Patreon Adds MCA-like Product With Patreon Capital

February 20, 2020 Patreon, the membership platform that provides payment and subscription services for creators, will now start funding those artists that are on its site through Patreon Capital. Said to be modeled after Shopify Capital, the service will be available to certain creators initially, with Patreon reaching out directly to them to offer merchant cash advances.

Patreon, the membership platform that provides payment and subscription services for creators, will now start funding those artists that are on its site through Patreon Capital. Said to be modeled after Shopify Capital, the service will be available to certain creators initially, with Patreon reaching out directly to them to offer merchant cash advances.

The move comes after CEO Jack Conte had been quoted in January saying that “The reality is Patreon needs to build new businesses and new services and new revenue lines in order to build a sustainable business.”

It seems like this new service is part of a trend that has overtaken tech companies recently, best exemplified by the Apple Card, wherein established players, worried about longevity, are moving further into financial services, hoping to get long-lasting hooks into their customers.

Historically, Patreon has made money by taking a 5% cut from the subscription payments made to artists on its platform, with a further 5% going towards covering transaction fees, and the remaining 90% being left for the artist, who retains complete ownership of their work. It currently has over 100,000 creators on its site and over three million active monthly users. Contributions begin at $1, with content being unlocked in exchange for payment. Thus far, Patreon has paid out over $1 billion.

It has been reported that about a dozen deals have been made between creators and Patreon Capital so far. Hot Pod News ran a story featuring one such case, in which Multitude, a Brooklyn-based podcast studio, disclosed that it took funding of $75,000 over two years in order to pay the SAG-AFTRA rates of the actors it wanted to employ for a new audio sitcom titled Next Stop.

“We were running into this problem where we have a ton of great ideas, but because we’re a small business, we constantly have to decide between putting money towards paying our people and getting more equipment versus saving it up for a bigger project,” Multitude’s CEO, Amanda McLoughlin, told Hot Pod.

The premium attached to the financing was not revealed, however Multitude did note that the revenues of one of the studio’s other shows, Join the Party, would be taken as collateral if Next Stop is not profitable enough to pay the premium after two years.

“This arrangement is directly tied to the fact that we have successful podcasts making money on Patreon, and that we’ve already invested in the Patreon system to pay this stuff back,” comment Eric Silver, Multitude’s Head of Creative, underlining how Patreon Capital is linked with the analytics of Patreon’s base service. Much like how Amazon uses sales metrics and user data to gauge which retailers to lend to on its own marketplace, Patreon appears to be making use of seven years of data on its creators to determine who is best positioned to receive funding.

“Patreon has access to all the data about a creator’s earnings history, what they offer as benefits, how much they engage with their patrons … everything needed to forecast their earnings and retention, without a creator even needing to submit an application.” Patreon VP of Finance Carlos Cabrero stated. “This would be essentially impossible for a bank to replicate.”

Shopify Capital Originated $430 Million in Loans and MCAs in 2019

February 17, 2020 Shopify Capital, the e-commerce giant’s small business financing arm, originated $430 million in funding through loans and merchant cash advances in 2019. Shopify now has more than 1 million e-commerce merchants on its platform, the company says. Earlier in the year the company began rolling out funding to merchants that are not using its payment service.

Shopify Capital, the e-commerce giant’s small business financing arm, originated $430 million in funding through loans and merchant cash advances in 2019. Shopify now has more than 1 million e-commerce merchants on its platform, the company says. Earlier in the year the company began rolling out funding to merchants that are not using its payment service.

Though 2019 year-end reporting for the industry is still sparse, the company’s origination figures will likely cause Shopify to move up the rankings maintained by AltFinanceDaily.

PayPal, who AltFinanceDaily predicts will keep its #1 spot, did not disclose its annual origination figures in its already-reported Q4 earnings.

The Scoop Behind Sprout Funding’s Acquisition of Jet Capital

January 25, 2020 News from North Texas this month as Dallas-based Sprout Funding announced its acquisition of Jet Capital. The move comes as Sprout seeks to expand its technical operations.

News from North Texas this month as Dallas-based Sprout Funding announced its acquisition of Jet Capital. The move comes as Sprout seeks to expand its technical operations.

“Sprout built a reputation as a group that funds a lot of its own internal deals, and Jet had spent a lot of time, energy, and money on their tech platforms,” Sprout’s CEO and Founder Brad Woy told AltFinanceDaily. “So while we were really good on the sales and marketing side, they seemed to be a little bit more advanced in their tech and reporting, and we brought those two things together.”

