Sean Murray to Moderate Best Practices Panel at New York Institute of Credit Event

October 15, 2018AltFinanceDaily President and Chief Editor Sean Murray will be moderating a best practices panel at the New York Institute of Credit Event on October 16th. The event is also supported by the IFA Northeast, the Alternative Finance Bar Association, and AltFinanceDaily.

The subject of the panel is to discuss best practices when dealing with different financial firms, namely ABL, factoring, and merchant cash advance. The panelists are:

- Bill Gallagher, President, CFG Merchant Solutions

- Bill Elliott, President, First Business Growth Funding

- Raffi Azadian, CEO, Change Capital

- Dean Landis, President, Entrepreneur Growth Capital

Is Your Firm Ready for Machine Learning?

October 15, 2018Artificial intelligence such as machine learning has the potential to dramatically shift the alternative lending and funding landscape. But humans still have a lot to learn about this budding field.

Across the industry, firms are at different points in terms of machine learning adoption. Some firms have begun to implement machine learning within underwriting in an attempt to curb fraud, get more complex insights into risk, make sounder funding decisions and achieve lower loss rates. Others are still in the R&D and planning stage, quietly laying the groundwork for future implementation across multiple areas of their business, including fraud prevention, underwriting, lead generation and collections.

“It’s entirely critical to the success of our business,” says Paul Gu, co-founder and head of product at Upstart, a consumer lending platform that uses machine learning extensively in its operations. “Done right, it completely changes the possibilities in terms of how accurate underwriting and verification are,” he says.

While there’s no absolute right way to implement machine learning within a lender’s or funder’s business, there are many data-related, regulatory and business-specific factors to consider. Because things can go very wrong from a business or regulatory perspective—or both—if machine learning is not implemented properly, firms need to be especially careful. Here are a few pointers that can help lead to a successful machine learning implementation:

Using machine learning, funders can predict better the likelihood of default versus a rule-based model that looks at factors such as the size of the business, the size of the loan and how old the business is, for example, says Eden Amirav, co-founder and chief executive of Lending Express, a firm that relies heavily on AI to match borrowers and funders.

Machine learning takes hundreds and hundreds of parameters into account which you would never look at with a rule-based model and searches for connections. “You can find much more complex insights using these multiple data points. It’s not something a person can do,” Amirav says.

He contends that machine learning will optimize the number of small businesses that will have access to funding because it allows funders to be more precise in their risk analyses. This will open doors for some merchants who were previously turned down based on less precise models, he predicts. To help in this effort, Lending Express recently launched a new dashboard that uses AI-driven technology to help convert business loan candidates that have been previously turned down into viable applicants. The new LendingScore™ algorithm gives businesses detailed information about how they can improve different funding factors to help them unlock new funding opportunities, Amirav says.

Lenders and funders always have to be thinking about what’s next when it comes to artificial intelligence, even if they aren’t quite ready to implement it. While using machine learning for underwriting is currently the primary focus for many firms, there are many other possible use cases for the alternative lenders and funders, according to industry participants.

Lead generation and renewals are two areas that are ripe for machine learning technology, according to Paul Sitruk, chief risk officer and chief technology officer at 6th Avenue Capital, a small business funder. He predicts that it is only a matter of time before firms are using machine learning in these areas and others. “It can be applied to several areas within our existing processes,” he says.

Collection is another area where machine learning could make the process more efficient for firms. Machines can work out, based on real-life patterns, which types of customers might benefit from call reminders and which will be a waste of time for lenders, says Sandeep Bhandari, chief strategy and chief risk officer at Affirm, which uses advanced analytics to make credit decisions.

“There are different business problems that can be solved through machine learning. Lenders sometimes get too fixated on just the approve/decline problem,” he says.

“Most underwriters don’t have enough data to effectively incorporate AI, deep learning, or machine learning tools,” says Taariq Lewis, chief executive of Aquila, a small business funder. He notes that effective research comes from the use of very large datasets that won’t fit in an excel spreadsheet for testing various hypotheses.

Problems, however, can occur when there’s too much complexity in the models and the results become too hard to understand in actionable business terms. For example, firms may use models that analyze seasonal lender performance without understanding the input assumptions, like weather impact, on certain geographies. This may lead to final results that do not make sense or are unexpected, he says.

“There’s a lot of noise in the data. There are spurious correlations. They make meaningful conclusions hard to get and hard to use,” he says.

