Maxim Commercial Capital Funds Deals in 30 States During 2Q 2020

July 16, 2020Maxim Commercial Capital is pleased to report it funded hard asset-secured financings for small and mid-sized businesses (SMBs) in 30 states across the United States during the second quarter of 2020. After pivoting quickly in March to safer-at-home working conditions for its 30+ team members, Maxim experienced a steady increase in applications from equipment brokers and vendors for their borrowers with challenged credit. Maxim lends $10,000 to $3,000,000 to SMBs nationwide secured by heavy equipment and real estate to facilitate asset purchases, working capital and to refinance expensive short term debt.

“Maxim was founded during the Great Recession of 2008,” noted Behzad Kianmahd, Chairman and CEO. “We are applying our experiences gained during that time to overcome today’s extraordinary economic challenges and long term uncertainty caused by the COVID-19 pandemic. We have reaffirmed our commitment to finance SMBs, which are the backbone of our economy, refreshed our underwriting standards, and are continually improving our infrastructure by investing in technology and communication tools for the benefit of our customers, vendors, brokers and team members.”

During the second quarter, Maxim received numerous applications from business owners with strong credit but negative cash flow due to the economic downturn. Funded transactions for such borrowers included $95,000 secured by a 2019 Mack GR64F Tri-Axle Dump Truck for a growing landscaping company in New Jersey; $42,500 for a seasoned contractor’s purchase of a 2014 Caterpillar 312E Hydraulic Excavator; and, $29,000 to enable a business started up by seasoned contractors to purchase a 2020 Reinert ZR Concrete Pump.

Buyers of used class 8 trucks faced numerous challenges during the second quarter, ranging from lenders shutting down without warning to closed DMVs. Maxim successfully funded deals across the country, including $26,500 for a California-based long-haul truck owner-operator to purchase a 2017 Volvo 780; $20,800 for an Ohio-based transportation company to purchase a 2017 Freightliner Cascadia; and, $23,000 for a Texas-based owner-operator to purchase a 2016 Freightliner Cascadia to replace a truck with mechanical issues.

“We are humbled and encouraged by our team’s commitment to positively impact our customers’ future success, and by our customers’ continuous effort to make tough but rational decisions to stay in business during these difficult times,” commented Michael Kianmahd, Executive Vice President. “Based on our experience over the past few months, we are confident that SMBs across the nation will contribute substantially to the nation’s recovery from the biggest economic shock since The Great Depression.”

About Maxim Commercial Capital

Maxim Commercial Capital helps small and mid-sized business owners seize opportunity by providing financing in amounts up to $3,000,000 secured by heavy equipment and real estate. Maxim facilitates equipment purchases, provides working capital and refinances debt for companies across all industries located nationwide. Through Maxim’s tailored financing programs, businesses unlock capital tied up in underleveraged assets, often replacing expensive short-term debt and daily repayment working capital loans with longer term capital. As a leading provider of transportation equipment finance, Maxim funds up to 75% of the acquisition cost of class 8 and class 6 trucks, trailers and reefers for owner-operators and small businesses. Learn more at www.maximcc.com or by calling 877.776.2946.

Ready Capital Was The Biggest PPP Lender By Volume in Round 1 of PPP Funding

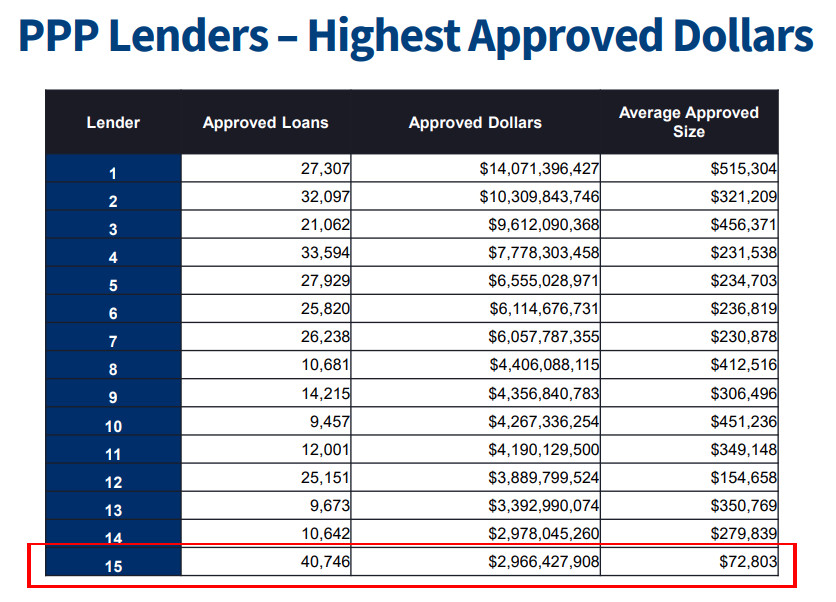

April 22, 2020 Ready Capital, a multi-strategy real estate finance company and one of the largest non-bank SBA lenders in the country, was the top PPP lender by loan volume in the country. Company CEO Thomas Capasse appeared on Fox Business yesterday and announced key statistics that aligned with data published by the SBA. By dollars, Ready Capital was the 15th largest PPP lender.

Ready Capital, a multi-strategy real estate finance company and one of the largest non-bank SBA lenders in the country, was the top PPP lender by loan volume in the country. Company CEO Thomas Capasse appeared on Fox Business yesterday and announced key statistics that aligned with data published by the SBA. By dollars, Ready Capital was the 15th largest PPP lender.

“As a leading non-bank, SBA lender, there’s 14 of us, we’re number two in terms of originations last year,” Capasse said on Fox Business, “we focused broadly, we don’t have deposit relationships, so we open our doors broadly to in particular the smaller mom and pop, the local deli, the pizzeria, the nail salon, so just in terms of the numbers, round one of the PPP, we approved 40,000 loans which is number one in the US, it was about $3 billion in total approvals. And our average balance was only $73,000 versus $230,000 for the average in round one.”

Among Ready Capital’s channels for acquiring PPP loan applications is Lendio, who reported consistent figures (a rough average of $80,000 per PPP loan facilitated), and high volume. Lendio has said on social media that they have been working with several partners, Ready Capital among them.

