Lendini is Back

September 2, 2020 Bensalem, PA –September 3, 2020– Lendini is excited to announce its return to small business funding. Through superior efficiency and analysis, the company has improved the process of alternative funding from some of the brightest minds in finance, technology and analytics. With updated (temporary COVID-19) guidelines, they remain dedicated and committed to their merchants and ISOs in these unprecedented times.

Bensalem, PA –September 3, 2020– Lendini is excited to announce its return to small business funding. Through superior efficiency and analysis, the company has improved the process of alternative funding from some of the brightest minds in finance, technology and analytics. With updated (temporary COVID-19) guidelines, they remain dedicated and committed to their merchants and ISOs in these unprecedented times.

Lendini works directly with you to prepare the best package for your client, whether that be a Business Cash Advance (BCA) or Merchant Cash Advance (MCA). Simply put, Lendini advances money based on the average monthly gross sales of a business or average monthly credit card sales. Money can be advanced quickly because securing assets and collateral is not required.

Get clients funded in 4 easy steps; application submission, information review, approval or denial, final review and your client is funded. Minimal documentation is required. The company must have 18 months in business with $7,500 per month in gross sales and an average daily balance of $750. We require a minimum of 5 deposits, monthly into the business bank account.

Funding Stipulations:

- Bank login

- Funding call with merchant

Required Documents:

- Application

- All 2020 business bank statements + MTD

- Signed and dated agreement

- Proof of business existence

- Meets state registration requirements

- Proof of ownership

- Merchant interview

- Driver’s license

- Voided check (starter checks will not be accepted)

Industries accepted:

- Restaurants (with takeout)

- Pharmacies

- Healthcare

- Manufacturing

- Transportation (freight)

- Healthcare (primary care)

- Automotive repair

- Grocery stores

With $540 million dollars funded to 15,000 small businesses, Lendini offers incomparable solutions customized specifically for your client. The company prides itself in being able to offer up to $300,000 in as little as 1 business day (in most cases). Funding can be used for any business purpose you may have.

Lendini is not a bank and does not provide loans, they offer cash advances. With Lendini, business owners receive the capital they need without lengthy delays or excessive paperwork. In general, Lendini offers pre-approvals in under three hours and next day funding of approved advances. The staff provides unparalleled customer service and treats each business owner with the respect they deserve.

Banks, Non-Banks, Fintech and More Came Through for Lendio on PPP, But it Wasn’t Easy

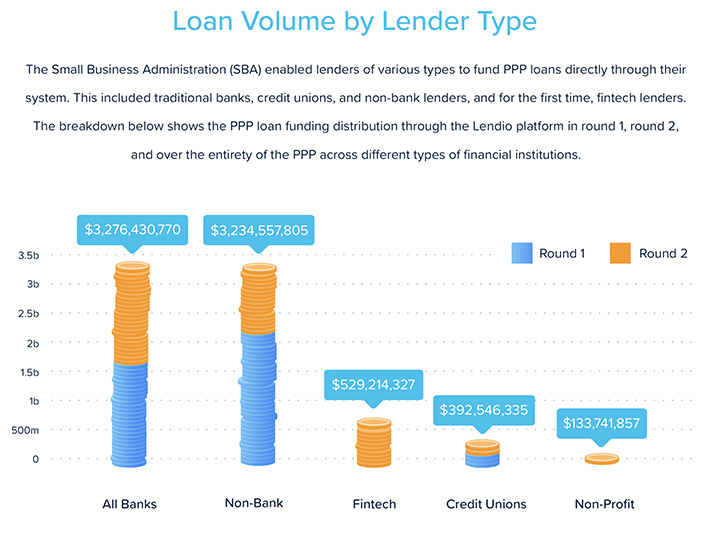

August 27, 2020 Last week, Lendio, a facilitator of small business loans, released a report analyzing the $8 billion of PPP loans that were approved through its lending platform. A coalition of more than 300 lenders was able to give aid, saving an estimated 1.1 million jobs, Lendio indicates.

Last week, Lendio, a facilitator of small business loans, released a report analyzing the $8 billion of PPP loans that were approved through its lending platform. A coalition of more than 300 lenders was able to give aid, saving an estimated 1.1 million jobs, Lendio indicates.

Through Lendio’s service, traditional banks approved the most funding at $3.3 billion- or about 44% of the PPP dollars on the platform. Though non-bank lenders secured the highest number of approvals at 50,264 transactions in lesser dollar amounts.

Fintech lenders funded 6% of the total loan volume through the platform.

Lendio was well situated to facilitate lending from institutions to those that needed help through funds provided by the SBA. Brock Blake, CEO, and co-founder of Lendio, said the company’s success in delivering on PPP was no accident— they had to remove all stops and almost bet on the success of the PPP program.

“Our mission at Lendio is normally ‘Fueling the American Dream’: helping the American business owner accomplish their dream,” Blake said. “We tweaked our mission during this timeframe to ‘Saving the American Dream.'”

Blake said while other companies were closing their doors and sending off employees on furlough, Lendio took on 250 new hires- and buckled down for thousands of hours of engineering work to overhaul their system. Not just loan sales, but legal processes, onboarding, training, and backend tech work had to be updated in just days.

This all came on fast, but so did the quarantine. Beginning in April, more than 100,000 business owners applied for economic relief under the PPP using Lendio’s online marketplace.