Almost all of Jet’s employees will be joining Sprout, with the exception of one person who chose to go their separate way following the merger.

Jet’s COO Allan Thompson spoke kindly of the purchase, saying in a statement that “There is a great cultural alignment in addition to the obvious benefits of combining our technology, processes and people. The result will provide increased capabilities for Sprout and opportunity for all of our customers and partners.”

The financial terms of the acquisition were not disclosed.

The Scoop Behind The Primary Capital / Infinity Capital Funding Acquisition

January 6, 2020 This morning, Primary Capital announced that it had acquired the merchant cash advance division of Infinity Capital Funding. Infinity, which has been operating from California since 2006, began as an MCA company before expanding to offer small business loans as well. The acquisition will see Infinity’s thirteen years of data, technology, and merchant portfolios pass onto Primary.

This morning, Primary Capital announced that it had acquired the merchant cash advance division of Infinity Capital Funding. Infinity, which has been operating from California since 2006, began as an MCA company before expanding to offer small business loans as well. The acquisition will see Infinity’s thirteen years of data, technology, and merchant portfolios pass onto Primary.

Speaking on the acquisition, Primary Capital Managing Member David Korchak said that “anything that you can acquire with that much time behind it and that much experience behind it is excellent, and for us with what we’re trying to do it’s tremendous. It’s a big, massive help for us.”

As well as the intangible assets that will be conferred to Primary, Isaiah Kenigsberg will be joining their team. Having served as Infinity’s Financial Controller, Kenigsberg is now CFO at Primary.

The decision to acquire Infinity’s book came after Primary noticed that it was winding down its MCA operations, Korchak told AltFinanceDaily. Seeing the value in obtaining such a trove of data proved too enticing to pass the Managing Member said, and Primary has been digging into the information obtained for the last three months.

For Korchak, something that has stood out from this analysis is the patterns that have emerged in the portfolio. “The thing that’s remarkable for these companies that have been around as long as them, is everyone seems to have clients that have taken 30 advances from them. They have clients that started back in ’07, ’08, that are still active merchants which is remarkable.

“The only difficulty is trying to analyze and say, ‘Why is this merchant after 30 different cash advances over a 12-year period still taking cash?’ And that’s really our model. And our goal for this year is to try and help subprime borrowers get out from having to take toxic debt like cash advances for their business. Ultimately, the data that we’re acquiring from ICF and this acquisition is going to help us study a lot of the transitions that MCA merchants have made since the beginning and see which ones have actually been able to get out of it.”

Asked whether there are any more acquisitions in the pipeline, Korchak responded, “Absolutely, we’re heavily data and service-driven for this year specifically, and we have a lot more to come.”

How GRID Finance’s Cash Advances Are Building Stronger Irish Communities

December 27, 2019

Five years ago, a small company in Dublin put Ireland’s fintech scene on the map by advising local SMEs to “get on the GRID.” GRID Finance, founded by Derek F Butler, introduced a peer-to-peer lending model to Irish businesses at a time when the industry was just beginning to form. From the beginning, the company’s secret sauce was the GRID Score, a proprietary credit score system that enabled the company to take on the difficult task of assessing the risk of SMEs.

Butler, who I sat down with in September at the company’s headquarters alongside Chief Marketing Officer Andrea Linehan, says the GRID Score is an SME’s “passport to the economy.”

It’s the upper tier that GRID caters to while providing a unique product within Ireland known as a cash advance. The setup is similar to Square and PayPal in the US in that the loans are repaid via a percentage of an SME’s credit/debit card transactions on a daily basis. The term of the loan is fixed and the costs are reasonable.

“The reality is that small business funding and financing is a high risk,” Linehan says.

“There’s no subprime market here,” Butler adds. “We’re trying to build a prime cash advance market versus a subprime one in the US.”

Like GRID’s competitors in the industry, Linehan believes that finance in Ireland will transition online. “Ireland is still dominated by two banks,” she says, referring to Bank of Ireland and AIB. The company, therefore, believes it has a good head start on the impending shift. But in the meantime, they’ve learned how important it is to be embedded in the local communities. To that end, GRID has an office in Limerick, Ireland’s third largest city with 95,000 people that’s located about 200km away from its headquarters in Silicon Docks.