Ready Capital’s Capasse reasoned that their speed could probably be attributed to an affiliated fintech lender. “We are maybe more efficient than some of the banks because we have an affiliated fintech lender which is able to create online portals and processes to work in a more efficient manner and that enabled us to not only process these loans more efficiently but also to provide broad access to the program, to the smaller business owners.”

The company acquired Knight Capital, a small business finance provider, late last year.

A Q&A With Viceland’s Host Of ‘Hustle’ John Henry

March 5, 2020 Entrepreneur and investor John Henry, who also hosted TV show ‘Hustle‘ on Viceland, recently spoke with AltFinanceDaily Chief Editor Sean Murray about his experience as a young successful entrepreneur (Q&A is below). Henry will be a special guest speaker at Broker Fair 2020 on May 18th in New York City. YOU WON’T WANT TO MISS IT!!!

Entrepreneur and investor John Henry, who also hosted TV show ‘Hustle‘ on Viceland, recently spoke with AltFinanceDaily Chief Editor Sean Murray about his experience as a young successful entrepreneur (Q&A is below). Henry will be a special guest speaker at Broker Fair 2020 on May 18th in New York City. YOU WON’T WANT TO MISS IT!!!

—–

About John Henry

Voted to Forbes’ 30 Under 30 and Ebony’s Power 100 lists – John Henry is a Dominican-American entrepreneur and investor. Henry started his first business at 18, an on-demand dry cleaning service for the Film and TV industry in New York City, with clients such as The Wolf of Wall Street, Boardwalk Empire, Power, and more. Henry led the company through its acquisition in 2014 — founding and selling his first business by the age of 21. On the heels of his first win, Henry launched Cofound Harlem — a non-profit incubator that aims to foster a robust tech ecosystem North of 96th street in New York City. Cofound Harlem has launched numerous high-growth companies in Harlem, gaining recognition from Fast Company, TechCrunch, Business Insider, and more. He is a former Partner at Harlem Capital, a diversity-focused early stage venture capital firm on a mission to change the face of entrepreneurship. Henry is also the host of VICELAND’s latest show, HUSTLE, which is Executive Produced by Alicia Keys and focused on helping scrappy entrepreneurs grow their business to the next level.

—–

Q (Sean Murray): You started your first business at 18 but what made you want to start one?

A (John Henry): It was driven by necessity more than a desire to be an entrepreneur, but I did exhibit some of the traits that pushed me towards that path. Entrepreneurs tend to have a history of non-conformity where there’s no pre-chartered path and in an environment that demands conformity, anyone that likes to express their own views comes up against a lot of friction. So, for me it was necessity but also part of my character to do things differently.

Q: What kind of lessons did you learn from running a business at such a young age?

A: It’s a serious game and it’s full of responsibility. I was telling myself at one point that I was just 18 and so the struggles I faced running a business could be overlooked because of my age, but the world doesn’t care how old you are. If you’re running a business, there’s no way around the responsibilities it demands.

The other thing is, when you come up against really tough situations, you need to be brave and have courage to go through those moments. I’m glad I had the courage in them. Once you take them head-on, you come out feeling better on the other side.

Q: As a former partner of a Venture Capital firm, what’s the #1 mistake you saw entrepreneurs and business owners make?

A: You’ve got to have macro understanding and micro-chops. Everything is connected, it’s not just knowing your business but knowing where you’re situated in the economic or market cycle and understanding what customer sentiment is. That’s what a lot of entrepreneurs miss. Like if your idea is to make a mobile app, that’s great, but how many apps are already out there? How long have apps been part of the market already? What’s going to make your app stand out from every other app? And this doesn’t apply just to startups, but also existing companies. Every 3 months, you should be asking yourself the business question and evolve if necessary. The hardest part though is when your gut is telling you you’re right but every other person out there is telling you you’re wrong. And that’s something you’ll really have to figure out.

Q: Why has helping minority entrepreneurs and businesses been so important to you?

A: I’m not usually asked why, but I was seeing less and less minority representation among entrepreneurs that were receiving capital. There are some systemic factors that make it harder to get ahead but at the same time people can become inclusive to the point where they’re becoming exclusive. So, I think it’s about helping those that are on their way to overcoming tremendous odds to get far.

Q: Real estate, what can you tell me about your foray into that market?

A: I can say it’s the best business that I have been in so far. Real estate is the #1 fundamental building block of wealth. When I first got into it, I was shocked that you could put down 20% and the bank would put in the other 80%. This is a game of physical assets and I’m glad I came across it when I did. I’m currently building a bedrock of business around real estate, my preference being residential multi-family apartments.

Funding Metrics Deal Puts Them On The Map

March 4, 2020 A new $100 million revolving credit facility is poised to give a big boost to small business funding provider Funding Metrics. The company operates the Lendini and QuickFix Capital brands, and this new credit facility comes as the company seeks to increase its base of more than 9,500 small businesses served so far.

A new $100 million revolving credit facility is poised to give a big boost to small business funding provider Funding Metrics. The company operates the Lendini and QuickFix Capital brands, and this new credit facility comes as the company seeks to increase its base of more than 9,500 small businesses served so far.

“We now have the money to grow over all aspects of that spectrum,” President Jim Carnes said. Since 2014, the company has provided more than $500 million dollars of funding to small businesses in a variety of industries, including healthcare, real estate, construction, restaurants and others.

The $100 million worth of revolving credit comes from what the company called a “a multi-billion dollar institutional credit fund,” with Brean Capital serving as Funding Metrics’ exclusive financial advisor for the transaction. The new credit line as well as a newly developed website and streamlined funding process will allow for growth and fantastic customer service. Among the company’s main ideals is to provide funding request approvals or denials within three hours or less.

One of the main challenges for online small business funding and its related activities in 2020, said Funding Metrics co-founder David Frascella, is increasing awareness of all the offers and products out there, including from his company. “There are plenty of options in today’s market,” he said. Increasing that awareness, he added, is something the industry should come together to better address. “We look forward to additional submissions from the ISO network and funding the next wave of small business leaders nationwide,” he said.

Funding Metrics is also a platinum sponsor of Broker Fair 2020 on May 18th in New York City.