The demand for capital was outrageous.

“It was more demand in one weekend than the SBA had seen in the last 14 years combined,” Blake said. “We were helping these business owners that were watching their entire lifes’ work flushed down the drain in a matter of weeks, and they were desperate for capital.”

Lendio was finding that many institutions could simply not handle the volume, Blake said, and he knew if banks were only able to process loan requests for their current customers, there would be an exploding demand for loan processing. The company took on 100 new partners who needed help during this time.

“Our systems were tested to their limits, like 1000 times more pressure than we ever saw before,” Blake said. “Some partners of ours got so much demand they couldn’t handle it and turned off their spigot. So we scrambled to find lenders that would take on new customers.”

Though it was ten times more challenging than anything Blake has done in his career, it was ten times more satisfying. Lendio doubled the number of loans it has issued since 2011, and quintupled the dollar amount the platform facilitated in just four short months. Where are they going to go from here?

For one, Lendio is one company out of many that are hoping for another round of PPP funding. Blake said he is getting customer feedback all the time asking for help, dealing with quarantine regulation that is harming business, like restaurants that have nowhere to seat patrons.

Outside of PPP, Blake said that many of the 110,000 businesses they served are now applying for other loans, or using Lendio’s bookkeeping and loan forgiveness applications. Lendio is happy to help business owners and banks through this tough time by launching digital applications.

“Before, lenders across the country were requiring business owners to come into branches [with] paper applications,” Blake said. “Now, there’s not one business owner in America that wants to walk into a bank branch. The demand for lenders to go digital is as high as it’s ever been.”

CEO Of Online Lender Arrested For PPP Fraud

August 19, 2020 Sheng-wen Cheng, aka Justin Cheng, the CEO of Celeri Network, was arrested on Tuesday by the FBI. Celeri offers business loans, merchant cash advances, SBA loans, and student loans.

Sheng-wen Cheng, aka Justin Cheng, the CEO of Celeri Network, was arrested on Tuesday by the FBI. Celeri offers business loans, merchant cash advances, SBA loans, and student loans.

Cheng applied for over $7 million in PPP funds, federal agents allege, on the basis that Celeri Network and other companies he owns had 200 employees. In reality he only had 14 employees, they say.

Cheng succeeded in obtaining $2.8M in PPP funds but rather than use them for their intended lawful purpose, he bought a $40,000 Rolex watch, paid $80,000 towards a S560X4 Mercedes-Maybach, rented a $17,000/month condo apartment, bought $50,000 worth of furniture, and spent $37,000 while shopping at Louis Vuitton, Chanel, Burberry, Gucci, Christian Louboutin, and Yves Saint Laurent.

He also withdrew $360,000 in cash and/or cashiers checks and transferred $881,000 to accounts in Taiwan, UK, South Korea, and Singapore.

This, of course, is all according to the FBI. Statements made to Law360 indicate that Cheng maintains his innocence.

A press release published by Celeri late last year said that the company had raised $2.5M in seed funding that valued the company at $11M.

Where Fintech Ranks on the Inc 5000 List for 2020

August 12, 2020Here’s where fintech and online lending rank on the Inc 5000 list for 2020:

| Ranking | Company Name | Growth |

| 30 | Ocrolus | 7,919% |

| 46 | Yieldstreet | 6,103% |

| 351 | Direct Funding Now | 1,297% |

| 402 | GROUNDFLOOR | 1,141% |

| 486 | LoanPaymentPro | 946% |

| 534 | LendingPoint | 862% |

| 539 | OppLoans | 860% |

| 566 | dv01 | 830% |

| 647 | Fund That Flip | 724% |

| 1031 | Fundera | 449% |

| 1035 | Nav | 447% |

| 1053 | Fundrise | 442% |

| 1103 | Bitcoin Depot | 409% |

| 1229 | Smart Business Funding | 365% |

| 1282 | Global Lending Services | 349% |

| 1360 | CommonBond | 327% |

| 1392 | Forward Financing | 319% |

| 1398 | Fundation Group | 318% |

| 1502 | Fountainhead Commercial Capital | 293% |

| 1736 | Seek Capital | 246% |

| 1746 | PIRS Capital | 244% |

| 1776 | Braviant Holdings | 240% |

| 1933 | Choice Merchant Solutions | 218% |

| 2001 | Fundomate | 212% |

| 2257 | Lighter Capital | 185% |

| 2466 | Bankers Healthcare Group | 167% |

| 2501 | Fund&Grow | 165% |

| 2537 | Central Diligence Group | 162% |

| 2761 | Lendtek | 145% |

| 3062 | Shore Funding Solutions | 127% |

| 3400 | Biz2Credit | 110% |

| 3575 | National Funding | 103% |

| 4344 | Yalber & Got Capital | 76% |

| 4509 | Expansion Capital Group | 70% |

“A Bad Solution in Search of a Problem”: SBFA’s Response to the New York Disclosure Bill

August 6, 2020 “It’s actually shocking to me how tone deaf those who claim to represent our industry are when it comes to policy,” is how Steve Denis, Executive Director of the Small Business Finance Association, described the Innovative Lending Platform Association’s response to and influence over the drafting of bill A10118A/S5470B. Known as New York’s APR disclosure bill, S5470B has been passed by the state legislature, and if signed by Governor Cuomo, will require small business financing contracts to disclose the annual percentage rate as well as other uniform disclosures.

