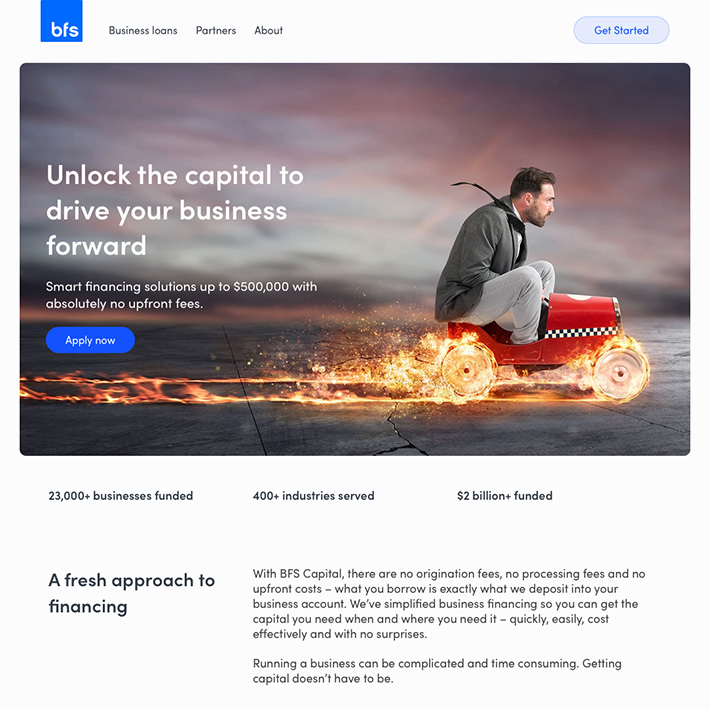

BFS Capital Eliminates Upfront Fees to Simplify Financing for Small Business Owners

October 1, 2019 CORAL SPRINGS, FLA. (Oct. 1, 2019)—BFS Capital, a leader in small business financing, today announced it has eliminated all upfront fees on its financing solutions, including loans and business advances, as it simplifies pricing for small business owners.

CORAL SPRINGS, FLA. (Oct. 1, 2019)—BFS Capital, a leader in small business financing, today announced it has eliminated all upfront fees on its financing solutions, including loans and business advances, as it simplifies pricing for small business owners.

With pricing that is transparent, flexible and easy to understand, BFS Capital is leading the evolution of small business financing. BFS Capital customers can now apply for and receive up to $500,000 in financing with no origination fees, no processing fees and no upfront costs. Customers are able to pay back a loan with a fixed daily or weekly payment, or as a flexible payment calculated as a percentage of credit card sales.

“There will be no hidden costs or unexpected surprises. What customers borrow is what gets funded into their accounts,” said BFS Capital CEO Mark Ruddock. “We are committed to empowering small businesses by meeting their needs with straightforward, cost-effective and timely online financing, whether it be to smooth cash flow, invest in adding staff, purchase equipment or upgrade a space.”

BFS Capital is also preparing to roll out a new, state-of-the-art digital lending platform. Over the next few weeks, the BFSCapital.com website will showcase a refreshed brand and exciting advances in automation across the entire loan application and approval process.

BFS Capital is also preparing to roll out a new, state-of-the-art digital lending platform. Over the next few weeks, the BFSCapital.com website will showcase a refreshed brand and exciting advances in automation across the entire loan application and approval process.

Partners, including Independent Sales Organizations (ISOs) that match small businesses to BFS Capital’s financing solutions, will also benefit from the company’s new no fee product proposition, evolving digital capabilities and dedication to transparency. ISOs and partners will soon have real-time visibility into the status of their leads across the entire customer relationship lifecycle, from the initial application through the life of the loan and beyond.

“As we embark on our mission of reimagining small business financial services, we are reinforcing support for our partners with API integration and faster, fully underwritten personalized offers, all complemented by market-leading pricing and commissions,” Ruddock added.

BFS Capital has over a decade long history of helping small business owners thrive and has provided more than $2 billion in financing. To qualify, businesses must be in operations for at least two years and generate at least $12,000 in monthly revenue. More than 23,000 businesses have been funded by BFS Capital across 400 industries.

To learn more, please visit BFSCapital.com.

About BFS Capital

BFS Capital champions the long-term growth and prosperity of small businesses by providing timely, flexible financing solutions. BFS Capital’s leading small business financing platform leverages customized underwriting and proprietary algorithms to fund businesses in the United States, Canada, and through its United Kingdom subsidiary, Boost Capital. Since 2002, BFS Capital has provided over $2 billion in total financing to over 23,000 small businesses across more than 400 industries. Headquartered in South Florida with offices in New York, California and the United Kingdom, BFS Capital is an accredited BBB company with an A+ rating.