2020 and Beyond – A Look Ahead

March 3, 2020 With the doors to 2019 firmly closed, alternative financing industry executives are excited about the new decade and the prospects that lie ahead. There are new products to showcase, new competitors to contend with and new customers to pursue as alternative financing continues to gain traction.

With the doors to 2019 firmly closed, alternative financing industry executives are excited about the new decade and the prospects that lie ahead. There are new products to showcase, new competitors to contend with and new customers to pursue as alternative financing continues to gain traction.

Executives reading the tea leaves are overwhelming bullish on the alternative financing industry—and for good reasons. In 2019, merchant cash advances and daily payment small business loan products alone exceeded more than $20 billion a year in originations, AltFinanceDaily’s reporting shows.

Confidence in the industry is only slightly curtailed by certain regulatory, political competitive and economic unknowns lurking in the background—adding an element of intrigue to what could be an exciting new year.

Here, then, are a few things to look out for in 2020 and beyond.

Regulatory developments

There are a number of different items that could be on the regulatory agenda this year, both on the state and federal level. Major areas to watch include:

- Broker licensing. There’s a movement afoot to crack down on rogue brokers by instituting licensing requirements. New York, for example, has proposed legislation that would cover small business lenders, merchant cash advance companies, factors, and leasing companies for transactions under $500,000. California has a licensing law in place, but it only pertains to loans, says Steve Denis, executive director of the Small Business Finance Association. Many funders are generally in favor of broader licensing requirements, citing perceived benefits to brokers, funders, customers and the industry overall. The devil, of course, will be in the details.

- Interest rate caps. Congress is weighing legislation that would set a national interest rate cap of 36%, including fees, for most personal loans, in an effort to stamp out predatory lending practices. A fair number of states already have enacted interest rate caps for consumer loans, with California recently joining the pack, but thus far there has been no national standard. While it is too early to tell the bill’s fate, proponents say it will provide needed protections against gouging, while critics, such as Lend Academy’s Peter Renton, contend it will have the “opposite impact on the consumers it seeks to protect.”

- Loan information and rate disclosures. There continues to be ample debate around exactly what firms should be required to disclose to customers and what metrics are most appropriate for consumers and businesses to use when comparing offerings. This year could be the one in which multiple states move ahead with efforts to clamp down on disclosures so borrowers can more easily compare offerings, industry watchers say. Notably, a recent Federal Reserve study on non-bank small business finance providers indicates that the likelihood of approval and speed are more important than cost in motivating borrowers, though this may not defer policymakers from moving ahead with disclosure requirements.

“THIS WILL DRIVE COMMISSION DOWN FOR THE INDUSTRY”

If these types of requirements go forward, Jared Weitz, chief executive of United Capital generally expects to see commissions take a hit. “This will drive commission down for the industry, but some companies may not be as impacted, depending on their product mix, cost per lead and cost per acquisition and overall company structure,” he says.

- Madden aftermath. The FDIC and OCC recently proposed rules to counteract the negative effects of the 2015 Madden v. Midland Funding LLC case, which wreaked havoc in the consumer and business loan markets in New York, Connecticut, and Vermont. “These proposals would clarify that the loan continues to be ‘valid’ even after it is sold to a nonbank, meaning that the nonbank can collect the rates and fees as initially contracted by the bank,” says Catherine Brennan, partner in the Hanover, Maryland office of law firm Hudson Cook. With the comments due at the end of January, “2020 is going to be a very important year for bank and nonbank partnerships,” she says.

- Possible changes to the accredited investor definition. In December 2019, the Securities and Exchange Commission voted to propose amendments to the accredited investor definition. Some industry players see expanding the definition as a positive step, but are hesitant to crack open the champagne just yet since nothing’s been finalized. “I would like to see it broadened even further than they are proposed right now,” says Brett Crosby, co-founder and chief operating officer at PeerStreet, a platform for investing in real estate-backed loans. The proposals “are a step in the right direction, but I’m not sure they go far enough,” he says.

Precisely how various regulatory initiatives will play out in 2020 remains to be seen. Some states, for example, may decide to be more aggressive with respect to policy-making, while others might take more of a wait-and-see approach.

“I think states are still piecing together exactly what they want to accomplish. There are too many missing pieces to the puzzle,” says Chad Otar, founder and chief executive at Lending Valley Inc.

As different initiatives work their way through the legislative process, funders are hoping for consistency rather than a patchwork of metrics applied unevenly by different states. The latter could have significant repercussions for firms that do business in multiple states and could eventually cause some of them to pare back operations, industry watchers say.

“While we commend the state-level activity, we hope that there will be uniformity across the country when it comes to legislation to avoid confusion and create consistency” for borrowers, says Darren Schulman, president of 6th Avenue Capital.

Election uncertainty

The outcome of this year’s presidential election could have a profound effect on the regulatory climate for alternative lenders. Alternative financing and fintech charters could move higher on the docket if there’s a shift in the top brass (which, of course, could bring a new Treasury Secretary and/or CFPB head) or if the Senate flips to Democratic control.

If a White House changing of the guard does occur, the impact could be even more profound depending on which Democratic candidate secures the top spot. It’s all speculation now, but alternative financers will likely be sticking to the election polls like glue in an attempt to gain more clarity.

Election-year uncertainty also needs to be factored into underwriting risk. Some industries and companies may be more susceptible to this risk, and funders have to plan accordingly in their projections. It’s not a reason to make wholesale underwriting changes, but it’s something to be mindful of, says Heather Francis, chief executive of Elevate Funding in Gainesville, Florida.

“Any election year is going to be a little bit volatile in terms of how you operate your business,” she says.

Competition

The competitive landscape continues to shift for alternative lenders and funders, with technology giants such as PayPal, Amazon and Square now counted among the largest small business funders in the marketplace. This is a notable shift from several years ago when their footprint had not yet made a dent.

This growth is expected to continue driving competition in 2020. Larger companies with strong technology have a competitive advantage in making loans and cash advances because they already have the customer and information about the customer, says industry attorney Paul Rianda, who heads a law firm in Irvine, Calif.

It’s also harder for merchants to default because these companies are providing them payment processing services and paying them on a daily or monthly basis. This is in contrast to an MCA provider that’s using ACH to take payments out of the merchant’s bank account, which can be blocked by the merchant at any time. “Because of that lower risk factor, they’re able to give a better deal to merchants,” Rianda says.

