The FTC Wants To Police Small Business Finance

October 22, 2019 On May 23, the Federal Trade Commission launched an investigation into unfair or deceptive practices in the small business financing industry, including by merchant cash advance providers.

On May 23, the Federal Trade Commission launched an investigation into unfair or deceptive practices in the small business financing industry, including by merchant cash advance providers.

The agency is looking into, among other things, whether both financial technology companies and merchant cash advance firms are making misrepresentations in their marketing and advertising to small businesses, whether they employ brokers and lead-generators who make false and misleading claims, and whether they engage in legal chicanery and misconduct in structuring contracts and debt-servicing.

Evan Zullow, senior attorney at the FTC’s consumer protection division, told AltFinanceDaily that the FTC is, moreover, investigating whether fintechs and MCAs employ “problematic,” “egregious” and “abusive” tactics in collecting debts. He cited such bullying actions as “making false threats of the consequences of not paying a debt,” as well as pressuring debtors with warnings that they could face jail time, that authorities would be notified of their “criminal” behavior, contacting third-parties like employers, colleagues, or family members, and even issuing physical threats.

“Broadly,” Zullow said in a telephone interview, “our work and authority reaches the full life cycle of the financing arrangement.” He added: “We’re looking closely at the conduct (of firms) in this industry and, if there’s unlawful conduct, we’ll take law enforcement action.”

Zullow declined to identify any targets of the FTC inquiry. “I can’t comment on nonpublic investigative work,” he said.

The FTC investigation is one of several regulatory, legislative and law enforcement actions facing the merchant cash advance industry, which was triggered by a Bloomberg exposé last winter alleging sharp practices by some MCA firms.

The FTC investigation is one of several regulatory, legislative and law enforcement actions facing the merchant cash advance industry, which was triggered by a Bloomberg exposé last winter alleging sharp practices by some MCA firms.

The Bloomberg series told of high-cost financings, of MCA firms’ draining debtors’ bank accounts, and of controversial collections practices in which debtors signed contracts that included “confessions of judgment.”

The FTC long ago outlawed the use of COJs in consumer loan contracts and several states have banned their use in commercial transactions. In September, Governor Andrew Cuomo signed legislation prohibiting the use of COJs in New York State courts for out-of-state residents. And there is a bipartisan bill pending in the U.S. Senate authored by Florida Republican Marco Rubio and Ohio Democrat Sherrod Brown to outlaw COJs nationwide.

Mark Dabertin, a senior attorney at Pepper Hamilton, described the FTC’s investigation of small business financing as a “significant development.” But he also said that the agency’s “expansive reading of the FTC Act arguably presents the bigger news.” Writing in a legal memorandum to clients, Dabertin added: “It opens the door to introducing federal consumer protection laws into all manner of business-to-business conduct.”

FTC attorney Zullow told AltFinanceDaily, “We don’t think it’s new or that we’re in uncharted waters.”

The FTC inquiry into alternative small business financing is not the only investigation into the MCA industry. Citing unnamed sources, The Washington Post reported in June that the Manhattan district attorney is pursuing a criminal investigation of “a group of cash advance executives” and that the New York State attorney general’s office is conducting a separate civil probe.

The FTC’s investigation follows hard on the heels of a May 8 forum on small business financing. Labeled “Strictly Business,” the proceedings commenced with a brief address by FTC Commissioner Rohit Chopra, who paid homage to the vital role that small business plays in the U.S. economy. “Hard work and the creativity of entrepreneurs and new small businesses helped us grow,” he said.

But he expressed concern that entrepreneurship and small business formation in the U.S. was in decline. According to census data analyzed by the Kaufmann Foundation and the Brookings Institution, the commissioner noted, the number of new companies as a share of U.S. businesses has declined by 44 percent from 1978 to 2012.

“It’s getting harder and harder for entrepreneurs to launch new businesses,” Chopra declared. “Since the 1980s, new business formation began its long steady decline. A decade ago births of new firms started to be eclipsed by deaths of firms.”

Chopra singled out one-sided, unjust contracts as a particularly concerning phenomenon. “One of the most powerful weapons wielded by firms over new businesses is the take-it-or-leave-it contract,” he said, adding: “Contracts are ways that we put promises on paper. When it comes to commerce, arm’s length dealing codified through contracts is a prerequisite for prosperity. “But when a market structure requires small businesses to be dependent on a small set of dominant firms — or firms that don’t engage in scrupulous business practices — these incumbents can impose contract terms that cement dominance, extract rents, and make it harder for new businesses to emerge and thrive.”

As the panel discussions unfolded, representatives of the financial technology industry (Kabbage, Square Capital and the Electronic Transactions Association) as well as executives in the merchant cash advance industry (Kapitus, Everest Business Financing, and United Capital Source) sought to emphasize the beneficial role that alternative commercial financiers were playing in fostering the growth of small businesses by filling a void left by banks.

The fintechs went first. In general, they stressed the speed and convenience of their loans and lines of credit, and the pioneering innovations in technology that allowed them to do deeper dives into companies seeking credit, and to tailor their products to the borrower’s needs. Panelists cited the “SMART Box” devised by Kabbage and OnDeck as examples of transparency. (Accompanying those companies’ loan offers, the SMART Box is modeled on the uniform terms contained in credit card offerings, which are mandated by the Truth in Lending Act. TILA does not pertain to commercial debt transactions.)

Sam Taussig, head of global policy at Kabbage, explained that his company typically provides loans to borrowers with five to seven employees — “truly Main Street American small businesses” — that are seeking out “project-based financing” or “working capital.”

Sam Taussig, head of global policy at Kabbage, explained that his company typically provides loans to borrowers with five to seven employees — “truly Main Street American small businesses” — that are seeking out “project-based financing” or “working capital.”