Media Contact

Archie Group for BFS Capital

Gregory Papajohn

gregory@archiegroup.com

917.287.3626

Prominent Attorney Criminally Charged In 1 Global Capital Mess

September 17, 2019 Another individual has been criminally charged in connection with the 1 Global Capital securities case. 74-year-old Jan Douglas Atlas, a securities attorney, was charged with 1 count of securities fraud by the US Attorney in South Florida on Tuesday for authoring opinion letters in 2016 that falsely described that the investments were not securities nor subject to federal securities laws or registration requirements.

Another individual has been criminally charged in connection with the 1 Global Capital securities case. 74-year-old Jan Douglas Atlas, a securities attorney, was charged with 1 count of securities fraud by the US Attorney in South Florida on Tuesday for authoring opinion letters in 2016 that falsely described that the investments were not securities nor subject to federal securities laws or registration requirements.

The charges allege that Atlas “came to understand” that individuals representing 1 Global were not interested in accurate legal advice based on real facts and that they instead wanted false legal cover that would advance the desired outcome to continue to profit from 1 Global. He allegedly made false and misleading statements despite knowing the true nature of how the investments worked and that they were in fact securities as defined under federal securities laws.

“Atlas’s opinion letters were used and relied upon by 1 Global employees and agents to continue to raise money illegally,” the Department of Justice said in an announcement.

Atlas was also compensated by receiving a percentage of the commissions generated from the fundraising scheme to the tune of $627,000 paid to his personal checking account. These payments were not disclosed to his employer, Kopelowitz Ostrow, as required.

Atlas was also separately charged by the SEC.

His employer was not charged with any wrongdoing in either action. Atlas was previously listed as a partner at the firm but is no longer on the firm’s website.

Atlas is the second individual to be criminally charged in connection with 1 Global Capital. The first individual, Alan Heide, who served as 1 Global Capital’s CFO, pleaded guilty to conspiracy to commit securities fraud. He is scheduled to be sentenced on December 12th.

Stripe Ventures Into Merchant Cash Advance Financing

September 6, 2019 Stripe, a payments firm lauded as the world’s most valuable private fintech company (at $22.5B), has officially launched a merchant cash advance product.

Stripe, a payments firm lauded as the world’s most valuable private fintech company (at $22.5B), has officially launched a merchant cash advance product.

Dozens of news outlets have announced that the company is providing loans, but that’s not all, AltFinanceDaily has learned. Both loans and merchant cash advances are available.

The company’s FAQ page originally explained the “Capital” product as a merchant cash advance but it’s since been updated to reflect that they offer access to both merchant cash advances and loans. An official Stripe spokesperson also clarified that an offer could be an MCA or a loan. The updated FAQ says that funding terms would be available in the customer dashboard, in the funding contract, and that which one a customer qualifies for depends on the specifics of their business.

Stripe merchant account customers can find out if they’re eligible for funding in their dashboard. If they’re not, they can still send Stripe a note through the dashboard to signal that they’re interested, say how much they’re looking for, and select what they plan to do with the funds. Stripe says they will not review your credit report and that all offers are based solely on Stripe transaction history.

The new product will not disrupt the separate integration with Funding Circle, according to a statement provided to Digital Transactions. Stripe customers can still apply to Funding Circle by connecting their Stripe account. Funding Circle offers term loans that range from six months to five years.

Stripe’s MCA product is currently only available in the US, but the company’s founders, Patrick and John Collison, brothers, hail from an unlikely place, rural Ireland. The company handles tens of billions of dollars in payments a year across 34 countries.

Like other recent entrants into the small business funding space, Stripe’s advantage is its ability to tap into its existing customer base. Other payments companies such as PayPal and Square, for example, were among the top four largest originators (for which public data is available) of alternative small business funding in 2018.

Note: This article has been updated to reflect the changes made on Stripe’s website as well as an additional clarification from the company.

Gold Rush: Merchant Cash Advances Are Still Hot

August 18, 2019

Last year, when Kevin Frederick struck out on his own to form his own catering company in Annapolis, the veteran caterer knew that he’d need a food trailer for his business to succeed.

He reckoned that he had a good case for a $50,000 small-business loan. The Annapolis-based entrepreneur boasted stellar personal credit, $30,000 in the bank, and a track record that included 35 years of experience in his chosen profession. More impressively, his newly minted company—Chesapeake Celebrations Catering—was on a trajectory to haul in $350,000 in revenues over just eight months of operations in 2018. And, after paying himself a salary, he cleared $60,000 in pre-tax profit.