“It’s actually shocking to me how tone deaf those who claim to represent our industry are when it comes to policy,” is how Steve Denis, Executive Director of the Small Business Finance Association, described the Innovative Lending Platform Association’s response to and influence over the drafting of bill A10118A/S5470B. Known as New York’s APR disclosure bill, S5470B has been passed by the state legislature, and if signed by Governor Cuomo, will require small business financing contracts to disclose the annual percentage rate as well as other uniform disclosures.

Speaking to AltFinanceDaily over the phone, Denis expressed disappointment with both the bill as well as comments made by ILPA’s CEO, Scott Stewart, in a recent article.

“Small businesses in New York are struggling right now,” the Director noted. “They’re waking up every single day wondering if they should even stay open or close permanently, and companies and organizations in our space are using their resources to push a disclosure bill that nobody has asked for. There’s no widespread issue with disclosure. There’s been no outpouring of complaints to regulators. No bad reviews on Trustpilot. This is a really bad solution in search of a problem. We have real problems right now, we should be coming together as an industry to help solve them. We want to make sure that capital is available to small businesses on the other side of this pandemic, and this group of tone deaf companies are spending resources trying to push a meaningless disclosure bill that’s just going to hurt the access to capital for real small businesses who are grinding and trying to figure out how to stay open. It’s unbelievable.”

The SBFA showed AltFinanceDaily a list of issues and complaints made to the New York legislature regarding S5470B. According to the trade group, these were largely ignored and the bill was pushed through with the issues left in. Among these were problems relating to definitions and terms. No definition for the application process is included, nor is there one for a finance charge. As well as this, one senator was quoted using the term “double dipping” to refer to consumers refinancing debts that have prepayment penalties; which Denis said was “creating a whole new term that’s never been used or defined before, and applying it to commercial finance, something that’s never been done.”

Accompanying these complaints was one regarding how APR is calculated, as S5470B includes two different calculations for this, producing different results while not clearly defining when to use each.

When asked why he believes these issues were allowed to remain in the language of the bill, Denis was baffled.

When asked why he believes these issues were allowed to remain in the language of the bill, Denis was baffled.

“I think that the companies and organizations that support this legislation don’t fully understand what’s actually in the bill. […] They have no problem pounding the table and taking credit for its passage, but I guess they don’t realize it will subject them and the rest of the alternative finance industry to massive liability, massive fines—upwards of billions of dollars worth of fines.”

Denis’s fear going forward is that funders in New York will tighten up their channels going forward or cease funding entirely, given the increased riskiness of funding under the terms of S5470B if Cuomo signs it into law. Before that happens though, the Director mentioned that he believes there will be legal challenges to the bill in the future, saying that its wording is just too unclear and poorly drafted. Adding to this, Denis said that he believes many members of New York’s state government are aware that this bill is imperfect and were comfortable with the thought of it being edited once passed. Looking forward, Denis wants the SBFA to be deeply involved in those edits, saying that they’re willing to work with the Governor, the state assembly, and the New York Department of Financial Services.

“We’re for disclosure, we think there should be standard disclosure. … Our message to the Governor’s office is ‘Let’s take a step back.’ The Department of Financial Services needs to look at our industry, they need to get to know our industry. They are the experts that understand the space, they understand disclosure, and they understand what they need to do to bring responsible lending to New Yorkers. And we would like to work with the NYDFS and a broader industry to put forward a bill that’s led by the Governor and the Governor’s office that brings meaningful disclosure and meaningful safeguards to this industry.”

LendingPoint Partners with eBay to Fund Online Sellers

August 6, 2020 LendingPoint announced this week that it is partnering with the online marketplace eBay to provide funding to sellers on its platform. Titled eBay Seller Capital, the program will offer terms of up to 48 months, with no origination or early payback fees, and which will be capped at $25,000 during its pilot program.

LendingPoint announced this week that it is partnering with the online marketplace eBay to provide funding to sellers on its platform. Titled eBay Seller Capital, the program will offer terms of up to 48 months, with no origination or early payback fees, and which will be capped at $25,000 during its pilot program.

“We’re committed to empowering entrepreneurs to make their dreams a reality, and we are continuing to partner with our sellers to provide them with the tools they need to thrive, eBay’s VP of Global Payments Alyssa Cutright said in a statement. “We’re excited to make flexible financing options available that are integrated with our new payments experience. The program with LendingPoint will enable critical funding opportunities for eBay sellers, especially during this time of economic uncertainty.”

In its early stages now, eBay Seller Capital will only be available for selected sellers, with the plan being for it to be made available to all eligible sellers in the US later this year. Beyond the program, LendingPoint has made clear in its statement that it aims to “expand their offering to provide eBay sellers with more tools to help run their businesses,” however, when asked, CEO and Co-Founder Tom Burnside did not give details of these future plans.

“I don’t want to leave the proverbial cat out of the bag yet with that,” Burnside commented in a call, “but what I will tell you is that I think when we are done eBay will be able to offer best-of-class seller financing.”

IN DEFAULT OR ABOVE WATER: How PPP Saved or Didn’t Save America

July 31, 2020 Kristy Kowal, a silver medalist in the 200-meter breast stroke at the 2000 Olympic games in Australia, had recently relocated to Southern California and embarked on a new career when the pandemic shutdown hit in March.