“The average small business according to our research only has about 27 days of cash flow on hand,” Taussig told the fintech panel, FTC moderators and audience members. “So if you as a small business owner need to seize an opportunity to expand your revenue or (have) a one-off event — such as the freezer in your ice cream store breaks — it’s very difficult to access that capital quickly to get back to business or grow your business.”

Taussig contrasted the purpose of a commercial loan with consumer loans taken out to consolidate existing debt or purchase a consumer product that’s “a depreciating asset.” Fintechs, which typically supply lightning-quick loans to entrepreneurs to purchase equipment, meet payrolls, or build inventory, should be judged by a different standard.

A florist needs to purchase roses and carnations for Mother’s Day, an ice-cream store must replenish inventory over the summer, an Irish pub has to stock up on beer and add bartenders at St. Patrick’s Day.

The session was a snapshot of not just the fintech industry but of the state of small business. Lewis Goodwin, the head of banking services at Square Capital, noted that small businesses account for 48% of the U.S. workforce. Yet, he said, Square’s surveys show that 70% of them “are not able to get what they want” when they seek financing.

Square, he said, has made 700,000 loans for $4.5 billion in just the past few years, the platform’s average loan is between $6,000 and $7,000, and it never charges borrowers more than 15% of a business’s daily receipts. The No. 1 alternative for small businesses in need of capital is “friends and family,” Goodwin said, “and that’s a tough bank to go back to.”

Panelist Gwendy Brown, vice-president of research and policy at the Opportunity Fund, a non-profit microfinance organization, provided the fintechs with their most rocky moment when she declared that small businesses turning up at her fund were typically paying an annual percentage rate of 94 percent for fintech loans. And while most small business owners were knowledgeable about their businesses — the florists “know flowers in and out,” for example — they are often bewildered by the “landscape” of financial product offerings.

Panelist Gwendy Brown, vice-president of research and policy at the Opportunity Fund, a non-profit microfinance organization, provided the fintechs with their most rocky moment when she declared that small businesses turning up at her fund were typically paying an annual percentage rate of 94 percent for fintech loans. And while most small business owners were knowledgeable about their businesses — the florists “know flowers in and out,” for example — they are often bewildered by the “landscape” of financial product offerings.

“Sophistication as a business owner,” Brown said, “does not necessarily equate into sophistication in being able to assess finance options.”

Panelist Claire Kramer Mills, vice-president of the Federal Reserve Bank of New York, reported that the country’s banks have made a dramatic exit from small business lending over the past ten years. A graphic would show that bank loans of more than $1 million have risen dramatically over the past decade but, she said, “When you look at the small loans, they’ve remained relatively flat and are not back to pre-crisis levels.”

Mills also said that 50% of small businesses in the Federal Reserve’s surveys “tell us that they have a funding shortfall of some sort or another. It’s more stark when you look at women-owned business, black or African-American owned businesses, and Latino-owned businesses.”

On the merchant cash advance panel there was less opportunity to dazzle the regulators and audience members with accounts of state-of-the-art technology and the ability to aggregate mountains of data to make online loans in as few as seven minutes, as Kabbage’s Taussig noted the fintech is wont to do.

Instead, industry panelists endeavored to explain to an audience — which included skeptical regulators, journalists, lawyers and critics — the precarious, high-risk nature of an MCA or factoring product, how it differs from a loan, and the upside to a merchant opting for a cash advance. (To their credit, one attendee told AltFinanceDaily, the audience also included members of the MCA industry interested in compliance with federal law.)

Instead, industry panelists endeavored to explain to an audience — which included skeptical regulators, journalists, lawyers and critics — the precarious, high-risk nature of an MCA or factoring product, how it differs from a loan, and the upside to a merchant opting for a cash advance. (To their credit, one attendee told AltFinanceDaily, the audience also included members of the MCA industry interested in compliance with federal law.)

A merchant cash advance is “a purchase of future receipts,” Kate Fisher, an attorney at Hudson Cook in Baltimore, explained. “The business promises to deliver a percentage of its revenue only to the extent as that revenue is created. If sales go down,” she explained, “then the business has a contractual right to pay less. If sales go up, the business may have to pay more.”

As for the major difference between a loan and a merchant cash advance: the borrower promises to repay the lender for the loan, Fisher noted, but for a cash advance “there’s no absolute obligation to repay.”

Scott Crockett, chief executive at Everest Business Funding, related two anecdotes, both involving cash advances to seasonal businesses. In the first instance, a summer resort in Georgia relied on Everest’s cash advances to tide it over during the off-season.

When the resort owner didn’t call back after two seasonal advances, Crockett said, Everest wanted to know the reason. The answer? The resort had been sold to Marriott Corporation. Thanking Everest, Crockett said, the former resort-owners reported that without the MCA, he would likely have sold off a share of his business to a private equity fund or an investor.

By providing a cash advance Everest acted “more like a temporary equity partner,” Crockett remarked.

In the second instance, a restaurant in the Florida Keys that relied on a cash advance from Everest to get through the slow summer season was destroyed by Hurricane Irma. “Thank God no one was hurt,” Crockett said, “but the business owner didn’t owe us anything. We had purchased future revenues that never materialized.”

The outsized risk borne by the MCA industry is not confined entirely to the firm making the advance, asserted Jared Weitz, chief executive at United Capital Service, a consultancy and broker based in Great Neck, N.Y. It also extends to the broker. Weitz reported that a big difference between the MCA industry and other funding sources, such as a bank loan backed by the Small Business Administration, is that ”you are responsible to give that commission back if that merchant does not perform or goes into an actual default up to 90 days in.

“I think that’s important,” Weitz added, “because on (both) the broker side and on the funding side, we really are taking a ride with the merchant to make sure that the business succeeds.”

FTC’s panel moderators prodded the MCA firms to describe a typical factor rate. Jesse Carlson, senior vice-president and general counsel at Kapitus, asserted that the factor rate can vary, but did not provide a rate.