Like GRID’s competitors in the industry, Linehan believes that finance in Ireland will transition online. “Ireland is still dominated by two banks,” she says, referring to Bank of Ireland and AIB. The company, therefore, believes it has a good head start on the impending shift. But in the meantime, they’ve learned how important it is to be embedded in the local communities. To that end, GRID has an office in Limerick, Ireland’s third largest city with 95,000 people that’s located about 200km away from its headquarters in Silicon Docks.

And their mission goes beyond providing funds. “If we can help get [SMEs] ready by giving them the tips to improve their financial health right now, let’s try and do that,” Butler says. “We want them to understand their financial health versus their cost of capital.”

While the company has sustained modest growth, Business Post reported earlier this month that GRID plans to raise €100 million in 2020 to provide even more loans through its platform.

Butler likens GRID’s mission to the MetLife Foundation, promoting financial health and building stronger communities. “We do a lot of work with the MetLife foundation because of the impact they have,” he says. “It’s why I launched GRID Finance.”

Merchant Cash Advance Valuation Dynamics

November 20, 2019Understanding the differences in cashflow dynamics between small business loans and MCAs is crucial for investors when valuing these alternative investments. A small business loan usually has familiar terms such as a principal amount that is paid back with interest over time, typically with a monthly payment schedule. An MCA agreement does not have these terms. Instead, the merchant agrees to sell a certain percentage of future revenues generated by the business, up to a specified “Purchased Amount,” to the funder in exchange for a lump sum of cash (the “Funded Amount”). MCAs often have an initially agreed-upon dollar amount that is debited daily by the funder via ACH. However, merchants have the ability to reconcile the total debited at the end of each month based on their actual sales activity and the agreed-upon percentage. If the merchant’s sales are slower than projected, the MCA company owes the merchant back a portion of the month’s debits to be in line with the contractual percentage of sales, and the daily ACH amount may be adjusted.

The preferred approach for valuing MCAs is discounted cashflow analysis. Given the nuances of MCA cash flow dynamics, modeling should be done individually for each MCA. Projections should be modeled using assumptions that are supportable from historical data and the methodologies used should be transparent. This modeling should incorporate not only the cash flow from the merchant, but also the cash flows arising from deal mechanics such as commissions paid, origination fees and ongoing fees as well as expected charge-offs. Since the funder cannot know for certain which merchants will realize revenues higher or lower than projected or default when underwriting the MCA, any attempt at an accurate projection of future cash flows must incorporate probabilities for scenarios where the timing and amount of cash flows is different than the underwritten scenario. Because businesses in a particular sector may have similar historical cash flow behavior, each MCA should be analyzed based on the historical experience of MCAs with similar characteristics such as business type, advance amount and purpose for taking out the MCA. A smaller but related issue is incorporating the probability that the merchant chooses to pay off the Purchased Amount via a lump sum payment and negotiates a discount to the Purchased Amount.