Kristy Kowal, a silver medalist in the 200-meter breast stroke at the 2000 Olympic games in Australia, had recently relocated to Southern California and embarked on a new career when the pandemic shutdown hit in March.

After nearly two decades as a third-grade teacher in Pennsylvania, Kowal was able to take early retirement in 2019 and pursue her dream job. At last, she was self-employed and living in Long Beach where she could now devote herself to putting on swim clinics, training top athletes, and accepting speaking engagements. “I’ve been building up to this for twenty years,” she says.

But fate had a different idea. The coronavirus not only grounded her from travel but closed down most swimming pools. At first, she tried to collect unemployment compensation. But after two months of calling the unemployment office every day, her claim was denied. “‘Have a great day,’ the lady said, and then she hung up,” Kowal reports. “She wasn’t rude; she just hung up.”

Then, in June, the former Olympian heard from friends about Kabbage and the Paycheck Protection Program. Using an app on her smart phone, Kowal says, she was able to upload documents and complete the initial application in fewer than 20 minutes. A subsequent application with a bank followed and within a week she had her money.

“I was down to ten cents in my checking account,” says Kowal, who declined to disclose the amount of PPP money for which she qualified, “and I’d begun dipping into my savings. This gives me the confidence that I need to go back to my fulltime work.”

Kowal is one of 4.9 million small business owners and sole proprietors who, according to the U.S. Small Business Administration, has received potentially forgivable loans under the Paycheck Protection Program. The PPP, a safety-net program designed to pay the wages of employees for small businesses affected by the coronavirus pandemic, is a key component of the $1.76 trillion Coronavirus Aid, Relief, and Economic Security Act (CARES Act). Since the U.S. Congress enacted the law on March 27, the PPP has been renewed and amended twice. It’s now in its third round of funding and Congress is weighing what to do next.

Kowal is one of 4.9 million small business owners and sole proprietors who, according to the U.S. Small Business Administration, has received potentially forgivable loans under the Paycheck Protection Program. The PPP, a safety-net program designed to pay the wages of employees for small businesses affected by the coronavirus pandemic, is a key component of the $1.76 trillion Coronavirus Aid, Relief, and Economic Security Act (CARES Act). Since the U.S. Congress enacted the law on March 27, the PPP has been renewed and amended twice. It’s now in its third round of funding and Congress is weighing what to do next.

Kowal’s experience, meanwhile, is also a wake-up call for the country on the prominent role that both fintechs like Kabbage as well as community and independent banks, credit unions, non-banks and other alternatives to the country’s biggest banks play in supporting small business. Before many in this cohort were deputized by the SBA as full-fledged PPA lenders, a significant chunk of U.S. microbusinesses – especially sole proprietorships — were largely disdained by the brand-name banks.

“After the first round,” notes Karen Mills, former administrator of the U.S. Small Business Administration and a senior fellow at the Harvard Business School, “more institutions were approved that focused on smaller borrowers. These included fintechs and I have to say I’ve been very impressed.”

Among the cadre of fintechs making PPP loans – including Funding Circle, Intuit Quickbooks, OnDeck, PayPal, and Sabre — Kabbage stands out. The Atlanta-based fintech ranked third among all U.S. financial institutions in the number of PPP credits issued, its 209,000 loans trailing only Bank of America’s 335,000 credits and J.P. Morgan Chase’s 260,000, according to the SBA and company data. Kabbage also reports processing more than $5.8 billion in PPP loans to small businesses ranging from restaurants, gyms, and retail stores to zoos, shrimp boats, beekeepers, and toy factories.

To reach businesses in rural communities and small towns, Kabbage collaborated with MountainSeed, an Atlanta-based data-services provider, to process claims for 135 independent banks and credit unions around the U.S. The proof of the pudding: Eighty-nine percent of Kabbage’s PPP loans, says Paul Bernardini, director of communications at Atlanta-based Kabbage, were under $50,000, and half were for less than $13,500.

The figures illustrate not only that Kabbage’s PPP customers were mainly composed of the country’s smaller, “most vulnerable” businesses, Bernardini asserts, but the numbers serve as a reminder that “fintechs play a very important, vital role in small business lending,” he says.

The helpfulness of such financial institutions contrasts sharply with what many small businesses have reported as imperious indifference by the megabanks. Gerri Detweiler, education director at Nav, Inc., a Utah-based online company that aggregates data and acts as a financial matchmaker for small businesses, steered AltFinanceDaily toward critical comments about the big banks made on Nav’s Facebook page. Bank of America, especially, comes in for withering criticism.

“Bank of America wouldn’t even take my application,” one man wrote in a comment edited for brevity. “I have three accounts there. They are always sending me stuff about what an important client I am. But when the going got tough, they wouldn’t even take my application. I’m moving all my business from Bank of America.”

Lamented another Bank of America customer: “I was denied (PPP funding) from Bank of America (where) I have an individual retirement account, personal checking and savings account, two credit cards, a line of credit for $20.000, and a home mortgage. Add in business checking and a business credit card. Yesterday I pulled out my IRA. In the next few days I’m going to change to a credit union.”