The more precise firms can be with the data, the more predictive a machine learning model can be, says Bhandari of Affirm. So, for example, instead of looking at credit utilization ratios generally, the model might be more predictive if it includes the utilization rate over recent months in conjunction with debt balance. It’s critical to include as targeted and complete data as possible. “That’s where some of our competitive advantages come in,” Bhandari says.

Underwriters also have to pay particularly close attention that overfitting doesn’t occur. This happens when machines can perfectly predict data in your data set, but they don’t necessarily reflect real world patterns, says Gu of Upstart.

Keeping close tabs on the computer-driven models over time is also important. The model isn’t going to perform the same all along because the competitive environment changes, as do consumer preferences and behaviors. “You have to monitor what’s going well and what’s not going well all the time,” Bhandari says.

Certainly, as AI is integrated into financial services, state and federal regulators that oversee financial services are taking more of an interest. As such, firms dabbling with new technology have to be very careful that any models they are using don’t run afoul of federal Fair Lending Laws or state regulations.

“If you don’t address it early and you have a model that’s treating customers unfairly or differently, it could result in serious consequences,” says Tim Wieher, chief compliance officer and general counsel of CAN Capital, which is in the early stages of determining how to use AI within its business.

“AI will be transformative for the financial services industry,” he predicts, but says that doing it right takes significant advance planning. For instance, Wieher says it’s very important for firms to involve legal and compliance teams early in the process to review potential models, understand how the technology will impact the lending or funding process and identify the challenges and mitigate the risk.

“AI will be transformative for the financial services industry,” he predicts, but says that doing it right takes significant advance planning. For instance, Wieher says it’s very important for firms to involve legal and compliance teams early in the process to review potential models, understand how the technology will impact the lending or funding process and identify the challenges and mitigate the risk.

To be sure, regulation around AI is still a very gray area since the technology is so new and it’s constantly evolving. Banking regulators in particular have been looking closely at the issues pertaining to AI such as its possible applications, short-comings, challenges and supervision. Because the waters are so untested, there can be validity in asking for regulatory and compliance advice before moving ahead full steam, some industry watchers say.

Upstart, for example, which uses AI extensively to price credit and automate the borrowing process, wanted buy-in from the Consumer Financial Protection Bureau to help ease the concern of its backers as well as to satisfy its own concerns about the legality of its efforts. So the firm submitted a no-action request to CFPB. The CFPB responded by issuing a no-action letter to Upstart in September 2017, allowing the company to use its model. In return, Upstart shares certain information with the CFPB regarding the loan applications it receives, how it decides which loans to approve, and how it will mitigate risk to consumers, as well as information on how its model expands access to credit for traditionally underserved populations.

The No-Action Letter is in force for three years and Upstart can seek to renew it if it chooses.

Theoretically firms could have a computer underwriting model constantly updating itself without having a human oversee what the model is doing—but it’s a bad idea, industry participants say. “I believe there are companies doing that, and it’s a risky thing to do,” says Scott M. Pearson, a partner with the law firm Ballard Spahr LLP in Los Angeles.

During review of the models—and before implementing them—people should carefully review the models and the output to make sure there’s nothing that causes intrinsic bias, says Kathryn Petralia, co-founder and president of Kabbage, which is one of the front-runners in using machine learning models to understand and predict business performance.

“If you’re not watching the machine, you don’t know how the machine is complying with regulatory requirements,” she says.

Kabbage has teams of data scientists regularly developing models that the company then reviews internally before deploying. The company is also in frequent contact with regulators about its processes. Petralia says it’s very important that firms be able to explain to regulators how their models work. “Machines aren’t very good at explaining things,” she quips.

As a best practice, Pearson of Ballard Spahr says lenders and funders shouldn’t use any machine learning model until it’s been signed off on by compliance. “That strikes a pretty good balance between getting the benefits of AI and making sure it doesn’t create a compliance problem for you,” he says.

While AI has many benefits, industry participants say alternative lenders and funders need to be mindful of how it can be applied practically and effectively within their particular business model.

Craig Focardi, senior analyst with consulting firm Celent in San Francisco, contends that the classic FICO score continues to be the gold standard for credit decisions in the U.S. He warns firms not to get overly distracted trying to find the next best thing.

“Many fintech lenders have immature risk management and operations functions. They’re better off improving those than dabbling in alternative scoring,” he says, noting that data modeling is an entirely separate core competency.