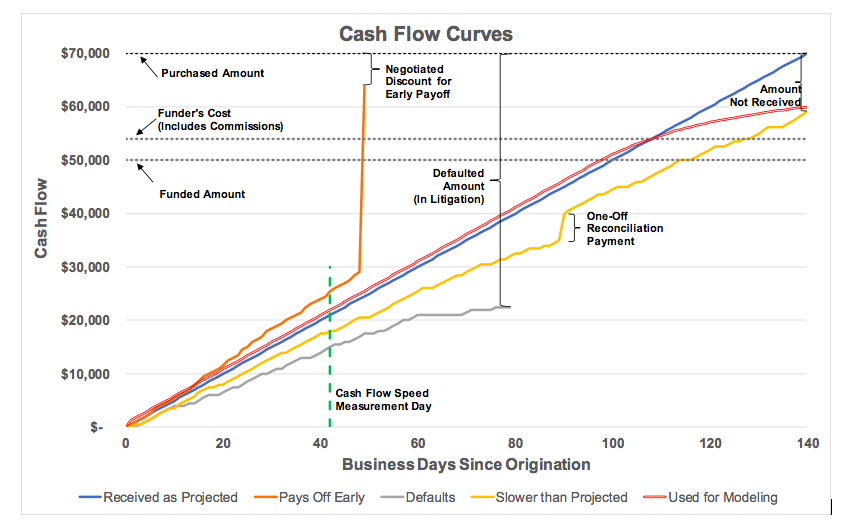

Examining payment behavior involves creating payment curves that compare the cash flow received at each point in time, expressed as a percentage of the Purchased Amount, to the cash flow projected to have been received at that time during underwriting. This curve is the “Cash Flow Curve,” and its steepness is the “Cash Flow Speed.” More specifically, the Cash Flow Speed is the cash flow received to date divided by the cash flow projected to be received as of that date during underwriting. A perfectly underwritten MCA would be one on which no reconciliations are made and each daily ACH goes through without issues, meaning that all of the Purchased Amount was received exactly as originally projected, and its Cash Flow Speed would be 100.0% every day. As with most things, this does not work in practice like it does in theory. Some merchants will have ACHs which fail, make additional payments to make up for failed ACHs, renegotiate the daily ACH amount as part of a reconciliation or after a failed ACH, turn off ACH completely or have other issues. Analyzing the Cash Flow Curve for each MCA and comparing it to its cohort is essential to understanding performance drivers when projecting future cash flows.

To illustrate a possible MCA agreement, assume a merchant sells $70,000 of future sales (the Purchased Amount) to the funder for $50,000 (the Funded Amount). The Purchased Amount is to be received via ACH daily, with $500 debited per day for the next 140 business days based on projected revenues. In this example, the Gross Factor is 1.40, i.e. $70,000 divided by $50,000. Assuming that the funder pays a commission of 8% of the Funded Amount, the Funder’s Cost is $54,000, and the Net Factor is 1.30, i.e. $70,000 divided by $54,000. The graph below illustrates some possibilities of what the actual Cash Flow Curves might be.

Received as Projected: depicts an MCA where debits via ACH are received each day, and the ACH is unchanged until the full Purchased Amount is received. Its Cash Flow Speed at the measurement day (and every day) is 100.0%.

Pays Off Early: depicts an MCA where the merchant elects to send additional cash flow to the funder, eventually negotiating to pay off the MCA early after 49 business days with a discount to the Purchased Amount negotiated with the funder. Its Cash Flow Speed at the measurement day is 121.4%.

Defaults: depicts and MCA where the ACH debit fails with increasing frequency until the bank account is closed and the funder takes the merchant into litigation for the remaining Purchased Amount (the “Defaulted Amount”). Note that the funder may be entitled to recoup amounts beyond the Defaulted Amount in litigation. Its Cash Flow Speed at the measurement day is 71.4%.

Slower than Projected: depicts an MCA where ACH fails sometimes, but the merchant does not shut down and the funder receives cash flow slower than projected. An example of a one-off reconciliation payment is included, assuming the merchant had not been paying in accordance with the contract and agreed to make a “catch-up” payment. After 140 days only $59,000, or 84.3% of the $70,000 Purchased Amount, has been received, although the funder would likely still expect to recoup most or all of the remaining Purchased Amount. Its Cash Flow Speed at the measurement day is 85.7%.

Used for Modeling: When analyzing this MCA on day 0, before any cash flow behavior is known, each of these possibilities (as well as others) would be incorporated into the analysis on a probability-weighted basis. An example of a probability-weighted average Cash Flow Curve is shown. After 140 days 85.7% of the Purchased Amount has been received, although cash flow is assumed to continue to be received until 210 days (150% of the underwritten projection), with 90.3% of the Purchased Amount received by then. Its Cash Flow Speed at the measurement day is 104.6%.

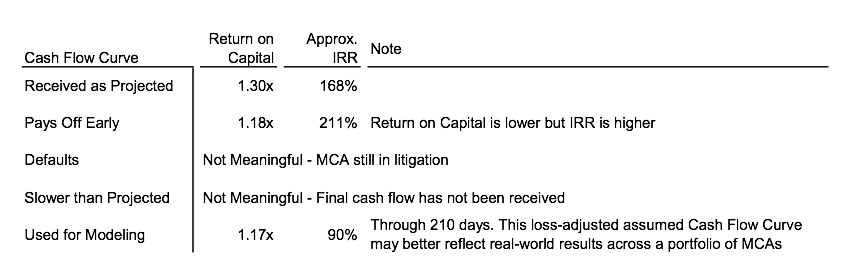

Based on the Funder’s Cost, the chart below shows some return metrics based on these Cash Flow Curves.

As the industry matures and attracts more capital from institutional investors, it is increasingly important to have clearly defined metrics in place to evaluate underwriting effectiveness, assess relative credit performance of originators or cohorts of MCAs, and to perform valuations. Standardizing on terms such as Funded Amount, Purchased Amount, Gross Factor, and Net Factor and concepts such as Cash Flow Curve and Cash Flow Speed should ease the understanding of MCAs by eliminating ambiguity amongst various participants in the industry.

