made a name for itself in the lending space. Cash App Borrow originated $9B in loans in 2024 while its sister company Square Loans, which provides capital to small businesses, is the largest online small business lender that AltFinanceDaily tracks. Square Loans originated $5.7B in 2024.

In March of this year Block received FDIC approval for its industrial bank, Square Financial Services Inc, to offer the Cash App Borrow loan product directly.

The Largest Sales-Based Financing Providers

May 27, 2025Who are some of the largest sales-based financing providers in the US? The following companies are repaid as a percentage of sales or revenue, in which the payment amount may increase or decrease according to the volume of sales made or revenue received by the recipient:

| Sales-Based Financing Providers |

| Square |

| PayPal |

| Amazon (via Parafin) |

| Walmart (via Parafin) |

| Shopify |

| Intuit |

| Stripe |

| DoorDash (via Parafin) |

The State of Washington has also recently announced it will be offering sales-based financing through a Department of Commerce initiative.

Among those listed above, Square recently published a White Paper on the impact of its sales-based financing.

“Square Loans has opened credit to populations who traditionally have had less access to business loans. As of the third quarter of 2024, approximately 58% of Square Loan customers are women-owned businesses, compared to the industry average of 19%.38 And 15% of Square Loans go to Black/African-owned businesses compared to an industry average of 6.6%, while 14% of loans go to Hispanic/Latinx-owned businesses compared to the industry average of 11.3%.”

The State of Washington Launches a Revenue Based Financing Business

May 25, 2025 The State of Washington is getting in to the revenue based financing business. Coinciding with Broker Fair 2025 on May 19th, the Washington State Department of Commerce announced it was launching the Revenue-Based Financing Fund (RBF) loan program for small businesses. Its administered by Grow America.

The State of Washington is getting in to the revenue based financing business. Coinciding with Broker Fair 2025 on May 19th, the Washington State Department of Commerce announced it was launching the Revenue-Based Financing Fund (RBF) loan program for small businesses. Its administered by Grow America.

“This is one of the most innovative loan programs we’ve ever launched,” said Commerce Director Joe Nguyễn. “It’s not a typical business loan. It’s a Pay-As-You-Earn loan that works with the reality of running a small business. Instead of fixed monthly payments, businesses repay based on what they actually make. So if sales slow down, payments stay low. If business picks up, payments adjust. It’s flexible, it’s fair, and it’s the kind of practical solution we need to support small businesses across Washington.”

$13M in funding has been allocated to this program so far. Funding works similar to a business loan from Square or PayPal where there is technically a term and minimum monthly payment required, but the repayment system is based on a percentage of sales, namely 20% of them.

“At Grow America, we’re excited to launch the Washington Revenue-Based Financing Fund,” said Daniel Marsh III, Grow America president. “This program offers flexible capital, empowering Washington’s small businesses, especially entrepreneurs, to scale operations and achieve sustainable success.”

“Revenue-based financing provides you with flexible upfront capital, and its payback terms are customized to your cash flow and fluctuate based on your revenue,” the marketing materials state. “It’s ideal for small businesses that are seasonal, may not have a consistent income, or require an alternative to a traditional loan.”

Top Online Small Business Lenders of 2024

March 7, 2025Below is a list of the top online small business lenders in 2024 for those that disclose their data:

| Company | 2024 Origination Volume |

| Square Loans | $5.7B |

| Enova | $3.98B |

| Bankers Healthcare Group | $3.7B |

| Shopify Capital | $3B |

| PayPal | $3B |

| QuickBooks Capital | $1.8B |

| North Mill Equipment Finance | $654M |