Increased competition has been driving rates down, especially for merchants with strong credit, which means high-quality merchants are getting especially good deals—at much less expensive rates than a business credit card could offer, says Nathan Abadi, president of Excel Capital Management. “The prime market is expanding tremendously,” he says.

Certain funders are willing to go out two years now on first positions, he says, which was never done before.

Even for non-prime clients, funders are getting more creative in how they structure deals. For instance, funders are offering longer terms—12 to 15 months—on a second position or nine to 12 months on a third position, he says. “People would think you were out of your mind to do that a year ago,” he says.

Because there’s so much money funneling into the industry, competition is more fierce, but firms still have to be smart about how they do business, Abadi says.

Meanwhile, heightened competition means it’s a brokers market, says Weitz of United Capital. A lot of lenders and funders have similar rates and terms, so it comes down to which firms have the best relationship with brokers. “Brokers are going to send the deals to whoever is treating their files the best and giving them the best pricing,” he says.

Profitability, access to capital and business-related shifts

Executives are confident that despite increased competition from deep-pocket players, there’s enough business to go around. But for firms that want to excel in 2020, there’s work to be done.

Funders in 2020 should focus on profitability and access to capital—the most important factors for firms that want to grow, says David Goldin, principal at Lender Capital Partners and president and chief executive of Capify. This year could also be one in which funders more seriously consider consolidation. There hasn’t been a lot in the industry as of yet, but Goldin predicts it’s only a matter of time.

“A lot of MCA providers could benefit from economies of scale. I think the day is coming,” he says.

He also says 2020 should be a year when firms try new things to distinguish themselves. He contends there are too many copycats in the industry. Most firms acquire leads the same way and aren’t doing enough to differentiate. To stand out, funders should start specializing and become known for certain industries, “instead of trying to be all things to all businesses,” he says.

Some alternative financing companies might consider expanding their business models to become more of a one-stop shop—following in the footsteps of Intuit, Square and others that have shown the concept to be sound.

Sam Taussig, global head of policy at Kabbage, predicts that alternative funding platforms will increasingly shift toward providing more unified services so the customer doesn’t have to leave the environment to do banking and other types of financial transactions. It’s a direction Kabbage is going by expanding into payment processing as part of its new suite of cash-flow management solutions for small businesses.

“Customers have seen and experienced how seamless and simple and easy it is to work with some of the nontraditional funders,” he says. “Small businesses want holistic solutions—they prefer to work with one provider as opposed to multiple ones,” he says.

Open banking

This year could be a “pivotal” year for open banking in the U.S., says Taussig of Kabbage. “This issue will come to the forefront, and I think we will have more clarity about how customers can permission their data, to whom and when,” he says.

Open banking refers to the use of open APIs (application program interfaces) that enable third-party developers to build applications and services around a financial institution. The U.K. was a forerunner in implementing open banking, and the movement has been making inroads in other countries as well, which is helping U.S. regulators warm up to the idea. “Open banking is going to be a lively debate in Washington in 2020. It’ll be about finding the balance between policymakers and customers and banks,” Taussig says.

The funding environment

While there has been some chatter about a looming recession and there are various regulatory and competitive headwinds facing the industry, funding and lending executives are mostly optimistic for the year ahead.

“If December 2019 is an early indicator of 2020, we’re off to a good start. I think it’s going to be a great year for our industry,” says Abadi of Excel Capital.

How Hot Is The Legal Cannabis Industry?

February 24, 2020 One gauge of the commercial excitement over legal weed, medical marijuana and cannabis’s byproducts could be witnessed at the Las Vegas Convention Center in early December where the Marijuana Business Conference & Expo was overflowing with 31,523 attendees.

One gauge of the commercial excitement over legal weed, medical marijuana and cannabis’s byproducts could be witnessed at the Las Vegas Convention Center in early December where the Marijuana Business Conference & Expo was overflowing with 31,523 attendees.

Appealing to that audience—roughly the population of Juneau, Alaska—were more than 1,300 exhibitors who hailed from 79 different countries and touted products and services as varied as advancements in crop cultivation, medicinal breakthroughs, and innovative consumer products like marijuana-laden pastry.

Appealing to that audience—roughly the population of Juneau, Alaska—were more than 1,300 exhibitors who hailed from 79 different countries and touted products and services as varied as advancements in crop cultivation, medicinal breakthroughs, and innovative consumer products like marijuana-laden pastry.

That’s some 30% more than the 1,000 vendors who packed into the Central Hall in 2018 and about double the 678 who were showing off their wares in the smaller North Hall two years ago, reports Chris Day, vice president for external relations at Denver-based Marijuana Business Daily, which follows the cannabis industry and sponsored the Las Vegas trade show.

“In December, 2019,” Day declares, “we did not have to turn people away because we expanded. We had enough room for exhibitors but we needed both halls.” Unable to resist a boast, he adds: “We’ve been the fastest-growing trade show in the country three years running.”

One face in the December crowd was seasoned financial broker Scott Jordan, the Denver-based managing director of the Alternative Finance Network. He was occupying a booth accompanied by two attractive female models in fetching T-shirts emblazoned with the message: “How much would you borrow at zero percent?”

The young ladies’ arresting appearance and the message worked to the extent that “it got people talking,” Jordan says. As for the zero-interest rate, it’s not exactly free money. “I’ve got a product that puts together a line of credit,” he explains, “and after they receive the line of credit, it charges them a fee.”

As a broker, Jordan does the spade work of poring through a cannabis business’s financial statements and business model before he tees up a deal—typically between $250,000 and $750,000—to “a cadre” of 35 lenders in 10 states. He’ll ascertain whether the best funding option should be structured as equipment leasing, a working-capital loan, a revolving line of credit, project financing, or a real estate loan.

One recent cannabis deal that Jordan midwifed involved a “post-revenue, pre-profitability” manufacturing and processing company headquartered in Colorado. The financing, which closed in April, 2019, involved a pair of four-year term loans: one for $400,000 to refinance existing machinery, and a second for an additional $500,000 to acquire new laboratory equipment. Both credits carried interest rates in the “mid-teens,” he says, and were secured by the equipment.