FTC’s panel moderators prodded the MCA firms to describe a typical factor rate. Jesse Carlson, senior vice-president and general counsel at Kapitus, asserted that the factor rate can vary, but did not provide a rate.

“Our average financing is approximately $50,000, it’s approximately 11-12 months,” he said. “On a $50,000 funding we would be purchasing $65,000 of future revenue of that business.”

The FTC moderator asked how that financing arrangement compared with a “typical” annual percentage rate for a small business financing loan and whether businesses “understand the difference.”

Carlson replied: “There is no interest rate and there is no APR. There is no set repayment period, so there is no term.” He added: “We provide (the) total cost in a very clear disclosure on the first page of all of our contracts.”

Ami Kassar, founder and chief executive of Multifunding, a loan broker that does 70% of its work with the Small Business Administration, emerged as the panelist most critical of the MCA industry. If a small business owner takes an advance of $50,000, Kassar said, the advance is “often quoted as a factor rate of 20%. The merchant thinks about that as a 20% rate. But on a six-month payback, it’s closer to 60-65%.”

He asserted that small businesses would do better to borrow the same amount of money using an SBA loan, pay 8 1/4 percent and take 10 years to pay back. It would take more effort and the wait might be longer, but “the impact on their cash flow is dramatic” — $600 per month versus $600 a day, he said — “compared to some of these other solutions.”

Kassar warned about “enticing” offers from MCA firms on the Internet, particularly for a business owner in a bind. “If you jump on that train and take a short-term amortization, oftentimes the cash flow pressure that creates forces you into a cycle of short-term renewals. As your situation gets tougher and tougher, you get into situations of stacking and stacking.”

On a final panel on, among other matters, whether there is uniformity in the commercial funding business, panelists described a massive muddle of financial products.

Barbara Lipman: project manager in the division of community affairs with the Federal Reserve Board of Governors, said that the central bank rounded up small businesses to do some mystery shopping. The cohort — small businesses that employ fewer than 20 employees and had less than $2 million in revenues — pretended to shop for credit online.

As they sought out information about costs and terms and what the application process was like, she said, “They’re telling us that it’s very difficult to find even some basic information. Some of the lenders are very explicit about costs and fees. Others however require a visitor to go to the website to enter business and personal information before finding even the basics about the products.” That experience, Lipman said, was “problematic.”

She also said that, once they were identified as prospective borrowers on the Internet, the Fed’s shoppers were barraged with a ceaseless spate of online credit offers.

John Arensmeyer, chief executive at Small Business Majority, an advocacy organization, called for greater consistency and transparency in the marketplace. “We hear all the time, ‘Gee, why do we need to worry about this? These are business people,’” he said. “The reality is that unless a business is large enough to have a controller or head of accounting, they are no more sophisticated than the average consumer.

“Even about the question of whether a merchant cash advance is a loan or not,” Arensmeyer added. “To the average small business owner everything is a loan. These legal distinctions are meaningless. It’s pretty much the Wild West.”

In the aftermath of the forum, the question now is: What is the FTC likely to do?

In the aftermath of the forum, the question now is: What is the FTC likely to do?

Zullow, the FTC attorney, referred AltFinanceDaily to several recent cases — including actions against Avant and SoFi — in which the agency sanctioned online lenders that engaged in unfair or deceptive practices, or misrepresented their products to consumers.

These included a $3.85 million settlement in April, 2019, with Avant, an online lending company. The FTC had charged that the fintech had made “unauthorized charges on consumers’ accounts” and “unlawfully required consumers to consent to automatic payments from their bank accounts,” the agency said in a statement.

In the settlement with SoFi, the FTC alleged that the online lender, “made prominent false statements about loan refinancing savings in television, print, and internet advertisements.” Under the final order, “SoFi is prohibited from misrepresenting to consumers how much money consumers will save,” according to an FTC press release.

But these are traditional actions against consumer lenders. A more relevant FTC action, says Pepper Hamilton attorney Dabertin, was the FTC’s “Operation Main Street,” a major enforcement action taken in July, 2018 when the agency joined forces with a dozen law enforcement partners to bring civil and criminal charges against 24 alleged scam artists charged with bilking U.S. small businesses for more than $290 million.

In the multi-pronged campaign, which Zullow also cited, the FTC collaborated with two U.S. attorneys’ offices, the attorneys general of eight states, the U.S. Postal Inspection Service, and the Better Business Bureau. According to the FTC, the strike force took action against six types of fraudulent schemes, including:

- Unordered merchandise scams in which the defendants charged consumers for toner, light bulbs, cleaner and other office supplies that they never ordered;

- Imposter scams in which the defendants use deceptive tactics, such as claiming an affiliation with a government or private entity, to trick consumers into paying for corporate materials, filings, registrations, or fees;

- Scams involving unsolicited faxes or robocalls offering business loans and vacation packages.

If there remains any question about whether the FTC believes itself constrained from acting on behalf of small businesses as well as consumers, consider the closing remarks at the May forum made by Andrew Smith, director of the agency’s bureau of consumer protection.

“(O)ur organic statute, the FTC Act, allows us to address unfair and deceptive practices even with respect to businesses,” Smith declared, “And I want to make clear that we believe strongly in the importance of small businesses to the economy, the importance of loans and financing to the economy.

Smith asserted that the agency could be casting a wide net. “The FTC Act gives us broad authority to stop deceptive and unfair practices by nonbank lenders, marketers, brokers, ISOs, servicers, lead generators and collectors.”

As fintechs and MCAs, in particular, await forthcoming actions by the commission, their membership should take pains to comport themselves ethically and responsibly, counsels Hudson Cook attorney Fisher. “I don’t think businesses should be nervous,” she says, “but they should be motivated to improve compliance with the law.”