Many PPP borrowers who initially got the cold shoulder from multi-billion-dollar conglomerate banks have found refuge with local — often small-town — bankers and financial institutions. Natasha Crosby, a realtor in Richmond, Va., reports that her bank, Capital One, “didn’t have the applications available when the Paycheck Protection Program started” on April 6. And when she finally was able to apply, she notes, “the money ran out.”

Crosby, who is president of Richmond’s LGBTQ Chamber of Commerce, is media savvy and was able to publicize her predicament through television appearances on CNN and CBS, as well as in interviews with such publications as Mother Jones and Huffington Post. A “friendly acquaintance,” she says, referred her to Atlantic Union Bank, a Richmond-based regional bank, where she eventually received a PPP loan “in the high five figures” for her sole proprietorship.

“It took almost two months,” Crosby says. “I was totally frozen out of the program at first.”

Talibah Bayles heads her own firm, TMB Tax and Financial Services, in Birmingham, Ala. where she serves on that city’s Small Business Council and the state’s Black Chamber of Commerce. She told AltFinanceDaily that she’s seen clients who have similarly been decamping to smaller, less impersonal financial institutions. “I have one client who just left Bank of America and another who’s absolutely done with Wells Fargo,” she says. “They’re going to places like America First Credit Union (based in Ogden, Utah) and Hope Credit Union (headquartered in Jackson, Miss.). I myself,” she adds, “shifted my business from Iberia Bank.”

Main Street bankers acknowledge that they are benefiting from the phenomenon. “In speaking to our industry colleagues,” says Tony DiVita, chief operating officer at Bank of Southern California, an $830 million-asset community bank based in San Diego, “we’ve seen that many of the big banks have slowed down or stopped lending small-dollar amounts that were too low for them to expend resources to process.”

Main Street bankers acknowledge that they are benefiting from the phenomenon. “In speaking to our industry colleagues,” says Tony DiVita, chief operating officer at Bank of Southern California, an $830 million-asset community bank based in San Diego, “we’ve seen that many of the big banks have slowed down or stopped lending small-dollar amounts that were too low for them to expend resources to process.”

At the same time, DiVita says, his bank had made 2,634 PPP loans through July 17, roughly 80% of which went to non-clients. Of that number, some 30% have either switched accounts or are in the process of doing so. And, he notes, the bank will get a second crack at conversion when the PPP loan-forgiveness process commences in earnest. “Our guiding spirit is to help these businesses for the continuation of their livelihoods,” he says.

Noah Wilcox, chief executive and chairman of two Minnesota banks, reports that both of his financial institutions have been working with non-customers neglected by bigger banks where many had been longtime customers. At Grand Rapids State Bank, he says, 26% of the 198 PPP applicants who were successfully funded were non-customers. Minnesota Lakes Bank in Delano, handled PPP credits for 274 applicants, of whom 66% were non-customers.

“People who had been customers forever at big banks told us that they had been applying for weeks and were flabbergasted that we were turning those applications around in an hour,” says Wilcox, who is also the current chairman of the Independent Community Bankers of America, a Washington, D.C.-based trade group representing community banks.

Noting that one of his Gopher State banks had successfully secured funding for an elderly PPP borrower “who said he had been at another bank for 69 years and could not get a telephone call returned,” Wilcox added: “We’ve had quite a number of those individuals moving their relationships to us.”

For Chris Hurn, executive director at Fountainhead Commercial Capital, a non-bank SBA lender in Lake Mary, Fla., the psychic rewards have helped compensate for the sometimes 16-hour days he and his staff endured processing and funding PPP applications. “It’s been relentless,” he says of the regimen required to funnel loans to more than 1,300 PPP applicants, “but we’ve gotten glowing e-mails and cards telling us that we’ve saved people’s livelihoods.”

Yet even as the Paycheck Protection Program – which only provides funding for two-and-a-half months – is proving to be immensely helpful, albeit temporarily, there is much trepidation among small businesses over what happens when the government’s spigots run dry. The hastily contrived design of the program, which has relied heavily on the country’s largest financial institutions, has contributed mightily to the program’s flaws.

“The underbanked and those who don’t have banking relationships were frozen out in the first round,” says Sarah Crozier, director of communications at Main Street Alliance, a Washington D.C.-based advocacy organization comprising some 100,000 small businesses. “The new updates were incredibly necessary and long overdue,” she adds, “but the changes didn’t solve the problem of equity in access to the program and whom money is flowing to in the community.”

Professor David Audretsch, an economist at Indiana University’s O’Neill School of Public and Environmental Affairs and an expert on small business, says of PPP: “It’s a short-term fix to keep businesses afloat, but it missed in a lot of ways. It was not well-thought-out and a lot of money went to the wrong people.”

The U.S. unemployment rate stood at 11.1% in June, according to the most recent figures released by the Bureau of Labor Statistics, about three times the rate of February, just before the pandemic hit. The BLS also reported that 47.2% of the U.S. population – nearly half –was jobless in June. Against this backdrop, SBA data on PPP lending released in early July showed that a stunning array of cosseted elite enterprises and organizations, many with close connections to rich and powerful Washington power brokers, have been feasting on the PPP program.

In a stunning number of cases, the program’s recipients have been tony Washington, D.C. law firms, influential lobbyists and think tanks, and even members of Congress. Many businesses with ties to President Trump and Trump donors have also figured prominently on the SBA list of those receiving largesse from the SBA.