Once the debt financing was in place, the manufacturing operation was “fully functioning,” Jordan reports, paving the way for the company to raise $30 million in venture capital financing. Jordan argues that “even if they pay a 10-20 percent interest rate, it’s better to preserve equity and finance through a normal type of loan. If you need an extraction machine or packaging equipment,” he adds, “why give up equity if you can finance it through debt?”

Jordan’s reasoning appears to sit well with clients and funders alike. Since 2014, he has brokered 85 transactions worth $33 million. He reckons that two out of three deals that he takes to funders meet with success. “My best year was 2015 because there were only a few competitors and I was the only guy on the block,” he says.

As the country steadily decriminalizes and legalizes pot, however, early market entrants like Jordan no longer have the cannabis business all to themselves. Thirteen states have legalized recreational marijuana for adults. These include California, Colorado, Oregon, Washington and Nevada in the West; Illinois and Michigan in the Midwest; and Massachusetts, Vermont and Maine in the East. Hawaii and Alaska permit it and, if you’re over 21, you can legally grow, smoke or ingest weed in the District of Columbia, but it cannot be sold commercially.

An additional 24 states have approved medical marijuana. While research on cannabis’s medicinal properties remains thin—largely because of objections by federal law enforcement—it is being prescribed for a range of maladies, including cancer, glaucoma, epilepsy, Crohn’s Disease, multiple sclerosis, nausea, and pain. [“The marijuana plant contains more than 100 different chemicals called cannabinoids,” according to WebMD. “Each one has a different effect on the body. Delta-9- tetrahydrocannabinol (THC) and cannabidiol (CBD) are the main chemicals used in medicine. THC also produces the ‘high’ people feel when they smoke marijuana or eat foods containing it.”]

Industry data assembled by MJBizDaily reflects both the broad acceptance of legal cannabis use and its increasing commercial popularity. U.S. revenues from legal weed and its byproducts are expected to clear $16.4 billion this year, a 40% growth rate over the $11.75 billion in estimated revenues for 2019. The legal cannabis industry now employs about 200,000 persons in the U.S., about the same number as flight attendants (120,000) and veterinarians (80,00) combined.

For more evidence that the cannabis market is hot look no further than the state of Illinois, where recreational marijuana went on sale Jan. 1, 2020. The Prairie State’s governor also pardoned some 11,000 citizens with criminal records for possession and the sale of low levels of marijuana.

For more evidence that the cannabis market is hot look no further than the state of Illinois, where recreational marijuana went on sale Jan. 1, 2020. The Prairie State’s governor also pardoned some 11,000 citizens with criminal records for possession and the sale of low levels of marijuana.

“We’re showing that sales were close to $3.2 million on the first day of 2020,” says MJBiz’s Day. “Illinois is the big story right now,” he adds. “Anytime a new state opens up in the market, you’re seeing enormous pent-up demand and enthusiasm.”

Even as the cannabis industry takes giant strides toward public acceptance, the plant continues to face hostility from the U.S. federal government, which has criminalized its use for 80 years. Marijuana remains classified by the Drug Enforcement Agency as a Schedule 1 drug, keeping company with heroin, LSD and Ecstasy.

Even as the cannabis industry takes giant strides toward public acceptance, the plant continues to face hostility from the U.S. federal government, which has criminalized its use for 80 years. Marijuana remains classified by the Drug Enforcement Agency as a Schedule 1 drug, keeping company with heroin, LSD and Ecstasy.

That designation has also made it hard for the cannabis industry to engage in simple financial transactions, much less obtain financing. “Despite the majority of states’ having adopted cannabis regimes of some kind, federal law prevents banks from banking cannabis businesses,” Joanne Sherwood, president and chief executive at Citywide Banks, a $2.3 billion-asset bank headquartered in Denver, testified to Congress last summer. “The Controlled Substances Act,” added Sherwood, who is chair of the Colorado Bankers Association, “classifies cannabis as an illegal drug and prohibits its use for any purpose. For banks, that means that any person or business that derives revenue from a cannabis firm is violating federal law and consequently putting their own access to banking services at risk.”

And despite the herculean efforts by the cannabis industry to soften its image, obtaining financing from traditional sources like pension funds, insurance companies and university endowments remains a daunting proposition as well, says David Traylor, senior managing director at Golden Eagle Partners. His four-person, boutique investment fund, which makes equity investments in up-and-coming cannabis companies, relies on wealthy individuals and family offices for the bulk of its funds.

“Capital is hard to come by for this industry,” Traylor says. “From day one, most venture capitalists have been staying out of it. It’s still illegal in many states and their limited partners are endowments like Harvard and Yale, which see marijuana as the antithesis of education.”

Sarah Sanger, chief financial officer at Oak Investment Funds, a real estate investment firm based in Oakland, says: “There’s a great deal of economic activity in California but it’s stymied by the lack of financing and difficulty with changing regulations. It provides an opportunity for really expensive debt from private investors willing to do due diligence.”

That absence of establishment financing has opened up a plethora of opportunities for alternative funders, and not just in agriculture and plant cultivation. While agriculture represents the bedrock of the industry there is no downstream product, of course, without the cannabis leaf— growing and harvesting cannabis is just one stage of the industry’s life cycle.

MJBiz’s Day notes, for example, that that the legal cannabis industry is regulated for safety, so growers must show that “the flower has no molds or contaminants.” That means that crops are subject to rigorous testing and decontamination, which requires both materials and expertise. To process the leaf and develop “infused products” by extracting cannabis-based oils entails the purchase and deployment of costly technology. Packaging and labeling along with tracking systems that, Day says, “are stricter than in other places” are also key components of the farm-to-market supply chain.

Meanwhile, in an ongoing effort to appeal to a fresh cohort of customers, Jordan notes, the cannabis industry continues to develop innovative uses for the plant. “There are so many applications and new products that keep appearing, like ice cream with marijuana, vaporizers, inhalers, and syrup,” he says. “Now, there are mints—something I hadn’t seen before—and different ways to ingest the product and get high and not look like a druggie.”