She recommends that companies make certain that they have a robust vendor-management policy in place, and that they review contracts with ISOs. Companies should also ensure that they have the ability to audit ISOs and monitor any complaints. “Take them seriously and respond,” Fisher says.

Companies would also do well to review advertising on their websites to ascertain that claims are not deceptive, and see to it that customer service and collections are “done in a way that is fair and not deceptive,” she says, adding of the FTC investigation: “This is a wake-up call.”

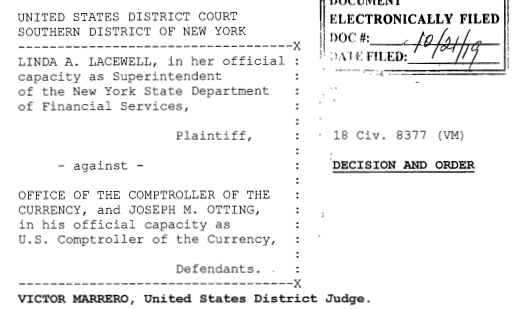

Federal Judge Rules New York’s “Win” Against OCC’s Fintech Charter Nullifies The Fintech Charter Concept Entirely

October 21, 2019 The Office of the Comptroller of The Currency took a gamble with a federal judge in a lawsuit brought by the New York Department of Financial Services (DFS) and lost. On Monday, Judge Victor Marrero ruled that the OCC must “set aside” its special purpose (fintech) national bank charters entirely, not just for those with a nexus to New York.

The Office of the Comptroller of The Currency took a gamble with a federal judge in a lawsuit brought by the New York Department of Financial Services (DFS) and lost. On Monday, Judge Victor Marrero ruled that the OCC must “set aside” its special purpose (fintech) national bank charters entirely, not just for those with a nexus to New York.

The outcome is a byproduct of a ruling issued on May 2nd where the OCC had sought to dismiss the challenge from the onset. DFS was somewhat victorious then in that the case was allowed to proceed, be litigated, and eventually tried. But the OCC felt the case was lost before it had begun because “the Court [had already] ruled on the issue of the law at the heart of the case: whether, under the National Bank Act, OCC has the authority to issue special purpose national bank charters to financial technology companies that do not accept deposits.”

The Court made it clear, that “OCC does not have the authority because the relevant language in the National Bank Act unambiguously defines ‘the business of banking to include deposit-taking.”

The Court made it clear, that “OCC does not have the authority because the relevant language in the National Bank Act unambiguously defines ‘the business of banking to include deposit-taking.”

As a result, OCC negotiated with DFS to reach an agreed upon final judgment in DFS’s favor. The only remaining question was to what level of defeat the OCC would concede. OCC argued a judgment should preclude only New York companies from applying for a fintech charter while the DFS argued it should apply beyond New York’s borders to all 50 states.

On Monday, the judge went with DFS’s version, pointing out that ordinarily prevailing on an Administrative Procedure Act claim, as OCC had indeed consented to judgment on, would mean that the agency’s order would be vacated, not that the plaintiff would win some special relief.

It is hereby ordered, adjudged and decreed that:

OCC’s regulation 5 C.F.R. 5.20(e)(1)(i), is set aside with respect to all fintech applicants seeking a national bank charter that do not accept deposits.

DFS Superintendent Linda A. Lacewell issued an official comment on the ruling:

This decision makes the financial well-being of consumers from New York and around the country a priority. It reflects the rational conclusion that DFS and other state banking regulators have the expertise to provide the strict supervisory oversight and enforcement of anti-money laundering and consumer protection statutes and regulations that non-depository financial service providers are required to follow. The decision stops OCC’s attempt to usurp state authority by establishing a federal fintech regulatory framework at the expense of consumers. Going forward, DFS will continue to be a fierce advocate for consumers in New York and nationwide.

National Business Capital & Services Expands into Cannabis Funding with CannaBusiness Financing Solution

October 15, 2019 Today National Business Capital & Services (NBC&S) announced it has begun serving cannabis companies. Through its new program, CannaBusiness Financing Solution, NBC&S is now accepting applications for loans starting at a minimum of $10,000 from firms in the industry that are over one year old.

Today National Business Capital & Services (NBC&S) announced it has begun serving cannabis companies. Through its new program, CannaBusiness Financing Solution, NBC&S is now accepting applications for loans starting at a minimum of $10,000 from firms in the industry that are over one year old.

“The CannaBusiness Financial Solution will allow business owners to seamlessly obtain the capital they need, and allocate funding toward either hiring new employees, purchasing inventory, marketing strategies, or any other business need right away, without government regulations hindering growth opportunities or having to give up equity,” explained NBC&S President Joseph Camberato. “We’re not a bank and the lenders we work with aren’t banks either, so it falls into a different area of commercial lending.”

CannaBusiness is available in the 33 states where cannabis is legal, be it for medicinal or recreational uses, as well as in Canada.

“It’s a rapidly growing space, no pun intended,” joked Camberato when asked about the differences in funding cannabis companies compared to the industries NBC&S has served in its 12 years of business. “It would still be underwritten, just like one of our normal businesses. But we’re definitely going to want to know a little bit more about the business and understand what exactly they’re doing, how they’re operating, and exactly what are they’re focused on.” They’ll also examine if the business is in compliance with state laws. Qualifying cannabis companies must be in business for at least 1 year, with a minimum of $10K in monthly revenue. There is no minimum FICO score requirement.

While it’s not the first funder for cannabis companies, NBC&S views the move as a step in the right direction to “get ahead of the curve” according to Camberato. “We’re living through a modern-day prohibition, I think in 20 years we’ll look back on it and talk about it with our grandchildren and be like, ‘wow’ … I don’t think people realize how big of a deal this really is, but it is a business and it is another industry that has bloomed in front of us, again no pun intended. I think it’s fascinating that we get to witness this and that we’re really at the forefront of it and helping folks get the funds they need to grow.”