Businesses owned by private equity firms, for which the definition of “small business” strains credulity, were also showered with PPP dollars. Bloomberg News reported that upscale health-care businesses in which leveraged-buyout firms held a controlling interest, were impressively adept at accessing PPP money. Among this group were Abry Partners, Silver Oak Service Partners, Gauge Capital, and Heron Capital. (Small businesses are generally defined as enterprises with fewer than 500 employees. The SBA reports that there are 30.7 million small businesses in the U.S. and that they account for roughly 47% of U.S. employment.)

Businesses owned by private equity firms, for which the definition of “small business” strains credulity, were also showered with PPP dollars. Bloomberg News reported that upscale health-care businesses in which leveraged-buyout firms held a controlling interest, were impressively adept at accessing PPP money. Among this group were Abry Partners, Silver Oak Service Partners, Gauge Capital, and Heron Capital. (Small businesses are generally defined as enterprises with fewer than 500 employees. The SBA reports that there are 30.7 million small businesses in the U.S. and that they account for roughly 47% of U.S. employment.)

Boston-based Abry Partners, which currently manages more than $5 billion in capital across its active funds, merits special mention. Among other properties, Abry holds the largest stake in Oliver Street Dermatology Management, recipient of between $5 million and $10 million in potentially forgivable PPP loans. Based in Dallas, Oliver Street ranks among the largest dermatology management practices in the U.S. and, according to a company statement, boasts the most extensive such network in Texas, Kansas and Missouri.

Meanwhile, the design of the program and the formula for the looming forgiveness process is proving impractical. As it currently stands, loan forgiveness depends on businesses spending 60% of PPP money on employees’ wages and health insurance with the remaining 40% earmarked for rent, mortgage or utilities.

Many businesses such as restaurants and bars, storefront retailers and boutiques – particularly those that have shut down — are preferring to let their employees collect unemployment compensation. “Business owners had a hard time wrapping their heads around the requirement of keeping employees on the payroll while they’re closed,” notes Detweiler, the education director at Nav. “They have other bills that have to be paid.”

Many businesses such as restaurants and bars, storefront retailers and boutiques – particularly those that have shut down — are preferring to let their employees collect unemployment compensation. “Business owners had a hard time wrapping their heads around the requirement of keeping employees on the payroll while they’re closed,” notes Detweiler, the education director at Nav. “They have other bills that have to be paid.”

The forgiveness formula remains vexing for businesses where real estate costs are exorbitant, particularly in high-rent cities such as New York, Boston, Washington, D.C., San Francisco, and Chicago. Tyler Balliet, the founder and owner of Rose Mansion, a midtown Manhattan wine-bar promising an extravagant, theme-park experience for wine enthusiasts, says that it took him a month and a half to receive almost $500,000 from Chase Bank. Unfortunately, though, the money isn’t doing him much good.

“I have 100 employees on staff, most of whom are actors,” he says. “We shut down on March 13. I laid off 95 employees and kept just a few people to keep the lights on.”

At the same time, his annual rent tops $1 million and the forgivable amount in the PPP loans won’t even cover a month’s rent. “I haven’t paid rent since March and I’m in default,” Balliet says. “Now I’m just waiting to see what the landlord wants to do.”

Like many business owners, Balliet financed much of his venture with credit card debt, which creates an additional liability concern, notes Crozier of the Main Street Alliance. “It’s very common for borrowers to have signed personal guarantees in their loans using their credit cards,” she says. “As we get closer to the funding cliff and as rent moratoriums end,” she adds, “creditors are coming after borrowers and putting their personal homes at risk.”

Mark Frier is the owner of three restaurants in Vermont ski towns, including The Reservoir — his flagship — in Waterbury. In toto, his eateries chalked up $6.5 million in combined sales in 2019. But 2020 is far different: the restaurants have not been open since mid-March and he’s missed out on the lucrative, end-of-season ski rush.

Consequently, Frier has been reluctant to draw down much of the $750,000 in PPP money he’d secured through local financial institutions. “We could end up with $600,000 in debt even with the new rules,” Frier says, adding: “We live off very thin margins. We need grants not loans.”

As the country recorded 3.7 million confirmed cases of coronavirus and more than 141,000 deaths as of mid-July, PPP money earmarked by businesses for health-related spending was not deemed forgivable. Yet in order to comply with regulations promulgated by the Occupational Safety and Health Administration and mandates and ordinances imposed by state and local governments, many establishments will be unable to avoid such expenditures.

“What we really needed was a grant program for companies to pivot to a business environment in a pandemic,” says Crozier. She cites the necessity businesspeople face of “retrofitting their businesses, buying masks, gloves and sanitizers and cleaning supplies, restaurants’ taking out tables and knocking down walls, installing Plexiglass shields, and improving air filtration systems.”

Meanwhile, as Covid-19 was taking its toll in sickness and death, the economic outlook for small business has been looking dire as well. The recent U.S. Census’s “Pulse Survey” of some 885,000 businesses updated on July 2 found that roughly 83% reported that Covid-19 pandemic had a “negative effect on their business. Fully 38% of all small business respondents, moreover, reported a “large negative effect.”