Indeed, Lewis of Aquila cautions underwriters not to view AI as a silver bullet. “AI is just one tool out of many in the lenders’ toolbox, and our industry should use it and respect its limitations,” he says.

The Broker: How Andy Savarese Changes Collars and Closes Deals

October 12, 2018 Title:

Title:

I’m the Managing Partner at JustiFi Capital, a brokerage in Farmingdale, Long Island. I started it September 2017 with my cousin, who’s the owner and my best friend. We do mostly MCA, but also some term loans.

His schedule:

I have a part-time/full-time job in the mornings. I work in sanitation for the town of Oyster Bay on Long Island. I typically wake up at around 3:37 a.m. I get into my yard at 4:15 a.m. and I go right into my route. My job is task completion. So the faster you work, the faster you get to go home. You get paid the same. I was fortunate to get on a fast truck, so I’m usually done between 7:45 a.m. and 9:30 a.m.

I go home, I take a quick shower, and I change my outfit. I go from blue collar to white collar. I get into the office around 10:30 a.m. and I start doing more of a mental hustle compared to a physical hustle.

At around 12:45 p.m., I take my lunch and I go to the gym for about 45 minutes. I get back to the office and I keep up the closing, the pitching, the selling, the prospecting. At around 5:30 p.m., I leave the office, I pick up my son from daycare, and since my wife works evenings, I take care of him at night until around 7:30 p.m., and get him ready for bed. The second he hits his crib, I hit my bed and I call it a day.

His background in the business:

About three years ago, I was driving oil trucks after sanitation, and my cousin, who is also my best friend, gave me a call. He knew I was breaking my butt all day. He had a friend that was starting his own ISO. So I did that for a year and I learned the industry. It didn’t really work out there, so I convinced my cousin to open up our own shop, which is JustiFi.

His process:

At JustiFi, we’ve been growing. We’re just grinding it out and things are going really well. We have four brokers and we keep it tight. We keep it small so that everybody is inundated with files and everybody’s making money and everybody’s happy. We don’t have any processors or chasers. We do it all on our own. We’re working the deal from beginning to end. My cousin has devised a pretty strategic marketing plan that inundates us with leads all day. I disperse them and I follow up with my guys and see how I can help. I overlook all of the closings and make sure that everything than can get worked is getting worked.

His biggest challenge as a broker:

A lot of people will say getting good leads and keeping your brokers happy. What I found is the most challenging part of being a broker in this industry is keeping a really level head and keeping your emotions out of the game. It’s a very tumultuous industry. One day, you could have 12 deals in the funding chute, the next day, your pipe could be dry. You could have a deal you think is going close and something happens on the funding call and it gets derailed. The point is that you’ve got to stay positive, you’ve got to stay confident, and you’ve got to roll with the punches. If not, you’re going to lose it and you’re going to get eaten alive. Because it’s a battlefield out there. You’ve got to keep your composure, no matter what the size of the deal. You’ve got to just keep pushing through. Because if not, you’re not going to make it.

His largest deal funded:

$250,000. And I made $38,000.

His advice for brokers:

When I go to close a good sized deal, or a tough deal, I don’t like to come off as a salesman. I’ll never do that. I’m going to come off as an advisor. I’m going to come off as a partner with you where I’m going to explain the ins and outs of the deal. I’m going to explain how it benefits you. I’ll never put on pressure or talk slang. I’m going to be a professional. You’ve got to kind of put yourself in [the merchant’s] shoes and you’ve got to see that it really makes sense for them. Because when it makes sense to you and it makes sense to them, you’re going to close the deal and you’re going to move forward.

But there are always deals that will never close, deals that you can’t sell. So you can’t be too hard on yourself. You’ve got to stay positive. You can’t beat yourself up if you don’t sell something. You’ve got to just do your best, stay neutral, and just talk to clients how you want to be talked to.

What he does to pump himself up for a deal:

If I know my day is bringing a big deal that I have to sell and I’m a little uneasy about it, I have an advantage. I’m on the back of a garbage truck all morning and I focus on what’s in store for me that day. If I have a big deal, I recite in my head [from the truck] how I’m going to report to my client. So when I get into the office, I dial up and I already know how the conversation is going to go. I have my rebuttals in my head, I have the direction, I have everything ready to go so that when I get on the call, I’m fully prepared.

Will you quit your morning job?