Jordan Fein, chief executive at Greenbox Capital in Miami, says his firm prefers to fund downstream companies selling cannabis products. “We do agricultural lending but it’s less attractive and harder to qualify the business. It’s not as tangible as a retail business which will have a website and product reviews. The same goes for edibles.”

Jordan Fein, chief executive at Greenbox Capital in Miami, says his firm prefers to fund downstream companies selling cannabis products. “We do agricultural lending but it’s less attractive and harder to qualify the business. It’s not as tangible as a retail business which will have a website and product reviews. The same goes for edibles.”

Recent Greenbox Capital deals in 2019, Fein says, included one with merchant cash advances of $80,000 and $60,000 in growth capital to a Colorado dispensary. The operation put the money to work adding two retail outlets during the year, he says, bringing to four its total number of storefronts. In addition to cannabis flower, the dispensary sells “edibles, tinctures, lotions, and wax concentrates,” Fein reports. Both short term cash advances require regular ACH payments.

Greenbox Capital also made a $135,000 cash advance to a cannabis-testing laboratory in Southern California in August, 2019 for the purchase of sophisticated equipment. The company, he says, is doing $140,000-a-month in revenue and cashflow is strong and on the rise.

“Greenbox is always interested in higher risk deals,” Fein says, noting that banking services remain off limits to legal cannabis firms. “But we fund them for the same reason we fund lawyers and auto sales—things that most others will not do. There’s nothing wrong with risk,” he adds, “as long as you clearly assign a proper value to the deal and price to it.”

Steve Sheinbaum, a New York broker and chief executive at Circadian Funding, has unabashedly climbed aboard the cannabis bandwagon. “The market is exploding and it’s attractive to lenders because it’s a product people can put their hands on,” he says. “If I’m dealing with a grower, I can leverage real estate and usually there’s equipment. If they’re producing, there’s inventory and I can look at the income statement to see what kind of cash flow the business is generating.”

He recently brokered a $10 million loan for a licensed grower and distributor of medicinal marijuana in New England with monthly revenues of $3-$4 million. The credit bore a 17% annual percentage rate and a six-year maturity, he says. The deal was brought to Circadian by a private equity investor who was looking to grow the enterprise tenfold. The deal, which was interest-only, was secured by a second position on real estate and a lien on the borrower’s license. “The lender was comfortable with the interest-only loan,” Sheinbaum explains. “They can refinance in six years.”

He recently brokered a $10 million loan for a licensed grower and distributor of medicinal marijuana in New England with monthly revenues of $3-$4 million. The credit bore a 17% annual percentage rate and a six-year maturity, he says. The deal was brought to Circadian by a private equity investor who was looking to grow the enterprise tenfold. The deal, which was interest-only, was secured by a second position on real estate and a lien on the borrower’s license. “The lender was comfortable with the interest-only loan,” Sheinbaum explains. “They can refinance in six years.”

In another recent deal, Circadian arranged an unsecured merchant cash advance for $300,000 to a Pacific Northwest technology company developing specialty, point-of-sale software for the cannabis industry. The firm showed monthly revenues of $300,000.

“It’s not federally permitted for cannabis firms to take payments from Visa, Mastercard or American Express,” Sheinbaum explains. “But this technology company is using debit or credit cards to pay for cryptocurrency which is stored on a prepaid card which customers can then use to purchase cannabis.”

The tech company had been struggling to find money and Sheinbaum took satisfaction in a deal announcement that went out in an e-mail to the industry. “Funding complicated deals is what gets our blood flowing,” Sheinbaum wrote. “Anyone can get a restaurant or dentist funded. No one needs help with that.”

Manny Columbie, a Miami-based senior funding manager at H&J Capital Group, an Orlando firm, reports funding agricultural and dispensary businesses in California, Colorado and Washington State. In the Evergreen State, he says, he recently provided funding to a woman who owned a marijuana-themed café connected to a cannabis dispensary. The deal went through after examining her recent bank statements and two years of federal tax returns.

“The best thing about lending to people in this industry is their ability to repay,” Columbie says. “They’re never lacking in funds.”

He provided more detail on a deal currently in the works involving a physician in Irvine, California, with an 800-plus credit score from the rating agency Experian and personal tax returns showing $2 million in annual income. The doctor, Columbie says, has been making transdermal patches infused with THC in addition to his medical practice and needs specialized equipment to lower his manufacturing costs to 55 cents per patch. The patches sell for $40-$60 apiece, Columbie says, depending on the THC content.

If the deal goes through and is approved by H&J’s credit committee, the physician would likely be extended a $350,000 loan with a 10-year maturity secured by the Chinese-manufactured equipment. Factoring in the doctor’s excellent credit and other positives, the interest rate on the credit could be as low as 5%-7%.

While the environment for legal cannabis seems to grow more favorable by the day, market participants urge funders to remain circumspect. One remaining fly in the legal cannabis ointment has been the persistence of an illegal black market. Estimates are that as much as 60% to 80% of the marijuana market in California is illicit, says Craig Behnke, an equity analyst at MJBiz.

Law-abiding businesses must also contend with overbearing regulators and high taxation. The California Department of Fee and Tax Administration recently jacked up its excise tax on cannabis to 80%, effective on Jan. 1, 2020.

And the state’s constabulary isn’t helping matters either, notes Sanger of Oak Funds. “There are going to be a lot of operators that end up being losers because of the regulatory environment,” she says. “Law enforcement is using all of its resources to make sure legitimate businesses are following the rules instead of clamping down on black market activity. That makes it harder for legitimate retailers to make money because people are still shopping in the black market.”

The recent collapse of the shares of publicly traded Canadian cannabis companies, which some blame in part on the illicit competition from the black market, also stands as a cautionary sign. Last August, the Motley Fool listed ten “Pot Stocks”—including Canopy Growth and Aurora Cannabis, both of which are listed on the New York Stock Exchange—that together lost a stunning $20 billion in market capitalization.

The drubbing that heedless investors have taken in the Canadian stocks reminds analyst Behnke of the debacle in dotcom stocks back in 2001-2002, but with a big difference. “The dotcoms were a brand-new invention and people had no idea how big the Internet companies would be,” he told AltFinanceDaily. “But cannabis has been around for a thousand years. I feel like it was a shame on investors and the companies. This shouldn’t have happened.”