But Frederick’s business-credit profile was so thin that no bank or business funder would talk to him. So woeful was his lack of business credit, Frederick reports, that his only financing option was paying a broker a $2,000 finder’s fee for a high-interest loan.

Luckily, he says, everything changed when he discovered Nav, an online, credit-data aggregator and financial matchmaker.

Based in Utah, Nav had him spiff up his business credit with Dun & Bradstreet, a top rating agency and a Nav business partner. This was accomplished with a bankcard issued to Frederick’s business by megabank J.P. Morgan Chase. Soon afterward, he says, Nav steered him to Kapitus (formerly Strategic Funding Source), a New York-based lender and merchant cash advance firm that provided some $23,000 in funding.

“They led me in the right direction,” Frederick says of Nav. “A lady there (at Nav) helped me with my credit, warning me that the credit card I’d been using had an effect on my personal credit. Then she led me to Kapitus, all probably within a week.”

Now, Frederick has his food trailer. He reports that its total cost—$14,000 for the trailer, which came “with a concession window, mill-finished walls, and flooring” plus $43,000 in renovations—amounted to $57,000. Equipped with a full kitchen—including refrigeration, sinks, ovens, and a stove—the food trailer can be towed to weddings, reunions, and the myriad parties he caters in the Delmarva Peninsula. In addition, Frederick can also park the trailer at fairgrounds and serve seafood, barbeque, and other viands to the lucrative festival market.

Now, Frederick has his food trailer. He reports that its total cost—$14,000 for the trailer, which came “with a concession window, mill-finished walls, and flooring” plus $43,000 in renovations—amounted to $57,000. Equipped with a full kitchen—including refrigeration, sinks, ovens, and a stove—the food trailer can be towed to weddings, reunions, and the myriad parties he caters in the Delmarva Peninsula. In addition, Frederick can also park the trailer at fairgrounds and serve seafood, barbeque, and other viands to the lucrative festival market.

Meanwhile, the caterer’s funders are happy to have him as their new customer. The people at Kapitus, to whom he is making daily payments (not counting weekends and holidays), are especially grateful. “Nav provides a valuable service,” says Seth Broman, vice-president of business development at Kapitus. “They know how to turn coal into diamonds,”

Nav does not charge small businesses for its services. As it gathers data from credit reporting services with which it has partnerships—Experian, TransUnion, Dun and Bradstreet, Equifax—and employs additional metrics, such as cashflow gleaned from an entrepreneur’s bank accounts, Nav earns fees from credit card issuers, lenders and MCA firms.

The company has close ties to financial technology companies that include Kabbage and OnDeck, and also collaborates with MCA funders such as National Funding, Rapid Finance, FundBox, and Kapitus. “We give lenders and funders better-qualified merchants at a lower cost of client acquisition,” says Caton Hanson, Nav’s general counsel and co-founder, adding: “They don’t have to spend as much money on leads.”

As banks have increasingly shunned small-business lending in the decade since the financial crisis, and as the economy has snapped back with a prolonged recovery, alternative funders—particularly unlicensed companies offering lightly regulated, high-cost merchant cash advances (MCAs)—have been piling into the business.

And service companies like Nav—which is funded by nearly $100 million in venture capital and which reports aiding more than 500,000 small businesses since it was founded in 2012—are thriving alongside the booming alternative-funding industry.

Over the past five years, the MCA industry’s financings have been growing by 20% annually, according to 2016 projections by Bryant Park Capital, a Manhattan-based, boutique investment bank. BPC’s specialty finance division handles mergers and acquisitions as well as debt-and-equity capital raising across multiple industries and is one of the few Wall Street firms with an MCA-industry practice. By BPC’s estimates, the MCA industry will have more than doubled its small business funding to $19.2 billion by year- end 2019, up from $8.6 billion in 2014.

Bankrolled by a broad assortment of hedge funds, private equity firms, family offices, and assorted multimillionaire and billionaire investors on the qui vive for outsized returns on their liquid assets, the MCA industry promises a 20%-80% profit rate, reports David Roitblat, president of Better Accounting Solutions, a New York accountancy specializing in the MCA industry. Based on doing the books for some 30 MCA firms, Roitblat reports that the range in profit margins depends on the terms of contracts and a funder’s underwriting skills.