No. When my pension kicks in, I’ll leave. But I told myself the day I started this and the day I started seeing the return, “I’m never leaving sanitation. I won’t.” I made that promise to myself. There’s been days when I’ll have a five figure commission day and the next morning it’ll be pouring rain out, and I’ll say to myself, “Man, I just want to take the day off.” But no, I made a promise. I go in.

Why?

It keeps me grounded, it’s a stress relief. It’s what I am. It’s what I do.

Brief AltFinanceDaily San Diego Recap

October 6, 2018 More than 300 people attended the first AltFinanceDaily CONNECT event on the west coast at the Andaz Hotel in San Diego. The half-day learning and networking conference drew people in the small business finance space from across the country, including New York, Philadelphia, Detroit, Houston, Salt Lake City, and cities in Florida and all throughout California.

More than 300 people attended the first AltFinanceDaily CONNECT event on the west coast at the Andaz Hotel in San Diego. The half-day learning and networking conference drew people in the small business finance space from across the country, including New York, Philadelphia, Detroit, Houston, Salt Lake City, and cities in Florida and all throughout California.

Sam Bobley, CEO of Ocrolus, which provides technology solutions mostly to direct funders, was among the first to check in before the official start time at 1:30 p.m. He came in from New York.

“We went to Broker Fair in Brooklyn and made a lot of connections,” Bobley said. “We go to the other events, LendIt and Lend360, which are great, but they’re fairly broad. There, 1-2 out 5 people might be relevant [to online lending.] Here, everyone is. There’s no wasting time.”

“We went to Broker Fair in Brooklyn and made a lot of connections,” Bobley said. “We go to the other events, LendIt and Lend360, which are great, but they’re fairly broad. There, 1-2 out 5 people might be relevant [to online lending.] Here, everyone is. There’s no wasting time.”

The learning component of the day focused on sales and dealing with new regulations, primarily coming out of California.

“We wanted to learn about [the status of CA regulations],” said Kyle Readdick, CEO of Synergy Direct Solution in San Diego, a lead generator and funder in San Diego. “It’s obviously a concern.” He attended with his brother and CFO, Travis Readdick.

On the sales sides, Jennie Villano of Kalamata Advisors, Matt Price of Reliant Funding and Ilya Fridman of BFS, gave advice during the “Tips for ISOs” seminar. Technology and CRMs was one area of particular focus among the panelists as a must-have to scale.

“I’m so happy to be here,” said Mike Brooks, ISO relations manager with Smart Business Funding who flew in from New York. “I’m here to meet people, make contacts and make some money.”

Photos will follow soon. You should also follow us on instagram.

Greenbox Capital Introduces On Demand Loan Checkout Process

October 3, 2018Miami Gardens, Fl, 10-03-18

This latest on demand loan process function grants ISO partners the ability to increase term and funding amounts up to one month and 10%, respectively, without submitting a request. “The Box” was developed by CEO Jordan Fein and the innovative Greenbox IT team to give brokers additional flexibility.

The development mandate was to eliminate extraneous steps between the merchant and the broker which would further enhance those relationships and promote long lasting partnerships. “The Box” is now considered the most efficient, convenient user technology available.

“When the difference between winning and losing a deal is time, Greenbox Capital has provided a solution that allows our brokers to make more favorable terms, instantly! We have our pulse on the industry and the needs of our ISO partners. We regularly request feedback and implement upgrades to our technology to meet industry needs,” states Fein.

Greenbox Capital specializes in alternative funding options for small-and medium-sized business averaging at least $7,500 in revenue in each of the past 3 months. Greenbox Capital’s fast business cash advances and short-term small business loans make goals attainable.

The company’s small business financing programs include:

- Merchant Cash Advances (in available USA regions)

- Small Business Loans (in available USA and Canada regions)

- Invoice Factoring

- Business Lines of Credit

- Unsecured Financing

- Collateral-backed Funding

“We empower business owners to succeed by providing what they need most: access to working capital. We are committed to industry leadership in technology and will continue to develop processes that lead to a positive outcome for both merchant and broker,” adds Fein.