While it’s not the first funder for cannabis companies, NBC&S views the move as a step in the right direction to “get ahead of the curve” according to Camberato. “We’re living through a modern-day prohibition, I think in 20 years we’ll look back on it and talk about it with our grandchildren and be like, ‘wow’ … I don’t think people realize how big of a deal this really is, but it is a business and it is another industry that has bloomed in front of us, again no pun intended. I think it’s fascinating that we get to witness this and that we’re really at the forefront of it and helping folks get the funds they need to grow.”

Jumping off from the politically charged word of ‘prohibition,’ NBC&S’ Vice President of Marketing, T.J. Muro, noted that he believed cannabis legislation to be one of the few issues that can be bipartisan, saying, “Out of everything today in our political climate, I think it’s the one thing that has unified people in the political parties. The liberal side appreciates the cultural influence and significance there, and then on the more conservative side it’s the tax revenue.”

The upcoming Senate vote on the SAFE Banking Act will put this theory to the test. The bill, which would allow the cannabis industry wider access to banking, has already passed the House.

To Niche or Not to Niche, That Is the Fintech Question

October 1, 2019 A store that sells only cufflinks. A restaurant that serves nothing but grilled cheese sandwiches. A tiny stand where you buy only artisanal salt. In the not-too-distant past, these kinds of shopping and dining options were almost unheard of. Readers of a certain age will remember that if you wanted cufflinks, you went to an all-in-one department store like Macy’s. If you had a hankering for a grilled cheese sandwich, you ordered one off the kids menu at TGI Fridays. And if you wanted fancy salt, you probably learned how to make it yourself. But as times changed, so did consumer behavior, and industries adapted; these days a consumer can find a singular shopping or dining experience for almost any bespoke want or need (entirely egg-based restaurants—they’re a thing). These specialty places have done well by a) focusing on a niche product or service, b) applying expertise to something they believe in and c) executing and perfecting it daily.

A store that sells only cufflinks. A restaurant that serves nothing but grilled cheese sandwiches. A tiny stand where you buy only artisanal salt. In the not-too-distant past, these kinds of shopping and dining options were almost unheard of. Readers of a certain age will remember that if you wanted cufflinks, you went to an all-in-one department store like Macy’s. If you had a hankering for a grilled cheese sandwich, you ordered one off the kids menu at TGI Fridays. And if you wanted fancy salt, you probably learned how to make it yourself. But as times changed, so did consumer behavior, and industries adapted; these days a consumer can find a singular shopping or dining experience for almost any bespoke want or need (entirely egg-based restaurants—they’re a thing). These specialty places have done well by a) focusing on a niche product or service, b) applying expertise to something they believe in and c) executing and perfecting it daily.

In the past decade, the fintech industry has followed this model to a tee. Whether it was B2B or B2C, fintech startups broke the banking business into narrower segments, offering singular niche services for various finance needs, e.g. credit card refinancing, small business loans, student loans, P2P payments, mortgages and more. From this model, big banks became the TGI Fridays of financial offerings (where you go to experience a full spread of financial services), and fintech platforms became the speciality grilled cheese shops (where you go to get the one thing you really crave).

Fintech Niches Fill Big Gaps

Many startups went niche not only because it was a business model that worked, but because the legacy banking industry model was out of date and there was room for true disruption. With these opportunities, niche fintechs could hone in on services that fulfilled singular needs, and they could do it with a focus, passion and dedicated customer service that most general banks couldn’t provide—and the results of this have been mostly positive. Globally, financial inclusion of unbanked people has improved. According to The World Bank, 69 percent of adults or 3.8 billion people now have an account at a bank or mobile money provider. In the U.S., niche fintechs made it easier for small businesses to get a loan post-recession. A host of online lenders stepped in to fill the gap, understanding that without access to relevant capital, small businesses struggle, which ultimately affects economic growth, jobs and inflation.

Can Fintechs Stand up to Tech Giants?

Tech giants thrive when users treat their platforms/offerings as a one-stop shop, something that is already commonplace in China, where millions of people use Tencent’s WeChat app to do almost everything—pay bills, book medical appointments, chat, play games, read news and pay for meals. Although this is not at the same level of activity in the U.S., it is a trend likely to continue.

The winds have been shifting as fintech companies question whether it makes sense to stay true to their niche or offer additional services as a path to scalability and profitability. By taking the latter path, former niche startups are now either a) building out and offering more financial services or b) partnering with more established companies/banks. Some recent examples include eBay and Square Capital, Venmo and Uber and KeyBank and HelloWallet. These partnerships seem to be a win-win—for the niche companies hoping to solve for scale and revenue stream issues, and for the established companies looking to offer complimentary services their core customers already use—but they also have fintech startups standing at a crossroads. Will working a niche be sustainable in 2020 and beyond, or is becoming a jack of all trades the only means of survival?

Beware of Diluting the Brand

For starters, the only means of survival for any fintech company is to solidly define what the company brand is and what it stands for. For example, many small business lenders are deeply passionate about fueling the American dream through helping business owners unlock their financial potential. Supporting small business is key to our country’s economic fabric. Dynamism and the ability to recover from an economic downturn are both dependent on startups’ ability to grow quickly, and in most cases, the only way for them to do so is through access to capital. For a fintech lender to become a trusted brand to small business owners, it must remain devoted to them as a company that has the financial wellbeing and vitality of small businesses in mind. This means facilitating the right loan for them, right when they need it.

The key for fintech companies is to be careful about diluting the brand. When companies stray too far from what they are passionate about, their core audiences suffer. Tech giants enter new spaces every day, whether from R&D or acquisitions. A strong brand (and the loyalty its customers have to it) will not only insulate a fintech company from the tech giant threat, but make its mission and voice stronger by comparison. Think about this the next time you are eating at In-N-Out Burger (sorry, East Coasters!). The humble hamburger shop became a cultural phenomenon through its razor-sharp focus on simplicity, quality and consistency.