The numerical size and growth of the MCA industry is hard to ascertain, reports Sean Murray, editor of AltFinanceDaily (this publication), which tracks trends in the industry and sponsors several major conferences. “So much is anecdotal,” Murray says.

Even so, the evidence that MCA companies are proliferating—and prospering—is undeniable. Over the past two years, AltFinanceDaily’s events, which experience substantial attendance from the MCA industry, have consistently sold out, requiring the events to be moved to larger venues. In Miami, attendance in January this year topped 400-plus attendees, Murray reports, roughly double the crowd that packed the Gale Hotel in 2018.

Similarly, the May, 2019, Broker Fair in New York at the Roosevelt Hotel drew more than 700 participants compared with the sellout crowd of roughly 400 last year in Brooklyn. (Despite ample notice that this year’s Broker Fair at the Roosevelt was sold out and advance tickets were required, as many as 40-50 latecomers sought entry and, unfortunately, had to be turned away.)

The upsurge of capital and the swelling number of entrants into the MCA business has all the earmarks of a gold rush. “Everybody and his brother is trying to get a piece of the action,” asserts Roitblat, the New York accountant.

And there are two ways to hit paydirt in a gold rush. One way is to prospect for gold. But another way is to sell picks and shovels, tents, food, and supplies to the prospectors. “If you can find a way to service the gold rush, you can make a lot of money,” says Kathryn Rudie Harrigan, a management professor and business-strategy expert at the Columbia University Graduate School of Business. “It’s like profiteering in wartime.”

And there are two ways to hit paydirt in a gold rush. One way is to prospect for gold. But another way is to sell picks and shovels, tents, food, and supplies to the prospectors. “If you can find a way to service the gold rush, you can make a lot of money,” says Kathryn Rudie Harrigan, a management professor and business-strategy expert at the Columbia University Graduate School of Business. “It’s like profiteering in wartime.”

As Professor Harrigan suggests, cashing in on the gold rush by servicing it has parallels across multiple industries. Consider the case of Charles River Laboratories, which has capitalized on the rapid development of the biotechnology industry over the past few decades.

As scientists searched for biologics to battle diseases like cancer and AIDS, the Boston-area company began producing experimental animals known as “transgenic mice.” Informally known as “smart mice,” Charles River’s test animals are specially designed to carry human genes, aiding investigators in their understanding of gene function and genetic responses to diseases and therapeutic interventions. (The smart mouse’s antibodies can also be harvested. “Seven out of the eleven monoclonal antibody drugs approved by the Food and Drug Administration between 2006 and 2011,” according to biotechnology.com, “were derived from transgenic mice.”)

In the MCA version of the gold rush, a bevy of law and accounting firms, debt-collection agencies and credit-approval firms, among other service providers, have either sprung to life to undergird the new breed of alternative funder or added expertise to suit the industry’s wants and needs. (This cohort has been joined, moreover, by a superstructure of Washington, D.C.-based trade associations and lobbyists that have been growing like expansion teams in a professional sports league. But their story will have to wait for another day.)

Rather than being exploitative, supporting companies serve as a vital mainstay in an industry’s ecosystem, notes Alfred Watkins, a former World Bank economist and Washington, D.C.-based consultant: “A gold miner can’t mine,” he says, “unless he has a tent and a pickaxe.”

And in the high-risk, high-reward MCA industry, which can have significant default rates depending on the risk model, many funders can’t fund if they don’t have reliable debt collection. Many of the bigger companies, says Paul Boxer, who works on the funding side of the industry, have the capability of collecting on their own. But for many others—particularly the smaller players in the industry—it’s necessary to hire an outside firm.

One of the more widely known collectors for the MCA industry is Kearns, Brinen & Monaghan where Mark LeFevre is president and chief executive. The Dover (Del.)- based firm, LeFevre says, first added MCA funders to its client roster in 2012; but it has only been since 2014 that “business really took off.”

LeFevre won’t say just how many MCA firms have contracted with him, but he estimates that his firm has scaled up its staff 35%-40% over the past five years to meet the additional MCA workload. The industry, LeFevre adds, “is one of the top-growth industries I’ve seen in the 36 years that I’ve been in business.”

He also says, “People in the MCA industry know a lot about where to put money, but collections are not one of their strong points. They need to get a professional. It gives them the free time to make more money while we go in behind them and collect.”

If repeated dunning fails to elicit a satisfactory response, KBM has several collection strategies that strengthen its hand. The big three, LeFevre says, are “negotiation, identifying assets, and litigation.” He adds: “We have a huge database of attorneys who do nothing but file suit on commercial debt internationally. Then we can enforce a judgment. You don’t want someone who just makes a few phone calls.”