Greenbox Capital

855.442.3423

Info@greenbox.capital

The Largest Merchant Cash Advance in History

September 28, 2018 How would you like to be the funder to do a $40 million MCA transaction? According to the Securities & Exchange Commission, a deal of such magnitude was one of the many negligent acts that 1st Global Capital CEO Carl Ruderman did with investor money. Though the SEC refers to the merchant as an auto dealership in California, it’s roughly 9 dealerships with common ownership that collectively gross more than $550 million a year in sales. It’s the deal of a lifetime except that the ISO who brokered it has become the largest unsecured creditor to file a claim in the 1st Global bankruptcy. Records show they are owed approximately $3.9 million in unpaid commissions.

How would you like to be the funder to do a $40 million MCA transaction? According to the Securities & Exchange Commission, a deal of such magnitude was one of the many negligent acts that 1st Global Capital CEO Carl Ruderman did with investor money. Though the SEC refers to the merchant as an auto dealership in California, it’s roughly 9 dealerships with common ownership that collectively gross more than $550 million a year in sales. It’s the deal of a lifetime except that the ISO who brokered it has become the largest unsecured creditor to file a claim in the 1st Global bankruptcy. Records show they are owed approximately $3.9 million in unpaid commissions.

And its performance has not been without challenges, according to emails disclosed in the SEC case.

In April 2018, 1st Global employees discussed what to do about the dealerships’ lingering cash flow problems after becoming aware that the owner intended to either recapitalize the debt or sell the dealerships. The choice by then had come down to either continuing to fund them or to cut their losses, an email says.

“If they were to become insolvent, everyone loses,” wrote the Director of Accounting and Finance.

1st Global continued to fund them. The $40 million (approximate amount) was not disbursed all at once but in increments over the course of a year.

One week before 1st Global filed for bankruptcy, they signed a Binding Letter of Understanding with the dealerships acknowledging that the owner would be selling them. At that time the merchant had unpaid taxes of at least $9 million and had an outstanding receivable balance with 1st Global of $43 million. The Letter said that 1st Global would accept “whatever amount it receives [..] at this point as complete satisfaction” of the current RTR when the business is sold. 1st Global also agreed to forever release the dealerships’ owner personally from all legal claims. It was signed by Carl Ruderman 8 days before he resigned.

The merchant has not returned AltFinanceDaily’s inquiries. The banker named in the Binding Letter as having been exclusively hired to sell the dealerships, told AltFinanceDaily over the phone that he has never heard of 1st Global. 1st Global ceased operations on July 27th. The SEC filed a complaint against Ruderman and the company on August 23rd and an amended complaint on September 26th. The dealership transaction is used as an example of malfeasance in it twice.

New Record

No longer candidates for the largest merchant cash advance in history, two ancient deals that were famous during their eras for their size, ended up in default, and in doing so showed the industry that there was such a thing as too big.

One was a $4 million advance made by Strategic Funding Source in 2011 to a tourist attraction being produced at the Tropicana Hotel in Las Vegas. The Las Vegas Mob Experience, billed as the most technologically advanced interactive presentation of historical artifacts ever devised and set up in a 26,000 square foot total immersion facility, it was predicted to bring in 1.5 million visitors per year. But the deal quickly spiraled out of control, the exhibit shut down, and allegations of fraud were lodged in court. Though the Mob Experience was dubbed the largest merchant cash advance in history, it depends on whether or not you’re counting common ownership of multiple businesses as individual deals or one deal.

Dozens of advances made by Global Swift Funding in 2007 and 2008 to businesses controlled by the same west coast-based restaurateur, led to Global Swift’s demise. When the “restaurant king,” as he was known, filed for bankruptcy across all of his entities, Global Swift had outstanding future receivables with his businesses of approximately $8 million. Dan Chaon, a then representative of Global Swift, told a local newspaper at the time that the restaurateur was “a helluva sales-talk artist… he provided false financial statements, and everyone got caught up in that game.”

The Broker: How Elana Kemp Turns Values into Value

September 26, 2018 Title: Broker at Fundomate, a commercial finance brokerage in Los Angeles.

Title: Broker at Fundomate, a commercial finance brokerage in Los Angeles.

Background in business:

I started four years ago when I was living in Israel and I was working American hours. It was tough because I have four kids…A [non business] opportunity brought me to LA where my dad lives and where I’m from originally. So I jumped on that and continued doing brokerage part-time as a one man show for about a year. I met some people in the industry here in LA and started working with them. From there I went to Fundomate, then somewhere else. And then I came back to Fundomate.

What’s the difference between working for yourself and for a brokerage company?