Always Consider the Human Factor

Innovation and automation are both critical to survival in the fintech space. But how much tech can a fintech leverage in its solutions to avoid becoming too niche? The answer lies in understanding the core customers’ needs and how much technology can be used to fulfill those needs. For an e-wallet app, the key needs of customers are frictionless payments and transfers happening in real time; it is not a solution (when it’s working) that needs a lot of human interaction. A fintech company such as this can use technology and machine learning to automate most of its services.

Conversely, the human factor is still a huge part of the equation in some fintech services. For example, a person’s livelihood is at stake when a small business takes on a loan or another capital solution for its growth needs. This is a very personal and consequential decision for a business owner. In fact, in the majority of cases, they don’t want to rely solely on a technology-powered platform to deliver the most appropriate loan options for their needs, not to mention address their specific concerns and questions. A fintech lender can leverage technology at every touchpoint to optimize the application and loan approval process; but ultimately, many business owners will desire interaction with a live representative, not a chatbot. The human factor is crucial in business lending, and something that could become lost as a result of brand dilution. While scalability is important, customer service is equally so.

In the end, the decision to offer niche services or to go wide will depend on what’s at the core of a fintech company. Indeed, the pressures to scale, grow and earn returns for investors are huge for any business, but decision-makers must keep their perspective on the market they serve and the problems they solve best. If expanded offerings and partnerships with other service providers enhance your brand and what it stands for, then this approach makes sense for growth and customer satisfaction. If not, then serving up the best grilled cheese sandwiches around, to the folks who really crave them, may well be the best path.

No Fees, Ever – Is Goldman Sachs Winning Or Losing The Online Lending Battle?

September 30, 2019 Peer-to-Peer lending in the United States died the day Goldman Sachs launched a rival online lending company in 2016. Armed with a low cost of capital and the trust of a household name, Marcus, as Goldman Sachs referred to themselves, sought to further disrupt consumer lending by eliminating every type of fee including late fees. Its pitch was simple, “No fees. Ever.” Three years later, the company still hasn’t caught up to competitors like Lending Club in origination volume (Marcus’ loan book is $5B vs. Lending Club’s $15B). Its fee-less model may also be backfiring.

Peer-to-Peer lending in the United States died the day Goldman Sachs launched a rival online lending company in 2016. Armed with a low cost of capital and the trust of a household name, Marcus, as Goldman Sachs referred to themselves, sought to further disrupt consumer lending by eliminating every type of fee including late fees. Its pitch was simple, “No fees. Ever.” Three years later, the company still hasn’t caught up to competitors like Lending Club in origination volume (Marcus’ loan book is $5B vs. Lending Club’s $15B). Its fee-less model may also be backfiring.

Goldman’s consumer lending business has racked up major losses, according to the WSJ. “It spent heavily to buy startups and cloud-storage space, hire hundreds of techies, and build call centers in Utah and Texas. Loans have gone bad at a higher rate than that of rivals.”

For all of the bank’s early bluster, they were so afraid of negative PR, that they launched without a collections department, leading to significantly high bad debt, the WSJ reports. That has since changed. But where Goldman Sachs appears to have lost, they may still be on track to win. As a consumer “bank” Marcus can also accept deposits. It had collected $36 billion as of year-end 2018 and added another $14 billion this year so far. Goldman also scored a valuable partnership with Apple on a branded credit card. The pitch is a familiar one, “No fees. Not even hidden ones.”

Apple promotes its card as “Created by Apple, not a bank,” yet The WSJ ironically reports that Goldman spent $300 million creating the card for Apple.

Apple promotes its card as “Created by Apple, not a bank,” yet The WSJ ironically reports that Goldman spent $300 million creating the card for Apple.

In a Q2 earnings call, Goldman CFO Stephen Scherr said that the bank was shifting its consumer lending focus from Marcus to the Apple Card. “I’d also say that if you look at the level and rate of growth in the Marcus loan business, while it continues to grow and perform well, we have slowed the increasing growth in that in contemplation of taking on increasing consumer credit through the card business,” he said. “What’s important for us is that we look at this on a risk-adjusted return basis not simply on a return on asset construct.”

Competitively, however, Scherr couldn’t answer if the consumer lending business’s costs will ultimately look more like a fintech lender or a bank as they scale. “What I can tell you is that what we have built jointly with Apple both on the front end and on the back end is intended to be operationally resilient, but equally is intended to be efficient both in terms of the application all through the delivery and on the back-end and so my expectation is that the efficiency will be reflected in that, but again premature to sort of put numbers around it.”

Of note is that Goldman acquired or acqui-hired from Clarity Money, Bond Street, and Final.

Up Next On The New York Legislative Agenda: Funder, Lender, and Broker Licensing

September 10, 2019 New York State Senator James Sanders Jr. has introduced S6688, a commercial financing licensing bill that would require persons or entities engaging in the business of making or soliciting commercial financing products in New York state to obtain a license from the New York Department of Financial Services. The bill covers small business lenders, merchant cash advance companies, factors, and leasing companies for transactions under $500,000.

New York State Senator James Sanders Jr. has introduced S6688, a commercial financing licensing bill that would require persons or entities engaging in the business of making or soliciting commercial financing products in New York state to obtain a license from the New York Department of Financial Services. The bill covers small business lenders, merchant cash advance companies, factors, and leasing companies for transactions under $500,000.

The bill likely won’t see any activity until the New York legislative session resumes in 2020, at which point it could be amended or killed.

As currently drafted, applicants for a license would be subject to a criminal background search and be required to submit their fingerprints for a review by agencies such as the FBI. In addition to paying an application fee, applicants would be required to maintain liquid assets of $50,000.