Because business has become so competitive, LeFevre says, he won’t discuss his fee schedule. As to KBM’s success rate, he says no tidy figure is available either, but asserts: “Our checks sent to our clients are more than most agencies because of our proprietary collection process.”

Jordan Fein, chief executive at Greenbox Capital in Miami and a KBM client told AltFinanceDaily: “We work with them. They’re organized and communicate well and they know to collect. They’re on the expensive side, though. I’ve got other agencies that I use that are cheaper.”

Debt-collection firm Merel Corp, a spinoff from the Tamir Law Group in New York, might be a lower-cost alternative. Formed in just the past 18 months to service the growing MCA industry, Merel typically takes 15%-25% of whatever “obligation” it can collect, says Levi Ainsworth, co-chief operating officer.

A successful collection, Ainsworth asserts, really begins with the underwriting process and attention to detail by the funders. “Instead of coming in at the end,” he says, “we try to prevent problems at the start of the process.”

For an MCA firm dealing with an excessive number of defaults, Merel sometimes places one of its employees with the funder to handle “pre-defaults,” for which it charges a lower fee. The collections firm has also built a reputation for not relying on a “confession of judgment.” Now that COJs have been outlawed for out-of-state collections in New York State, Merel’s skills could be more in demand.

Better Accounting Solutions, which has its offices on Wall Street, is another service-provider promising to lighten the workload of MCA firms by providing back-office support. The company is headed by Roitblat, a 36-year- old former rabbinical student turned tax-and-accounting entrepreneur. Since he founded the company with two part-time employees in 2011, it’s ballooned to some 70 employees.

Roitblat does not have all of his firm’s eggs in one MCA basket. His firm handles tax, accounting and bookkeeping work for law firms, the fashion industry, restaurants and architectural firms. Even so, he says, thirty MCA clients— or more than half his clientele—rely on the firm’s expertise, three of whom were just added in June. His best month was January, 2018, when six funders contracted for his services. “Growth in the MCA industry has been explosive,” he says.

MCA accounting work has its own vagaries and oddities. For example, because of the industry’s high default rate, Roitblat notes, a 10%-slice of every merchant’s payment is funneled into a “default reserve account.” And when an actual default occurs, credits are moved from the receivables account to the default reserve account.

Roitblat takes pride that his firm’s MCA work has passed audits from respected accounting firms like Friedman, Cohen, Taubman and Marcum LLP. Moreover, he has helped clients uncover internal fraud and, in one instance, spotted costly flaws in a business model. An early MCA client, Roitblat says, had no idea that “he was losing close to $100,000 a month by spending on Google ads.”

Better Accounting also keeps its rates low. The firm typically assigns a junior accountant to handle clients’ accounts while a senior manager oversees his or her work. “He (Roitblat) does a fantastic job,” says David Lax, managing partner of Orange Advance, a Lakewood (N.J.)-based MCA firm. “They understand the MCA business. And even if your business is small, they can set up the infrastructure and do the work more economically and efficiently than you can. You’d have to create the position of comptroller or senior-level accountant,” Lax adds, “to equal their work.”

Top-notch competence and low rates, Lax says, are not the only reasons he often refers Roitblat’s firm to fellow MCA companies. “The only thing better than their work,” he says, “is the people themselves.”

Whether it’s oil and gas, banking and real estate, construction, health care or high-technology—you name it—lawyers have an important role across nearly every industry. So too with the MCA industry where, as has been shown, there is an especially high demand for attorneys skilled at winning debt-collection cases.

To hear Greenbox’s Fein tell it, a skilled lawyer handling debt collection can write his or her own ticket. A talented attorney, he says, not only retrieves lost money and prevents losses, but enables the funder to “offer the product cheaper than the competition.

“We use a ton of attorneys in 35 states in the U.S. and in Canada,” Fein adds, “and you have no idea how many attorneys we go through until we find a good one.”

Until recently, much of the MCA industry’s success has resulted from a hands-off, laissez faire legal and regulatory environment—particularly the legal interpretation that a merchant cash advance is not a loan. The industry has also benefited from the fact that most credit regulation focused on consumer credit and not on business and commercial financings.

But now, as the MCA industry is maturing and showing up on the radar screens of state legislatures, Congress, regulatory agencies, and the courts, there is heightening demand for legal counsel. In just the past 12 months, California passed a truth-in-lending statute requiring MCA firms not only to clearly state their terms, but to translate the short-term funding costs of MCAs into an annual percentage rate. The state of New York, as has been noted, passed legislation restricting the use of COJs.