Meanwhile, as Covid-19 was taking its toll in sickness and death, the economic outlook for small business has been looking dire as well. The recent U.S. Census’s “Pulse Survey” of some 885,000 businesses updated on July 2 found that roughly 83% reported that Covid-19 pandemic had a “negative effect on their business. Fully 38% of all small business respondents, moreover, reported a “large negative effect.”

Amid the unabated spikes in the number of coronavirus cases and the country’s grave economic distress, PPP recipients are faced with the unsettling approach of the PPP forgiveness process. As Congress, the SBA, and the U.S. Treasury Department continue to remake and revise the rules and regulations governing the program, businesses are operating in a climate of uncertainty as well. Currently, the law states that the amount of the PPP loan that fails to be forgiven will convert to a five-year, one-percent loan — a relaxation in terms from the original two-year loan which is not necessarily cheering recipients.

“One of the biggest problems with PPP is that the rule book has been unclear,” frets Vermont restaurateur Frier, glumly adding: “This is not even a good loan program.”

Ashley Harrington, senior counsel at the Center for Responsible Lending, a research and policy group based in Durham, N.C., argued in House committee testimony on June 17, that there ought to be automatic forgiveness for PPP loans under $100,000. Such a policy, she declared, “would likely exempt firms with, on average, 13 or fewer employees and save 71 million hours of small business staff time.”

She also said, “The smallest PPP loans are being provided to microbusinesses and sole proprietors that have the least capacity and resources to engage in a complex (forgiveness) process with their financial institution and the SBA.”

William Phelan, president of Skokie (Ill.)-based PayNet, a credit-data services company for small businesses which recently merged with Equifax, sounded a similar note. Observing that there are some 23 million “non-employer” small businesses in the U.S. with fewer than three employees for whom the forgiveness process will likely be burdensome, he says: “Estimates are that it will cost businesses a few thousand dollars just to get a $100,000 loan forgiven. It’s going to involve mounds of paper work.”

The country’s major challenge now will be to re-boot the economy, Phelan adds, which will require massive financing for small businesses. “The fact is that access to capital for small businesses is still behind the times,” Phelan says. “At the end of the day, it took a massive government program to insure that there’s enough capital available for half of the U.S. economy” during the pandemic.

For his part, Professor Audretsch fervently hopes that the country has learned some profound lessons about the need to prepare for not just a rainy day, but a rainy season. The pandemic, he says, has exposed how decades of political attacks on government spending for disaster-preparedness and safety-net programs have left the U.S. exposed to unforeseen emergencies.

“We’re seeing the consequence of not investing in our infrastructure,” he says. “That’s a vague word but we need a policy apparatus in place so that the calvary can come riding in. This pandemic reminds me a lot of when Hurricane Katrina hit New Orleans,’ he adds. “The city paid a heavy price because we didn’t have the infrastructure to deal with it.”

MCA in Conversation: Where do we go from here?

July 27, 2020 DeBanked Magazine recently posted the “Underwriter’s Song” to highlight an entire industry’s yearning for simpler times, claiming it was the MCA soundtrack for 2020. But I disagree and nominate a different song. You see, growing up in the south with a close-knit family gave way to a childhood filled with generations worth of entertainment. Many of my summers and holiday vacations were spent with the Turner Classic Movie channel playing in the background, and songs from the Oldies Country station on the radio. I tell you this to explain how I am reminded of a song I’ve heard countless times before, and is more applicable today than ever before. That song is “If We Make It Through to December” by the venerable Merle Haggard, a tune whose message resonates with not only the merchant cash advance industry, but our entire country.

DeBanked Magazine recently posted the “Underwriter’s Song” to highlight an entire industry’s yearning for simpler times, claiming it was the MCA soundtrack for 2020. But I disagree and nominate a different song. You see, growing up in the south with a close-knit family gave way to a childhood filled with generations worth of entertainment. Many of my summers and holiday vacations were spent with the Turner Classic Movie channel playing in the background, and songs from the Oldies Country station on the radio. I tell you this to explain how I am reminded of a song I’ve heard countless times before, and is more applicable today than ever before. That song is “If We Make It Through to December” by the venerable Merle Haggard, a tune whose message resonates with not only the merchant cash advance industry, but our entire country.

The Expectations and Reality

Way back in March and April, the consensus appeared to be an expected return to “normal” by June, while areas hit hardest by COVID-19 would return by July. Yet here we are, teeter-tottering on the fence of moving forward. Now, our country is faced with the possibility of a second wave of shutdowns, rising crime, riots, a fourth stimulus, and funders whose workforce remains remote or have yet to resume funding. The proverbial “goal post” has moved yet again, and with it the expectations of many of us in the industry. Over the past few weeks, I had the opportunity to speak with a number of our referral partners to gauge their thoughts on the current state of our industry. A common theme in our discussions was the desire for validation. Not just as a business owner, but as an employer. They wanted to be reassured that they were taking the best steps forward and not alone in their decision making. To help those seeking the same validation, here is what the majority had to say:

- Yes, all had to terminate or furlough staff on various levels.

- Yes, all adjusted marketing budgets.

- Yes, all are struggling with managing remote employees.

- Yes, all are finding it harder to place files.

- Yes, all are seeing interruptions in relationships with funders and merchants alike.

- Yes, all are competing against the Government’s low-cost products.

- Yes, all are having files killed in late stages of funding or having offers adjusted.