Pacific Equity And Loan Acquires Emerald Capital Funding

January 12, 2020 This week Pacific Equity & Loan, a hard money lender based in Washington state, acquired Emerald Capital Funding. Done to “provide more resources and investment opportunity to real estate investors in the Washington market,” according to a statement from PEL, the merger will see all of ECF’s staff move over to PEL.

This week Pacific Equity & Loan, a hard money lender based in Washington state, acquired Emerald Capital Funding. Done to “provide more resources and investment opportunity to real estate investors in the Washington market,” according to a statement from PEL, the merger will see all of ECF’s staff move over to PEL.

“The move comes amid a rapidly evolving mortgage industry in specifically the private money and hard money lending sector,” ECF’s President and Founder Christopher Robinson commented. “We need to stay ahead of the curve and assure that our customer receive the best value, the best technology, and continue to work with a trusted local lender.”

Speaking to AltFinanceDaily, Sang Yoon, PEL’s Director of Business Development and Co-founder said that he was excited to move forward, noting that it’s a “two heads are better than one situation. By merging or acquiring a company, we are better able to service our customers.”

Fears of Possible Recession Don’t Phase CRE Lenders

December 16, 2019 Depending on your vantage point, a slowdown is either already in progress, just around the bend or several years away. But some alternative commercial real estate professionals are trying to filter out the noise.

Depending on your vantage point, a slowdown is either already in progress, just around the bend or several years away. But some alternative commercial real estate professionals are trying to filter out the noise.

Instead, they are more aggressively forging ahead with growth plans, including trying to grab market share from banks.

The commercial real estate lending market remains highly competitive and alternative lenders say they remain focused on looking for opportunities to expand their business, even as the possibility of recession looms. At present, a number of professionals don’t see an imminent threat of recession, and even if there is one, they say they stand to benefit from picking up business banks don’t want to take on—or can’t—because of increased regulatory controls imposed on them since the last recession.

There are plenty of opportunities for alternative commercial real estate lenders to get ahead, even in this environment, says Chris Hurn, founder and chief executive of Fountainhead Commercial Capital, a Lake Mary FL-based, non-bank direct small business lender in the commercial real estate lending space.

To be sure, alternative commercial real estate lenders say that for the most part, there hasn’t been a major pullback in their space. But due in part to mounting economic concerns and changing business priorities, banks—which had already scaled back from their pre- Great Recession exuberance—have been taking an even more cautious approach to lending. This is especially true in certain regions of the country, or in sectors deemed higher-risk such as hospitality and retail, alternative lenders say. While the pullback hasn’t been broad-based, it’s been enough in some cases to create strategic pockets of opportunity for opportunistic non-bank lenders such as private equity funds, debt funds, crowdfunding portals and others.

To be sure, alternative commercial real estate lenders say that for the most part, there hasn’t been a major pullback in their space. But due in part to mounting economic concerns and changing business priorities, banks—which had already scaled back from their pre- Great Recession exuberance—have been taking an even more cautious approach to lending. This is especially true in certain regions of the country, or in sectors deemed higher-risk such as hospitality and retail, alternative lenders say. While the pullback hasn’t been broad-based, it’s been enough in some cases to create strategic pockets of opportunity for opportunistic non-bank lenders such as private equity funds, debt funds, crowdfunding portals and others.

For many of these commercial real estate professionals, whether or not a recession is on the horizon is not a guessing game that’s worth playing. And with good reason, given how much disagreement there is among market watchers, investment management professionals and others about where the economy is headed.

Certain economic data continues to be strong, for instance, but political and geopolitical factors such as trade wars continue to raise red flags. Then there’s the fatalistic notion that the economy has been on a tear for so long that it’s due for a pullback at some point. This all translates into a hodgepodge of speculation and indecision about the economy’s direction. The dichotomy is evident from the difference in sentiment expressed in two fund manager surveys from Bank of America Merrill Lynch taken a month apart. October’s survey was decidedly bearish; by November, the bulls were back, muddying the waters even more.

Instead of wavering in indecision, however, some alternative commercial real estate players are hunkering down and highly focused on building their business in a cautiously optimistic and strategic manner.

Hurn of Fountainhead Commercial Capital predicts a number of increased opportunities for alternative commercial real estate lenders due to pullback from banks and a growing need for capital. He cautions alternative lenders against being too pessimistic and losing out on potentially lucrative market opportunities as a result.

“I think we might be going into a period of slightly slower growth, but none of the indicators suggest we’re remotely close to where things were 10 years ago,” Hurn says. “If we’re not careful, we’re going to talk our way into recession. It’s a self-fulfilling prophecy.”

Indeed, even as perplexing questions about the economy’s long-term health persist, some alternative commercial lenders anticipate growth in the coming year. Evan Gentry, chief executive and founder of Money360, a tech-enabled direct lender specializing in commercial real estate, says the company’s loan origination business is on track to close between $650 million and $700 million in 2019. That’s expected to increase to about $1 billion in 2020, fueled by growth in some strategic markets, including Washington DC, Atlanta, Miami and Charlotte, N.C., where the company is seeking to add loan origination personnel. Gentry says the company also continues to experience strength in many of the western markets, including the intermountain west markets of Colorado, Utah and Idaho, where growth is expected to continue.

CommLoan, a commercial real-estate lending marketplace in Scottsdale, Ariz., also sees strategic opportunities to grow in this environment. Mitch Ginsberg, the company’s co-founder and chief executive, predicts 2020 will be a strong growth year for his company, after a several-year beta period. CommLoan has plans, for example, to start hiring account executives to build relationships in additional states. Initially, the focus will be on institutions in the Southwestern U.S., with plans to add lenders in Texas, Utah, Colorado and New Mexico in the early part of 2020, Ginsberg says.

Though certain regions or business lines within commercial real estate may be experiencing some pullback, he says his overall outlook for the economy and commercial real estate remains strong. “There is still an enormous amount of activity,” he says. “If and when a correction does happen, it’s going to be a lot softer and not that deep and not that long because of the fundamentals in the economy.”

FINDING WAYS TO COMPETE MORE EFFECTIVELY WITH BANKS AND OTHERS

Some commercial real estate professionals say they are focusing more attention on sectors, regions and concentrations that the banks aren’t going after so readily.