Moreover, notes Mark Dabertin, special counsel at Pepper Hamilton, a top national law firm based in Philadelphia, the state of New Jersey is contemplating licensing MCA practitioners. The Minnesota Court of Appeals recently determined in Anderson v. Koch that, because of a “call provision” in a funding contract, a merchant cash advance was actually a loan.

And, Dabertin warns, the Federal Trade Commission, which has the authority to treat a merchant cash advance as a consumer transaction—replete with the full panoply of consumer disclosures and protections—is training its gunsights on the industry. “On May 23,” Dabertin reports in a memo to clients, “the FTC launched an investigation into potentially unfair or deceptive practices in the small business financing industry, including by merchant cash advance providers.”

These pressures from government and the courts will only make doing business more costly and drive up the industry’s barriers to entry. Failing to stay legal, moreover, could not only result in punitive court judgments, but render an MCA firm vulnerable to legal action by their investors.

“It’s inevitable that the industry will evolve,” Dabertin says, and firms in the industry will have to self-police. “They will need to hire counsel and a compliance staff,” he adds. “You can’t just do it by the seat of your pants.”

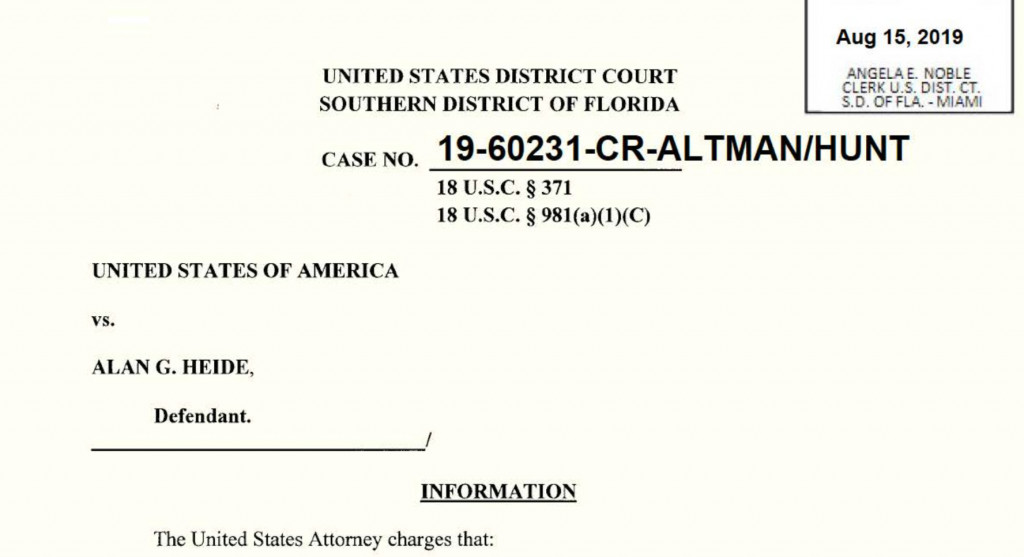

Alan Heide, CFO Of 1 Global Capital, Hit With Criminal Charge & SEC Violations

August 15, 2019

Update: Alan Heide has pleaded guilty to one count of conspiracy to commit securities fraud.

The former CFO of 1 Global Capital, Alan Heide, was stacked with bad news on Thursday. The US Attorney’s Office for the Southern District of Florida lodged criminal charges against him at the same time the Securities & Exchange Commission announced a civil suit for defrauding retail investors.

Heide was criminally charged with conspiracy to commit securities fraud.

According to the criminal complaint:

It was a purpose of the conspiracy for the defendant and his conspirators to use false and fraudulent statements to investors concerning the operation and profitability of 1 Global, so that investors would provide funds to 1 Global, and continue to make false statements to investors thereafter so that investors would not seek to withdraw funds from 1 Global, all so that the conspirators could misappropriate investors’ funds for their personal use and enjoyment.

He is facing a maximum of 5 years in prison.

1 Global Capital CEO Carl Ruderman, who recently consented to judgment with the SEC, has not been charged criminally to-date. However, he is mentioned throughout the pleading against Heide as “Individual #1 who acted as the CEO of 1 Global.”

Civil charges were simultaneously lodged by the SEC.

According to the SEC’s complaint:

Although 1 Global promised investors profits from its short-term merchant cash advances to businesses, the company used substantial investor funds for other purposes, including paying operating expenses and funding Ruderman’s lavish lifestyle. The SEC alleges that Heide, a certified public accountant, for nine months regularly signed investors’ monthly account statements that he knew overstated the value of their accounts and falsely represented that 1 Global had an independent auditor that had endorsed the company’s method of calculating investor returns.