Sanders, the bill’s sponsor, is the Chairman of the banking committee. You can read the full text of the bill here.

Chinese Funder MYBank Using Advanced Tech to Provide Capital

August 1, 2019 MYBank, the largest non-bank funder in China, is using new technological systems to approve loan applicants. The company, which is backed by Alibaba founder, second richest person in China, and former English teacher Jack Ma, is now in its fourth year of operations and has thus far provided 2 trillion yuan ($290 billion) in funding to 16 million customers.

MYBank, the largest non-bank funder in China, is using new technological systems to approve loan applicants. The company, which is backed by Alibaba founder, second richest person in China, and former English teacher Jack Ma, is now in its fourth year of operations and has thus far provided 2 trillion yuan ($290 billion) in funding to 16 million customers.

Having partnered with Ant Financial Services, a payment processing company which Ma is also involved in, MYBank has received access to a host of data. In order to apply for a loan, SMB owners give access to their real-time payment records, and from the analysis of these, as well as the non-bank’s own risk-management appraisal system which runs through over 3,000 variables, a judgment is made as to whether or not to fund the applicant.

Ant also provides MYBank with other tech, such as facial recognition software to detect fraud, and aids them with their implementation of cloud-computing and big data. But as well as these methods is another system unique to China: social credit. Currently in its pilot stages, this national reputation system is set to rival traditional credit score systems. It works by increasing or decreasing a citizen’s rating based off whether they perform a good or bad action. Yell at someone unnecessarily on your commute? Your social credit scores lowers. Help an old woman cross the street? It’ll go up.

When discussing how the system could be implemented, MYBank President Jin Xiaolong gave the example of a small business owner who, upon forgetting to return a borrowed umbrella, finds it harder to get a loan. As well as this, Bloomberg reported in 2018 that a very poor social credit score could lead citizens to being barred from staying at luxury hotels, buying high-end real estate, and enrolling their children in elite schools. The flip side of this is that those with impeccable ratings will receive discounts when commuting, relaxed scrutiny when seeking financial aid, and priority when applying to schools.

Made possible by data-tracking tech, social credit scores appear to be almost revolutionary for the alternative finance industry. Partnered with the other technological tools available to MYBank, the company could experience previously unseen heights of successful loans. Or rather it does already, with default rates at approximately 1%.

Accessible via a few taps on a smartphone, MYBank’s application process takes 3 minutes and due to automation, customers are often instantly approved with funds being made available straight away. One customer described this shift in supply as “unimaginable” and praised how easy it now was to find capital as soon as he needed it.

MYbank also revealed Tuesday that it intended to raise $871 million at a valuation of approximately $3.5 billion.

The Industrial Hemp and CBD Industries, and the Potential Risks for Merchant Cash Advance Funders

June 22, 2019 Authored by Josh Herndon of Global Legal Law Firm

Authored by Josh Herndon of Global Legal Law Firm

It seems that we are constantly being bombarded by news of the growing industrial hemp and cannabidiol (more commonly known as “CBD”) industries. Indeed, industrial hemp (and products derived therefrom, such as CBD) is now legal, and these industries have experienced substantial growth that is expected to continue into the foreseeable future. As such, the businesses in these industries seem to be ideal candidates for merchant cash advances (an “MCA”, or “MCAs”), as such businesses seem more than capable of repaying an MCA.

However, businesses in the industrial hemp and CBD industries are still subject to federal law, and their ability to sell their product can be impacted by enforcement of federal law by federal agencies. MCA funders partnered with such businesses may be harmed by if those businesses are unable to generate the sales needed to repay MCAs. Nevertheless, the possibility of an enforcement action by a federal agency doesn’t mean that all activities in which a business in the industrial hemp and CBD industries could engage would be a violation of federal law. Indeed, there are industrial hemp-related and CBD-related business- activities that likely would not violate federal law.

In sum, MCA funders considering MCAs to businesses in the industrial hemp and CBD industries need to be aware of all risks associated with such MCAs before making an informed decision about whether to make such MCAs.

Background Regarding The Industrial Hemp And CBD Industries.

A fast-growing, sustainable and inexpensively produced plant, industrial hemp is a variety of cannabis sativa L. that contains less than 0.3 percent plant chemical delta-9 tetrahydrocannabinol (more commonly known as “THC”). Unlike marijuana (which, like industrial hemp, is derived from cannabis), which is cultivated to yield psychoactive THC, industrial hemp yields more than 25,000 oil and fibrous products that are embraced by farmers as a hedge against lower-value soy, cotton and alfalfa crops.

Industrial hemp was legalized late last year pursuant to the Agricultural Improvement Act of 2018 (also commonly known as the “Farm Bill”). Related thereto, production of industrial hemp skyrocketed in 2018, with 112,000 acres licensed for cultivation, 3,546 cultivation licenses issued, 78,176 total acres cultivated, and 40 universities conducting research.

Numerous products are derived from industrial hemp including CBD, which is an oil-based product that has uses as a nutritional supplement and food additive In fact, seventy-eight percent of all industrial hemp grown in 2018 was for CBD. The market for CBD has exploded, and is expected to continue exploding. According to the Brightfield Group, industrial hemp-based CBD sales hit $170 million in 2016, and it is anticipated that a 55% compound annual growth rate over the five years thereafter will cause the market for industrial hemp-based CBD to crack the billion-dollar mark.

In addition to legalizing industrial hemp, the Farm Bill also guarantees that industrial hemp and industrial hemp-derived products can be imported, exported and transported from state to state like any other crops. The Farm Bill also allows industrial hemp businesses to access insurance and banking.

The FDA And Its Role With Respect To The Industrial Hemp And CBD Industries.