- Yes, all are struggling to predict what comes next.

- Yes, all are managing unrealistic expectations from clients.

- Yes, all are having merchants walk away from fair and just offers.

- Yes, all are struggling to remain motivated.

- And yes, all of you are doing the best you can!

The New Normal

The Word Cloud below describes the state of the MCA industry using our partners’ own words. I find that the overall thoughts are best visualized by taking a step back to see which stand out the most. Our conversation was focused on the industry as a whole, then a discussion specific to Elevate Funding and how we’ve pivoted during these unprecedented times. As you can see, some of the keywords that stand out the most are; merchants, PPP, offers, funders, and marketing.

Much of the conversations focused around merchants and their new funding expectations. Each partner I spoke with agreed the demand for money is there, but the willingness to move forward on offers was very low. This reluctance is driven in part by low cost expectations based on PPP and SBA product rates, as well as uncertainty over increased debt in an unstable market. We’re also seeing a change in merchant demographics, where the mid-sized small businesses who previously did not qualify for SBA loans, now have access to these products. As a result, the remaining merchants whose best option is an MCA are now located on the opposite extreme ends of the spectrum; either those who did not qualify for PPP or SBA EIDL, and the large-scale businesses whose lines were revoked by their bank. Our response as a company has been to adjust our offers to better suit merchant’s expectations, and to shift from underwriting a business owner’s activity to underwriting the consumers’ activity. Monitoring government restrictions down to a county level countrywide and understanding consumer trends has enabled us to further mitigate risk during a time of uncertainty, and not only fund deals, but fund deals that will perform.

Meanwhile, our industry is seeing credit profiles and business profiles that have never applied in our space before, as a decreasing number of providers are available to service current merchants. During our conversations, some expressed a concern over lack of A-paper funders. Many of whom have either paused funding or entirely moved over to servicing PPP products. Another concern was the mental toll of having deals fall apart at the eleventh hour due to fast changing qualifications, variations in merchant revenue, or funders deciding to pause funding at inopportune times. These factors combined with the increasingly common “bait-and-switch” technique of funders providing a large offer, only to change to a much lower offer in the final stages of funding, has left many broker shops and ISOs feeling very discouraged.

The Path Upward and Onward

The conversations were not entirely negative, as new marketing opportunities have opened up with the goliaths of the industry such as Kabbage, OnDeck, Lendio, and Square shifting their marketing dollars towards PPP and SBA products. Many folks are finding their advertising dollars across marketing platforms are stretching further, particularly with search engine optimization. While this opens up an increased likelihood of fraud and in applicants who fall below qualifications, it has enabled many shops to operate on an even playing field with inbound marketing. Many small funders, including Elevate Funding, have already created new products to cater to lower revenue merchants and those directly affected by COVID-19. We’ve already received tremendous response on this change from partners and merchants alike. As merchants slowly shift back towards alternative financing solutions once the government runs out of money for its loan products, we remain optimistic there will be increased opportunities in terms of both volume and quality.

While the Word Cloud highlighted a number of topics, it also highlighted important topics that were not discussed; Expectations, Renewals, Commission, Aggression, and Repositioning.

Expectations in particular, is of note as it is different from opinions. Everyone has an opinion, but there is a tremendous sense of uncertainty going forward and it’s very difficult to create expectations or goals when forecasting is not possible. Many companies are doing away with forecasting models altogether, and switching to a dashboard for production goals and expectations based on real time data.

The drastic change we’re seeing now should demonstrate the importance of renewals and customer retention. Neither of which were brought up during all of my partner discussions. Over time, the industry has moved away from a “residual mindset” to seeking instant gratification of new fundings in the quest for market share supremacy. As funders, we have to ask ourselves; Are we inadvertently throwing out the baby with the bathwater with new deal bonus structures and monthly promotional campaigns to drive new deal growth? Or perhaps, renewals were scarce in discussions because when funders said when funding stopped, they meant all funding? While I can’t speak to each funder’s operations, Elevate has continued to fund throughout the pandemic with established merchants and renewals being a saving grace to drive our momentum forward. In my opinion, client retention has never been more important during an ever-changing landscape.

I was shocked to see commission taking a backseat to approvals and banks during our discussion. But the focus has seemingly move towards approvals and conversions, which will in turn lead to commissions returning. Which brings me to Aggression and Repositioning. The state of our industry is a timid one, and it’s neither the fault of the funders or the merchants. Many experts will tell you that our space was overdue for a market correction of sorts, because many were far too aggressive for far too long. This aggression gave way to bad habits such as lowered underwriting standards and lack of consideration for merchant ability to repay. More and more funders are shifting back to “normal” guidelines, providing fair and just offers. This is an encouraging sign that we are finding our way back to sustainable positive growth. But it will take time for the industry to fully reposition itself. Something that is being delayed by products from the PPP, SBA, and the hope for a third round of stimulus.

But hope is on the horizon. While the pessimists will look at that word as a form of denial, I challenge all of you to take a glass half-full approach. Hope is the confident expectation of good. The change and adjustments we’re experiencing now are what life is all about, and will ultimately lend way to better things. If you’re in need of a little dose of hope, or want a sounding board to know you’re not alone through this, feel free to drop me a line at heather@elevatefunding.com.

Stay safe, be well, and do not lose hope.