According to an SEC statement, Heide agreed to settle the SEC’s charges as to liability, without admitting or denying the allegations, and agreed to be subject to an injunction, with the court to determine the penalty amount at a later date.

1 Global Capital filed for bankruptcy last year after investigations by the SEC and US Attorney’s Office hampered their ability to raise capital. Ruderman’s recent settlement with the SEC put him on the hook for $50 million to repay investors.

SecurCapital Acquires Breakout Capital Finance’s Lending Business

July 17, 2019Supply chain and logistics company acquires the lending business of leading fintech small business lender and injects new equity capital

MCLEAN, VA — SecurCapital Corp, an expanding supply chain and financial services provider headquartered in California, today announced the acquisition of the lending business of Breakout Capital Finance, a leading fintech company and nationwide small business lender. SecurCapital is also providing additional equity capital to drive growth in Breakout Capital Finance’s two primary lending products: its highly regarded and innovative term loan product and its FactorAdvantage ® lending solution for small businesses that utilize factoring to finance their business. The acquired lending business assets will be operated by a subsidiary of SecurCapital that will conduct business as Breakout Capital.

Steve Russell, CEO of SecurCapital commented, “We’re delighted to have found a highly respected team and innovative business model in the small business finance space. I share the founder’s vision of the massive potential of the FactorAdvantage lending solution and believe we now have the platform and capital to rapidly grow this industry-changing product. We couldn’t have found a better business to complement SecurCapital’s strategic vision for empowering small businesses.” SecurCapital, through a series of strategic acquisitions, provides supply chain and financial services to small businesses primarily in the logistics industry, including veteran-and minority owned businesses.

Breakout Capital Finance’s Founder, Carl Fairbank added, “After four years as Founder and CEO of Breakout Capital Finance, this transaction begins the next chapter of Breakout Capital’s lending business. SecurCapital is also committed to the proliferation of best practices to drive change in the broader market. I believe Breakout Capital, in partnership with SecurCapital, is now well positioned for substantial growth, especially with its commitment to FactorAdvantage.” Mr. Fairbank will provide strategic guidance during the transition, but has stepped down as CEO of the lending business to focus on driving innovation in advanced technology, including artificial intelligence, machine learning, and blockchain.

Tim Buzby has been appointed as the new CEO of Breakout Capital. He spent 17 years at Farmer Mac, in executive positions culminating as CEO. Notably, he oversaw a 58% increase in company earnings and an almost 4x increase in stock price and strategically matured the company into an agricultural lending industry leader.

Breakout Capital has also hired McLean Wilson, former CEO of Charleston Capital, an asset manager in the SME space, and former CEO of inFactor, a factoring company, as Chief Credit Officer. Mr. Russell added, “With the appointment of Tim as CEO and the addition of McLean to the management team, we expect Breakout Capital not only to carry forward its role in the industry as product innovator and transparent lender but also to deliver financing solutions to a much broader range of small businesses.” Breakout Capital is committed to maintain the high ethical standards, best practices, APR-based disclosure, and competitive pricing for which it has always been known.

About Breakout Capital

Breakout Capital, headquartered in McLean, Virginia, has been and will continue to be a leading fintech company, offering innovative small business lending solutions across the country. As part of SecurCapital, Breakout Capital will remain committed to transparent and responsible lending solutions through product innovation, small business borrowing education, and advocacy against predatory lending practices and will continue to empower small business through right-sized lending, suitability testing, improving terms and supporting the long-term financing objectives of small businesses. Breakout Capital has been widely regarded as the “white-hat” lender in the alternative finance space and intends to retain that reputation as part of SecurCapital.

FOR ADDITIONAL INFORMATION:

Breakout Capital www.breakoutfinance.com

CONTACT:

Public Relations and Media Contact:

Phone: 703.852.6142

Email: info@breakoutfinance.com

About SecurCapital

SecurCapital is headquartered in greater Los Angeles, California with locations in San Diego, Atlanta, Baltimore and Washington, DC. SecurCapital provides supply chain financial services and proven advisory services to logistics businesses from a seasoned team of logistics and financing professionals. SecurCapital offers mid-tier and startup companies access to working capital, M&A consulting, technology enablement and mission critical services for all their supply chain needs. SecurCapital offers forwarders, truckers, custom brokers, 3PL, wholesalers, 4PL, suppliers, veteran owned small businesses (VOSB), minority owned enterprises and government contractors’ on-line access to a broad range of services.