Although the Farm Bill legalized industrial hemp, industrial hemp and CBD businesses do not have carte blanche to take whatever actions they want with respect to their products. That is because the United States Food and Drug Administration (the “FDA”) is responsible for protecting and promoting public health through controlling and supervising food safety, tobacco products, dietary supplements, prescription and over-the-counter pharmaceutical drugs, cosmetics, animal foods and feed and veterinary products.

The FDA has stressed that although industrial hemp is no longer an illegal substance under federal law, it will continue to regulate cannabis products under the Food, Drug, and Cosmetic Act (the “FD&C Act”) and Section 351 of the Public Health Service Act. That means that any cannabis product (such as CBD) that is marketed with a claim of therapeutic benefit, regardless of whether it is hemp-derived, must be approved by the FDA before it can be sold. In fact, the FDA has specifically cited deceptive marketing practices as one of its chief concerns, and it has clearly established that selling unapproved products with a therapeutic claim is unlawful.

The FDA has stressed that although industrial hemp is no longer an illegal substance under federal law, it will continue to regulate cannabis products under the Food, Drug, and Cosmetic Act (the “FD&C Act”) and Section 351 of the Public Health Service Act. That means that any cannabis product (such as CBD) that is marketed with a claim of therapeutic benefit, regardless of whether it is hemp-derived, must be approved by the FDA before it can be sold. In fact, the FDA has specifically cited deceptive marketing practices as one of its chief concerns, and it has clearly established that selling unapproved products with a therapeutic claim is unlawful.

The FDA has also confirmed that the addition of CBD to food products and dietary supplements is unlawful, even if the CBD is derived from industrial hemp. The FDA’s rationale is that CBD is an active ingredient in FDA-approved drugs, and its addition to the food supply and dietary supplements is illegal under the FD&C Act.

Recent FDA Actions Involving The Industrial Hemp And CBD Industries, And The Impact On Those Industries.

The FDA recently, and dramatically, showed how it will exercise its authority over industrial hemp and CBD products on March 28, 2019, when it (along with the Federal Trade Commission) issued warning letters to three businesses who sell CBD products alleging false, unfounded, unsubstantiated, and egregious health claims about (without sufficient evidence or FDA approval) their products’ ability to limit, treat or cure. The three businesses had advertised a range of CBD-containing supplements, and boasted the ability of those supplements to effectively treat diseases (including cancer, Alzheimer’s and fibromyalgia) and “neuropsychiatric disorders” in both humans and animals. The FDA threatened the three businesses with product seizures, injunctions and sales proceeds reimbursement.

The above actions by the FDA understandably sent shockwaves through the industrial hemp industry, and those actions underscore the risks faced by industrial hemp and CBD companies. For instance, virtually all CBD products that make health and wellness claims, or are deemed a food or drug, are potentially subject to scrutiny from the FDA because such products are mostly sold over the internet and enter the “stream of interstate commerce”. However, it is such health and wellness applications, and food and beverage infusion, that makes CBD and other oil-based hemp derived products attractive to the consumers who are the target market of CBD companies. As such, industrial hemp companies that sell CBD products almost inevitably invite FDA scrutiny as a result of their efforts to market their products to their customers, and potentially imperil their ability to sell their products to those customers.

The above actions by the FDA understandably sent shockwaves through the industrial hemp industry, and those actions underscore the risks faced by industrial hemp and CBD companies. For instance, virtually all CBD products that make health and wellness claims, or are deemed a food or drug, are potentially subject to scrutiny from the FDA because such products are mostly sold over the internet and enter the “stream of interstate commerce”. However, it is such health and wellness applications, and food and beverage infusion, that makes CBD and other oil-based hemp derived products attractive to the consumers who are the target market of CBD companies. As such, industrial hemp companies that sell CBD products almost inevitably invite FDA scrutiny as a result of their efforts to market their products to their customers, and potentially imperil their ability to sell their products to those customers.

A Cautionary Tale For MCA Funders.

Although the industrial hemp and CBD industries seem to be ideal markets for MCA as a result of their past and anticipated future growth, the recent actions of the FDA described above highlight the very real perils faced by businesses in those industries. At first glance, businesses in those industries seem to be ideal candidates for repaying MCAs because of what appears to be bountiful future sales. However, product seizures and/or injunctions ordered by the FDA obviously could prevent businesses in those industries from selling their product and generating receivables from such sales. An MCA funder partnered with such a business would obviously be harmed if the business couldn’t generate the receivables needed to repay an MCA.

Fortunately, there are circumstances under which businesses in the industrial hemp and CBD industries can likely operate without fear of an enforcement action by the FDA. For instance, the FDA allows cannabis and cannabis-derived products to be introduced into interstate commerce where it approves such products (such as with the FDA’s approval of Epidiolex, a seizure medication containing CBD, in 2018). Moreover, the FDA has identified three lawful hemp derivatives (including hulled hemp seeds, hemp seed protein, and hemp seed oil) that can be marketed legally as long as they are not promoted with a therapeutic claim.

Based on the above, the circumstances under which an MCA funder should, or should not, make an MCA to a business in the industrial hemp and CBD industries can be very confusing. MCA funders need an insight into the industrial hemp and CBD industries, and the very real risks faced by those industries as described above, before making MCAs to businesses in those industries.

Fortunately, competent legal counsel versed in the MCA industry, as well as the industrial hemp and CBD industries, can provide such insight, and legal advice related thereto. As a practical matter, an MCA funder should not make an MCA to a business in the industrial hemp or CBD industries without first getting advice from such legal counsel so that the MCA funder can fully understand the risks involved in making such an MCA, and the circumstances in which such an MCA should, or should not, be made.

Bio

Mr. Herndon is an attorney at the Global Legal Law Firm, whose attorneys are well recognized as top industry experts. Mr. Herndon works in the compliance field helping electronic payment processing companies avoid getting fined, arrested, violate rules, or get sued from internal or external threats. Mr. Herndon is also involved in litigation in the payments space, including defending and pursuing electronic payments companies.