Generating leads is so challenging to do on your own. If it wasn’t for that, I’d be a one man show all day long. I have to admit, though, that after a year, I did miss the infrastructure of working with people and the energy.

Why is it so hard to find leads?

It’s hard to find an honest lead generator. They promise you a lot, but at the end of the day, you don’t get much. I tried many different avenues [when I was working alone.] And I had one lead guy who I was really happy with and then he ended up in the hospital. So there went that. But otherwise, most of them didn’t perform the way they promised.

What’s your morning like with four kids?

Well, I’m not the first in the office. I work for someone who’s very understanding of my situation. I have a kind of cart blanche in terms of my hours. Of course, though, I’m awake at 6 / 6:30, and the second I’m awake, I’m on my phone, checking my emails. So [while] I’m not physically in the office, the second I’m awake, my workday starts. So I don’t make it to the office until 8:15 / 8:30.

Is there any ritual you have to close a deal?

If I have a big deal pending, like a $250,000 deal, I definitely take the time to envision the funding email and kind of manifest that. I definitely believe in the power of energy. If I don’t make a deal, I try not to take it home with me. I believe it’s meant to be and I’ll get the next one. I do believe there’s enough out there for everyone.

I recently read a fun fact – that elephants eat 400 lbs of food a day. It blew me away. And I thought “if an elephant can find 400 lbs of food to eat a day, then I can find enough deals to fund and support my family.”

Largest deal funded:

$325,000. Commission was $26,000.

Her style:

I get really close to my merchants. Some people think I get too close to them. Everybody has a different [style]. Sometimes [getting very close to a merchant] will make me win a deal. Sometimes it will make me lose a deal. Everybody has a different vibe that they feel comfortable with.

I get close to people very quickly. It’s just who I am. And in my opinion it works to my advantage because I have merchants that renew with me multiple times a year. And I know, no matter how many calls they get [from other brokers], they’re going to turn to me. I know that they trust me. I’ve had one merchant come over for dinner at my house. I have some merchants I check in with every few months and sometimes we don’t talk about money at all. We just talk about life.

On honesty:

I try to imagine that the merchant is like my dad. I want to treat them properly. And I believe in karma. I also say that if I get a deal funded but it was not 100% honestly done, then I like don’t want to feed my kids with that money.

Advice for brokers:

Don’t give up on your values for a deal. Values are more valuable than one deal funded. You can always fund another deal…a [reputation] can be broken down in like 2 minutes.

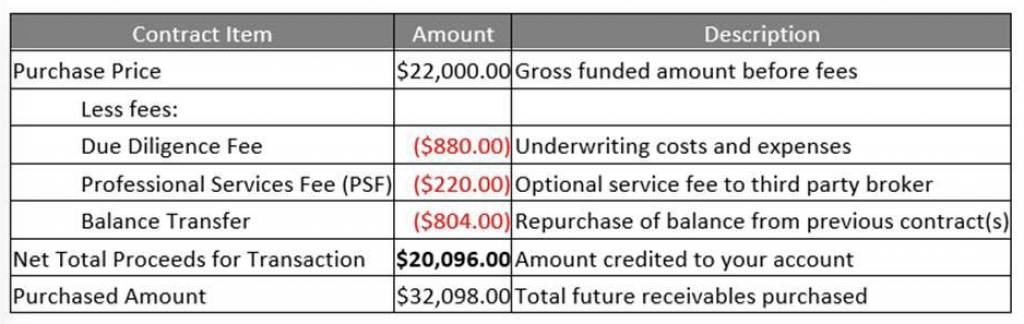

Yellowstone Capital Introduces a Smarter Box In Move Towards Transparency

September 26, 2018Yellowstone Capital CEO Isaac Stern announced a “Smarter Box” through social media channels this morning. The itemized box will be provided to merchants through a post-funding email as part of a company effort to maximize transparency.

According to the announcement:

“[We are] very serious about maximum transparency and disclosure to our funding partners’ great merchant customers. In addition to our new Purchase and Sale Agreement we will be using with each of the funding partners on our platform, we are also implementing a transaction summary email to ensure that all applicable fees, costs, disbursements and hold-backs are clearly understood by all parties. Our new contract will increase disclosure while simplifying the product, while our summary confirmation ensures greater understanding and improved communication between our funding partners and their customers.”

Example of the box:

Based in Jersey City, NJ, Yellowstone Capital has originated more than $2 billion to small businesses since inception.