Shopify Capital Originated $141M Of Loans And MCAs In Q3, Says It’s a Meaningful Part Of The Shopify Business

October 29, 2019Shopify Capital, Shopify’s small business funding division, originated $141 million in loans and merchant cash advances last quarter, an 85% increase over Q3 last year.

The company has now cumulatively originated $768.9M since it began funding in April 2016.

On the earnings call, Shopify COO Harley Finkelstein commented on the company’s recent initiative to fund non-Shopify payment merchants by saying that “while it’s still early, we’re seeing strong adoption from those merchants.”

“We started Shopify Capital to help solve another playing field for entrepreneurs, access to capital to grow their businesses,” he explained. “This is especially true as merchants gear up for their busiest selling season of the year.”

When asked about how funding would play a role in the company’s long term expansion and retention plans, Finkelstein said the following:

[P]art of this is making sure that we have merchants in the entirety of their journey to success, certainly things like having additional cash for things like inventory and marketing are very important to them. And there’s not too many place to get that with capital. So we think we’re helping merchants by doing this. It also serves of course as a way to retain merchants because we’re not only now their e-commerce platform or the point sale provider or the payments provider, we’re also now in some cases playing the role of their capital provider.

So this is a meaningful part of our business, and it keeps growing, and it’s certainly something we’re very proud of. And in terms of managing the risk, it’s something we keep a close eye on. We do a ton of trade forecasting and ensuring that we look at the data to update our models as we see trends changing. That being said, it’s important to remember that most of the capital that we put out there is insured by our partner EDC.

So we think that we continue to grow the capital business at the same time manage the risk and so we’re not doing anything that is outside of that loss ratio and risk exposure comfort zone that we think we have right now.

Shopify CEO Tobi Lutke later added how their Capital division adds to their Gross Merchandise Value (GMV) because merchants use funds to build their businesses.”What happens is a lot more businesses, that otherwise would not have access to loans get them and therefore actually continue building their business.”

CAN Capital Announces New CCO

October 15, 2019We are proud to announce that we have hired David Lafferty as CAN Capital’s new Chief Credit Officer (CCO.) Lafferty brings his expertise in commercial lending, business development, operational planning and profit & loss management to the CAN Capital team.

Lafferty has over twenty years of proven experience providing financial services to small businesses. He is the former Vice President of Capital Markets and Credit and Risk Management at Marlin Business Bank. In that role, he has assisted small businesses in obtaining the capital they need to operate and grow, with a special focus on helping businesses finance the lease or purchase of equipment. Lafferty is a graduate of Pennsylvania State University, and a member of the Equipment Leasing and Financing Association (ELFA) Small Ticket Advisory Council.

“I have focused my entire career on serving the small business owner as they are the backbone of the United States economy. Being given the opportunity to join this team in a time when the company is experiencing rapid growth and gaining significant market share is extremely exciting. I am really looking forward to joining an already very talented workforce as we take CAN Capital to the next level,” said Lafferty.

Ed Siciliano, CAN’s CEO, had this to say about the new hire: “I’m very excited to welcome Dave to CAN Capital. He will be joining a strong group of talented people focused on Risk and Credit Underwriting and applying his deep experience in small business lending to calibrate CAN’s 20-year proven credit models. We all welcome Dave and feel fortunate to have him join.”

A Philadelphia native who now resides in New Jersey, Lafferty is the proud father of twin sons. When he isn’t helping small businesses succeed, you’ll find Lafferty golfing or riding motorcycles, or on the water boating and fishing in Punta Gorda Isles, Florida.

Please join us in welcoming new CCO David Lafferty, who, along with our dedicated group of CAN Capital team members, is ready to support our mission of helping every small business succeed.

About CAN Capital

CAN Capital, Inc., established in 1998, is the pioneer in alternative small business finance, having provided access to over $7 billion in capital for over 81,000 small businesses in a wide range of locations and different business types. As a technology powered financial services provider, CAN Capital uses innovative and proprietary risk models combined with daily performance data to evaluate business performance and facilitate access to capital for entrepreneurs in a fast and efficient way.

CAN Capital, Inc. makes capital available to businesses through business loans made by WebBank, member FDIC, and through Merchant Cash Advances made by CAN Capital’s subsidiary CAN Capital Merchant Services, Inc. ©2019 CAN Capital. All rights reserved

Media Contact: Carey Kirk, 678-858-6911, ckirk@cancapital.com