Forward-Looking Statements Disclaimer: This press release contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. In some cases, you can identify forward-looking statements by the following words: “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “ongoing,” “plan,” “potential,” “predict,” “project,” “should,” “will,” “would,” or the negative of these terms or other comparable terminology, although not all forward-looking statements contain these words. Forward-looking statements are not a guarantee of future performance or results and will not necessarily be accurate indications of the times at, or by, which such performance or results will be achieved. Forward-looking statements are based on information available at the time the statements are made and involve known and unknown risks, uncertainty and other factors that may cause our results, levels of activity, performance or achievements to be materially different from the information expressed or implied by the forward-looking statements in this press release.

FOR ADDITIONAL INFORMATION:

SecurCapital Corp www.securcapital.com

CONTACT:

Public Relations and Media Contact:

Phone: 619-384-3359

Email: info@securcapital.com

Star Fundraiser For 1 Global Capital Settles With The SEC

July 15, 2019 Henry J. “Trae” Wieniewitz, III was charged by the SEC on Monday for his role in allegedly selling unregistered securities in two companies, 1 Global Capital (the now defunct merchant cash advance provider) and Woodbridge Group of Companies (a purported real estate lending business revealed to be a $1.2 billion ponzi scheme).

Henry J. “Trae” Wieniewitz, III was charged by the SEC on Monday for his role in allegedly selling unregistered securities in two companies, 1 Global Capital (the now defunct merchant cash advance provider) and Woodbridge Group of Companies (a purported real estate lending business revealed to be a $1.2 billion ponzi scheme).

“Wieniewitz and Wieniewitz Financial raised more than $11.4 million and reaped approximately $500,000 in commissions from unlawful sales of Woodbridge securities, and raised more than $53 million and obtained approximately $3 million in commissions from unlawful sales of 1 Global securities,” the SEC stated.

Wieniewitz was not a registered broker-dealer nor associated with a registered broker-dealer.

A settlement was announced simultaneously. “Wieniewitz and Wieniewitz Financial settled the SEC’s charges as to liability without admitting or denying the allegations, and agreed to be subject to injunctions, with the court to determine the amounts of disgorgement, interest, and penalties at a later date,” an SEC statement said.

Wieniewitz was not alone in selling investments in both 1 Global and Woodbridge.

Separately, the owner of Woodbridge and two former directors of the company were recently charged criminally.

No criminal charges have been brought to date in the 1 Global Capital saga. That could change. 1 Global Capital revealed in 2018 that it was being investigated by the US Attorney’s office. That along with the SEC investigation prompted the company to file for bankruptcy. The SEC subsequently brought civil charges.

Documents filed in the SEC case against 1 Global’s former owner, Carl Ruderman, have since revealed that at least one former employee had been approached by the FBI about the operations of 1 Global.

Last month, it appeared Ruderman and the SEC were heading towards a settlement.

One notable fact about 1 Global Capital is that the company participated in the largest merchant cash advance in history at $40 million. That transaction has become a point of significant controversy and litigation. The recipient of those funds, a conglomerate of car dealerships in California, have shut their doors.

Bitty Advance Opens Office in NYC

June 6, 2019

Bitty Advance has expanded to midtown Manhattan. The company’s first location, in Fort Lauderdale, FL, will remain intact as the corporate office.

“We wanted to have a New York presence to hire sales talent, underwriters and, of course, raise more capital because obviously this is the mecca for finance,” said CEO of Bitty Advance Edward Siegel.

Siegel said he is currently hiring salespeople and experienced underwriters for the New York office. There were about 10 well-dressed salespeople at the spacious Bitty Advance office in New York this morning, and Siegel said he plans to grow the office to about 20. He said there are 30 employees in Florida, none of whom moved to the New York office. The New York office does sales and underwriting, while the corporate office in Florida also handles sales and underwriting and houses the customer service and executive teams.

“We also wanted to have a presence in New York for our partners,” Siegel said.

Siegel’s partners include ISOs and other funders that don’t fund the smaller deals that Bitty Advance specializes in. Bitty Advance provides “micro advances” (from $2,000 to $10,000) to merchants doing less than $100,000 in revenue.

Siegel has another Florida-based funding company called Fundzio, and Bitty Advance launched in 2017 when Siegel recognized that almost 50% of online applications to Fundzio were coming from merchants doing less than $100,000 in revenue.

“I realized that the only proper way to do this was to create another company, carve out a niche, and build a team that was just focused on micro advances,” Siegel said.