If an alternative lender can offer more money than a bank on a particular deal or offer more flexible terms, or do deals that traditional lenders simply won’t do, for example, then it’s a boon for them. For a slightly higher price, alternative lenders—especially those whose business model relies heavily on technology—are able to take on slightly riskier deals than a bank might be able to stomach, says Jacob Goldsmith, managing partner of Goldwolf Ventures LLC, a privately held alternative investment and asset management company with offices in Miami and Austin.

“Alternative lenders are a lot more nimble,” says Goldsmith, who keeps close tabs on the commercial real estate lending industry.

Especially given the ambiguous economic climate, there are several areas that could be prime opportunities for savvy alternative commercial real estate lenders to gain a leg up. For instance, some banks of late have shied away from certain special purchase property types like hotels, day care facilities and free-standing restaurants, says Hurn of Fountainhead Commercial Capital. These types of properties are traditionally seen as riskier in the latter part of an economic cycle.

Especially given the ambiguous economic climate, there are several areas that could be prime opportunities for savvy alternative commercial real estate lenders to gain a leg up. For instance, some banks of late have shied away from certain special purchase property types like hotels, day care facilities and free-standing restaurants, says Hurn of Fountainhead Commercial Capital. These types of properties are traditionally seen as riskier in the latter part of an economic cycle.

Nonetheless, “there’s opportunity here for non-traditional lenders to step in and fill that gap,” he says. Retail loans are another category where banks have been pulling back. One reason banks are being more cautious is the sentiment that as online shopping becomes more pervasive, there’s less of a need for brick-and-mortar shops. This trend is underscored by the recent announcement of Transform Holdco—the company formed to buy the remaining assets of bankrupt retailer Sears Holdings Corp.—that it would close 96 Sears and Kmart stores by the end of February. Still, some industry watchers aren’t ready to concede retail’s demise.

While these types of announcements fan fears, concern over the death of retail is largely overblown, according to Troy Merkel, a partner and real estate senior analyst at RSM, which provides audit, tax and consulting services. “The banks are being too overly cautious,” he opines.

The opportunity for alternative lenders, he says, is not in funding loans that add to the supply, but rather in funding loans that change the existing supply. While the need for new development may not be as great, there is a growing demand for repurposed properties, he says. This includes upscaling an older mall or turning an existing retail building into a mixed use property, namely a mix of retail stores and multi-family apartment complexes. There is still a real need for these types of developments, Merkel says, and with banks shying away, the door is open for alternative lenders to “make a play,” he says.

Real estate professionals say they also see opportunities for alternative commercial real estate lenders to make loans in areas outside major metro cities, where the competition isn’t as strong.

“There will always be opportunities in the ups and downs, the ebbs and flows of the cycle. You just have to be a lot smarter in this part of the cycle,” says Goldsmith of Goldwolf Ventures.

BECOMING RECESSION-PROOF

Pockets of opportunity notwithstanding, alternative commercial real estate lenders have to play it smart, professionals say. For instance, they should not be overly bullish on a particular sector or throw caution to the wind when it comes to their underwriting practices.

That’s because when the market turns—as it inevitably will at some point—there will likely be more defaults and lenders that haven’t dotted their I’s and crossed their T’s will understandably face stronger headwinds. They need to keep their close eye on expenses as well, which may have ticked upward over the past several years. “People get complacent when times are good. This is probably not the time to be complacent anymore,” says Hurn of Fountainhead Commercial Capital.

Another protective measure against an eventual downturn is to diversify sales channels and property types. “If you put too many eggs in one basket, it’s a problem,” Hurn says.

It’s also important for lenders to have their guards up since higher risk deals can lead to losses if a recession hits. Lenders have to be smart when it comes to taking on risk, says Tim Milazzo, co-founder and chief executive of StackSource, an online marketplace for commercial real estate loans. “They have to have a certain expertise in underwriting these transactions correctly and assessing risk,” Milazzo says.

It’s also important for lenders to have their guards up since higher risk deals can lead to losses if a recession hits. Lenders have to be smart when it comes to taking on risk, says Tim Milazzo, co-founder and chief executive of StackSource, an online marketplace for commercial real estate loans. “They have to have a certain expertise in underwriting these transactions correctly and assessing risk,” Milazzo says.

In light of significant ambiguity about where the economy is heading, Gentry of Money360 says his company is protecting itself by taking an ultra- conservative approach. This means, for instance, only making first-lien position loans secured against income producing properties at a loan-to-value ratio on average of 65 percent, he says. Some alternative lenders are making these loans at a loan-to-value ratio of 80 percent or 85 percent, but Gentry says this is too high a rate for his taste. Also, Money360’s loans are also generally short- term—in the two-to-three-year range, which reduces some of the risk and seems especially prudent at this point in the cycle, he says.

When the market turns—as it inevitably will at some point—there will be more loan defaults, and those that are on the more aggressive end of lending will bear most of the challenges, he says.

He cautions other alternative lenders to avoid taking on excessive risk. “You’ve got to be thinking ahead and planning and lending as if the downturn is right around the corner—because it could be,” he says. Even taking a conservative approach, there are still significant business opportunities, he says.

BE ON THE LOOKOUT FOR RECESSIONARY OPPORTUNITIES

Meanwhile, if a recession does hit, alternative commercial real estate lenders say they will have even more opportunities to gain market share, participate in workout financing and hire key personnel. Alternative lenders that are more steeped in technology may potentially have even more of an upper hand since this can enable them to close deals much more efficiently and quickly and at a lower cost, while at the same time giving borrowers broader access.

“In a tighter market, every reduction in rate and cost will make more of a significant difference to borrowers than it does at the moment,” says Ginsberg of CommLoan, the commercial real-estate lending marketplace.

Although there are a growing number of alternative commercial real estate lenders who are relying more heavily on technology than they did in the past, commercial real estate lending still hasn’t flourished online to the extent personal and small business lending has. One reason is that the loans are larger and human intervention is often seen as beneficial, says Gentry of Money360.

However, online lending within the commercial real estate lending space is still on the horizon, according to Ginsberg of CommLoan. “It’s slow-go, but it’s inevitable,” he says.